From Ambition to Realisation: A Vision for Germany’s Decarbonisation

Executive Summary

Germany has made significant efforts toward achieving net-zero emissions and has markedly progressed in transforming its energy system. This success relies heavily on the expansion of renewable energy and enabling infrastructure. However, as weather-dependent renewable capacity grows, Germany increasingly faces periods of both energy surplus, when conditions are favourable, and scarcity. This energy paradigm brings new challenges that require thoughtful solutions.

Now Germany stands at a pivotal moment in its transition to net-zero emissions. As policymakers explore a broader range of technology-based solutions, this report presents a vision for an options-based energy portfolio that enhances reliability and resilience, extending beyond the current focus to ensure Germany’s economy remains competitive in the new geopolitical context. An options-based portfolio that includes deployment of a wide range of technologies (such as wind, solar, carbon capture and storage, zero-carbon fuels, superhot rock geothermal energy, and nuclear energy) offers a reliable, cost-effective, and safe energy supply for Europe’s largest economy.

The report is based on the findings of the accompanying study, “Power System Expansion in Germany,” by Quantified Carbon for Clean Air Task Force (CATF). The study aims to enhance the existing body of evidence from previous studies tailored to the German context and is among the first to incorporate nuclear power into the country’s power system technology portfolio.

The modelling included in this study demonstrates that without a technology-inclusive energy policy, Germany risks missing its climate targets and undermining its economic competitiveness. The study also underscores the benefits of embracing an options-based portfolio — one that leverages a diverse range of technologies, which would result in:

- The lowest total system costs;

- The lowest average electricity price and lowest price volatility;

- The lowest dependence on transmission infrastructure and the fewest new transmission lines;

- The lowest relative use of land and critical minerals; and

- A system that is best equipped to navigate uncertainties.

CATF advocates for an options-based approach to decarbonisation for hedging risks against relying on a single solution. Earlier mentioned power system optimisation study corroborate this assumption: results indicate that a technology-open approach and rapid acceleration of power system development are necessary to meet decarbonisation and energy reliability goals at lowest cost. Although Germany recently phased out all remaining nuclear energy plants, nuclear energy can make a valuable contribution to decarbonisation of the electricity system as well as selected industrial applications and district heat. CATF encourages Germany to reconsider its position on nuclear energy, given the technology’s benefits, but recognises current barriers may prevent such a move.

Based on findings from the underlying study and CATF’s track record in advancing energy systems, CATF recommends the German government prioritise the following actions:

1. Power System Strategy1

- Action 1. Establish a technology-inclusive framework.

- Action 2. Restart nuclear plants and establish frameworks for new nuclear energy.

- Action 3. Facilitate carbon capture on natural gas plants.

- Action 4. Promote long-duration energy storage as an alternative to other less cost-effective options.

- Action 5. Reinforce transmission grid expansion.

- Action 6. Transition away from coal while enabling acceleration of solar, onshore wind, and offshore wind deployment.

2. Clean Hydrogen Deployment

- Action 1: Prioritise hydrogen for the decarbonisation of industry and transport.

- Action 2: Focus on clean — not green — hydrogen production.

- Action 3: Conduct a realistic assessment of hydrogen imports.

3. Carbon Capture and Storage Deployment

- Action 1: Harness Germany’s CO₂ storage potential and coordinate efforts.

- Action 2: Advance CCS projects by providing financial security.

4. Methane Mitigation

- Action 1: Systematically set goals, monitor progress, and report outcomes.

- Action 2: Incentivise lower-emission livestock and manure management.

- Action 3: Implement the European Union (EU) Methane Regulation and monitor abandoned wells.

- Action 4: Ensure consistent application of the EU Methane Regulation.

5. Fusion Demonstration

- Action 1: Establish a legal framework to ensure certainty for investors and developers.

- Action 2: Foster public-private and intergovernmental collaboration.

6. Superhot Rock Energy Demonstration

- Action 1: Expand the geothermal energy strategy to include superhot rock energy.

- Action 2: Foster EU-wide collaboration on research and deployment.

Section 1: Why Germany Needs an Options-Based Climate and Energy Strategy

Germany has a stable foundation to transition its economy toward net-zero emissions.

| Climate Awareness | In Germany, more than one million people — the greatest number in any country worldwide — participated in the global climate strike in September 2019. CATF’s polling from 2023 found that, among the six surveyed European countries, respondents from Germany had the highest climate awareness, with nearly a third consuming climate news daily. More than 50 firms demanded higher investments in climate neutrality in an open letter to politicians in January 2024. More recently, in March 2025, 50 companies called for a transformation to climate neutrality. Even if climate change has recently been overshadowed politically by other pressing issues (such as economic competitiveness, migration, or security) and marked by some polarisation, the underlying awareness and concern remain present among both citizens and businesses. |

| Economy & Innovation Made in Germany | Despite recent economic slumps, Germany is one of the 11 countries with a triple A rating in credit-worthiness, resulting in low capital costs for loans. More than a quarter of Germany’s gross value-added stems from its industry — 8% more than in the U.S., for example. Its manufacturing sector employs 7.5 million people, nearly 12% of the population. of the population. As the third biggest exporting nation, Germany is one of the key players in the global economy. It is also one of the most innovative countries in the field of climate research, with the highest number of climate tech startups in the EU. Numerous highly efficient climate tech solutions are created every year at German universities, research societies, and leading frontier research organisations on climate technology such as the Karlsruhe Institute of Technology, the German Aerospace Center, and the Jülich Research Center. |

| Progress on Renewables | Germany’s Erneuerbare Energien Gesetz (Renewable Energy Sources Act), introduced in 2000 to support domestic renewable energy expansion, helped drive global solar industry growth by boosting demand. Today, renewable energy makes up over 60% of its produced electricity. While other countries have caught up in recent years, Germany still has the fifth-highest installed renewable energy capacity worldwide, just behind China, the U.S., Brazil, and India, countries with significantly larger land mass. |

Despite these favourable conditions, Germany has faced difficult times and a weak growth outlook. The energy crisis after Russia’s invasion of Ukraine has made clear that Germany has been overly reliant on unabated fossil fuels — endangering its energy security, exposing its industry to volatile prices, and preventing its energy system from decarbonising. Additionally, whilst Germany has been pursuing an ambitious renewable energy agenda, its decarbonisation, energy reliability, and security efforts have been hindered by an accelerated phase-out of nuclear power, resulting in higher consumption of emission-intensive coal and gas and counteracting progress made in deploying solar and wind generation.

Germany now faces both opportunities and challenges as it pursues its transition toward net-zero emissions. While prioritising climate action was once prominent in public discourse and policy debates, recent elections have demonstrated a significant shift: economic concerns and energy security are taking precedence over climate action for many citizens. This changing landscape requires a pragmatic reassessment of how decarbonisation efforts are framed and implemented. Despite recent economic headwinds and slower growth, Germany retains considerable industrial strength and technical capabilities that can be mobilised for transformation. And although its ambitious plans for wind and solar expansion face implementation hurdles, they still provide a foundation upon which to build and complement with clean firm power.

What is now critical is transforming Germany’s decarbonisation journey into a win-win proposition that addresses immediate economic concerns while positioning the country for future competitiveness. Doing so means pursuing a diverse portfolio of technological options rather than a single pathway, embracing innovation across multiple fronts, and maintaining flexibility as technologies mature at different rates. By adopting this options-based approach, Germany can develop solutions that simultaneously reduce emissions, create economic value, and enhance energy security — ensuring that its climate ambitions remain achievable even as political and economic conditions evolve.

Germany consumed 465,500 GWh of energy in 2024 alone. However, as sectors such as industry, transport, and heating undergo increasing electrification, power consumption is forecast to increase. While Germany remains committed to its climate goals, the focus has moved toward practical implementation challenges, particularly grid expansion and cost containment. A pathway dominated by weather-dependent wind and solar faces land use constraints, and social acceptance of those technologies is shifting in some areas. Meeting the dual challenges of maintaining a reliable, affordable power supply while decarbonising the economy will require a pragmatic assessment of all available technologies and their contributions to a 24/7 clean and reliable power grid. To this end, Germany needs to evolve its electricity decarbonisation strategy from one focused solely on renewable deployment to one that aims for 24/7 carbon-free energy — meaning that every kilowatt-hour of electricity consumption would be met with carbon-free electricity sources, every hour of every day, everywhere. Such a strategy would consider realistic infrastructure buildout speed or scale constraints and mitigate them by considering more technology solutions. A key enabler of a reliable, secure, and clean energy system with a variety of generation types is a robust transmission network. However, in recent years, the slow growth of the transmission grid has highlighted the challenges in overcoming barriers to infrastructure deployment, making the transmission system itself a bottleneck in the clean energy transition. Public acceptance is declining, and processes remain slow even with new laws aimed at acceleration. Germany currently operates approximately 37,000 km of transmission lines and is projected to require significant additional capacity by 2045. Estimates of investment required for these expansions are substantial, suggesting that transmission system operators alone will need to invest around €320 billion by 2045.

Even if future consumption assumptions are revised downward, it would not eliminate the long-term need for a robust grid. It may buy some time, but due to the complete reorganisation of energy production, existing transmission assets will still need to be upgraded — regardless of which generation technologies dominate. Upgrades include incorporating digital and innovative technologies and developing the smart grid, among others. Grid expansion should therefore be pursued as efficiently as possible, guided by an option-based and technology-open approach. And while storage can counterbalance fluctuations of renewable energy production, storage durations remain relatively short, and costs continue to pose a significant barrier.

Beyond the power sector, decarbonising Germany’s industry and transport will be critical — and even more complex. These sectors account for a large share of emissions, and many of their processes are difficult to electrify. Heavy-duty transport modes such as trucking, shipping, and aviation require high-density energy carriers. Key industrial processes, from steel and cement to chemicals, depend on high-temperature heat and carbon-intensive feedstocks.

Clean hydrogen will play an important role in decarbonising these sectors as an energy carrier and a feedstock, but its production is energy-intensive. Meeting projected hydrogen demand through electrolysis would require a near-quadrupling of Germany’s electricity supply, based on the Monitoring Report 2024 of the Expert Commission on Energy Transition Monitoring. Even with full reliance on wind and solar, producing the materials needed for clean infrastructure, like green steel for wind turbines, requires industrial transformation and access to reliable, low-emission power. Moreover, industrial competitiveness increasingly depends on the ability to supply low-carbon products, especially as global markets adopt carbon border adjustment mechanisms. Emission costs are becoming a defining factor in production economics — and access to affordable, firm, clean energy is a prerequisite for protecting jobs and attracting investment.

Taken together, these challenges make clear that a credible, future-proof energy strategy for Germany must be diverse, combining clean firm power and a portfolio of solutions such as carbon capture, zero-carbon fuels, and innovative technologies. Only by keeping multiple options in play while supporting the next generation of clean technologies can Germany reduce risk, maintain industrial strength, and ensure that its decarbonisation pathway remains both resilient and achievable.

This options-based approach is not just a theoretical concept; it is backed by robust system modelling. The following section outlines new analysis exploring how different technology pathways affect the cost, reliability, infrastructure needs, and emissions performance of Germany’s future power system. The results demonstrate that a diversified portfolio of clean technologies not only delivers the most secure and affordable route to net-zero, but also reduces exposure to infrastructure bottlenecks, land-use constraints, supply chain risks, economic volatility, and, ultimately, the risk of failure of any single technological pathway.

