Europe’s Clean Industrial Deal

Recommendations for an efficient transition towards a sustainable and competitive European industry

Overview

Faced with acute challenges of high energy prices and cost of living, fragile energy security, and growing international competition, as well as just transition concerns, the EU needs a robust strategy. This strategy must ensure that the bloc meets its decarbonisation goals, remains a global leader in sustainable industries, and safeguards economic competitiveness and job creation. The Draghi report laid out a dire situation of the EU industry and stressed the need for urgent and bold action. The Clean Industrial Deal will be crucial for the EU to strengthen its industries and support their timely transition to climate neutrality. It will have to provide a detailed plan and the enabling conditions for industries to decarbonise, build their business case, unlock investment and strengthen their competitiveness globally. Building on the European Green Deal and the insights from the Letta and Draghi reports, the EU is well-positioned to pursue this endeavour, shaping its unique model of competitiveness, industrialisation, and innovation.

Clean Air Task Force (CATF) has developed the following recommendations on the principles, scope, and measures of the Clean Industrial Deal.

1. Transversal principles: Sustainability, cohesion, and just transition

In addition to fostering competitiveness by positioning EU industries at the forefront of the clean energy revolution, the Clean Industrial Deal must fully integrate other key objectives: sustainability, cohesion, and just transition.

First, the EU needs to continue prioritising climate action by reducing greenhouse gas emissions, deploying clean technologies, and encouraging innovation in technologies to drive the global transition to a low-carbon economy. The goal of achieving climate neutrality by 2050 must remain front-and-centre and be strengthened by integrating the recommended 90% net emissions reduction target for 2040 into EU law as soon as possible. Backtracking is not an option; it would expose the EU to further climate shocks and damage its competitiveness.

Second, the Clean Industrial Deal should have a strong focus on EU cohesion. All EU regions should be able to decarbonise at an affordable cost, and all Member States should benefit from and contribute to the clean transition. While a revision of state aid and competition law can help support key industries, this needs to be balanced with a strategy that addresses disparities in industrial and financial capacity among Member States, to prevent widening the economic and social fragmentation.

Third, the concept of a just transition should be at the core of the Clean Industrial Deal. The clean transition must be inclusive, ensuring that workers from traditional industries are not left behind and that high-quality jobs are created across the EU thanks to this transition. Only a Clean Industrial Deal with a strong social component can ensure durable support from EU citizens for the transition.

Lastly, the Clean Industrial Strategy should also provide ample opportunities for a varied group of stakeholders to contribute meaningfully. The development of comprehensive and bespoke sectoral and technology roadmaps within the Deal must be informed by industry needs and align with on-the-ground realities, particularly for energy-intensive industries and hard-to-abate sectors. Additionally, it should actively engage different actors, including civil society and local authorities.

2. Technology neutrality: Diversifying options

The European industry is confronting a serious threat to its competitiveness, driven by intensifying competition from China, substantial energy price disparities compared to other major industrial players like the U.S., and growing concerns over strategic dependencies on clean energy technologies. Varying rates of renewable deployment among Member States, differences in legacy energy systems among countries, and the unique social, economic, and resource circumstances of each Member State imply that a one-size-fits-all approach will not suffice. A broader, customised portfolio of climate solutions and technology options can and should be deployed to deliver on climate neutrality and energy security while improving resilience to unexpected developments and events, security of supply, reliability, and affordability.

Achieving climate neutrality by 2050 and ensuring energy security across Europe will require the deployment of a diverse range of low-carbon technologies. Renewable energy generation and improved energy efficiency will contribute to significantly reducing emissions but must be complemented by other strategies. The EU needs to develop and implement an approach based on flexibility and optionality, recognising that different regions and sectors may require tailored solutions and acknowledging the inherent risks of decarbonisation pathways relying on a narrow set of solutions. Technologies should be evaluated based on their potential for emissions reduction, scalability, and affordability.

Ensuring a consistent and adequate supply of clean electricity over the coming decades will require a portfolio of solutions. The EU should therefore adopt and support a diverse set of clean firm energy generation pathways alongside other climate-protecting technologies. Examples include clean hydrogen and ammonia, carbon capture, removal, and storage, small modular reactors (SMRs), and innovations such as superhot rock geothermal energy and fusion energy.

