Clean Firm Electricity Technologies: What, Why, How

Achieving an affordable, reliable, and abundant clean energy future will require electricity systems to grow while rapidly decarbonizing. Delivering a reliable, least-cost power system will depend not only on scaling renewables, storage, and demand-side solutions, but also on deploying clean electricity technologies with complementary capabilities. Much like a well-balanced investment portfolio, a diversified technology mix offers advantages over long time horizons.

One category of clean energy technologies with significant untapped potential, and the focus of this report, is “clean firm” generation — dispatchable, low-emission electricity generation sources that do not rely on the weather. This group includes nuclear fission, fusion, geothermal energy, fossil generation with high levels of carbon capture and upstream methane mitigation, and combustion or gasification of sustainably sourced biomass or low-carbon synthetic fuels (such as low-carbon hydrogen1). While each of these technologies has unique characteristics, their common value lies in the ability to reliably deliver clean electricity whenever and for as long as it is needed. Some of these technologies also have additional beneficial characteristics, including low land use, flexible siting, reduced transmission infrastructure requirements, and low critical mineral requirements.

Clean firm generation technologies can act as key enablers of cost-effective and risk-resilient decarbonization. Academic- and industry-led electricity systems studies have consistently demonstrated2 that deployment of clean firm resources drastically reduces the scale of the infrastructure buildout necessary to achieve decarbonization. These studies conclude that the cost of fully decarbonizing the electricity sector could be significantly lowered through the development and cost-effective commercialization of one or more clean firm generation technologies, even with the complementary deployment of batteries and demand response. Furthermore, the siting flexibility and reduced material and infrastructure requirements of certain clean firm generation technologies could offer solutions to the most pressing — and likely persistent — deployment challenges.

The need to advance clean firm technology options is as pressing today as ever. Increasing electricity costs,3 concerns about reliability,4 projected but uncertain load growth,5 and the backsliding of climate progress6 are putting more pressure on clean energy strategies to achieve decarbonization at lower costs. If growing electricity demand is to be met and economy-wide decarbonization is to be achieved in the coming decades, clean firm generation technologies could be essential pieces of the solution, provided they are commercially available and deployable.

To unlock the benefits of clean firm generation technologies, however, challenges facing their commercialization or deployment must be addressed. One initial barrier is the exclusion of clean firm generation technologies from clean electricity policy. Some government clean energy targets currently exclude clean firm technologies from eligibility for certain incentives7 and some jurisdictions ban the deployment of certain forms of clean firm power altogether.8 Few governments have taken efforts to accelerate commercialization of clean firm generation technologies.9

Beyond exclusion from existing policy frameworks, challenges facing clean firm generation commercialization and deployment include, but are not limited to, early-stage project costs and risks, policy gaps or uncertainty, and electricity system planning shortfalls. For technologies that are proven, such as existing nuclear technologies, next-generation geothermal, and carbon capture, these barriers have stymied deployment. For more nascent emerging technologies, these challenges have so far resulted in a persistent lack of early-commercial stage clean firm financing and, by extension, deployment and technology progress. This creates a negative feedback loop where near-term deployment deficiencies result in stagnant technological progress and continued perceptions of financial risk, further stunting deployment.

To help overcome near-term barriers and unlock the long-term benefits of clean firm power, policy levers are available across all levels of government. To achieve success, policymakers need to work along two parallel paths: first, enabling near-term deployment of clean firm generation technologies to support technology commercialization and cost reduction, and second, implementing long-term planning and policies that enable optimal integration of clean firm generation technologies into the electricity sector.

The commercialization of clean firm power technologies must serve as a complement—not a substitute—for ambitious reforms that directly address near-term deployment barriers for currently commercialized clean technologies, like solar, wind, and storage. Most clean firm generation technologies will not be widely deployable in the next five years to meet near-term load growth. Moreover, even with cost-effective and available clean firm generation technologies, significant buildout of renewables, storage, transmission, and demand response will be needed in the long-term. But if the commercialization of clean firm generation technologies can be accelerated in the near term, their future availability will help the electricity system decarbonize faster, more affordably, and with resilience.

This report aims to describe the potential role of clean firm power technologies in electricity sector decarbonization and how this potential can be realized. The report is segmented into three parts:

- What: Clean firm generation technology options and their current statuses.

- Why: Clean firm generation technologies’ potential to lower the system costs of decarbonization and manage decarbonization speed and scale risks, while providing reliability.

- How: Policy actions that can overcome barriers and accelerate clean firm generation technologies’ commercialization.

Overall, this report presents a case for policy actions that support the commercialization of clean firm generation technologies and unlock their many potential benefits, in parallel to continued action to remove the barriers currently constraining the pace of deployment of currently commercialized solutions like wind, solar, storage, and transmission.

What are Clean Firm Generation Technologies?

Clean firm generation technologies are dispatchable, low-emission electricity generating resources that do not rely on the weather. They are distinguished by their ability to generate clean power on demand for an effectively indefinite period of time. This report focuses on clean generation technologies that are firm at an individual asset level, and does not include portfolios of multiple generation, storage, and demand-response technologies in its definition of “clean firm generation.” Portfolios can approximate the capabilities of clean firm generation technologies but as discussed later in this report, may require very large amounts of generation and storage capacity to do so and can come with other tradeoffs.

Clean firm generation technologies include geothermal, nuclear fission and fusion, fossil with high levels of carbon capture and upstream methane mitigation, and biomass or clean synthetic fuel combustion with sustainable low-emission fuel sourcing (e.g., low-carbon hydrogen). The commercial readiness of these technologies varies. Many have been technically demonstrated at or near commercial scale, but still face cost, supply chain, or other infrastructure and financing challenges. Others remain more nascent, requiring additional research, development, and demonstration to achieve commercial readiness. Below, we dive deeper into each of these technology options.

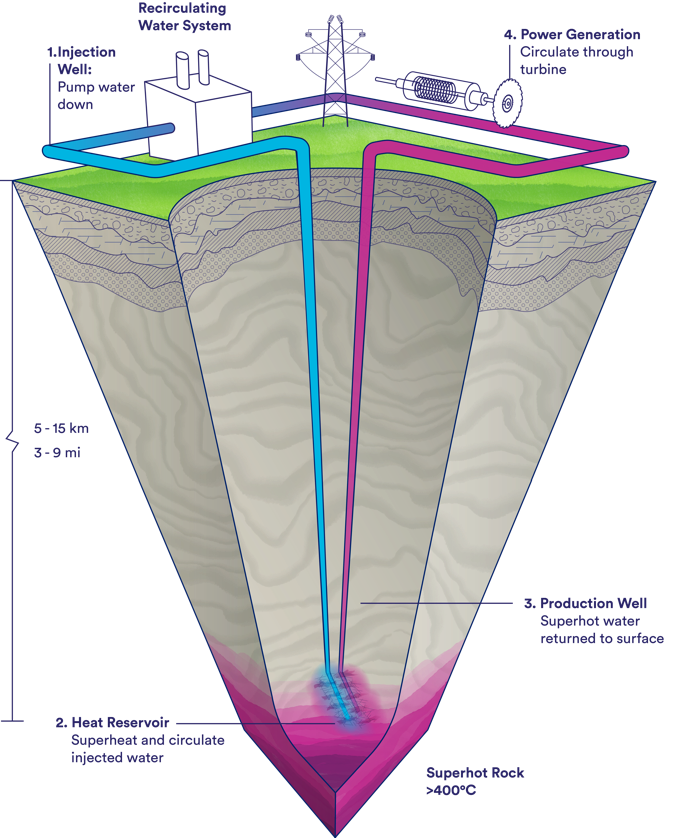

Geothermal

Geothermal power plants use natural heat sourced from deep underground to produce energy. Using water (or another fluid), the earth’s heat is brought to the surface, where it is used to spin a turbine to produce electricity.

Conventional geothermal power (sometimes known as “hydrothermal”) is an established technology that produces power from naturally occurring underground pockets of hot water or steam. Hydrothermal power has been utilized for over a hundred years. But hydrothermal reservoirs are rare and geographically concentrated, which limits the amount of energy that this technology can produce and the locations in which it can be utilized.

Recent innovations in “next-generation” geothermal technologies have made geothermal energy utilization possible in more places, dramatically expanding its potential. Rather than being dependent on preexisting pockets of hot water, next-generation geothermal works in dry rock, circulating water through this rock to extract heat. There are multiple mechanisms for producing next-generation geothermal: enhanced geothermal systems (EGS) create artificial reservoirs by fracturing hot rock, closed-loop geothermal systems (CLGS) circulate fluids through sealed wells without interacting with the surrounding rock, and various hybrid systems blend elements of both EGS and CLGS. Regardless of approach, what next-generation geothermal systems have in common is that they enable geothermal development across a much larger geographic range than was possible before.

Geothermal power development has traditionally targeted resources at temperatures moderately higher than the boiling point of water. Superhot rock geothermal (SHR) is a next frontier in geothermal energy that targets even higher temperatures found deep within the Earth’s crust, where water can become a supercritical fluid—a phase of matter that transfers heat more efficiently than either steam or liquid water. This opens up the possibility of extracting far more energy per well than traditional or current next-gen systems, expanding the geographic range of availability and drastically reducing cost.

In the power sector, geothermal holds the potential to deliver large-scale, around-the-clock clean electricity, thanks to its independence from weather and relatively low mechanical complexity. Geothermal systems commonly achieve availability factors between 90% and 96%—comparable to nuclear energy.10 They also require relatively little land compared to other clean energy sources and could be deployed in many regions using existing oil and gas infrastructure and workforce expertise. Finally, this technology has the capacity to scale to meet growing demand. Early modeling and CATF’s mapping suggests SHR could provide over 4 terawatts of potential capacity in the U.S., supporting up to 8 times the United States’s 2021 electricity consumption, and that just 1% of the heat available in Europe could power the equivalent of 1400 Berlins.

However, next-generation geothermal technologies face key challenges before reaching commercial scale. For next-gen systems operating at today’s accessible temperatures, the main needs are larger-scale and longer-term technology demonstration, better data sharing, and expanded development in a wider range of geological settings. For SHR systems, further innovation is required in high-temperature drilling tools, materials, and reservoir creation methods. Demonstration sites that allow for controlled testing in superhot conditions will be essential. While that innovation is within reach, government R&D support and policy support— similar to those that helped catalyze the shale gas boom — will be critical to accelerating the learning curve and realizing the full potential of next-generation geothermal.

Figure 1. Illustratiion of superhot rock geothermal plant.

Nuclear Fission

Nuclear fission occurs when a neutron slams into a large atom, forcing it to excite and split into two smaller atoms—also known as fission products. Additional neutrons are also released that can initiate a chain reaction. When each atom splits, a tremendous amount of energy is released. Nuclear power reactors use heat produced during atomic fission to boil water and produce pressurized steam. The steam is routed through the reactor steam system to spin large turbines and produce electricity.

Approximately 400 GW of nuclear fission capacity is installed worldwide today, delivering just under 10% of the world’s electricity.11 It is a cornerstone of several developed economies— in the U.S., it accounts for roughly 20% of electricity generation and half of its clean generation.12 Similarly, across the EU, nuclear fission generated 24% of electricity consumed in 2024, making it the single biggest contributor to clean electricity production.13 The technology plays a vital role in ensuring energy security, driving economic development, and meeting emission reduction targets. Beyond providing clean, firm power to complement growing renewables as electricity demand rises across many jurisdictions, emerging new nuclear designs can also be engineered to deliver direct medium-to-high-grade heat, potentially contributing to the decarbonization of other “hard to abate” sectors.

Despite its potential, the deployment of new nuclear reactors faces significant hurdles. The majority of the currently operating reactor fleet worldwide were built decades ago, and the industries supporting these large, capital-intensive projects have since atrophied due to shortage of new nuclear construction. The lack of an established industrial base and workforce can lead to project delays and cost overruns, which have been a feature of one-off nuclear projects during the 21st century (e.g., the Vogtle 3 and 4 reactors in the United States).

In the U.S., growing bipartisan support for nuclear fission and recent executive actions are aiming to advance nuclear energy. But a comprehensive strategy for commercializing and deploying new nuclear plants/reactors at scale has yet to be established. Utilities, private developers, large load customers, regulators, policymakers, and local communities will need to work together to overcome the barriers14 facing new builds by exploring demand aggregation and hybrid revenue models that blend public and private investment until the advanced nuclear energy market has reached maturity and build deployment confidence with a robust supply chain, an efficient, effective, and predictable regulatory environment, and a developed workforce.

A comparable scenario exists across the European continent, where numerous EU member states have expressed ambitious intentions regarding nuclear deployment. Nevertheless, policy, financing, and regulatory gaps remain that must be addressed before the potential of the forthcoming wave of nuclear deployment can be fully realized.