Section 2: Modelling Germany’s Net-Zero Power System

Technology optionality promises the lowest and most-reliable net-zero energy system strategy for Germany. To exemplify the costs of different power systems, CATF commissioned a study from Quantified Carbon to explore pathways to attaining a fully decarbonised German power system by 2050.

- Methodology

The study utilised 60 carefully crafted scenarios — including custom geospatial analysis of the technical potential of wind and solar and grounded assumptions for demand-side flexibility — to showcase varying projections related to crucial technology developments. These scenarios encompass optimistic and conservative viewpoints on parameters such as investment costs, commodity prices, maximum expansion potential, and build rates. With an emphasis on energy resilience, this methodology integrates investment and dispatch optimisation, relying on a comprehensive set of 33 historical weather years to ensure the construction of reliable power systems with realistic dispatch schedules and electricity prices. The robustness of the results in the technology pathways was thoroughly evaluated through explorations of around 60 scenario variations. Here, we summarise the results from four central scenarios (Table 1). For more information on the methods, please refer to the study.

- Results

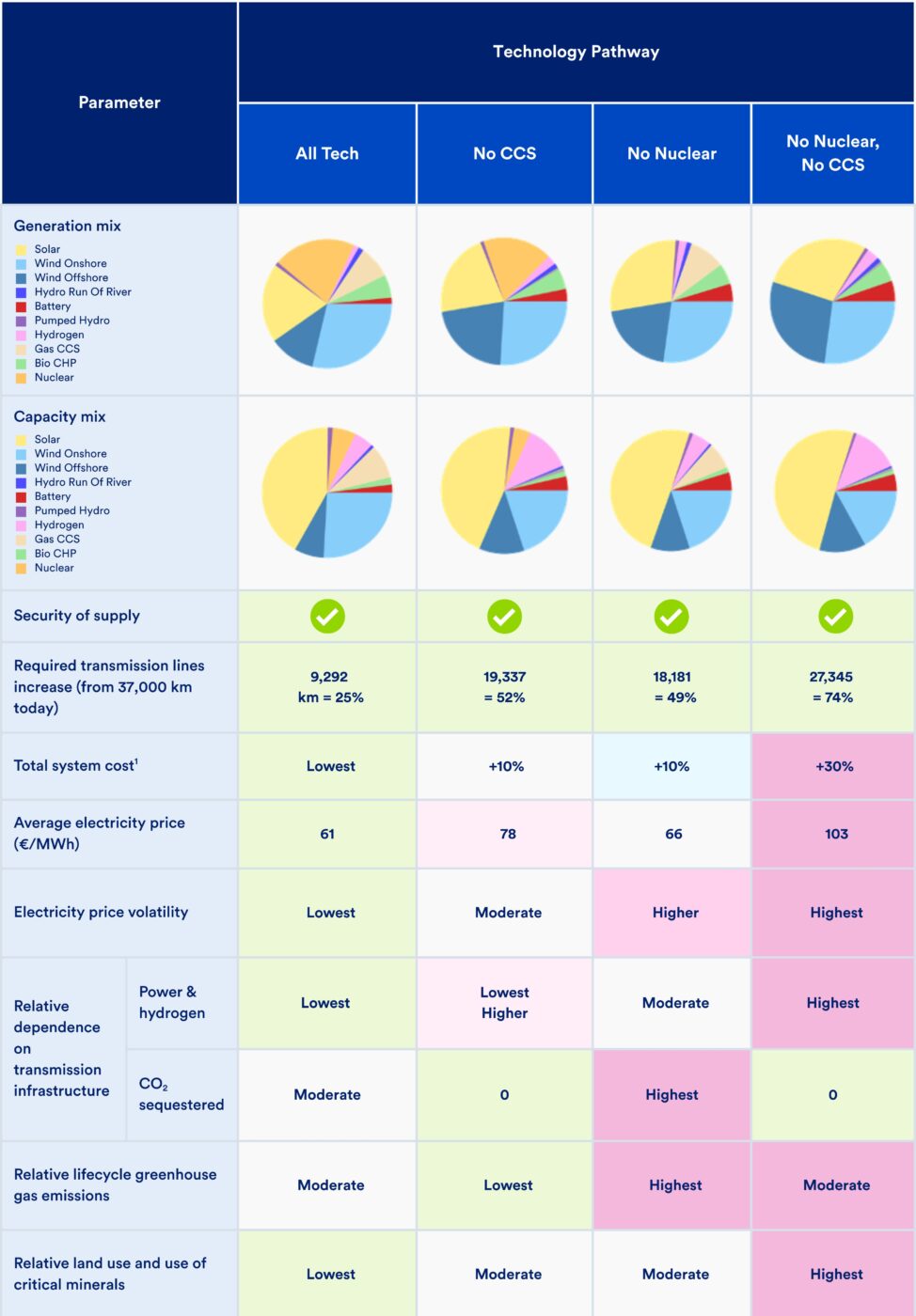

Results indicate that a technology-open approach and rapid acceleration of power system development are necessary to meet decarbonisation and energy reliability goals at lowest cost. In contrast, excluding technologies such as nuclear from power sector decarbonisation results in a pathway that lags considerably behind on all metrics. Without technology openness, total system costs are high, and electricity prices near 100 €/MWh, nearly double the electricity prices of a technologically diverse portfolio. In addition, a lack of technology diversity results in much more electricity price volatility, as shown in Figure 1.

Under all scenarios, Germany must significantly increase its deployment of renewable energy. This modelling further supports that solar and wind are key drivers for decarbonisation. However, without complementary technologies, a renewable energy generation and storage system results in significantly greater electricity price volatility (due to varying weather conditions) and has the highest use of land and critical minerals compared to other scenarios. The resulting high electricity prices and substantial volatility are likely unsustainable for both the public and German industry, posing risks of deindustrialisation and significant market uncertainty for investors.2

The study also shows that using hydrogen for energy storage to balance supply and demand in decarbonised power systems has high costs when compared to alternative strategies. It is, for example, roughly double the cost of gas with CCS as an alternative power source. Modelling shows that hydrogen for long-duration storage is most valuable if the system is constrained to achieve near-term decarbonisation and excludes alternative technology options, such as nuclear, other long-duration energy storage (LDES) technologies, or gas with CCS. When LDES or other clean firm technologies3 are available, the model shows a significant reduction in the amount of hydrogen built for storage. For near-term flexibility needs, the study found that non-hydrogen LDES can further significantly reduce the need for hydrogen for storage and gas plant generation. In the long run, clean firm technology options that are low-emission and can be readily dispatched, including gas with CCS and nuclear, show tremendous value in reducing system costs, transmission buildout, and customer prices. This result questions the long-term implications of Germany’s current strategy to build “hydrogen-ready” gas plants, as planned in the power plant strategy still under discussion. To ensure informed decision-making, the German government must fully estimate the long-term cost and system implications of “hydrogen-ready” gas plants, including the costs of hydrogen production, transport, storage, and turbine retrofit. Moreover, hydrogen use should be prioritised for the so-called no-regret sectors while ramping up other options that can provide clean firm energy generation for all sectors, such as nuclear.

Risk mitigation is a necessary complement — not a substitute — for ambitious reforms to existing clean energy bottlenecks. To manage an inherently uncertain future, this study’s results underscore the advantages of integrating diverse technology options into Germany’s energy policy. Embracing an options-based strategy will reduce system and customer costs, increase reliability, and enhance long-term resilience against unforeseen obstacles, such as resistance to expanding onshore wind technologies, slow transmission buildout, and potential stagnation in cost reductions for renewables and storage. When progress with one technology lags, others can compensate, ensuring continued advancement.

Table 1. Technology pathway scenarios considered in this report.

| Scenario | Storyline |

|---|---|

| All Tech. | Scenario embracing all supply technologies with reference input assumptions on simulation parameters. No local, Not-In-My-Backyard (NIMBY) opposition is considered. Restart of recently shut-down nuclear reactors gains political support. Groundwork is being laid for construction of new nuclear power plants with expectations that the first new plants may come online after 2040. Infrastructure development is underway such that captured CO2 from fossil power plants can be transported and stored. Moreover, infrastructure is being developed to draw hydrogen from an established pipeline network and storage, enabling its direct use as well as its use as fuel for power plants. |

| No CCS | Compared to All Tech., groundwork for CCS is not laid, reflecting a non-existent infrastructure in this technology pathway. |

| No Nucl. | Compared to All Tech., restart of recently shut-down reactors gains no political support, and building new nuclear power plants is not part of energy policy in this technology pathway. |

| No Nucl., No CCS | Compared to All Tech., neither nuclear nor CCS is allowed, thus representing the combination of No CCS and No Nucl. This scenario best represents current German energy policy. |

Figure 1. Summarised results comparing main parameters of German power systems in 2050 for four technology pathways.

The modelling suggests restarting Germany’s recently closed nuclear generators would facilitate decarbonisation while reducing costs and increasing reliability. Over the long run, new nuclear contributes to lowering costs, land use, transmission needs, power price volatility, and critical mineral requirements. However, nuclear power was phased out in 2023, and construction of new reactors has been banned since the 2002 Amendment of the Atomic Energy Act. The phase-out was adopted in 2011 under the CDU-CSU-FDP coalition, Cabinet Merkel II, in a reaction to the Fukushima nuclear accident. At that time, nuclear energy provided more than a quarter of Germany’s electricity. Given Germany’s complex history with nuclear power, the following sections explore how the country can adopt an option-driven approach to achieve decarbonisation as cost-effectively and rapidly as possible without prescribing a nuclear strategy — reflecting both the political phase-out decision and the ongoing contentious debate on the subject. While CATF acknowledges the current barriers to reversing Germany’s nuclear ban, it encourages policymakers to reevaluate nuclear energy’s role given its proven contributions to low-carbon, reliable electricity generation. Should Germany’s political landscape shift, advanced nuclear technologies, such as small modular reactors, could offer a viable pathway to complement renewables and reduce reliance on fossil backups. However, this analysis proceeds under the assumption that nuclear power remains excluded from Germany’s near-term energy roadmap.

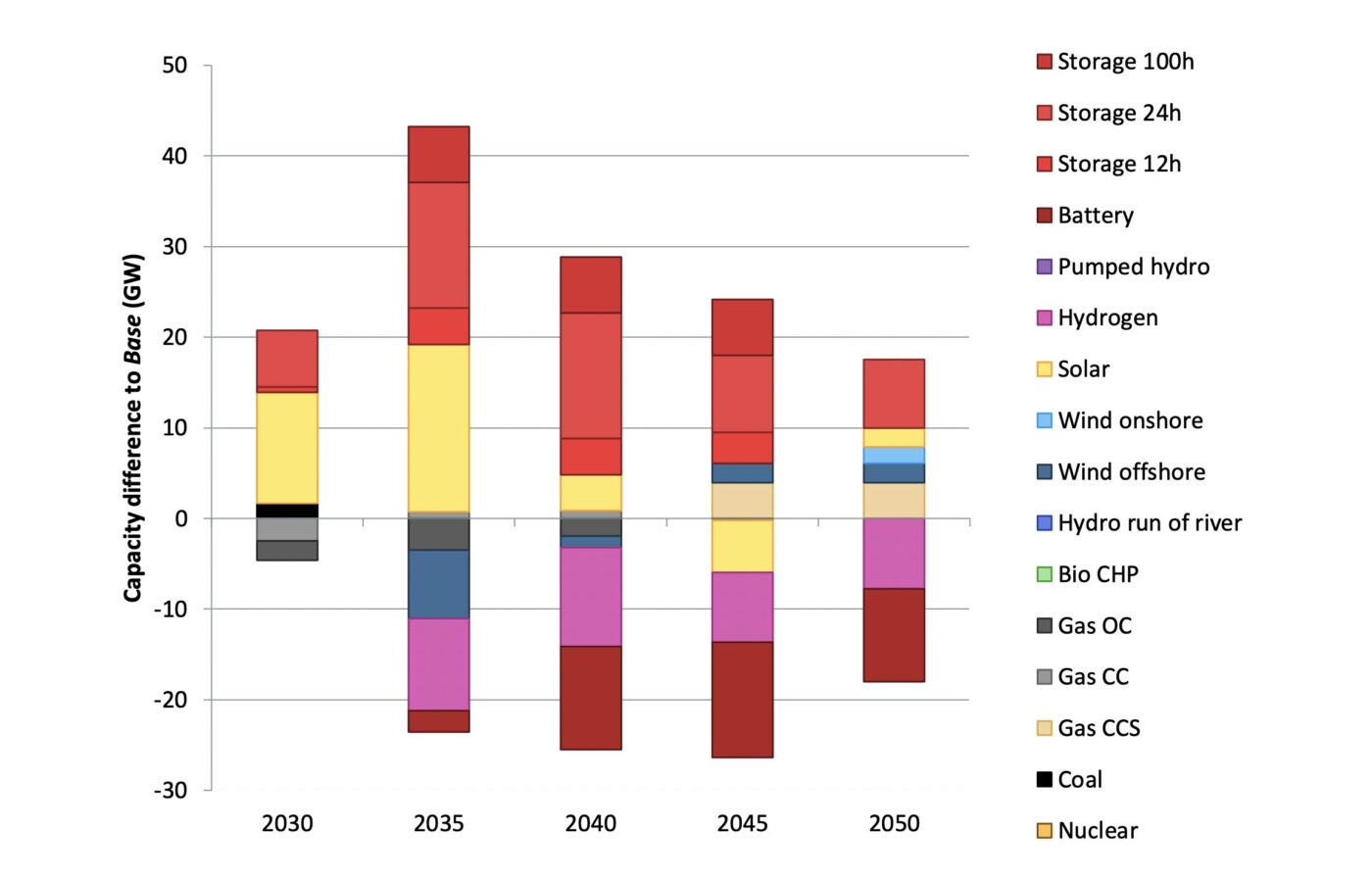

Figure 2. Difference in installed capacity when LDES is included, which shows LDES reduces need for hydrogen and fossil combustion and wind and has shorter storage requirements.

Section 3: Thematic Deep-Dive and Policy Recommendations

This section structures Germany’s decarbonisation opportunities across three complementary timeframes and strategic approaches. First, “Developing and Deploying Clean Technologies” focuses on scaling proven solutions that are commercially available today but require policy support for wider implementation. Second, “Fast Action for Emission Reduction” targets immediate opportunities to reduce emissions through efficiency improvements and addressing potent greenhouse gases like methane. Third, “Innovation in Clean Technology” looks toward emerging technologies that require further development but offer significant long-term potential. This three-pronged approach ensures a balance among immediate action, medium-term deployment, and long-term innovation — all necessary components of a successful and cost-effective transition.

Developing and Deploying Clean Technologies

3.1 Clean Hydrogen

The State of Clean Hydrogen in Germany

Two significant but challenging sectors that Germany must decarbonise fully are industry and transport, and for both sectors, clean hydrogen is expected to play a crucial role. In 2023, Germany consumed 46 TWh of hydrogen, making it the highest consumer of hydrogen in the EU. Almost all of this hydrogen, however, has very high associated emissions due to the process of producing the molecules.

Hydrogen is rarely found in a naturally abundant state and therefore must be liberated from a compound form. Most hydrogen produced globally today comes from reformation of natural gas, which produces around 8-10 kg of CO2 per 1 kg of hydrogen and collectively emits almost 1 Gt of CO2 per year.

Given the promise of clean hydrogen as a possible decarbonisation pathway for several hard-to-abate sectors, the Federal Ministry for Economic Affairs and Climate Action (BMWK) has predicted demand for hydrogen and its derivates of up to 440 TWh by 20455 and updated its national hydrogen strategy (Nationale Wasserstoffstrategie, NWS) in 2023 to outline market development and scale up. Key commitments are outlined in the NWS, including:

- Expanding nationwide electrolyser capacity to at least 10 GW by 2030.

- Developing at least 1,800 km of repurposed and newly built pipelines to establish a “core” hydrogen network in Germany by 2027-28, feeding into development of the wider European Hydrogen Backbone initiative.

- Adopting coherent regulatory conditions at the national, European, and, if possible, international levels, including efficient planning and approval procedures, uniform standards, and certification systems.

- Directing financial support to ramping up domestic renewables-based electrolytic (i.e., “green”) hydrogen production.

- Supporting a limited level of other clean hydrogen production pathways, such as “blue,” “turquoise,” or “orange” hydrogen, at least in the near term.6

- Establishing offtake in priority hard-to-abate sectors, including for industry, transport, and heat for buildings and power, through dedicated state funds.

Complementary to the NWS, Germany’s Hydrogen Acceleration Act and its Hydrogen Import and Power Plant strategies outline additional plans to support buildout of a national clean hydrogen economy.

The existing legislation underscores the country’s commitment to ramp up production and imports of the clean molecule while acknowledging the significant challenges associated with the planned increase in renewably produced electrolytic hydrogen. In June 2024, BMWK’s Expert Commission published its energy transition monitoring report, which emphasized that meeting the 2045 hydrogen demand target with electrolytic hydrogen alone will require nearly three times the current electricity production in Germany.7 Therefore, to decarbonise the national electricity grid while also providing the required renewable power to meet the 2045 electrolytic hydrogen production target, Germany would not only need to decarbonise its current electricity production but also significantly increase its electricity supply over the next ten years. With wind and solar power alone, reaching these goals appears to be a near-impossible feat, so a more realistic approach is needed.

Developing a Hydrogen Economy for Sufficient Clean Hydrogen Supply

Action 1: Prioritise Hydrogen for the Decarbonisation of Industry and Transport

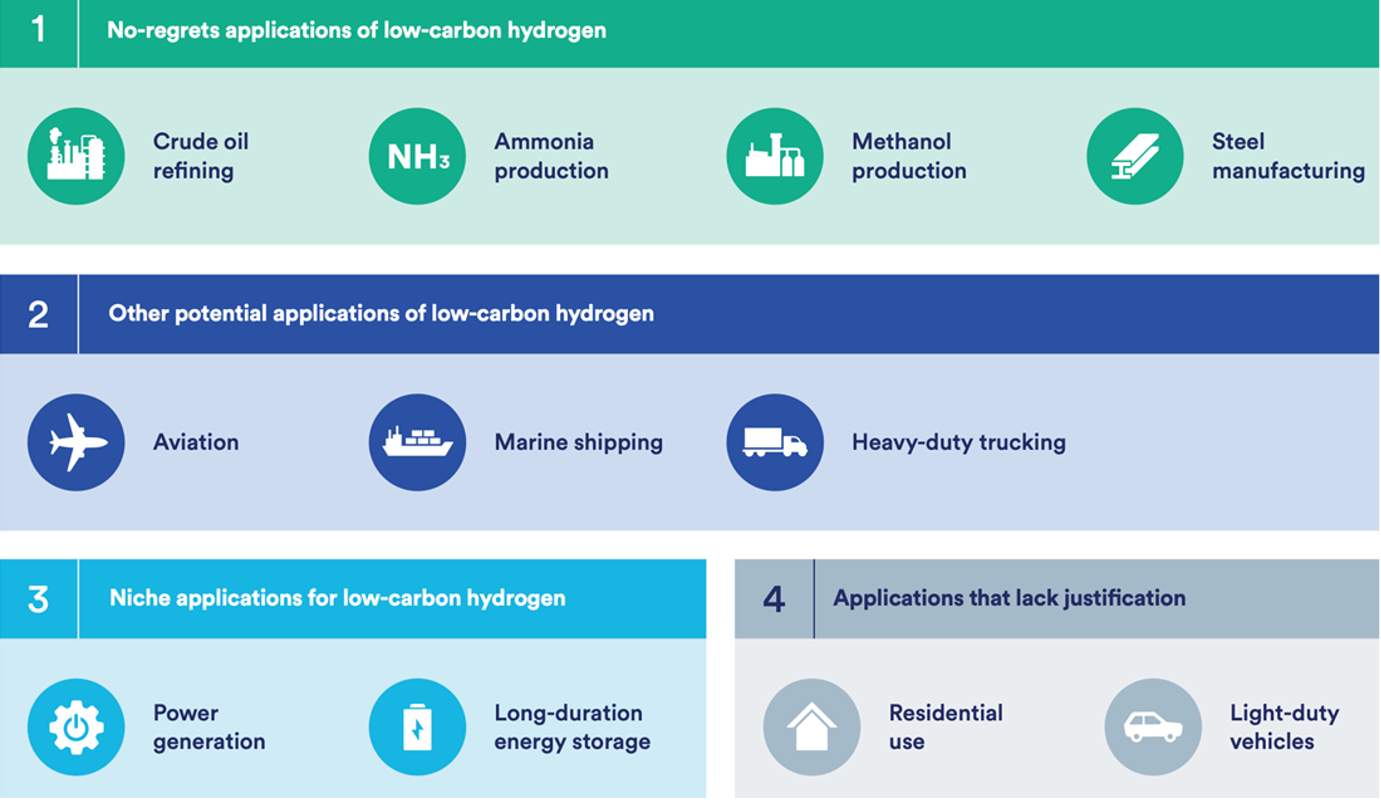

Clean hydrogen provides an essential tool for reducing emissions in specific sectors, but it is far from a panacea for decarbonisation. It should not be deployed indiscriminately to all sectors as if every potential end-use has equal merit. Given the limited domestic energy resources, clean hydrogen should be prioritised for use in hard-to-abate sectors (i.e., “no regrets” sectors), where it is needed as either a critical feedstock or energy carrier. Germany’s NWS highlights several sectors as priority off-takers for forthcoming clean hydrogen, including no-regrets segments of heavy industry and transport. Figure 3 outlines the key end-use sectors for which clean hydrogen will be crucial.

Figure 3. CATF priority ranking of potential clean hydrogen end-use sectors.