Fusion Energy

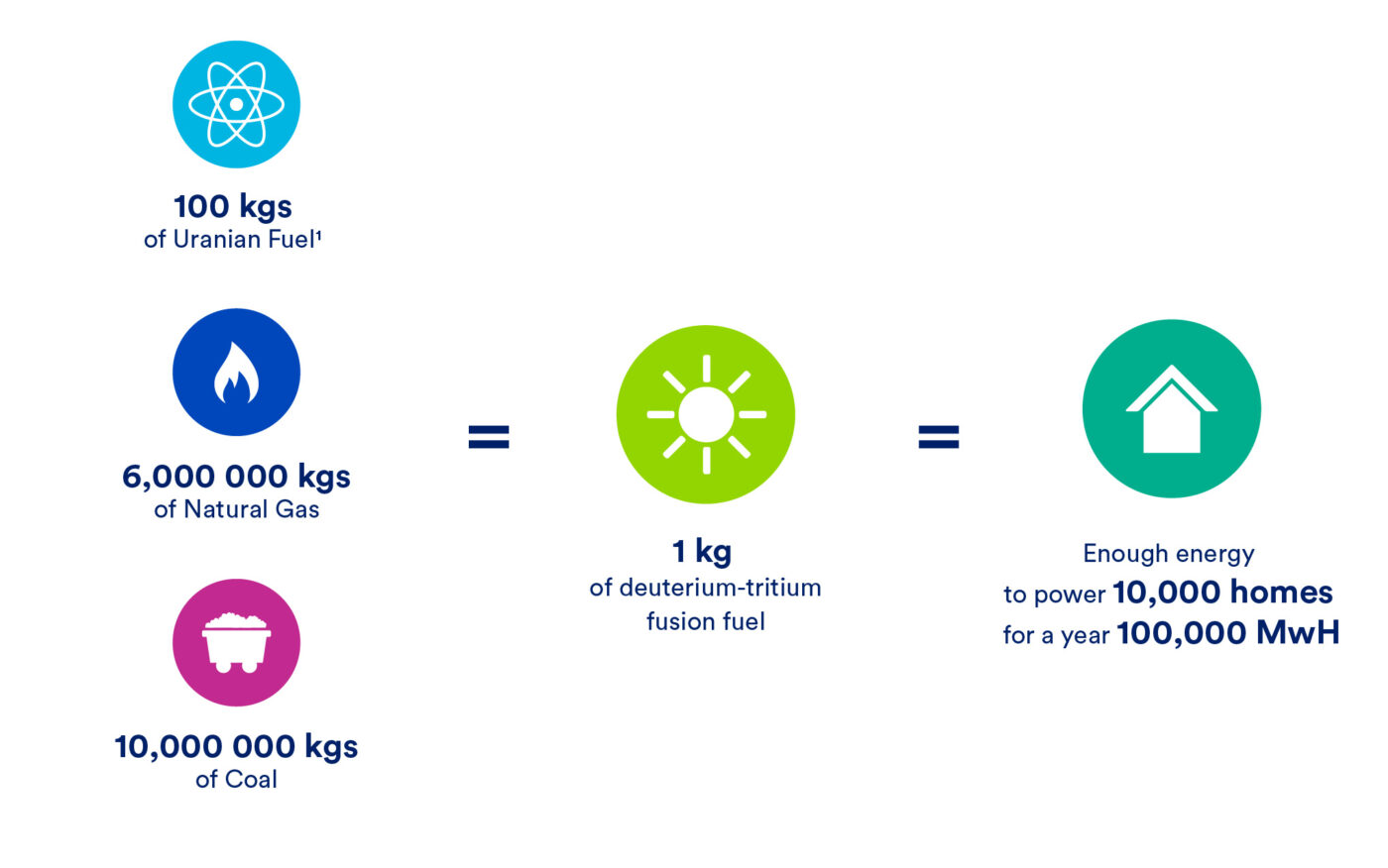

Fusion technology aims to replicate the natural processes that power the sun, where small atomic nuclei combine to form a larger nucleus, releasing an immense amount of energy. Fusion machines create the necessary high temperatures and pressures for enough time for these reactions to occur, but maintaining the extreme conditions necessary for fusion reactions to occur is technologically complex. This technology holds the promise of producing energy with minimal environmental impact, generating only low-level waste and using abundant fuel sources that can be found on Earth.

Figure 2. Illustration indicating the energy density of fusion fuel in comparison to other sources and consumption amounts.

Despite significant progress made in the last decade and key scientific and engineering breakthroughs, fusion power is not yet commercially available. Private sector firms estimate that there will be commercially viable machines in the next decade. The technology available is still largely experimental, and further development and testing of key reactor subsystems and systems will be required to achieve net-positive energy output — a key milestone for commercial viability. Furthermore, regulatory frameworks and technology-specific policies will be critical factors in the successful integration of fusion energy into the electricity sector. Ongoing work in the U.K. and U.S., where regulatory frameworks are being developed provide good examples of how to create a fusion industrial sector.

The economic challenges faced by fusion projects are considerable and multifaceted. One of the primary issues is the high initial capital investment required for research and development, as well as for the construction of experimental and demonstration machines. Technology risk and long commercialization timelines can deter private investment, as investors often seek quicker and lower-risk returns on their capital.

Fossil Energy with Carbon Capture and Storage

Carbon capture and storage (CCS) technologies separate the carbon dioxide (CO2) emitted by point sources and inject it into deep geological formations for permanent storage, thereby preventing its release into the atmosphere. In the electricity system, CCS can be retrofitted to existing gas or coal power plants or integrated into new power plant designs. In most current proposals, CO2 is separated from standard power plant flue gas, but other demonstrated approaches include the combustion of fuel in oxygen and CO2 (oxyfuel combustion) or the separation of CO2 from syngas produced by coal gasification (pre-combustion capture). Captured CO2 is typically purified, compressed, and then transported to suitable locations for safe underground storage.

CCS at high capture rates and paired with upstream methane controls can provide dispatchable power as the electricity system transitions. CCS-enabled power plants can fulfill different operational roles, either as baseload generation resources or flexibly ramping up and down to complement variable renewables. Following a decade of technical progress and significant policy support in some regions, the first large-scale gas power plants with CCS are now being deployed in the U.S. and the U.K.15 To further scale CCS, increased incentives and developing transport and storage infrastructure, proactively engaging with public stakeholders to address community concerns, and other policy and industry actions will be needed.

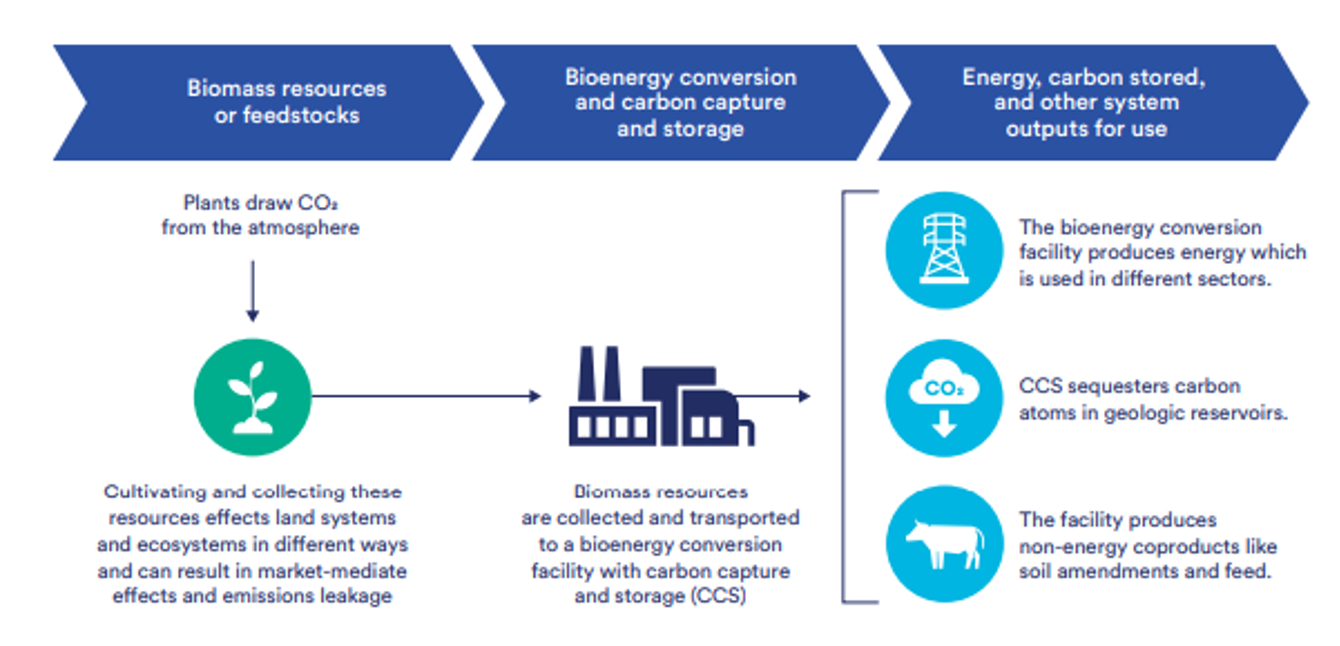

Bioenergy with Carbon Capture and Storage (BECCS)

Bioenergy with carbon capture and storage (BECCS) systems combine processes for converting biomass resources or feedstocks into usable forms of energy with technologies for capturing and permanently storing CO2 emissions. These systems offer the potential to remove CO2 from the atmosphere while supplying zero- or lower-carbon energy on a lifecycle basis.

Thermochemical BECCS systems, such as combustion and gasification, can generate electricity for the power sector while also sequestering atmospheric carbon in geologic storage. These thermochemical processes are generally flexible in terms of the biomass resources they use, but are typically most practical with low-moisture, high-lignin feedstocks, such as forest thinnings or dedicated energy crops like poplar. BECCS for power via gasification (to produce syngas which can be combusted in a gas turbine or combined cycle system) offers advantages over direct combustion, including higher efficiency and a more concentrated CO2 stream for capture and storage however, it is technically complex and less mature at scale.16

BECCS in the power sector is expected to be limited to around 5% of power production globally,17 and to be used as a complement to variable renewables by dispatching electricity to the grid when their generation is limited. Generally, the use of biomass for power is viewed as a less ideal pathway for utilizing biomass resources in comparison to other difficult-to-abate sectors. Still, BECCS has the potential to produce power and remove hundreds of millions of metric tons of CO2 annually at less than $100 per ton in the U.S.18

Despite the potential to deliver net-negative greenhouse gas emissions, BECCS for power faces several significant challenges, including the sustainable sourcing of biomass resources, establishing supply chains for climate-beneficial feedstocks, scaling carbon capture and storage infrastructure, high capital costs, and technological advancements in bioconversion.

Figure 3. Flow of biomass resource or feedstocks to bioenergy with carbon catpure and storage and other system outputs.

Clean Hydrogen

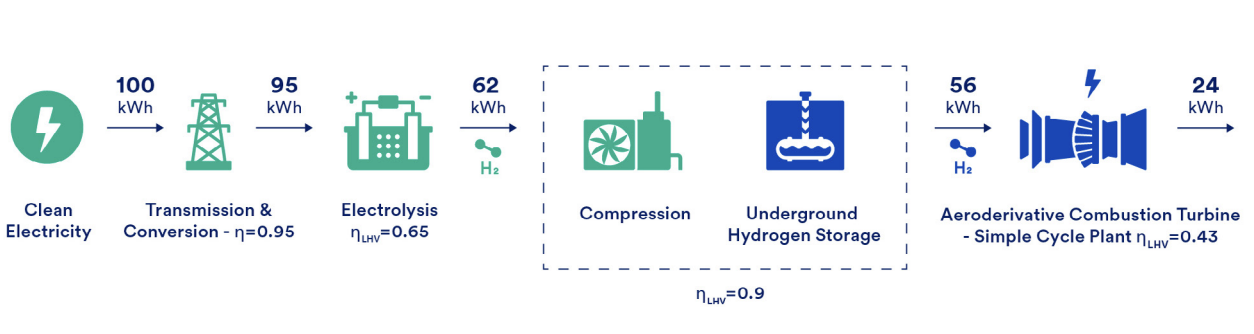

The combustion of hydrogen in power plants generates water vapor as its only direct by-product and can reduce greenhouse gas (GHG) stack emissions to zero in theory. Therefore, it is technically feasible for hydrogen that was produced with minimal upstream emissions to be used to generate low-emission electricity, whether it be in retrofitted gas plants or new hydrogen-burning turbines.