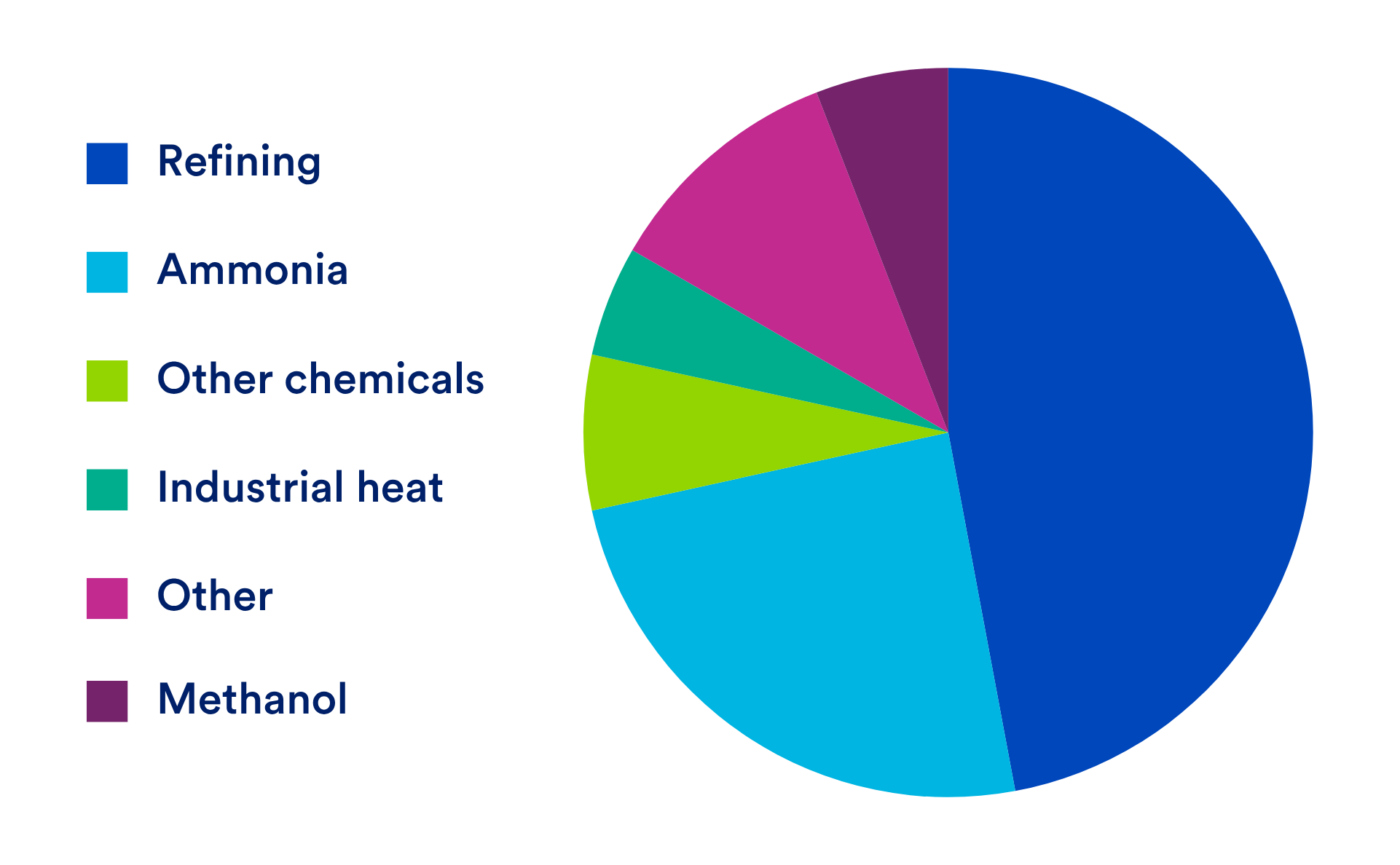

In 2023, Germany consumed 46 TWh of hydrogen (Figure 4), produced primarily through reformation of natural gas, which accounts for approximately 12 MtCO2e emissions per annum.8 Substituting this existing demand for a clean hydrogen alternative is a crucial no-regrets action for Germany to take in support of decarbonising its existing heavy industrial base and providing an offtake guarantee to the nascent clean hydrogen market.

Figure 4. 2023 hydrogen consumption in Germany.

Industry

The refining sector is currently the largest consumer of hydrogen in Germany, accounting for 22 TWh of demand. On average across the EU, around 40% of hydrogen consumed in refining is supplied as a byproduct of the refining process and as such cannot be replaced by exogenous hydrogen without disrupting complex value chains. In Germany, byproduct hydrogen accounts for around 8.7 TWh of hydrogen. Whilst the product profile of the refinery remains reliant on crude oil inputs, byproduct hydrogen can be decarbonised by integrating CCS into the refining process. Germany has 22 active refineries, which account for a significant number of jobs and produce essential products, including transport fuels, critical chemicals for lubricants, asphalt, and many others, all of which will continue to be crucial for the German economy. Decarbonisation of existing hydrogen in refineries, alongside decarbonisation of emissions from wider refining processes, is therefore an essential no-regrets action for Germany.

Ammonia production accounts for a further 11.1 TWh of hydrogen demand, as a crucial input for urea and nitric acid, which are used in production of fertilisers and other critical chemicals and consumer products, such as textiles, insulation, plastics, furniture, and agricultural chemicals. While further expansion of ammonia demand is possible for use in marine shipping, it is important that current production is decarbonised.

Methanol production is another critical process that currently utilises hydrogen, with Germany consuming approximately 2.6 TWh of hydrogen. Whilst its methanol production is smaller in scale than its ammonia production, Germany is Europe’s largest methanol producer, with a production capacity of 1.5 Mt/y across three major facilities owned by TotalEnergies (Leuna), BASF (Ludwigshafen), and BP (Gelsenkirchen). These plants are all integrated with refining operations, producing methanol in partial oxidation plants using residues from the refinery. As such, displacement of existing hydrogen with a clean hydrogen alternative is not a credible decarbonisation pathway for these existing facilities, and CCS would have to be explored.

Other chemical manufacturing accounts for a further 3 TWh of hydrogen demand in Germany, producing a range of chemicals, including aniline, cyclohexane, TDI, oxo-alcohols, and hydrogen peroxide.9 These chemicals are crucial for intermediate steps or onward use in a broad range of industries and products such as paints, polyurethane, adhesives, and plasticisers and as a bleaching agent in the paper industry.

Germany is also the largest steel producer in the EU, producing approximately 37 Mt of crude steel in 2024 and providing around 80,000 jobs in direct employment across the country in 2023. There are eight major primary steel plants in Germany, almost all of which are based on the carbon-intensive coal blast furnace production route. One plant, operated by ArcelorMittal in Hamburg, operates via the direct reduced iron (DRI) process, which uses natural gas and can be around two-thirds as carbon-intensive as a blast furnace. Decarbonisation of primary steel production is possible through operating DRI plants on 100% clean hydrogen, a technology with the potential to cut CO2 emissions to near zero. If Germany replaced its existing production with DRI and clean hydrogen, it would require 47 TWh of hydrogen annually,10 an almost doubling of existing hydrogen production capacity to meet this additional demand alone.

While many EU-based steel manufacturers have announced plans to develop green steel production through DRI and hydrogen, concerns have been continuously rising about the high costs of clean hydrogen, which may limit its realisation.11 Steel production is essential to the German economy, and offshoring activities could significantly contribute to deindustrialisation of the national economy, likely resulting in substantial job losses, increased dependence on resource imports, and displacement of CO2 emissions outside the EU to locations with less stringent climate regulations. Germany instead must chart a path forward that supports the transition of domestically manufactured steel to low-carbon methods, determining the deployment of the best decarbonisation options available (such as clean hydrogen and CCS) to each active steel plant in a pragmatic and cost-sensitive manner.

These sectors, along with existing hydrogen users, are the clear no-regret priorities for the German hydrogen sector. Priority should be given to supporting their decarbonisation where technically possible.

Transport

In addition to no-regrets industrial sectors, clean hydrogen is likely to be needed to decarbonise segments of Germany’s transport sector that are difficult to electrify. These include maritime shipping, aviation, and possibly parts of heavy-duty road transport, as recognised in the NWS.

For aviation, sustainable aviation fuels (SAF) continue to draw interest as an alternative to electrification as they offer compatibility with existing infrastructure and engines, often referred to as “drop-in” fuels. Clean hydrogen will be required to upgrade biomass-based sustainable aviation fuels (bio-SAF), to synthesise jet fuel from hydrogen and captured carbon (synthetic SAF), and, potentially, to power aircraft that directly utilise hydrogen as fuel. However, biomass feedstocks are limited, and synthetic fuel production is at present technically and economically challenging. As highlighted in a prior CATF report, land-use and supply chain constraints on biomass feedstocks mean that other fuel options will need to be developed, including synthetic fuels (or “e-fuels”) produced using a combination of hydrogen, electricity, and CO2 sourced from non-biogenic feedstocks. Synthetic fuel production, however, is currently technically and economically challenging.

In shipping, clean ammonia is a strong contender as a sustainable fuel, provided it is made from a clean hydrogen feedstock. Health, safety, and environmental concerns attributed to ammonia combustion would also need to be thoroughly examined before any wide-scale sectoral deployment. Furthermore, developing a clean ammonia fuel market should not detract from efforts to decarbonise existing ammonia production for present-day applications (e.g., for making low-carbon fertilisers). Another potential low-carbon marine shipping fuel is methanol, and many new cargo ships are being built with dual fuel capability to run on both marine oil and low-carbon methanol. However, unlike ammonia, methanol emits carbon at the point of combustion, so to produce a low-carbon fuel, “sustainable” carbon atoms would need to be sourced for the methanol production process.

In road transport, long-haul hydrogen fuel cell vehicles (FCEVs) can play a role alongside battery electric vehicles (BEVs) in decarbonising the trucking sector. The role that FCEVs play and their scale-up will ultimately be influenced by several factors, including cost, fuel and fuelling infrastructure availability, and well-to-wheel lifecycle emissions. Whilst parts of the transportation sector may require hydrogen and its derivatives to decarbonise, other forms of transportation, such as light-duty vehicles, would benefit by prioritising electrification as their primary pathway to decarbonisation. This priority is for reasons of cost as well as scalability, as hydrogen FCEVs require up to 2.5 times more energy than BEVs and their cost per kilometre or mile travelled is multiple times higher.

Given the importance of decarbonising its significant transport sector to meet climate goals, Germany should review where to best apply hydrogen alongside other leading decarbonisation options (e.g., BEVs) in the sector. It should prioritise volumes of clean hydrogen to priority transport segments as the technologies begin to scale, whilst also not drawing limited available clean hydrogen resource away from priority no-regrets sectors in the short term as clean hydrogen transportation technologies are developing.

Wider Uses

In the NWS, the government plans to establish “appropriate mandates for action and development” in industry and transport through direct state funding. However, the strategy does not rule out the use of hydrogen in other sectors, such as for power or heating buildings. CATF has conducted extensive analysis on hydrogen’s role in the power sector, which demonstrates that it will be a costly and energy-intensive process, whilst achieving limited reductions in emissions. Alternative methods for cleaning up the power sector would bring higher cost, energy, and emissions savings.

Likewise, blending clean hydrogen into the national gas grid for use in heating in commercial or residential settings would dilute the environmental benefits of a scarce commodity that could be better utilised in other sectors. For home heating specifically, numerous independent studies have concluded that alternatives such as heat pumps, solar thermal systems, and district heating are more economic, more efficient, and less resource-intensive and have a smaller environmental impact. Additionally, there are serious safety hazards associated with hydrogen use in residential settings owing to its high tendency for leakage and an ignition or explosive range that is six times that of natural gas.

Infrastructure

In order to supply hydrogen to a range of offtakers across the country, Germany has outlined an ambitious plan to develop at least 1,800 km of repurposed and newly built pipelines by 2027-28, feeding into development of the wider European Hydrogen Backbone pipeline initiative. This plan has been further developed with the proposal for a “hydrogen core network,” now approved by the Federal Network Agency (BNetzA), consisting of 9,040 km of pipeline scheduled to be gradually commissioned by 2032 (60% repurposed from natural gas and 40% new build) at an anticipated investment cost of €18.9 billion. While CATF analysis shows that pipelines are the best option for transporting hydrogen, initial implementation should focus on developing hydrogen production as close as possible to priority offtakers. This approach can help to avoid investment in a highly capital- and time-intensive pipeline network, which could be better prioritised to support development of a portfolio of hydrogen production projects.

Germany should first direct state funding to support priority segments of the industry and transportation sectors, whilst, in parallel, ruling out the use of clean hydrogen blending into the gas grid and for home heating. It should also take a more cautious look at whether and where hydrogen could support decarbonisation of the power sector.

Action 2: Focus on Clean – Not Green — Hydrogen Production

In its updated NWS, Germany laid out an ambitious framework of actions to meet anticipated hydrogen demand. Significantly, it aims to meet this demand almost entirely with renewables-based electrolytic hydrogen (powered primarily by wind and solar energy sources) and has set a domestic target of 10 GW installed electrolyser capacity by 2030 to achieve this goal.

This level of electrolytic production will create significant additional demand for renewable energy and is, by itself, unlikely to be sufficient to satisfy demand for clean hydrogen. Although domestic renewable capacity levels are increasing, it is counterintuitive to use renewable energy for dedicated hydrogen production while the grid remains carbon-intensive, particularly as electricity consumption is expected to grow with the increasing role of electrification in decarbonisation.

If renewably powered hydrogen is not available in substantial quantities to fully support forecasted German hydrogen demand, particularly in the near term, efficient deployment of alternative clean hydrogen applications based on proven technologies should be considered a necessary intermediate solution to rapidly scale up clean hydrogen production and begin addressing the current resource gap.12

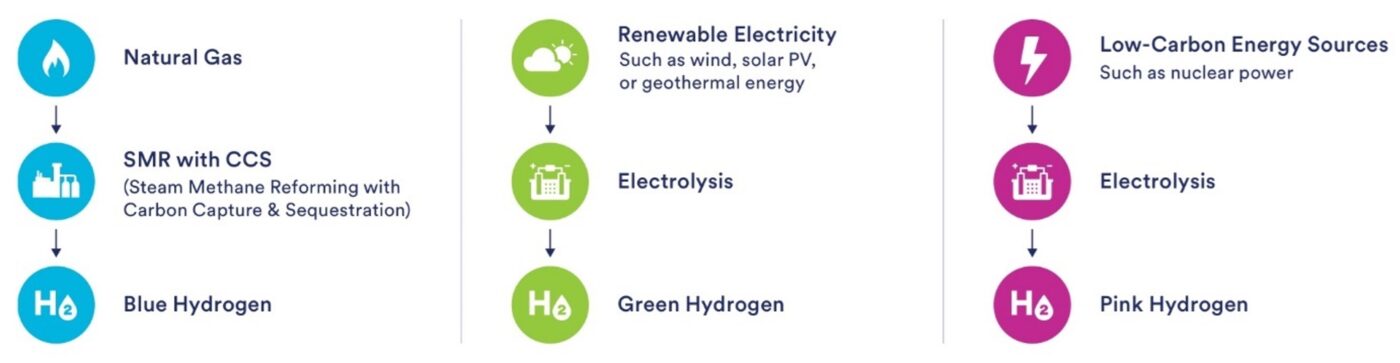

Production of clean hydrogen — which makes up only around 1% of all hydrogen produced today — is possible through various pathways, such as integrating carbon capture technologies into the existing natural gas reformation technologies used today to produce unabated hydrogen; but that possibility is viable only so long as strict methane emissions controls are imposed on the upstream natural gas value chain. Clean hydrogen can also be produced via electrolysis powered by alternative clean firm energy sources, such as superhot rock geothermal and nuclear energy (Figure 5).

A more holistic approach to hydrogen production is needed to ensure sufficient supply reaches the market in time, while creating the space for renewables-based electrolytic hydrogen to scale as renewable electricity becomes more abundant and large-scale storage solutions for intermittent supply are developed.

Figure 5. Low-carbon hydrogen production pathways.

Supporting a variety of clean hydrogen pathways, scaled in parallel, would allow Germany to decarbonise existing hydrogen demand today while expanding clean hydrogen production to meet emerging demands, thus accelerating emissions reductions across a broad range of priority offtakers.

The updated NWS recognises the need to utilise other forms of low-carbon hydrogen, at least in the short term, to help establish a functional and cost-competitive clean hydrogen market. However, financial support will mostly be limited to renewables-based electrolytic hydrogen. The simplicity of hydrogen colour coding does not reflect the actual value of greenhouse gas (GHG) emissions released across the molecule’s lifecycle from production to end use. Any incentives that Germany introduces for clean hydrogen production should be measured against its full GHG emissions reductions based on rigorous emissions accounting.13

Germany should direct its financial incentives and policy support to all clean hydrogen pathways that are measured as truly low carbon, following the EU guideline requiring a 70% emissions reduction and emissions below 3.4 kg of CO2 equivalents per kilogram of hydrogen (including production and transport). Further, CATF encourages Germany to work with the EU and other trading partners to implement a collective framework and strong standards that will certify any produced and delivered clean hydrogen (including imports) as truly low carbon.

Action 3: Conduct a Realistic Assessment of Hydrogen Imports

Even when hydrogen is produced from all clean energy sources available in Germany, domestic resources alone are unlikely to meet the projected demand for the molecule. As a result, Germany is increasingly relying on hydrogen imports to bridge this gap. The federal government’s assessment estimates that up to 70% of expected hydrogen demand must be met by imports (around 45-90 TWh per annum), with volumes expected to increase exponentially up to 2045 in line with increasing end-use demand (around 360-500 TWh for hydrogen and an additional 200 TWh for derivatives). To achieve this level, Germany has outlined a dedicated framework of measures to meet these import volumes over the coming years.

In its hydrogen import strategy, Germany will focus on two primary import methods: pipeline and ship transport. Imports will be sought from a range of European and near-Europe export regions where hydrogen production capacities are expected to be higher. This high-level analysis aligns with findings from a CATF techno-economic investigation into the most efficient methods to import hydrogen into European hubs from several global locations. These include Norway, the U.S., and the Middle East and North Africa — regions where Germany already has established Memorandums of Understanding or similar agreements.

Under all scenarios, this CATF analysis found that importing large quantities of hydrogen over long distances will be an expensive and relatively energy-inefficient endeavour due to the inherent properties of hydrogen, particularly its low volumetric density. Of the options available, the most cost-effective method is transporting hydrogen by pipeline, ideally over the shortest distances possible. Cross-border hydrogen trade within Europe — across EU Member States and with neighbouring non-EU countries — could be implemented via existing pipelines converted for hydrogen transport. Initial projects are already being planned with Denmark, Norway, and the UK, as well as larger “corridor” pipelines bringing hydrogen to Germany from the North Sea, Baltic Sea, and Southern European regions. Successful implementation, however, will require broad support from EU members, with actions coordinated at the EU level through the European Commission’s Important Projects of Common European Interest. It will also require swift execution of network development projects to convert existing pipeline infrastructure. Other cross-border collaborative projects, such as the EU Hydrogen Valleys, may also help streamline such efforts and mitigate implementation barriers.

Germany’s NWS plans on importing hydrogen and derivatives via ship as well. CATF analysis found that, of all the ship-based transportation methods, the most cost-effective is in the form of ammonia when applied for direct use in industrial processes or as a future transportation fuel (such as for fertiliser production or as a maritime shipping fuel). However, “cracking” ammonia to liberate pure hydrogen from the compound state incurs significant energy penalties — as much as 30% of the hydrogen delivered at the point of import — making the process much less efficient and more costly.

The import strategy considers additional ship-based import pathways, including methanol, e-fuels, and liquid organic hydrogen carriers (LOHC). When used directly (similarly to ammonia), these fuels could offer a net benefit to Germany, provided a hydrogen conversion step is avoided. Other options, such as liquified hydrogen or LOHC, would entail substantial energy penalties across the entire import value chain, as the molecule would need to be (re-)converted or (de-)hydrogenised, on top of the need for significant additional new infrastructure. Compared to pure hydrogen, ammonia is much cheaper and more stable to transport via ship and truck and has an established transport network via rail and truck that can accommodate current consumption levels.

Any hydrogen transport should (a) be limited to cases in which hydrogen serves a very specific need and (b) use the most energy- and cost-efficient methods, such as pipelines. Where connecting hydrogen infrastructure across borders is needs-driven, Germany should approach international collaborative efforts carefully, considering the logistics and cost-effectiveness of such large-scale hydrogen transportation. If hydrogen must be transported over longer distances, new infrastructure may be needed, which will come with long time horizons and significant costs for planning and buildout.

Furthermore, a net-zero Germany in a world that has not achieved significant emissions reductions will not be sufficient to address the global challenge. Low-carbon hydrogen imports to Germany should not come at the expense of decarbonisation efforts in other parts of the world, particularly in regions faced with energy poverty. These regions require their domestic resources for their own domestic purposes, such as expanding renewable electricity or producing low-carbon hydrogen for clean fertilisers to support local agriculture.

To avoid costly but ultimately unsuccessful ventures and stranded assets, Germany must prioritise identifying where realistic hydrogen demand gaps in 2030 could be met by uncracked clean ammonia and what part of the needed supply can be reasonably imported via pipeline from neighbouring countries, building out adequate infrastructure accordingly.

3.2 Carbon Capture and Storage

Carbon capture and storage (CCS) is a pollutant control technology that can reduce CO₂ emissions from carbon-intensive facilities such as heavy industrial processes and fuel combustion. The CO₂ is separated from other gases (captured), compressed, and transported to geological storage sites where it is stored deep underground in porous rock formations, covered by an impermeable cap rock that effectively traps the CO₂ in place. When CO₂ is stored in suitable geological formations, it is kept there permanently, with the injected CO₂ staying trapped in the subsurface for millennia.

An advantage of CCS to decarbonise industrial processes is its comparative cost-effectiveness, particularly when considering the cost to end consumers. As our analysis has outlined, pathways that use CCS to produce low-carbon industrial products are often the lowest-cost or only option available in some sectors. This finding is supported by analysis of the International Energy Agency (IEA). The cost increase incurred by decarbonised production processes becomes relatively small for downstream products. For example, if using CCS to produce low-carbon cement and steel, the cost of a bridge construction would increase by just 1% while more than halving its emissions.