However, hydrogen is unlikely to play a major role in power systems decarbonization. Low-carbon hydrogen can be produced from natural gas via steam methane reforming with carbon capture and storage, but this option suffers from upstream methane leakage that limits greenhouse gas reduction potential and results in high carbon abatement costs. Meanwhile, ‘green’ hydrogen produced via electrolysis of water using clean electricity and subsequently combusted for power generation has a round-trip efficiency of as little as 24%; three-quarters of the clean electricity used is lost in the process. Therefore, use of green hydrogen as a fuel source in the electricity sector only makes sense when there is a very large difference in value between the electricity used to produce the hydrogen and the electricity the hydrogen is used to generate, and when other higher-efficiency storage approaches are not economical due to limits on duration.

Figure 4. Hydrogen electrolysis and combustion supply chain, while tracking energy losses.

Despite its low efficiency, there may be a niche for hydrogen in the role of ultra-long-duration electricity storage due to the extremely low cost of underground hydrogen storage.19 Hydrogen could also be produced in one location with low-cost electricity inputs and transported to another location for use as fuel. However, this option needs to be evaluated in the context of a full system cost analysis considering other clean firm generation and storage options, including a full account of the necessary infrastructure requirements for hydrogen storage (e.g., hydrogen transport and storage).

For more details, please refer to Clean Air Task Force’s recent paper on the topic here.

Why Clean Firm: Potential Benefits

Power systems face significant challenges ahead. Existing legacy infrastructure is old and requires replacement. Load growth, while uncertain, has returned to many regions at a rate not experienced for decades. For regions with economy-wide decarbonization goals, future load growth from electrification is projected to be similarly steep. Meanwhile, clean supply will need to not only meet new load, but also replace existing unabated fossil generation as these facilities age and grow too expensive to maintain and grids pursue decarbonization.

In this section, we characterize the potential benefits of commercialized and cost-effective clean firm generation technologies. Our characterizations are largely informed by academic energy system studies, which not only assume progression of clean firm technology costs and availability, but also assume significant continued reductions in the cost of other supply- and demand-side decarbonization solutions. In a latter section, we address the near-term challenges facing clean firm technology commercialization.

Commercialization of clean firm generation technologies at reasonable costs will bring three broad categories of benefits:

- Benefit 1: Reducing the infrastructure buildout necessary to decarbonize the power sector while meeting demand growth

- Benefit 2: Reducing the costs of power sector decarbonization

- Benefit 3: Managing risks associated with a limited set of power sector decarbonization options

Benefit 1: Reducing Infrastructure Buildout Needs

Key Takeaways:

- Clean firm generation technologies can reduce the scale of the infrastructure buildout necessary to decarbonize the power system in comparison to pathways without clean firm generation technologies.

- Clean firm generation’s impact on total buildout needs directly reduces the land, material, and critical mineral requirements of decarbonization

The inclusion of clean firm generation technologies in power systems substantially reduces the scale of infrastructure buildout needed to meet load growth and achieve electricity decarbonization, while protecting grid reliability.

Analyses by the International Energy Agency (IEA) suggest global electricity demand is set to increase dramatically by 2050 under all future scenarios, with the most rapid increase occurring after 2030.20 In the U.S. and Europe, most electricity evolution analyses assume significant, often 200%-400%, increases in electricity demand and supply over that same period. Even before considering decarbonization, meeting load growth reliably while replacing aging infrastructure will require significant amounts of new infrastructure buildout. For example, McKinsey projects that Europe will require over 100 GW of new dispatchable capacity by 2035 to maintain reliability and manage costs.21

Infrastructure buildout requirements become even more substantial when pursuing decarbonization. In a scenario modeling a high-renewables pathway to a decarbonized U.S. economy in 2050, Princeton’s Net-Zero America study found that the country would need to deploy four times more wind and solar power than it has ever deployed in a single year, every year for the next two decades, to achieve this goal.22 Total electricity transmission capacity would need to increase by more than 400%.

A key benefit of clean firm generation technologies is their significant impact on the total infrastructure buildout necessary to meet load growth and achieve decarbonization. As discussed below, the presence of clean firm capacity substantially reduces the total generation, storage, and transmission capacity that is required to achieve clean energy targets while maintaining reliability. This reduction in total buildout needs directly reduces the land, material, and critical mineral requirements of decarbonization.23 Moreover, because some clean firm generation technologies can provide heat in addition to power, they could also help directly meet decarbonized heating needs and reduce electricity demand for heat.

A power sector with a robust suite of clean firm generation technologies allows for decarbonization with lower infrastructure requirements for several reasons. First, clean firm resources generally operate at higher utilization rates (50-100%) than variable renewables (20-50%), requiring less total generating capacity to produce the same amount of energy and less transmission capacity to carry it. Second, by providing clean generation that is consistently available for indefinite periods and regardless of weather conditions, clean firm resources reduce the need to overbuild other resources to ensure reliability during extreme conditions. Without clean firm options available, a grid targeting decarbonization must instead be equipped with sufficient wind, solar, storage, and transmission capacity to meet demand even during rare periods of extremely low wind and solar production – far more than is needed to meet demand under typical weather conditions.

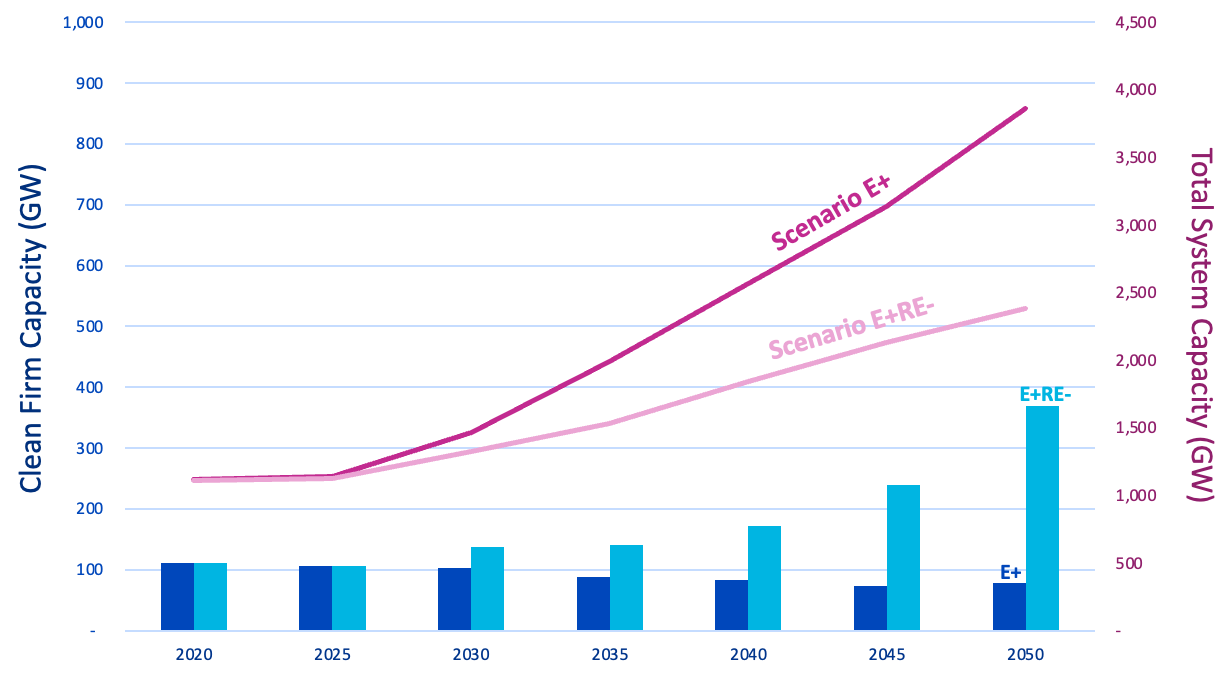

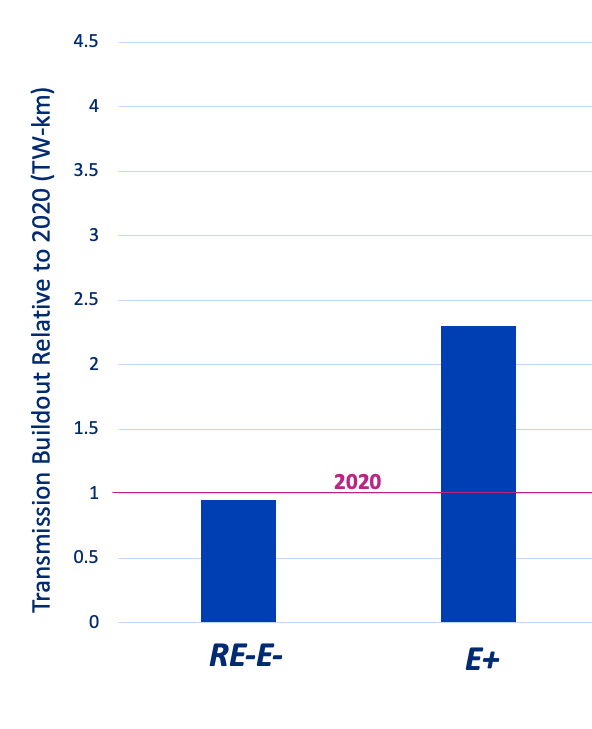

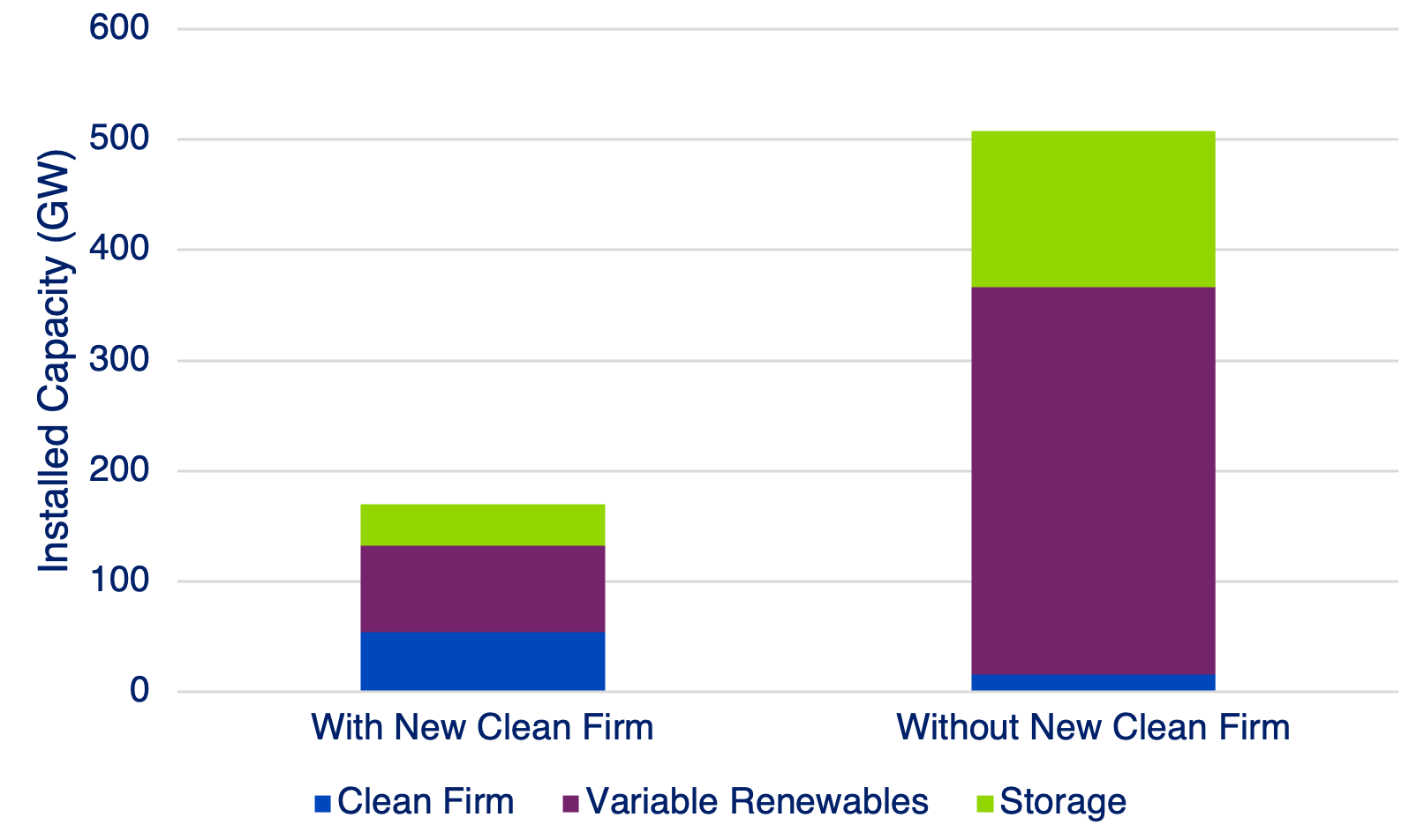

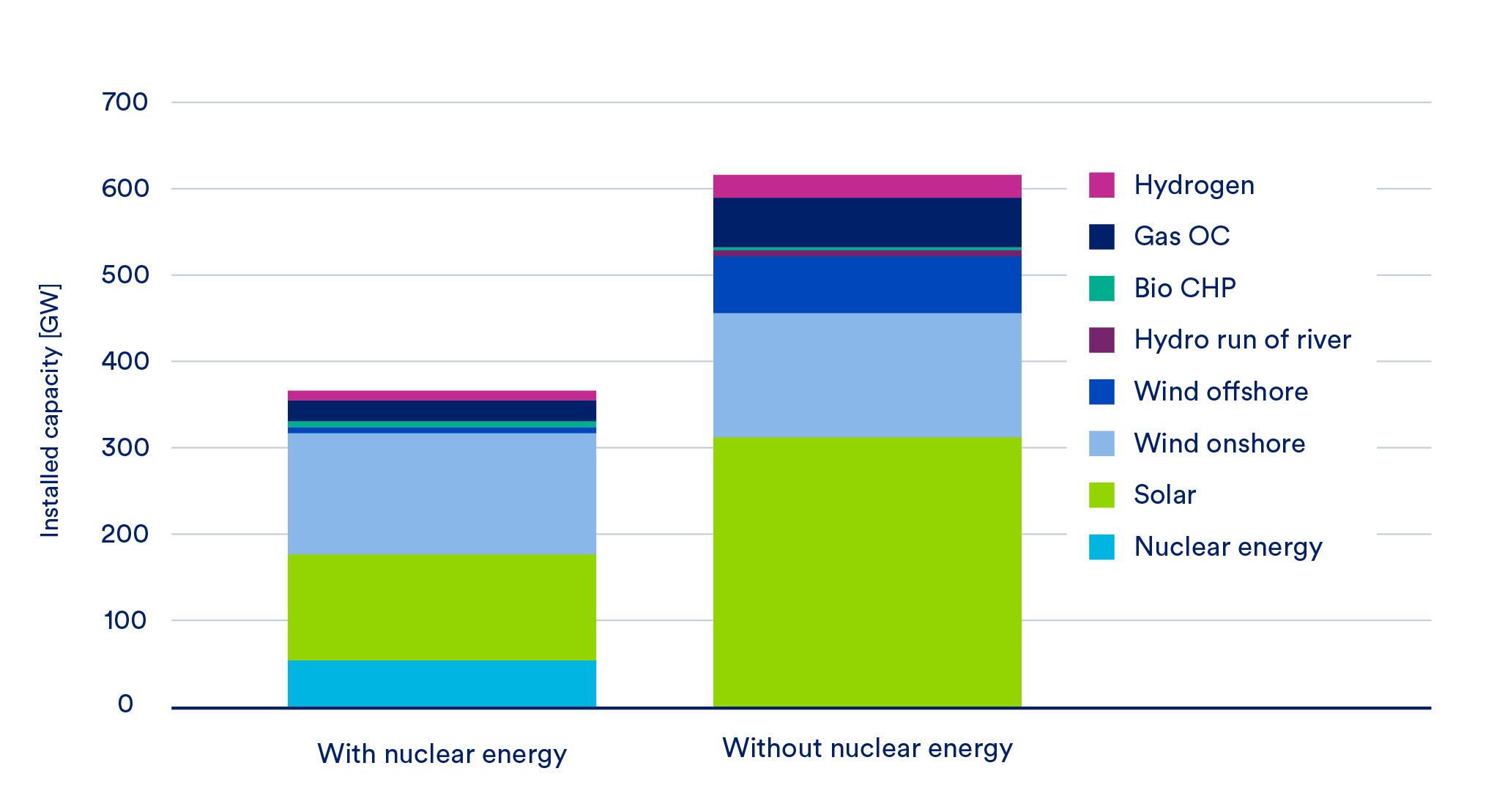

Clean firm generation can have an outsized impact in lowering the total infrastructure needs of a decarbonized grid. For example, the Net Zero America study found that 1 GW of clean firm capacity offsets roughly 5-8 GW of variable renewable and storage capacity needs (Figure 5).24 These impacts apply also to transmission, where clean firm buildout modeled in Net Zero America more than halved total transmission buildout needs (Figure 6). While these scenarios still require rapidly expanding renewables, storage, and transmission, the scale of their required deployment is reduced. Recent increases in future load forecasts, to the extent they materialize, would amplify both the scale of the challenge and the benefits of including clean firm resources. These findings hold for more granular regional studies, such as for California25 (Figure 7), New York,26 and other states. A recent review paper in Europe that summarized many power modeling studies had similar findings, where clean firm technologies reduce the total infrastructure buildout needed to decarbonise Europe-wide and in specific member states (Figure 8).27

Figure 5. Total system capacity (magenta) and clean firm resource capacity (blue) for the E+ (darker color) E+RE- (lighter color) scenarios in the Net Zero America study. Both scenarios assume aggressive end-use electrification, but the E+RE- scenario allows lower rates of wind and solar deployment and higher amounts of CO2 storage than E+.

Figure 6. Transmission buildout needs in 2050 (relative to 2020) for the E+ and E- scenarios in the Net-Zero America study, showing that higher-levels of clean firm deployment reduces transmission expansion by half.

Figure 7. Average installed capacity of clean firm power, variable renewables, and storage required to deliver 100% clean electricity in California in 2024 for scenarios with and without new-build clean firm options available, as analyzed by three different electricity system models.28

Figure 8. Results of power system modeling to achieve a decarbonized German power system by 2050 with (left) and without (right) nuclear power.

Benefit 2: Reducing Decarbonization Costs

Key Takeaways:

- Despite having higher levelized costs of electricity (LCOE) than wind and solar, the system-level impacts of clean firm generation technologies can significantly decrease ratepayer costs of power sector decarbonization compared to scenarios where they are unavailable.

- Clean firm generation technologies are cost-effective even under optimistic assumptions of continued cost declines for variable renewables and lithium-ion battery storage, large-scale transmission expansion, and widespread demand-side technology adoption, all of which are typically incorporated in power system studies.

Clean firm generation technologies can significantly decrease the ratepayer costs of power sector decarbonization compared to scenarios where they are unavailable by reducing the cost of ensuring seasonal supply-demand balancing and extreme weather resiliency.29 As noted in the previous section, the large amount of renewable and storage capacity required to ensure reliability (Figure 7 & 8) without clean firm power technologies means that much of this capacity goes effectively unused during normal weather conditions, significantly increasing the overall cost of decarbonized systems (as shown in Table 1 and 2).

This conclusion holds even under optimistic assumptions of continued cost declines for variable renewables and lithium-ion battery storage, large-scale transmission expansion, and widespread demand-side technology adoption, all of which are typically incorporated in power system studies. Although the availability of ultra-low-cost long-duration energy storage technologies could reduce the need for clean firm options by allowing for more cost-effective seasonal shifting of renewable energy, research indicates that storage costs would need to fall to a tenth or less of today’s lithium-ion battery costs for this option to act as an economically competitive substitute for clean firm power.30 In some cases where a storage medium takes the form of a fuel and can be transported, like electrolysis-derived hydrogen or methanol, the line between clean firm power and ultra-long-duration energy storage becomes indistinct. In either case, the use of long-duration storage to achieve deep decarbonization would still require very large amounts of renewable energy deployment and would therefore not address the infrastructure buildout challenges discussed in the previous section.

Despite having higher levelized costs of electricity (LCOE) than wind and solar, the system-level impacts of clean firm generation technologies can significantly decrease ratepayer costs of power sector decarbonization compared to scenarios where they are unavailable.31 This is because LCOE has significant shortfalls in assessing a technology’s value in power systems:

- LCOE does not consider a system’s needs,

- LCOE does not consider the technology’s generation profile or generation characteristics such as dispatchability and inertia, and

- LCOE often does not account for the full electricity system cost necessary to deploy a generator at a large scale, such as the transmission and distribution infrastructure necessary to deliver power to consumers.

A 2021 review by the Northbridge Group examined 40 studies on deep U.S. decarbonization between 2015 and 2021.32 It found that:

- In decarbonized electricity system models, clean firm options decreased costs by roughly 40-65% (Table 1).

- In full economy-wide models, clean firm generation technologies reduced costs by roughly 30% to 55% (Table 2).

More recent U.S. regional electricity system planning studies, such as those conducted by New England33 and New York,34 continue to find similar results.

Table 1. Summary of calculated cost premiums of highly variable renewable cases compared to a more diversified generation mix in electricity studies.

Cost savings of a diversified generation mix relative to a high variable renewable energy (VRE) strategy: Electricity sector net-zero studies

| Study | Reported Cost Metric | Modeled Scenarios | Average System Cost | System Cost Savings |

|---|---|---|---|---|

| Sepulveda (2018) | Annual Electricity Cost (Two Regions) | VRE and Storage Only (100%) vs. Low-C Firm Resources (20-40%) | $160 – $215/MWh $100 – $105/MWh | 40% – 50% |

| Clack (2019) | Annual Electricity Cost | Renewables Only (100%) vs. 100% Carbon-Free (65%) | $155/MWh $95/MWh | 40% |

| Baik (2021) | Annual Electricity Cost | VRE and Storage Only (N/A%) vs. All Options (N/A%) | $130 – $150/MWh $70-$95/MWh | 40% – 45% |

| Blanford (2021) | Incremental NPV of Cumulative Energy Services Costs | Renewables Only (95%) vs. All Options (55%) | $0.75 T $0.3 T | 65% |

Table 2. Summary of calculated cost premiums of highly variable renewable cases compared to a more diversified generation mix in economy-wide studies.

Cost savings of a diversified generation mix relative to a high variable renewable energy (VRE) strategy: electricity sector net-zero studies.

| Study | Reported Cost Metric | Modeled Scenarios | Average System Cost | System Cost Savings |

|---|---|---|---|---|

| Sepulveda (2018) | Annual Electricity Cost (Two Regions) | VRE and Storage Only (100%) vs. Low-C Firm Resources (20-40%) | $160 – $215/MWh $100 – $105/MWh | 40% – 50% |

| Clack (2019) | Annual Electricity Cost | Renewables Only (100%) vs. 100% Carbon-Free (65%) | $155/MWh $95/MWh | 40% |

| Baik (2021) | Annual Electricity Cost | VRE and Storage Only (N/A%) vs. All Options (N/A%) | $130 – $150/MWh $70-$95/MWh | 40% – 45% |

| Blanford (2021) | Incremental NPV of Cumulative Energy Services Costs | Renewables Only (95%) vs. All Options (55%) | $0.75 T $0.3 T | 65% |

Modeling of European power systems has shown similar results. In a meta-analysis, Quantified Carbon reviewed sixteen modeling studies with varying regions and approaches.35 While exceptions exist for countries with a very high proportion of flexible hydropower resources (e.g., Denmark, , which has transmission to access the hydropower of surrounding countries) and where models force too much clean firm generation (e.g., 100% clean firm generation), most of the reviewed studies show that systems with clean firm generation have lower costs and lower power price volatility than scenarios without clean firm generation.

In Southeast Asia, clean firm generation technologies can address power demand growth, fossil plant retirements, and declining hydropower production. To date, the majority of power demand growth in this region has been fueled by coal and natural gas. Clean firm generation technologies could provide lower-carbon, less-polluting alternatives, especially in regions with land availability constraints or low-quality renewable resources.36,37 Similarly in Africa, where energy demand is projected to rise rapidly over the coming decades, clean firm resources could play a key enabling role in the simultaneous expansion and decarbonization of electricity supply.38

Modeling Method Shortcomings that Impact Clean Firm Valuation

It should be noted that the electricity sector models used in these analyses likely underestimate the full value of clean firm resources (as well as other technologies like long-duration energy storage and demand response) by simplifying or omitting real-world constraints such as transmission bottlenecks, extreme weather events, and operational reliability constraints—all areas where clean firm resources provide additional cost savings and reliability benefits. Optimization models also schedule the operation of renewables and storage with perfect foresight (typically over an entire year), which artificially decreases the forecasting challenges associated with these resources. The significant financial benefits identified in the above studies can therefore be considered a lower bound on the value of clean firm power. However, it should also be noted that these models also often ignore challenges with clean firm buildout or operations, such as availability of cooling water to operate power plants.39

Benefit 3: Increasing Decarbonization Speed and Resiliency via Technology Diversity

Key takeaways:

- Clean energy deployment rates remain well below what would be necessary to achieve zero-emissions grids by 2050.

- Clean firm generation technologies’ impact on power systems can reduce the overall scale of the decarbonization challenge, making targets more achievable.

- Clean firm generation technologies complement renewables and storage, mitigating risks that affect technologies asymmetrically that may stall decarbonization.