The State of CCS in Germany

Nearly a quarter of Germany’s CO2 emissions come from its industrial sector, which is the highest emitting in Europe with more than 150 Mt CO2 emissions annually in the past years.14 Europe’s second largest emitter, France, emits just half of that number, with 75 Mt CO2 per year. Decarbonising Germany’s industries is thus imperative for achieving climate neutrality in Europe. Germany’s primary industrial emitters are iron and steel, cement and lime, refineries, and chemicals. Taking the cement sector as an example, two-thirds of this sector’s emissions are process emissions that currently cannot be completely mitigated through fuel switching or clinker substitution. The slower Germany’s industry is decarbonising until 2045, the higher will be the carbon price industrial facilities will face, risking their competitiveness while placing Germany’s climate targets outside of reach. While measures targeted at reducing these emissions, including electrification and improvements in energy efficiency, are being rolled out, Germany will not be able to achieve its 2045 climate neutrality goals without carbon capture as planned measures are not sufficient to completely decarbonise sectors such as cement production.

Achieving net-zero GHG emissions, or climate neutrality, will also depend on development and deployment of permanent carbon removals, such as those delivered through CCS-based methods including direct air capture and bio-CCS/BECCS to tackle remaining residual emissions. Deployment of these removal methods will depend on the same climate infrastructure, namely CO2 transport and storage, that point-source CCS requires.

For other sectors such as steel production, green hydrogen is not a panacea. As discussed above, renewable hydrogen production will not be sufficient to decarbonise the entire economy without imposing prohibitively high costs. Ultimately, any CO2 not emitted is a benefit to the climate, and applying CCS today will almost always be a lower-cost option than having to remove this CO2 from the atmosphere permanently at a later date. CCS can deliver large volume abatement on a wide variety of emission sources. Enabling a wide portfolio of technologies to decarbonise a diverse set of industries, including CCS, reduces the risk of one mitigation technology option not delivering as intended. Several companies are already advancing CCS projects in Germany, such as Heidelberg Materials GeZero carbon capture project to fully decarbonise cement production of its Geseke plant in North Rhine-Westphalia with support from the EU Innovation Fund.

One of the key barriers to CCS development in Europe has involved development of CO2 storage sites. The cost of CCS varies from facility to facility and hinges upon many factors, with the availability and proximity of CO₂ infrastructure being key. Without access to CO₂ storage sites in Germany, emitters may face considerably higher costs exporting their CO₂, especially those located far away from export terminals such as in the south of the country. As CATF analysis has shown (also here), an export-focused CO2 network could lead to capital costs two to three times higher than a scenario that also utilises a domestic storage resources scenario, while annual operating costs are over three times higher.

According to these two studies, ultimately, German industries will be able to equitably utilise CCS at lower cost only if Germany and the rest of Europe make both CO₂ transport and storage infrastructure more broadly available.

Basin-level estimates of Germany’s CO2 storage capacity vary between 20,000 Mt CO2 (low estimate) and 115,300 Mt CO2 (high estimate).15 With the May 2024 draft revision of Germany’s Key Principles for a Carbon Management Strategy and the Carbon Dioxide Storage Act, offshore storage would be allowed, and states can opt in for onshore storage. These changes would create flexibility in the national strategy and could enable CO2 storage for emitters far from export locations, thus lowering the overall costs of decarbonisation of industries. Once these legislative changes are passed by Parliament, states that are ready to implement these solutions can proceed, contributing to a broader, more effective deployment of CCS technologies across the country.

Notably, the state government of North Rhine-Westphalia had developed its own carbon management strategy before the federal strategy, and it will play a key role in industrial decarbonisation given the high industry density in the state. North Rhine-Westphalia’s strategy, based on extensive analysis by the Wuppertal Institute, places significant reliance on transport of CO2 to Norway and the Netherlands for storage. Given the large storage potential in Northern Germany, opting for onshore CO2 storage could be attractive for the industrial hub, as closer storage sites will significantly reduce costs. As CATF’s CCS cost tool shows, without a network of CO2 pipelines, the costs of CCS could range between €150/t and €250/t for most facilities in Germany. At carbon prices of €150/t, no industrial facility would be cost-effective without government subsidies.

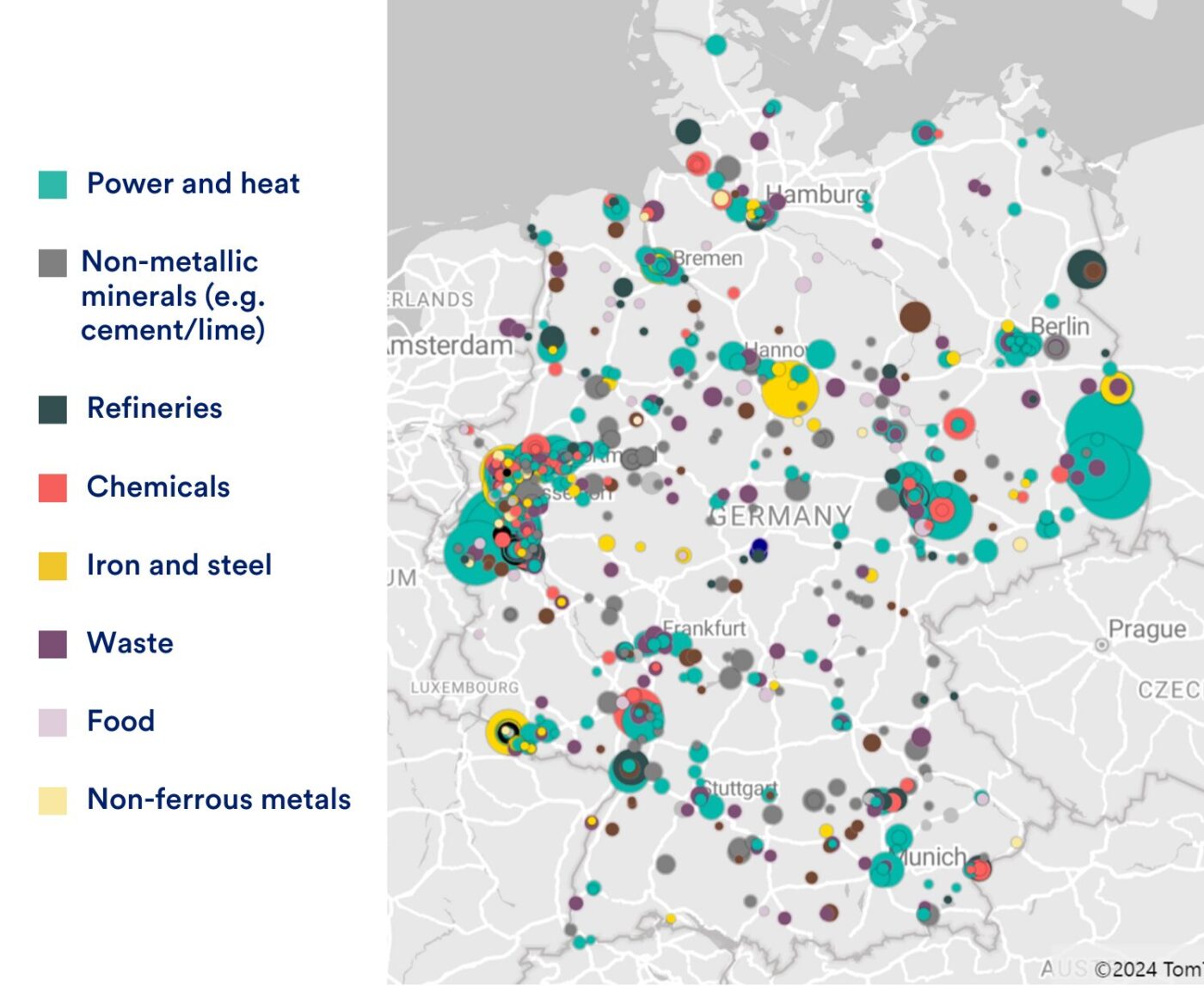

High costs for CCS also arise because CO2 point sources, specifically in the cement and lime sectors, are frequently located at dispersed locations far from a likely offshore storage site (Figure 6). Hence, apart from storage sites close to emitters, a transportation network to connect point sources to the storage sites is needed. Stakeholders are increasingly aware of that need, and a key study outlined the need for a network enabling CO2 transport both within Germany and for exporting abroad. Private entities have started planning CO2 pipeline networks, such as the grid proposed by the gas network operator OGE, but such projects will be challenging to realise without certain demand from capture projects or other sources of funding.

Figure 6. CO2 point source emissions in Germany.

Source: CaptureMap by Endrava

Accelerating Carbon Capture and Storage in Germany

To leverage the progress made the past year in updating and streamlining the draft carbon management legislation, the German government now needs to set clear goals and ensure that CCS projects are implemented to ensure that German industries can decarbonise at the lowest cost and retain economic competitiveness in the face of rising EU Emissions Trading System (ETS) prices.

Action 1: Harness Germany’s CO₂ Storage Potential and Coordinate Efforts

Building on the successful stakeholder process initiated in 2023, the government should continue involving industries, states, and other relevant stakeholders in planning the necessary CO2 infrastructure. While the pipeline network will be in private hands, the government should ensure that the buildout gives access to all emitters and collaborates with other EU Member States to further enhance benefits from economies of scale. Given that each EU member has unique characteristics including industrial emitters, geological conditions, existing pipeline, and other transport infrastructure, capturing, transporting, and storing CO₂ across borders will, in some cases, be the most economically efficient option. Bilateral or multilateral agreements like the Aalborg Declaration signed by France, Germany, Sweden, Denmark, and the Netherlands, are crucial to ensure a cost-effective European transportation and storage system. The German government should set clear goals for storing CO2, so that businesses and pipeline investors can better plan their investments.

Action 2: Advance CCS Projects by Providing Financial Security

Without incentives or regulatory measures, emitters have little reason to deploy carbon capture and storage. Therefore, the technology will not see widespread implementation unless a clear business case exists — or emitters are simply forced to deploy the technology. The economic advantage obtained by using CCS is derived from the ETS, through avoidance of surrendering allowances for emitters for each ton of CO₂ verifiably captured, transported, and stored. While rising costs under the ETS make it more and more economical to use CCS for industrial decarbonisation, the current Carbon Contracts for Difference programme is crucial to cover the prevailing cost gap and provide greater certainty to developers and investors, thus helping industries get ahead of the ETS impact and cut emissions sooner rather than later.

Fast Action for Emission Reduction

3.3 The Importance of Cutting Methane Emissions

An often-overlooked building block in reducing greenhouse gas (GHG) emissions is methane. As the second greatest contributor to climate change, it is over 80 times more potent than CO2 for global warming over a period of 20 years.16 Mitigation is therefore crucial to reduce the impact of climate change in our lifetimes and avoid irreversible tipping points. The Intergovernmental Panel on Climate Change’s Sixth Assessment Report identified methane mitigation as a priority and stressed the need for rapidly reducing methane emissions.