Electricity sector decarbonization faces significant uncertainties and risks that could derail success. These include logistical and regulatory barriers to large-scale clean energy deployment, supply chain shocks, geopolitical conflict, and uncertainties in the long-term evolution of technology costs and energy demand. Clean firm generation technologies present policymakers with options to reduce uncertainty and mitigate risks to achieving power sector decarbonization.

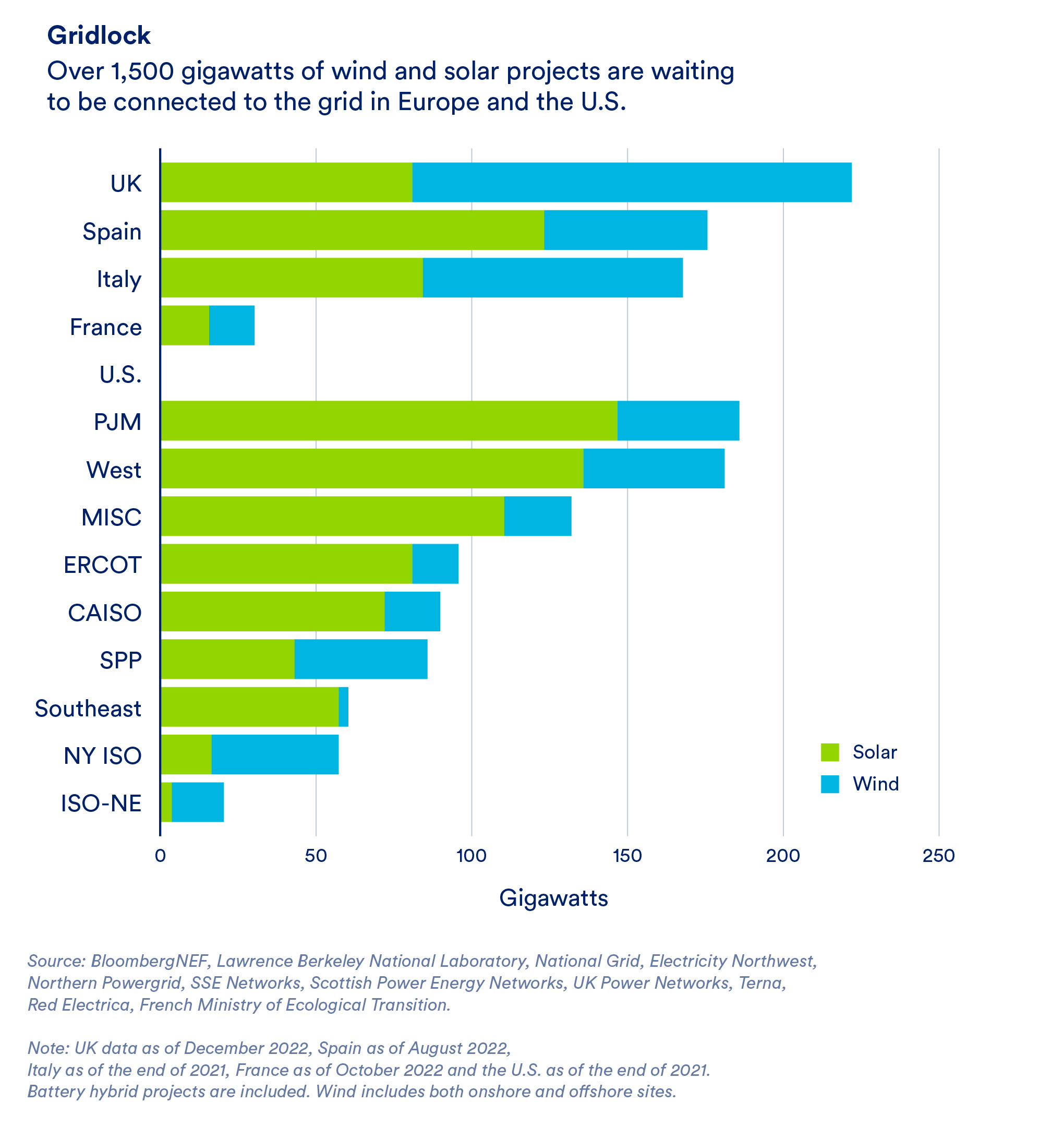

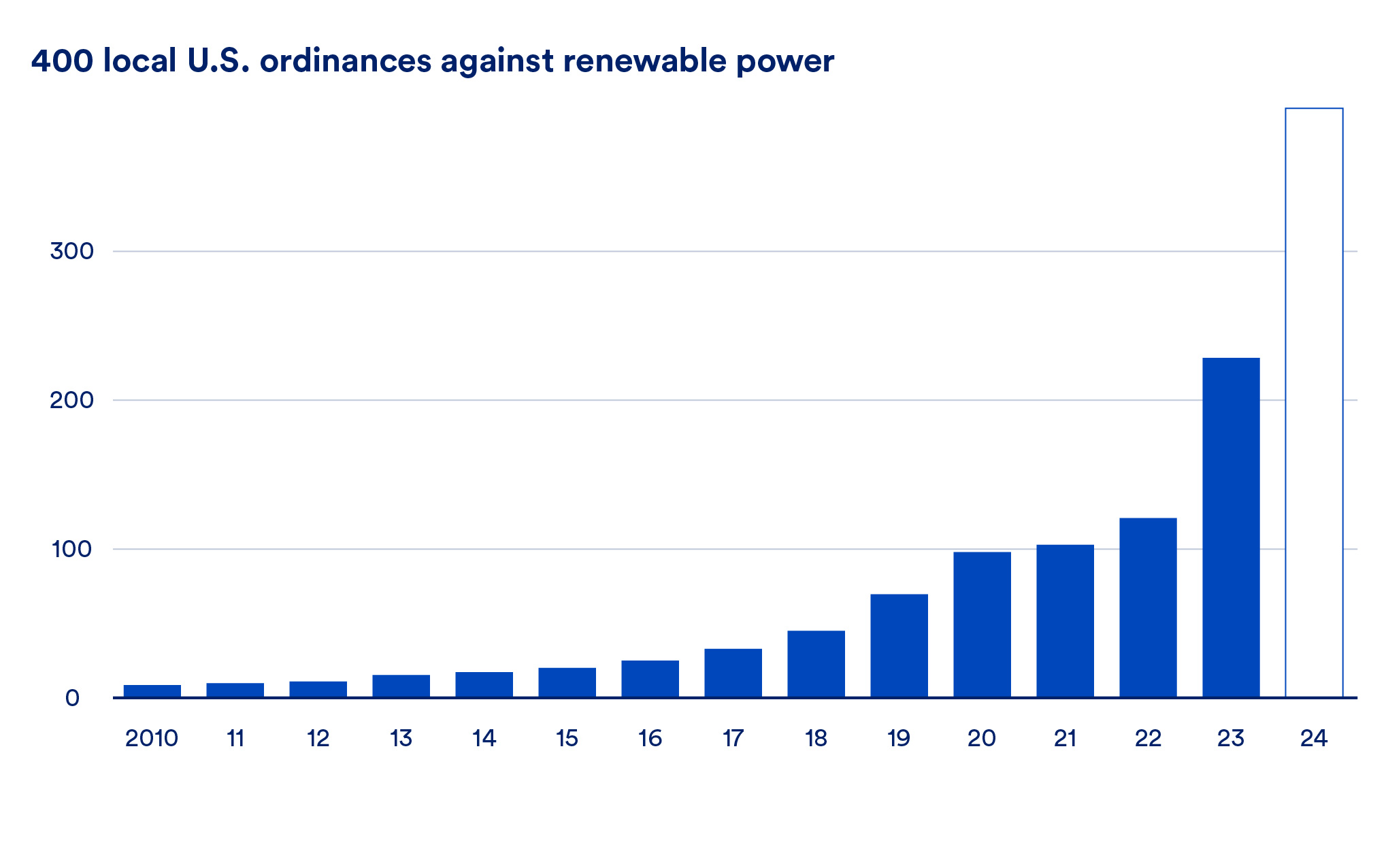

In the United States and Europe,40 project siting barriers, lack of transmission capacity, and interconnection queue backlogs have limited the pace of clean energy supply growth despite rising demand and policies designed to accelerate their deployment (see Figure 9). Although clean resources still account for the large majority of new generating capacity additions in these regions, deployment rates (particularly of wind power) remain well below what would be necessary to achieve zero-emissions grids by 2050.41 These barriers are all technically surmountable and policymakers are making progress on addressing some of them (e.g., interconnection queue reform efforts intended to reduce project development timelines). But challenges that limit clean energy growth may persist, and new challenges related to supply chain capacity or trade conflicts, may emerge.

Figure 9. Top: U.S. and European interconnection queues (BNEF, 2023). Bottom: Number of local ordinances against renewable power (Sabin Center of Climate Change Law, 2024).

The following is a non-exhaustive list of practical and procedural barriers that must be overcome to accelerate clean energy deployment:

- Reforming transmission planning processes to enable large-scale regional and interregional transmission and new transmission technologies (e.g., grid enhancing technologies);42

- Improving interconnection queue processes to connect clean energy resources faster;43

- Overcoming siting and permitting barriers while maintaining safeguards for the environment and community interests;44

- Updating market designs to better incentivize demand-response and enable easier variable renewable energy integration into power systems,45 and to adequately incentivize long-lead time and long-lived resources like clean firm resources;46

- Including the impacts of climate change and extreme weather in reliability and resiliency planning to improve the valuation of clean resources and ensure adequate complementary solutions;47

- Improving utility planning processes to be more proactive, long-term, transparent, and sophisticated;48

- Enacting new utility business models that incentivize performance (e.g., cost efficiency), not just capital expenditure, to enable utilities to deploy more novel supply- and demand-side solutions;49

- Enhancing rate design to include time-varying rates and real-time pricing for large customers;50

- Engaging local communities and landowners to proactively identify and solve future siting challenges;51

- Expanding supply chains rapidly to enable clean energy deployment at the necessary scale in the face of various uncertainties;52 and

- Managing economic and employment outcomes to ensure a just transition for workers and communities.53

Overcoming these challenges will require many stakeholders at different levels of government to rapidly reform incentive structures, needs assessment analyses, planning processes, and governance. If any single major challenge—such as siting resistance, supply chain bottlenecks, or permitting delays—is not fully overcome, decarbonization could stall. In this scenario, the failure of jurisdictions to achieve growth rate targets would not be because clean energy wasn’t cheap enough, but instead because it faced non-cost barriers. Policymakers at any single level of government—particularly local governments—frequently do not have the legal authority or tools to directly address all potential risks, and coordination challenges between and within governments abound.

Promoting the use of diverse technologies, including clean firm generation options, can help reduce the scale of these non-cost barriers that limit decarbonization. As discussed above, the deployment of clean firm resources can substantially reduce the amount of generation, storage, and transmission capacity that must be deployed to decarbonize the electricity sector. In doing so, clean firm technologies can minimize the impact of non-cost barriers that slow the pace of deployment.

In addition to reducing the overall severity of potential infrastructure buildout barriers, the inclusion of more technology solutions means that risks that affect technologies asymmetrically are less likely to become severe bottlenecks to decarbonization. If one technology pathway faces unique constraints at any point in time or in any region, a diverse technology portfolio ensures that other options are available to fill the gap. Through their unique characteristics, clean firm generation technologies can reduce electricity sector risk exposure in the following ways:

- Diversified resource and manufacturing needs can mitigate exposure to risks facing any individual technology’s supply chain.

- Lower land use by clean firm resources per unit of energy and capacity can reduce the overall footprint of a decarbonized system and in turn reduce siting and public opposition challenges.54

- More flexible project siting and higher transmission utilization require less greenfield transmission build.55

- Lower critical mineral requirements for some clean firm generation technologies can mitigate supply chain and/or trade uncertainties.56

- Lower exposure to global commodity markets mitigates exposure to global conflict shocks.

- Higher concentration of local economic benefits, including jobs — if well communicated and coupled with meaningful community engagement — could ease public acceptance risks.57

- Combined heat and power applications can help directly meet heating needs, reducing dependence on other approaches to decarbonized heat.58

Challenges and Policy Strategies for Clean Firm Generation Technologies

Challenges for Commercializing Clean Firm Generation Technologies

Despite their many benefits, clean firm generation technologies are not without their challenges. None of the clean firm technologies covered in this report are currently experiencing rapid deployment in the developed world, and some are too nascent to have seen any deployment at all. Nuclear power is a significant component of many electricity systems worldwide (10% of global generation in 202359), but large-scale nuclear power development in North America and Europe effectively ceased decades ago, with only individual projects delivered within the last decade, leaving supply chains and workforces to atrophy (though deployment activity is ongoing elsewhere, most actively in China, which is set to outsize the U.S. nuclear fleet by 2030). Other clean firm options have achieved high technology readiness levels but have not yet been deployed consistently at commercial scale. Some clean firm options (e.g., fusion power) are more nascent and have not yet achieved technical viability.

Despite their promise to reduce overall system costs if deployed at scale, clean firm generation technologies across the board face high initial costs stemming from first-of-a-kind risk premiums, immature supply chains and underdeveloped workforces, and early project cost-overrun risks. Beyond these early-stage barriers, clean firm generation technologies also face a set of more general challenges, including technology-specific siting, permitting, and public acceptance challenges;60 a lack of long-term planning and/or procurement incentives for utilities; and a lack of mechanisms that enable customers to directly procure their own clean firm projects in many regions.

Some clean firm generation technologies are also reliant on, or benefit from, enabling infrastructure that does not currently exist at scale. Projects involving carbon capture and storage, for instance, are typically more cost-effective when they can connect to an established CO2 pipeline network or trunk line rather than building their own transportation and storage infrastructure.61 These technologies could benefit strongly from such network effects if deployed at scale.

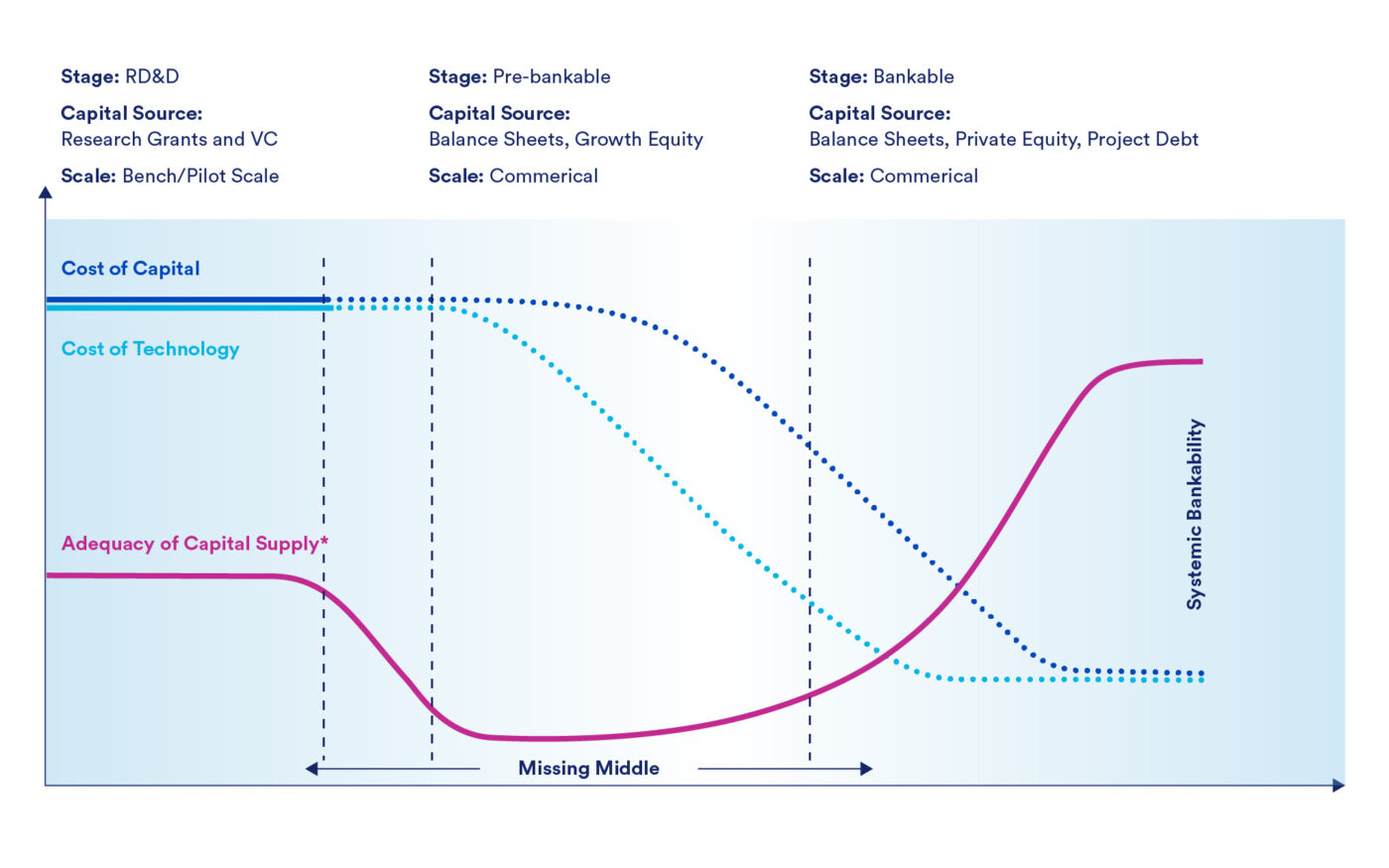

These challenges create a structural gap in development and financing for technologies that have progressed beyond basic R&D into commercial-scale development, but are not yet sufficiently derisked at that scale to achieve consistent bankability. Failure to unlock sufficient capital at this stage can cause progress to stagnate or fail altogether. This market gap is commonly referred to as the “missing middle,” or “valley of death,” and is a well-understood stage of the commercialization process for any capital-intensive technology:62,63

- Stage 1 (research, development, and demonstration): At the beginning of new technology development, government research funding and venture capital are available for high-risk bench- or lab-scale innovation, prototyping, testing, and piloting.

- Stage 2 (missing middle): Once the technology requires full demonstration in the field, however, there is a dearth of capital supply to build early-stage commercial-scale projects.

- Venture capital, where limited pools of equity capital make small investment bets with hopes for outsized returns, does not have the capacity to support the capital-intensive pilot and commercial-scale projects, and potential returns fall below their required levels.

- Such early-stage technologies are also considered too risky to access large, low-cost pools of institutional capital.

- Stage 3 (systemically bankable): Project bankability conditions (described below) allow for a technology to access a large scale of low-cost project debt from institutional investors.

Figure 10. Illustrative figure of cost of capital, cost of technology, and adequacy of capital from the early research, development and deployment (RD&D) stage to the pre-bankable and bankable stages.

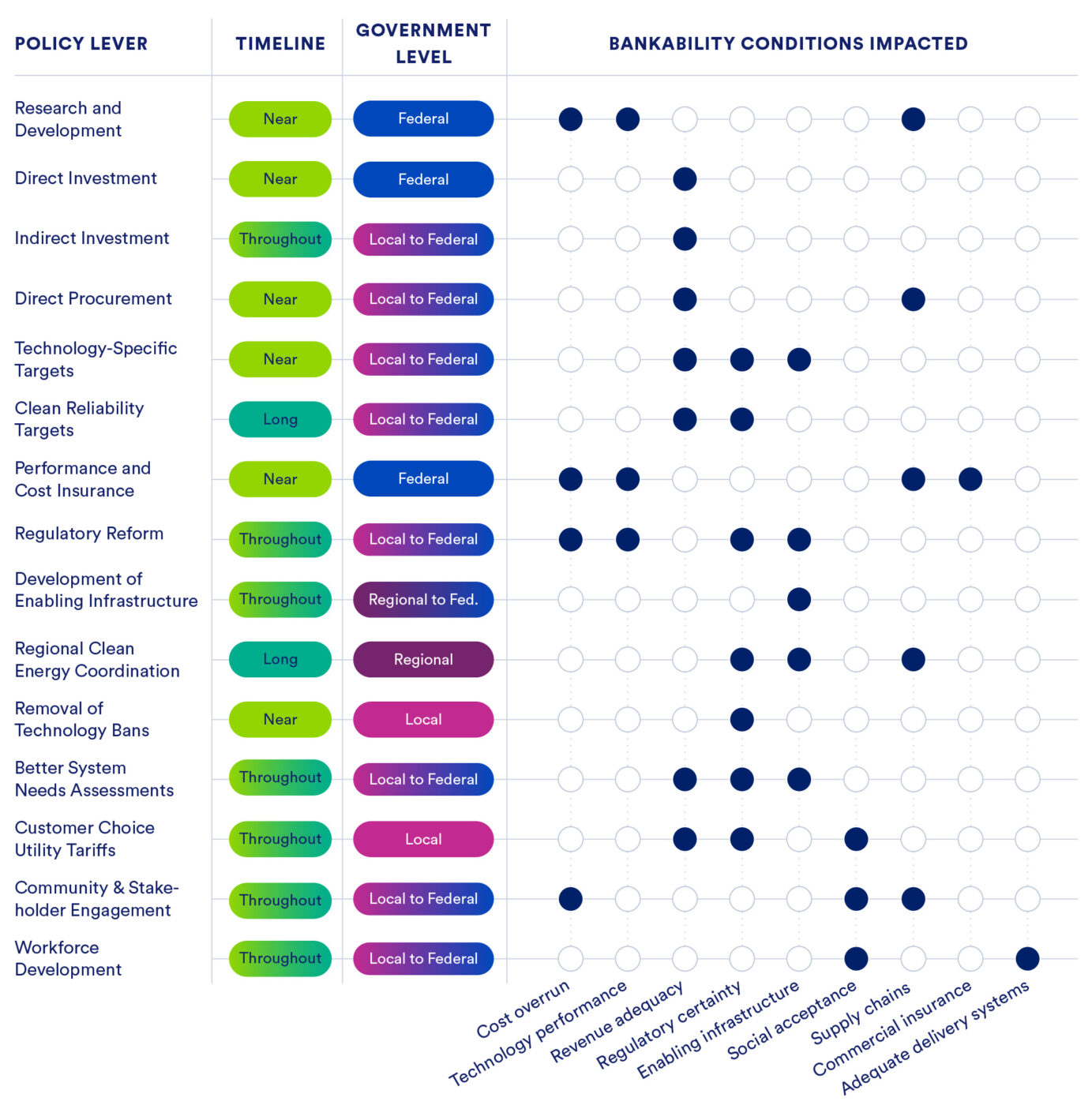

Most clean firm generation technologies are currently in the first or second stages of this process and lack one or more of the following project bankability conditions:64

- Negligible construction cost overrun risks

- Negligible technology performance risks

- Negligible revenue adequacy risks

- Regulatory certainty

- Access to enabling infrastructure networks (e.g., transmission)

- Durable and widespread social acceptance

- Robust supply chains

- Adequate delivery system (e.g., workforce capacity and engineering, procurement, and construction management (EPC) organizations).

Systemic bankability exists when the conditions for project bankability are pervasive and broadly met by many commercial projects for a specific technology or industry such that rapid, wide-scale deployment can occur.

Planning and Regulatory Gaps

In addition to bankability challenges, clean firm generation technologies face other structural barriers to adoption, including limited long-term planning and procurement incentives for utilities and a lack of customer procurement mechanisms in certain regions.

Clean firm generation technologies will be most valuable in future energy systems with ambitious climate policies where wind, solar, and storage resources require additional balancing that unabated fossil power can no longer provide. However, clean firm deployment must begin in earnest now if these technologies are to be able to contribute to these future systems at a sufficient scale. Even so, electricity system planning processes often focus almost exclusively on nearer term (5-10 years) electric system needs rather than longer term (10-30 years) needs that may require present-day investment for timely, efficient, and cost-effective execution.65 Without incentives for utilities in regulated markets or planning and procurement authorities in deregulated markets to look beyond 10 years, these entities will not adequately capture the long-run economic and risk mitigation benefits of clean firm generation technologies and may find themselves poorly positioned to address future system needs.

Inflexible utility procurement mechanisms for new generation can also stymie investment in clean firm generation technologies. Infrequent or prolonged procurement cycles can prevent timely responses to changing system or market conditions, or advances in technology readiness. A procurement process may also fail to realize the full benefits of competition by arbitrarily limiting candidate technologies or precluding third-party options in favor of utility self-builds. Additionally, regulations that require electricity customers to go through utilities rather than procuring their own resources directly can stymie clean firm uptake. Most announced offtake agreements for clean firm resources to date have been from large corporate electricity consumers that have greater willingness –to pay for these resources and their climate or reliability attributes than the general public. Unfortunately, such buyers are unable to act on this preference in vertically integrated markets where utilities do not offer supply choice.

Though some regulated utility markets have seen the development of “green” tariffs that enable customers to pay a premium for clean supply,66 many of these programs remain limited to or tailored for renewable energy resources rather than low- or zero-emitting resources more generally, including clean firm generation technologies.

The Role of Policy

Unlocking clean firm deployment will require coordinated action across national, regional, state, and industry actors. No single policy lever is sufficient. Creating and maintaining favorable conditions will almost certainly require a succession of commercial-scale, pre-bankable projects to be financed and built, showcase adequate operational and commercial performance, and achieve cost declines and price discovery. This requires government and/or customer investment at above-market prices to drive down costs.