Action 1: Systematically Set Goals, Monitor Progress, and Report Outcomes

At COP26, Germany signed the Global Methane Pledge, which aims to reduce global methane emissions by 30% by 2030. The government now needs to establish a robust Methane Action Plan that outlines detailed sectoral objectives and targets to reduce methane emissions, along with a corresponding plan to reach the goals. This plan must include implementing the EU Methane Regulation, harmonising it with national legislation, and adopting further measures. Furthermore, it requires an accurate estimation of emissions per sector to adopt effective policies. The National Inventory Report for the German Greenhouse Gas Inventory prepared by the Umweltbundesamt provides a comprehensive baseline. Emissions need to be continuously monitored and reported to track progress and ensure compliance with emission reduction targets.

Domestic Methane Emissions

- Agriculture

Germany’s main methane-emitting sector, with 39.1% of total methane emissions, is animal farming and agriculture. Reducing domestic methane emissions in agriculture is not only crucial for mitigating climate change but also for enhancing the sector’s productivity and competitiveness through adopting new practices and technologies. The primary contributor to methane emissions in agriculture is livestock’s enteric fermentation and manure management. Additionally, nitrous oxide emissions from agricultural soil management, chemical fertilizers, and non-livestock manure management add to the sector’s overall methane emissions. Despite a 58% reduction in methane emissions in Germany between 1990 and 2019, the agriculture sector has seen relatively modest emission decreases, with reductions in livestock numbers being the main driver.

Action 2: Incentivise Lower-Emission Livestock and Manure Management

Germany has established political priorities to reduce emissions from livestock through further reducing the number of animals and area restrictions of animal husbandry. There are opportunities to accelerate reduction in agricultural methane emissions by focusing on husbandry practices and technologies, some of which have already been mapped by the government. Therefore, the government should prioritise the following approaches to accelerate reduction of enteric emissions from livestock:

- Support development of a breeding index for low methane emissions intensity for dairy and beef cattle, in addition to efforts to breed dairy cattle for longevity. Although a long-term strategy, these reductions are permanent and additive. Preliminary analysis estimates reduction in methane between 20%-30% by 2050, depending on selection intensity. Since Germany has approximately 4M dairy cattle, mostly Holstein, the development of such index is a great opportunity for the dairy sector.

- Map opportunities and develop policies that support the livestock industry to optimise animal health and productivity by controlling diseases during critical periods, improving calf-rearing, and reducing mortality rates. The federal program to promote the conversion of livestock farming, for example, is likely to accelerate reduction in livestock numbers due to reduction in “waste” emissions from sick or dead animals and may be expanded to other areas. However, other issues such as a high incidence of perinatal dairy calf mortality may benefit from government support for improved management practices.

- Incorporate consumer-accepted feed additives that reduce enteric methane emissions from livestock as they directly influence the digestive process.

For manure management, Germany has long prioritised the treatment of manure and the use of anaerobic digestion with coverage of digestate lagoons. However, without an ongoing program to modernise digesters and a strong monitoring and verification framework, anaerobic digestion leaks may hinder the benefits provided in reducing methane emissions. Therefore, the government should:

- Incentivise adoption of other manure management practices effective at reducing methane emissions such as manure acidification.

- Build a program to maximise methane reduction and prevent leakages from operating anaerobic digesters that supports maintenance of operating systems and technology update when feasible.

- Develop and enforce a low-cost framework for leak detection and repair for operating and new anaerobic digesters, preventing leakage of methane into the atmosphere.

The government should also prioritise monitoring, reporting, and verification (MRV) of emissions from agriculture. A consistent and ongoing MRV program allows more effective practices to be further supported through the development of policies.

- Energy Sector

The second highest methane-emitting sector, with 25.8% of Germany’s total methane emissions, is the crude oil and natural gas industry. Whilst Germany has made progress tackling methane emissions from the energy sector, a report from Ember on substantial undercounting of emissions calls into question Germany’s leadership position in lowering methane emissions, as actual methane emissions from lignite mines are estimated to be 28 to 220 times higher than reported. Methane emissions in the energy sector arise from the controlled release and combustion of gas, known as venting and flaring, as well as through uncontrolled release of gas through faulty or malfunctioning equipment, commonly known as leaks. Methane leaks in the transmission and distribution of gas appear to be more significant than currently reported. In its Europe-wide mapping of methane source emissions, CATF found significant leaks, including from the country’s largest transmission compressor station at Mallnow near the Polish border.

However, tackling undercounted methane emissions from the oil and gas sector is one of the fastest, most cost-effective, and impactful actions Germany can take to address the energy and climate crisis and is one of the only low-hanging fruits remaining in the climate fight. According to the IEA’s Methane Tracker, 71% of emissions in the energy sector in the EU could be mitigated at low cost and 41% at no net cost. Globally, flaring, venting, and leaking amount to $47 billion in lost revenue per year, making it economical to address methane emissions. Cutting methane emissions would ensure that all the gas in the pipeline arrives at the consumers. These averted emissions within the EU could amount to 600 kt of methane per year and correspond to the annual consumption of gas in almost 1 million French homes.

In November 2023, the EU agreed to its first-ever rules on reducing methane emissions in the energy sector. These include the bloc’s first rules for domestic producers on leak detection and repair (LDAR), venting and flaring of gas, and emissions from abandoned and inactive wells, as well as annual monitoring and reporting of emissions, which are subject to verification by independent verifiers.

Action 3: Implement the EU Methane Regulation and Monitor Abandoned Wells

Furthermore, about 20,000 onshore wells have been abandoned in Germany. While they are required to be plugged to prevent harmful chemicals and gases from escaping the wells, a key study reported that some wells might still release emissions.17 It is therefore crucial that abandoned wells are monitored for potential leaks and then plugged if leaks are found.

To tackle domestic emissions from venting, flaring, and leaks in the extraction, transmission, and storage of natural gas and oil, the German government needs to ensure consistent implementation of the EU Methane Regulation. Doing so includes setting proportionate and dissuasive fees, requiring regular LDAR inspections by oil and gas installations to reduce fugitive methane emissions, implementing new obligations restricting routine venting and flaring, and ensuring a measurement-based MRV process to quantify methane emissions, as set forth in the regulation.

Imported Methane Emissions

With only 6% of natural gas being domestically supplied, the upstream emissions of gas are a crucial target to tackle for the EU’s largest importer of gas. The EU Methane Regulation includes landmark obligations on importers of fossil fuels. Starting in May 2025, importers will be required to collect data on imported oil, gas, and coal; and from 2027, importers will be required to demonstrate that imports meet the same MRV standards as those adopted in the EU’s Methane Regulation. These data-reporting and MRV obligations will be complemented by an intensity standard that limits maximum emissions per unit of oil, gas, or coal. The European Commission will define a methodology for how methane intensities are calculated in 2027 and set maximum emissions thresholds to be enforced by 2030.

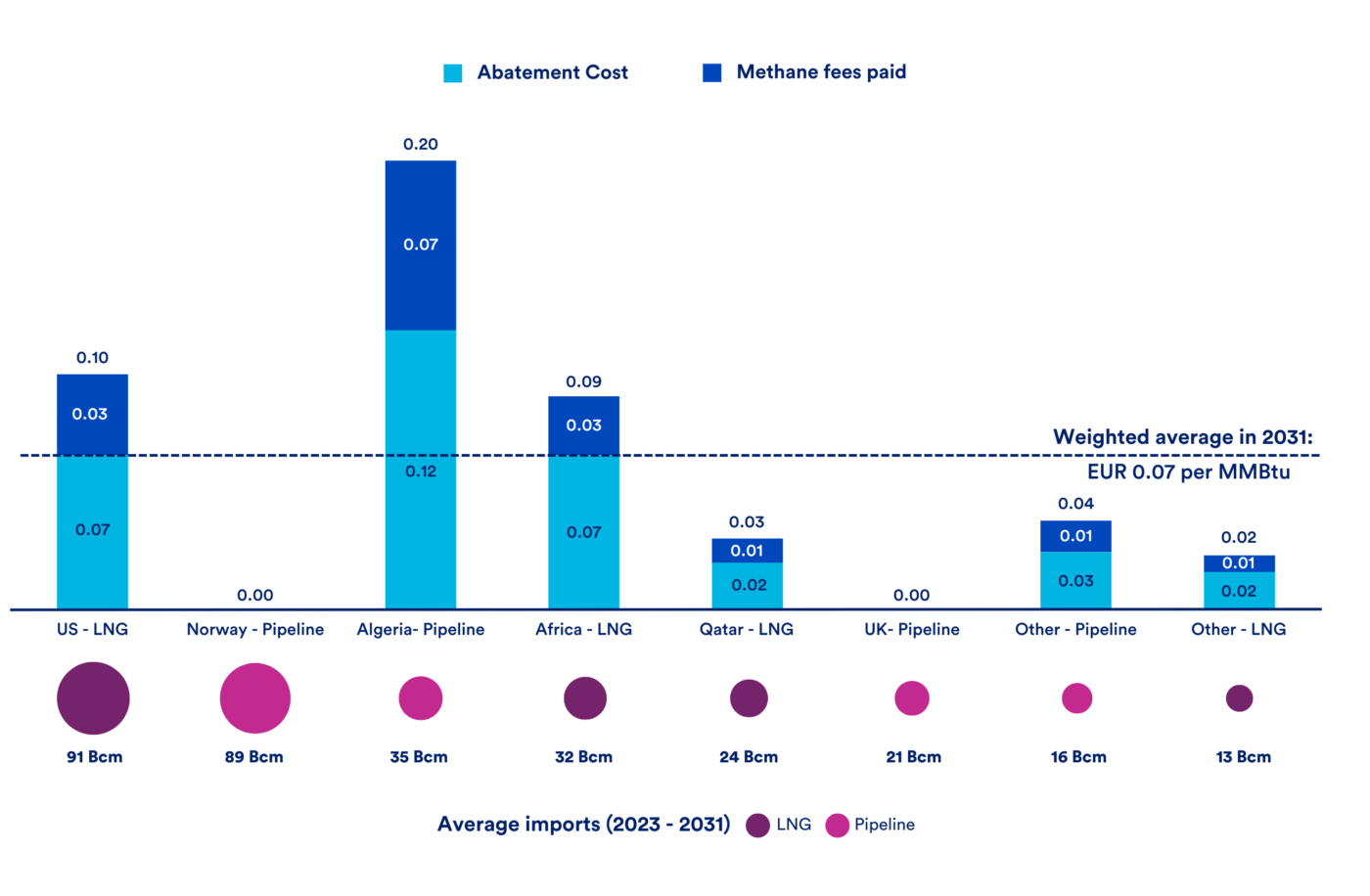

CATF’s analysis with Rystad showed that a phased import standard would have demonstrable emission reduction benefits, with minimal cost for suppliers of gas (Figure 7) and even less impact on consumers because many suppliers will be able to sufficiently reduce emissions to avoid paying a fee — leaving those required to pay the fee with little pricing power to pass the cost on to consumers. In the CATF-Rystad model, prices will therefore rise about 1%, at most, due to the import standard. Especially for Germany, price increases should be minimal, as it replaced Russian gas with high methane intensity (9.3 Gg methane per Mtoe gas) with Norway’s lowest weighted import intensity (0.1 Gg/Mtoe) after Russia’s invasion of Ukraine in 2022.

Figure 7. Incremental costs to gas exporters to the EU resulting from implementation of Minimum Import Price Scheme, 2031.