To drive cost declines that unlock clean firm generation technologies as widely available options requires time. As such, early support of these technologies is necessary to ensure their progress and availability in the future. As an example of how early policy support can drive down the cost of generation technologies, the enormous reductions in the cost of wind and solar power over the last several decades were enabled by generous government support and deployment mandates that enabled deployment to bring down the initially high costs of these technologies. For example, early feed-in-tariffs for new utility-scale solar in Germany reached 500 EUR/MWh in the early2000s 67 and solar renewable energy credits in the U.S. for behind-the-meter solar were roughly $200-$600/MWh, depending on the state, in the early 2010s.68 Energy storage and offshore wind deployment were also mandated in several jurisdictions before 2020, with resulting contracts often coming in well above $100/MWh.69 These early efforts have materialized in significant cost declines where solar and wind are now cost competitive in most jurisdictions. This is all on top of decades of research and development that made solar and wind technologically ready as well as large investments by governments to realize manufacturing efficiencies that reduced costs. Today, the world reaps the benefits of decades of government support.

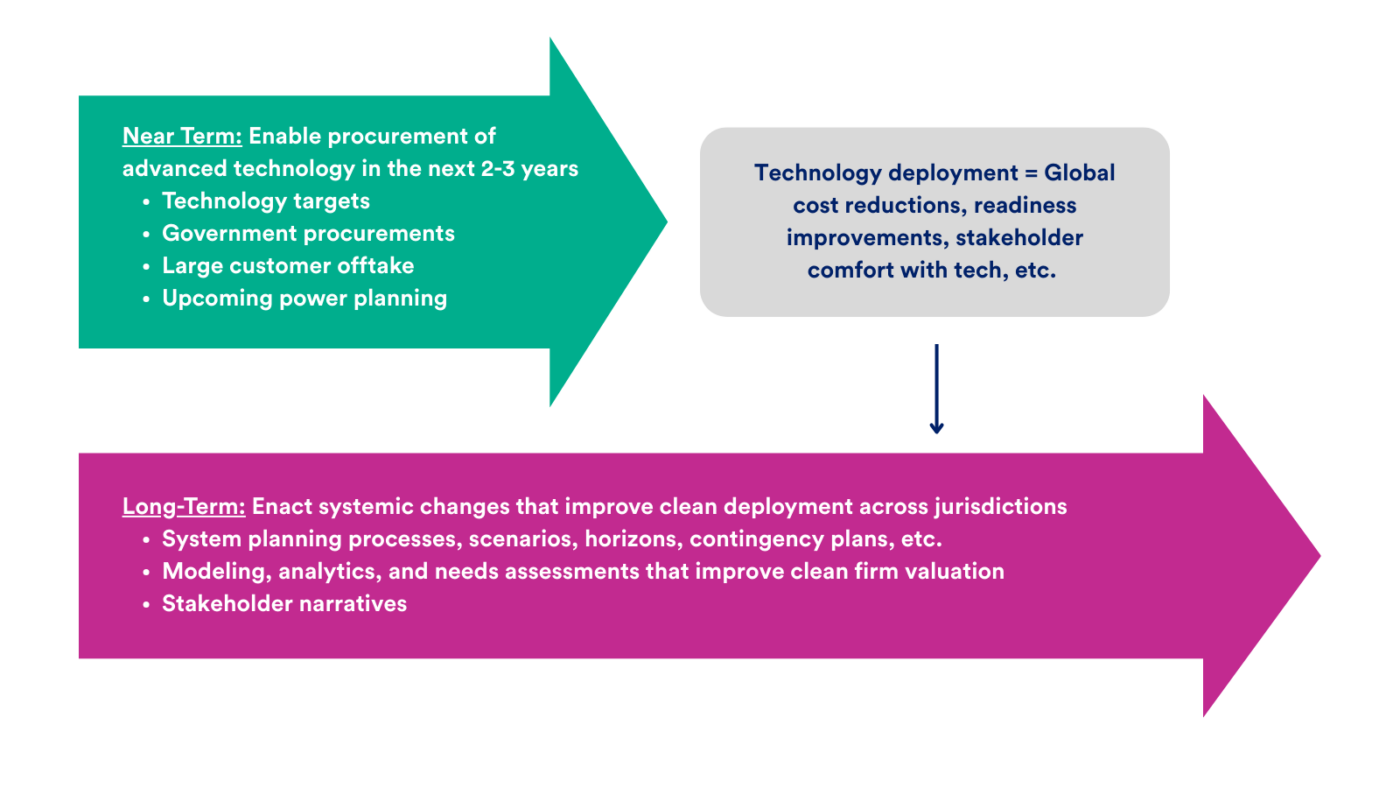

To unlock the enormous potential benefits of clean firm generation resources—and avoid the downsides of a failure to commercialize these technologies—a similarly robust, multi-layered, and forward-looking set of policy interventions are needed. Clean firm generation technologies will require targeted near-term support to ensure their successful initial deployment at what are likely to be above-market costs. Over the longer term, a supportive policy environment can help ensure that commercial bankability conditions are consistently met and establish price signals that support continued scaling of clean firm generation technologies, thereby driving experience-based reductions in cost.70 Coordinated policy strategies that address both these near- and long-term needs will be most effective at ensuring successful commercialization (Figure 11).

Figure 11. Near- and long-term strategies to advance clean firm generation technologies.

Clean Firm Policy Levers

There are many potential policy levers that can be used to address discrete challenges faced by clean firm generation technologies on the road to commercialization. The following is a non-exhaustive list of policy levers available to policymakers at various levels of government. Figure 12 shows how these interventions address key bankability challenges at different stages of the commercialization process.

- Research, Development, and Demonstration (RD&D): Support for pre-commercial RD&D to improve technology performance and/or reduce costs (e.g., funding for deep well drilling in superhot conditions or fundamental fusion research)

- Direct Investment: Targeted grants and loans to pre-bankable commercial scale pilot and demonstration facilities to overcome financing challenges for early-stage technologies (e.g., the European Commission’s Innovation Fund)71

- Indirect Investment: Production and investment incentives or emissions penalties to help clean technologies overcome cost premiums (e.g., investment or production tax credits, carbon pricing).

- Direct Procurement: Direct government procurement of power or products to overcome investment challenges and/or coordinate procurement efforts (e.g., government procurement to support supply chain investment for a clean firm technology).

- Public Ownership: Development of clean firm assets by government-owned utilities to ensure that deployment goals are met and financial risks are mitigated (e.g., French government ownership of Electricité de France during the utility’s large-scale nuclear fleet buildout72).

- Technology-Neutral Clean Energy Targets: Clean energy procurement mandates that allow all low-carbon electricity resources to qualify, rather than only renewables, to level the playing field for non-renewable clean firm technologies (e.g., Clean Energy Standards in several U.S. states73).

- Clean Reliability Targets: Adoption of reliability-focused clean procurement targets in addition to existing energy-focused targets to incentivize earlier procurement of clean firm generation technologies and recognition of their reliability benefits (e.g., clean capacity standards or hourly clean energy standards).

- Technology-Specific Targets: Technology-specific carveouts or procurement targets to support early-stage development of emerging technologies and enable long-term commercial availability (e.g., geothermal targets in California,74 CO2 injection targets in the EU75).

- Performance and Cost Protections: Government-provided backstops to mitigate customer and ratepayer cost risks, enabling regulatory approval (e.g., cost overrun protection for nuclear projects).

- Improving Project Development Processes: Reform or forward-looking development of regulations for advanced technologies to streamline development and provide regulatory certainty (e.g., streamlined permitting, such as EU’s Net-Zero Industry Act, for geothermal projects).

- Development of Enabling Infrastructure: Regional-level planning for enabling infrastructure to support technology deployment and/or reduce unit costs (e.g., regional planning for electricity transmission or CO2 transport and storage expansion).

- Coordination across jurisdictions or levels of government: Multi-jurisdiction coordination of climate policy or clean energy integration efforts to improve impact and avoid policy leakage (e.g. efforts to link carbon cap-and-trade programs across California, Oregon, Washington, and British Columbia76 or efforts develop cross-border clean energy infrastructure77).

- Removal of Technology Bans: Elimination of moratoriums that ban technologies to enable the full suite of clean firm options (e.g., the lifting of Illinois’ partial moratorium on new nuclear development in 202578 or Germany’s recent legislation that removed certain limits on CCS use79).

- Better System Needs Assessments: Improved system needs assessment analyses with longer time horizons, more technology options, and greater risk awareness to help decision makers more fully capture the value of clean firm power (e.g., the SB100 needs assessment in California,80 or CATF’s recommendations for the upcoming EU Grids Package81)

- Customer Choice Utility Tariffs: Utility tariffs that allow customers to procure specific desired clean firm generation technologies in vertically integrated regions, enabling initial above-market deployment (e.g., Nevada’s Clean Transition Tariff82)

- Community and Stakeholder Engagement: Proactive developer engagement with communities to provide education on the local value of clean firm and answer questions about new technologies (e.g., successful efforts to build community support for the Utah FORGE next-generation geothermal demonstration project83 or EU’s energy communities effort84)

- Workforce Development: Programs that train or retrain workforces for emerging clean industries to enable rapid scale-up and ensure that local communities benefit from high-road, well-paying employment opportunities (e.g., the EU’s Net-zero Industry Academies85).

Figure 12: Illustrative table showcasing policy actions that can support the commercialization of clean firm generation technologies, including the timelines and levels of government at which they can be applied and the commercial bankability conditions they address.

Strategies for Near- and Long-Term Impact

These levers are best applied in a multi-layered approach to support clean firm generation technologies at each stage of their journey toward full commercialization and economically competitive mass deployment. While the optimal policy mix will necessarily be context-dependent, the following narrative example illustrates how a mix of local, regional (either cross-country, multi-state, or other regional arrangements), and national actions could work together to bring clean firm power to commercial maturity:

Supporting Initial Deployment:

- Early-stage government RD&D programs that advance technology readiness and support successful demonstration of the technical viability of one or more clean firm generation technologies.

- A multinational, national, or subnational government or planning authority assesses the long-term need for clean firm generation technologies to ensure reliability and affordability while achieving decarbonization goals. The assessment could include assessing clean firm generation technologies’ local potentials, modeling systems to assess optimal portfolios, scenario-based and longer-horizon planning, community/stakeholder engagement, and other similar activities.

- Based on the long-term needs identified in the assessment, the government creates a technology development roadmap for local clean firm power. It identifies and addresses barriers to clean firm deployment, including siting, resource characterization, enabling infrastructure availability, and permitting processes.

- Government establishes a targeted clean firm procurement mandates or directs the relevant entity (e.g., a utility) to procure initial clean firm generation projects, setting up a competitive solicitation for clean firm resources or requiring local utilities to include qualifying resources in their integrated resource planning, and taking care to implement cost containment mechanisms for ratepayers. Private offtakers with above-market willingness-to-pay for clean firm power are also permitted to participate in solicitations, and government subsidies for clean firm resources reduce the anticipated cost for all potential offtakers. The procurement process identifies one or more technology providers and results in signed offtake agreements.

- In coordination with this procurement process, the government provides low-interest capital and cost overrun insurance to the selected projects, ensuring bankability and reducing both financing costs and ratepayer risks.

- The selected projects progress through construction to commercial operation, building local workforces and supply chains while reducing the projected cost of future builds.

Establishing Long-Term Bankability:

- Incentives are kept in place to support the first large tranche of clean firm generation projects following initial deployment. Subsidies can be adjusted over time as costs evolve, and may decline over time, have sunset rates, etc.

- Multinational, national, or subnational governments put in place more ambitious, technology-neutral policies to maintain long-run market signals for clean firm power. These could include hourly clean energy standards or clean capacity standards, tax credits, or mandates to retire unabated fossil infrastructure.

- Government works with interested planning authorities to establish an ‘order book’ beyond initial clean firm project development for a select set of clean firm generation technologies and designs, possibly coordinating procurement through a single federal process. This coordination helps unlock economies of scale and derisk investment in clean firm supply chains, reducing costs for all participants.

- National and subnational authorities ensure regulations enable interested corporate buyers to procure clean firm power directly (e.g., requiring utilities to offer ‘clean transition tariff’ procurement options or encouraging public-private partnership in order books), leveraging these customers’ greater buying power and willingness-to-pay.

- Regional planning authorities coordinate and make necessary interventions to ensure timely buildout of key enabling infrastructure for clean firm resources, including electricity transmission and CO2 pipelines.

- National and subnational support supply chain and workforce development programs to ensure the system has adequate delivery capacity to build projects.

- Project economic performance (including local economic benefits for communities) are documented and shared amongst all relevant stakeholders to ensure that technologies and their potential development tradeoffs are accurately understood.

The Role of the Private Sector

While government action is essential to the successful commercialization and deployment of clean firm generation technologies, there is also a significant potential role for the private sector as an accelerating force. Historically, voluntary private sector clean energy buyers have been a significant source of early demand for emerging clean electricity technologies, including wind and solar power.86 By paying a premium for these technologies above the initial market value of their power, corporate clean energy buyers have helped them reach the scale necessary to achieve market-competitive costs. Now, private-sector actors have the opportunity to do the same for the next generation of clean technologies.

Corporate buyers have already signed multiple key offtake deals for clean firm electricity projects, including next-generation geothermal,87 nuclear,88 and large-scale gas with CCS,89 among others. By building on this leadership, voluntary corporate actors can help ensure that these technologies continue to see strong demand as they grow, while in turn benefitting from increasing availability of reliable clean power to support the rise in electricity demand that many companies are experiencing. Movement toward more time- and location-granular accounting for corporate greenhouse gas emissions90 and membership in voluntary campaigns to achieve round-the-clock clean electricity supply91 can help further incentivize corporate procurement of clean firm generation technologies by placing greater value on their reliability attributes.

There are mechanisms available in both deregulated and regulated markets for governments to better facilitate voluntary procurement of clean firm power (alongside other clean energy sources). For example, to address accelerating electricity demand growth, deregulated regions could incentivize direct procurement of clean electricity through “bring your own clean energy” interconnection approaches pairing new large loads and clean energy generators, so long as the new load does not unfairly shift costs onto unrelated customers. Regulated regions could establish tariffs that enable large customers to procure clean firm power from the utility or “clean transition tariff” programs that allow large customers to directly work with third-party project developers to bring clean firm generation technologies to a utility’s system. These programs should be designed to preclude cost-shifting to other ratepayers while facilitating large customer “self-supply.” Under either scenario (deregulated and regulated markets), planners and utilities should account for the self-supplied generation in their planning assessments to ensure reliability and incentivize timely deployment of clean firm generation technologies.

Looking Forward

A robust decarbonization strategy requires a risk-insulated portfolio of diverse technologies, including those that can ensure reliable and cost-effective service even in the most unfavorable of weather conditions. Clean firm resources should be deployed alongside renewables, transmission, long-duration storage, and demand-side solutions, and they are undoubtedly an essential part of the electricity decarbonization toolbox. The societal investment case for clean firm power—significant reductions in the cost of decarbonized and improved decarbonization resilience—is clear. Yet some clean firm generation technologies are nascent and may face significant barriers to large-scale commercialization. As with wind, solar, and lithium-ion batteries before them, clean firm generation technologies will require multi-layered policy support from all levels of government to realize their full potential. With targeted and coordinated policy interventions and voluntary action, clean firm electricity can do its part to deliver a reliable, affordable, and sustainable energy future.

Footnotes

This report focuses on clean firm generation technologies that are dispatchable for an effectively indefinite amount of time at an individual asset level, and as a result does not include portfolios of generation, storage, and demand-response technologies. Portfolios with sufficiently large capacities of non-firm generation and storage can approximate some of the capabilities of firm resources but, as we will discuss, the capacities required would be exceedingly large and are generally most costly on their own.

See the “Why” section below for a summary of relevant literature.

Lutz, M. (2025). Residential electricity prices up more than 6% in August: EIA. Utility Dive. https://www.utilitydive.com/news/residential-electricity-prices-up-more-than-6-in-august-eia/803849/

Howland, E. (2025). NERC president warns of ‘five-alarm fire’ for grid reliability. Utility Dive. https://www.utilitydive.com/news/data-center-grid-reliability-ferc-nerc/803467/

Martucci, B. (2025). U.S. data center power demand could reach 106 GW by 2035: BloombergNEF. Utility Dive. https://www.utilitydive.com/news/us-data-center-power-demand-could-reach-106-gw-by-2035-bloombergnef/806972/

The City. (2025). New York State Energy Plan: peaker climate. The City. https://www.thecity.nyc/2025/12/16/new-york-state-energy-plan-peaker-climate/

See map of Renewable Portfolio Standards (which often exclude one or more clean firm generation technology) and Clean Energy Standards (which often include clean firm generation technologies): https://www.catf.us/clean-electricity-standards-map/

U.S. Department of Energy, Office of Nuclear Energy. (2024). What Is a Nuclear Moratorium? U.S. Department of Energy. https://www.energy.gov/ne/articles/what-nuclear-moratorium

- Some examples include New York State and Poland.

U.S. Energy Information Administration. (2025). Electricity Monthly. U.S. Energy Information Administration. https://www.eia.gov/electricity/monthly/

Gospodarczyk, M. M. (2024). IAEA releases nuclear power data and operating experience for 2023. International Atomic Energy Agency. https://www.iaea.org/newscenter/news/iaea-releases-nuclear-power-data-and-operating-experience-for-2023

U.S. Energy Information Administration. (2024). What is U.S. electricity generation by energy source? U.S. Energy Information Administration. https://www.eia.gov/tools/faqs/faq.php?id=427&t=3

World Nuclear Association. (2025). Nuclear Power in the European Union. World Nuclear Association. https://world-nuclear.org/information-library/country-profiles/others/european-union

Including high costs, construction risks, political risks, etc.

Simon, A. J., Smith, P., & Friedmann, J. (2025). Capture committed: Google and Broadwing sign carbon capture power deal. Carbon Direct. https://www.carbon-direct.com/insights/capture-committed-google-and-broadwing-sign-carbon-capture-power-deal

Sanchez et al. (2025). Electrocatalysis for CO₂ Conversion to Fuels and Chemicals. Sustainable Energy & Fuels. Royal Society of Chemistry. https://pubs.rsc.org/en/content/articlehtml/2025/su/d4su00552j;

Dees et al. (2023). Catalyst design and mechanisms for CO₂ reduction. Green Chemistry. Royal Society of Chemistry. https://pubs.rsc.org/en/content/articlehtml/2023/gc/d2gc02483gIEA Bioenergy. (2024). The role of bioenergy in decarbonising energy systems: Commentary. https://www.ieabioenergy.com/wp-content/uploads/2025/01/Commentary_RoleBioenergy_Dec2024l.pdf

Roads to Removal: Options for Carbon Dioxide Removal in the United States, December 2023, Lawrence Livermore National Laboratory, LLNL-TR-852901;

Dees et al. (2023). Green Chemistry. https://pubs.rsc.org/en/content/articlehtml/2023/gc/d2gc02483g;

Langholtz et al. (2020). Land. https://www.mdpi.com/2073-445X/9/9/299;

Sanchez et al. (2015). Nature Climate Change. https://www.nature.com/articles/nclimate2488Given the extremely long durations over which hydrogen can be economically stored and the distances over which it can be transported, this option blurs the line between clean firm generation and long-duration energy storage technology categories.

International Energy Agency. (2025). World Energy Outlook 2025. https://www.iea.org/reports/world-energy-outlook-2025

Schülde, M., Veillard, X., & Weiss, A. (2023). Four themes shaping the future of the stormy European power market. McKinsey & Company. https://www.mckinsey.com/industries/electric-power-and-natural-gas/our-insights/four-themes-shaping-the-future-of-the-stormy-european-power-market

Net-Zero America Project. (2021). The report. Princeton University. https://netzeroamerica.princeton.edu/the-report

Nøland et al. (2022). Scientific Reports. https://pubmed.ncbi.nlm.nih.gov/36481808/;

Lovering et al. (2022). PLOS ONE. https://journals.plos.org/plosone/article?id=10.1371/journal.pone.0270155;

van de Ven et al. (2021). Scientific Reports. https://doi.org/10.1038/s41598-021-82042-5;

International Energy Agency. (2021). Mineral requirements for clean energy transitions. https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions/mineral-requirements-for-clean-energy-transitionsThis statistic is derived from comparing the “E+” and “E+RE-” scenarios in the Net-Zero America study for years 2035–2050.

Long et al. (2021). Clean firm power is the key to California’s carbon-free energy future. Issues in Science and Technology. https://issues.org/california-decarbonizing-power-wind-solar-nuclear-gas/

New York State Energy Planning Board. (2025). Draft 2025 Energy Plan. https://energyplan.ny.gov/Plans/Draft-2025-Energy-Plan

Quantified Carbon. (2025). Clean Firm Power in Europe’s Energy Transition. https://cdn.prod.website-files.com/650ac0ab00dff792a8cebc3c/6978eef2e54578d3f5da976f_CATF_4%20Report.pdf

Long et al. (2021). Clean firm power is the key to California’s carbon-free energy future. Issues in Science and Technology. https://issues.org/california-decarbonizing-power-wind-solar-nuclear-gas/

The NorthBridge Group. (2021). Review and assessment of literature on deep decarbonization in the United States. https://cdn.catf.us/wp-content/uploads/2021/06/21092235/NorthBridge_Deep_Decarbonization_Literature_Review.pdf

Sepulveda et al. (2021). The design space for long-duration energy storage in decarbonized power systems. Nature Energy. https://www.nature.com/articles/s41560-021-00796-8

Clean Air Task Force. (2025). Beyond LCOE. https://www.catf.us/resource/beyond-lcoe/

The NorthBridge Group. (2021). Review and assessment of literature on deep decarbonization in the United States. https://cdn.catf.us/wp-content/uploads/2021/06/21092235/NorthBridge_Deep_Decarbonization_Literature_Review.pdf

- ISO New England. (2024). Economic Planning for the Clean Energy Transition. ISO New England.

https://www.iso-ne.com/static-assets/documents/100014/epcet_policy_final_results.pdf - Spokas, K., & Carlson, J. (2025). New role for nuclear power emerges in New York energy plan. Utility Dive. https://www.utilitydive.com/news/new-york-energy-plan-nuclear-catf/808048/

Quantified Carbon. (2025). Clean Firm Power in Europe’s Energy Transition. https://cdn.prod.website-files.com/650ac0ab00dff792a8cebc3c/6978eef2e54578d3f5da976f_CATF_4%20Report.pdf

Ember. (2024). ASEAN’s clean power pathways: 2024 insights. https://ember-energy.org/app/uploads/2024/10/Report-ASEANs-clean-power-pathways-2024.pdf

International Energy Agency. (2024). Southeast Asia Energy Outlook 2024. https://iea.blob.core.windows.net/assets/ac357b64-0020-421c-98d7-f5c468dadb0f/SoutheastAsiaEnergyOutlook2024.pdf

- https://iopscience.iop.org/article/10.1088/2516-1083/ae2bd7

Euronews. (2025). France and Switzerland shut down nuclear power plants amid scorching heatwave. https://www.euronews.com/2025/07/02/france-and-switzerland-shut-down-nuclear-power-plants-amid-scorching-heatwave

BloombergNEF. (2023). A power grid long enough to reach the Sun is key to the climate fight. https://about.bnef.com/insights/clean-energy/a-power-grid-long-enough-to-reach-the-sun-is-key-to-the-climate-fight/

U.S. Energy Information Administration. (2025). Rising electricity generation and evolving grid dynamics. https://www.eia.gov/todayinenergy/detail.php?id=64586;

Net-Zero America Project. (2021). The report. https://netzeroamerica.princeton.edu/the-reportPavia, N. (2024). Future-fitting the grid. https://www.catf.us/2024/07/future-fitting-grid-how-accelerate-federal-transmission-permitting/;

Hack, J. (2025). World Resources Institute. https://www.wri.org/insights/advanced-transmission-technologies-us-power-gridDunne, C. D. (2025). Interconnection reforms and processes across the Atlantic. https://www.catf.us/2025/10/interconnection-reforms-and-processes-across-the-atlantic-a-primer/

ClearPath. (2022). Hawkeye State Headwinds. https://clearpath.org/reports-and-more/hawkeye-state-headwinds/;

Clean Air Task Force. (2025). How to build transmission with communities, not around them. https://www.catf.us/2025/11/how-to-build-transmission-with-communities-not-around-them/Energy Systems Integration Group & NREL. (2025). ESIG demand response & wholesale markets report 2025. https://www.esig.energy/wp-content/uploads/2025/02/ESIG-Demand-Response-Wholesale-Markets-report-2025.pdf

- Joskow, P.L. Challenges for wholesale electricity markets with intermittent renewable generation at scale: the US experience. (2019). Oxford Review of Economic Policy, Vol 35, Num 2.

Craig et al. (2018). Renewable and Sustainable Energy Reviews. https://www.sciencedirect.com/science/article/abs/pii/S1364032118306701;

National Renewable Energy Laboratory. (2022). https://www.nrel.gov/docs/fy22osti/78394.pdfClean Air Task Force. (2025). Europe’s grids package marks positive shift. https://www.catf.us/2025/12/europes-grids-package-marks-positive-shift-coordinated-eu-wide-infrastructure-planning-permitting/

Rocky Mountain Institute. (2024). https://rmi.org/for-ratepayers-to-realize-savings-from-clean-energy-utility-business-models-need-an-update/