Action 4: Ensure Consistent Application of the EU’s Methane Regulation

As all contracts concluded after the EU Methane Regulation’s entry into force must comply with future obligations, Germany should ensure that future energy contracts meet standards adopted in the regulation, which requires a firm understanding of how these new obligations affect different types of energy contracts. The German government should immediately develop a future-orientated procurement strategy that takes these legal considerations into account and encourages compliance with all provisions in the regulation.

Effective implementation of the Methane Regulation’s new import standard will require the establishment of dissuasive fees on operators and importers to incentivise abatement throughout the value chain. Article 30 of the regulation stipulates that EU Member States must implement fines proportionate to the environmental damage and impact on human safety and public health; therefore, the German government should consider establishing fees on methane that take into account the significantly higher global warming potential of methane over CO2. While the import standards costs will ultimately depend on the European Commission’s forthcoming methodology, a joint CATF-Rystad baseline impact assessment showed that fees could be levied as high as €1500/MMBTU without significant adverse effects on gas prices.

Innovation in Clean Technology

Apart from leveraging ready-to-deploy technologies like clean hydrogen and CCS and taking fast action by tackling methane emissions, it is crucial to invest in future innovations that can drastically help to reduce emissions and decarbonise Germany’s economy. Technologies like fusion and superhot rock geothermal energy are good examples of innovations with important potential benefits in ensuring sufficient clean energy in Germany — and the EU as a whole However, demonstration is lagging due to the lack of coordinated efforts to support these innovative technologies.

3.4 Fusion Energy

Fusion energy could become a promising solution to meet Germany’s immense energy needs in the near-to-medium term. By replicating the same process that powers the sun, fusion energy represents a paradigm shift in power generation. Unlike traditional forms of energy production, fusion harnesses the vast power released when atomic nuclei merge, resulting in an abundant and sustainable energy source. The fusion industry is flourishing as new companies and start-ups are being created worldwide, including in Germany, and international collaborations and contracts are evolving quickly. Germany is one of the leading countries in the field globally and a leader in fusion technology in Europe. In recent months, fusion has gained momentum in the political landscape and was identified by The Draghi report on EU competitiveness as a key solution for closing the innovation gap, advancing decarbonisation for growth, and enhancing energy security, essential characteristics for boosting European competitiveness. CATF recently published a report detailing how the EU could prepare an industrial strategy for fusion energy to target these key action areas identified by the Draghi report. However, for fusion energy to be a driver of European competitiveness, the European fusion ecosystem must modernise and adapt to reflect the progress of the global private fusion energy industry. To support this transformation, the European Commission is currently developing a new fusion energy strategy, expected at the end of the year, to accelerate the deployment of fusion energy as a sustainable energy source.

Nuclear fusion occurs when one or more lighter atomic nuclei combine to form a heavier nucleus, releasing energy in the process. This reaction occurs in nature as the process that powers stars like the Sun, and it is this continuous release of energy that makes life on Earth possible. The rate of fusion reactions is dependent on a sufficient combination of three key factors, called the ”triple product”: pressure (n), temperature (T), and confinement time (τ). When these factors reach a critical threshold, known as the “Lawson Criterion,” the energy produced by fusion reactions exceeds the energy required to create the necessary conditions, resulting in “scientific breakeven”.

What Is Fusion?

The reaction between deuterium and tritium (D-T reaction) has the lowest temperature requirement for fusion reactions, and is therefore the favored fusion fuel for for a majority of private sector fusion startups. It is important to note that the process to generate a fusion reaction is completely different from the one needed for fission (as in contemporary light-water reactors). That means fusion will require new and distinct regulations.

Unlike fossil fuels, fusion energy does not emit greenhouse gases. Transitioning to fusion power can significantly reduce carbon footprints, preserve natural resources, and foster a cleaner environment for future generations. Deuterium-Tritium (DT) fusion energy machines will require the abundant fuel resource of deuterium, which can be extracted from seawater at scale, and tritium, which is planned to be bred from lithium blankets within fusion energy machines. The near-unlimited, geographically distributed fuel resources necessary for fusion energy therefore offers an opportunity to secure energy independence, as the ability to deploy fusion energy will be determined by technological know-how, not resource endowments. With an ample supply of fuel, fusion energy offers an opportunity for long-term energy security and relief from concerns over resource scarcity. As fusion is self-limiting, it is inherently safe as there is no possibility of a chain reaction. Moreover, fusion machines produce lower-level radioactive waste. While significant progress has been made in fusion research, several challenges persist on the path to commercialisation. Most D-T fusion reactions produce high-energy neutrons, which can activate surrounding materials, especially structural components. To address this, reduced-activation ferritic-martensitic steels (such as EUROFER97) are being developed; these materials can be classified as low-level waste approximately 100 years after service. However, fusion generates significantly lower levels of radioactive material compared to nuclear fission and does not produce long-lived radioactive waste.

As fusion startups progress towards producing electricity for the grid, clear, specific, and proportionate regulations are also needed to provide a consistent framework for developers and to streamline processes like licensing and siting. Meeting this need will require collaboration and coordination between governments to establish a global fusion industry with a global market.

The State of Fusion in Germany

Germany is a global leader in fusion energy, home to the world’s largest stellarator, and the only country with both a large tokamak and a stellarator-type fusion device. The Karlsruhe Institute of Technology and the Max Planck Institute for Plasma Physics in Garching and Greifswald, alongside the private companies Proxima Energy, Marvel Fusion, Focused Energy, and Gauss Energy, are at the forefront of advancing fusion development. Significant public funding has supported Germany’s advancements in fusion. The Federal Ministry of Education and Research launched a program to invest over one billion euros until 2029, although the budget has only slightly increased since the announcement in September 2023. The recent coalition paper also acknowledges fusion energy as a strategic research priority in the European context. Furthermore, the state of Bavaria had announced investments of 100 million euros by 2028 for fusion research.

Facilitating Fusion

Germany should now leverage its innovative potential and accelerate the commercialisation of fusion energy technology while growing its domestic fusion industry. Apart from delivering on its funding promises, the government must set up a legal framework and foster public-private sector collaboration, as well as collaboration with other governments.

Action 1: Establish a Legal Framework to Ensure Certainty for Investors and Developers

Given the significant differences between fission and fusion, the existing nuclear legislation does not apply to fusion technology, making a new regulatory framework necessary. Rather than waiting for an EU-wide proposal, Germany—Europe’s leader in fusion—should move forward with its own legislative framework that can serve as a model for future aligned regulations across the EU. The planned pilot project for a legal framework, which should be launched this year, is a good starting point but has not seen concrete action. Germany needs to design a framework that provides certainty to developers, investors, and companies now, so that the country can catch up with its counterparts in the U.S. and UK.

Action 2: Foster Public-Private Collaboration and with other Governments

Fusion has traditionally been studied and developed within the public sector, including at national laboratories, universities, and publicly funded research institutions. This public structure has resulted in a strong culture of international collaboration.

Given this growing private sector interest and the vast expertise of Germany’s public sector institutions on fusion, the government should actively foster collaboration between the public and private sectors to ensure funding and continued innovation leadership. Furthermore, to fully realise the potential of fusion energy, Germany should foster collaborative efforts among governments, research institutions, and private entities. The fusion community’s global cooperation is instrumental in advancing research, sharing knowledge, and accelerating the development of fusion technology. By pooling expertise and resources, the country can overcome technical barriers, fast-track progress, and unlock the transformative power of fusion energy.

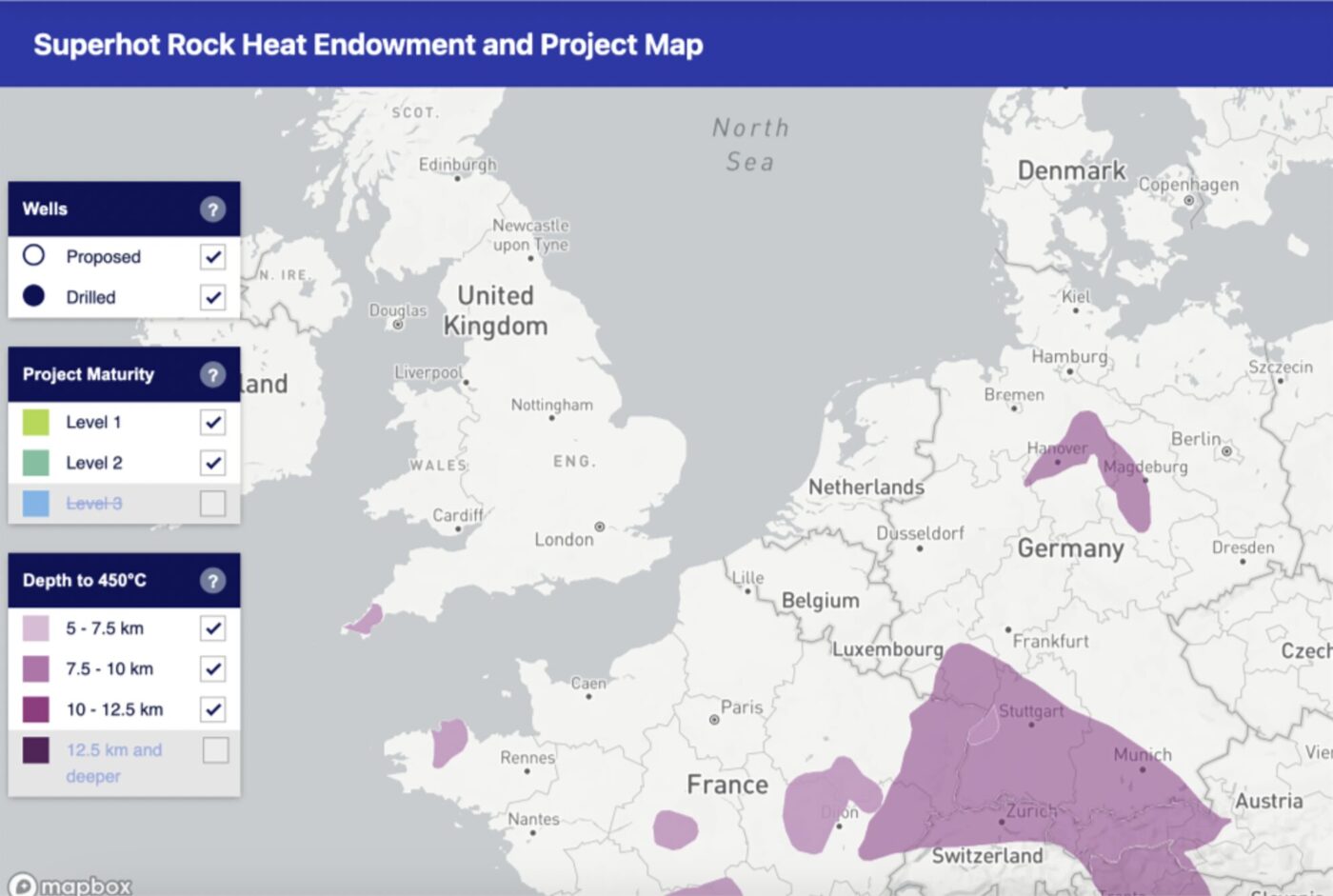

3.5 Superhot Rock Geothermal Energy