3. A portfolio of sector-specific strategies for heavy industry

The strengthened Emissions Trading System (ETS) ambition and the gradual phase-out of free allowances will confront hard-to-abate industries with an increasing carbon price. This will likely lead industries to either transition to cleaner technologies, bear escalating costs for their emissions, or relocate their activities outside the EU. It is therefore crucial to ensure that the industries have the tools to decarbonise and preserve their competitiveness. They will need a mix of multiple technologies, with different timelines and a broad scope of supportive policies.

The Clean Industrial Deal should include dedicated plans for hard-to-abate sectors to establish practical and scalable pathways to decarbonisation. Industries such as steel, cement, chemicals, and shipping are vital to the EU’s economy but are also among the largest emitters, with deeply embedded carbon footprints that require targeted solutions. Sector-specific approaches allow for the deployment of the most effective technologies, recognising that these industries face unique challenges and timelines that a single strategy cannot adequately address.

For instance, steel production could benefit significantly from accelerated adoption of hydrogen-based reduction technologies and carbon capture and storage (CCS). Meanwhile, the cement industry must address emissions from both energy use and chemical processes. Shipping and aviation also present additional complexities as global sectors, necessitating strong measures to scale sustainable fuels. The chemicals industry, given its diverse range of products and processes, also needs targeted efforts to enable the use of low-emission feedstocks and advanced recycling methods.

By adopting tailored roadmaps, the EU can maximise the impact of its investments, prioritise effective and adaptive solutions, coordinate complex deployment timelines, and incentivise innovation to address remaining gaps. A tailored approach not only accelerates decarbonisation but also helps safeguard industrial competitiveness and energy security are maintained.

Figure 1: Table of potential technologies needed to decarbonise hard to abate sectors

| Sector | Circular economy | Electrification | CCUS | Hydrogen | Biomass | Other process innovation |

|---|---|---|---|---|---|---|

| Iron and steel | More scrap recycling, replace by wood in construction | Electric arc furnace, electrolysis of iron ore | Capture ready: ULCOS, Hlsarna; Steel2-chemicals, Steelanol | H2-direct reduced iron: HYBRIT, SALCOS, H2Future, etc. | Blast furnace on bio-cokes | Hlsarna |

| Cement and lime | Concrete recycling | CCUS on clinker oven, LEILAC, mineral-isation | HT heat | Bio-fillers, biogas fired kiln | Low-carbon cemenr, CO2 curing | |

| Chemicals, polymers, and fertilizers | Higher quality plastics recycling, naphtha from waste plastic, reduce fertilizer use | Cracker of the future, electric boiler | CCUS on SMR, Oxy-fuel + CCUS | H2 from elect-rolyser, HT heat | Bio-based feed: MeOH, EtOH, bioBTX, H2 from biogas | Catalytic ethylene cracker, novel separation tech-nologies |

| Refineries | Recycled carbon fuels, reduction of demand by electric vehicles | Heat pumps, electric boiler | Synfuels, capture/ CCUS on SMR | HT heat | Biofuels, bio-crude as input | Novel separation tech-nologies |

4. Infrastructure build-out and planning

The transition will require significant infrastructure development and coordination, including across borders. The planning, retrofitting, and operation of Europe’s electricity transmission and distribution networks must align with the planning and operation of the new CO2 and hydrogen infrastructure, energy storage, and charging infrastructure for electromobility.

Affordable electricity prices and access to reliable base load energy are crucial for industries to remain competitive. Strengthening the backbone of the energy system – the power grid –forms a central part of this effort, alongside further implementing and refinement of the Electricity Market Design (EMD). Achieving these goals requires substantial and coordinated infrastructure investment to support a European electricity grid projected to grow three to four times its current size by 2050.1 This underscores the critical importance of comprehensive grid infrastructure planning and access to affordable 24/7 carbon-free electricity (CFE) as essential components of the Clean Industrial Deal. These elements are key to maintaining industrial competitiveness and energy security.

Regarding CCS, an indispensable climate-protecting technology, the EU needs to support the development of a comprehensive cross-border CO2 transport and storage network. This includes ensuring an effective implementation of the Net Zero Industry Act (NZIA) target of 50 million tonnes of operational storage capacity in the EU by 2030. While proposed CO2 capture projects in the EU exceed 50 million tonnes by 2030, only around 35 million tonnes of storage capacity is currently scheduled to come online by that date. Moreover, the Industrial Carbon Management Strategy (ICMS) outlines an objective of 250 million tonnes of storage capacity in the European Economic Area (EEA) by 2040. Achieving this would represent a massive CO2 infrastructure effort, requiring coordinated action to ensure its deployment.

Figure 2: Growth in CO2 storage capacity over time based on current announcements

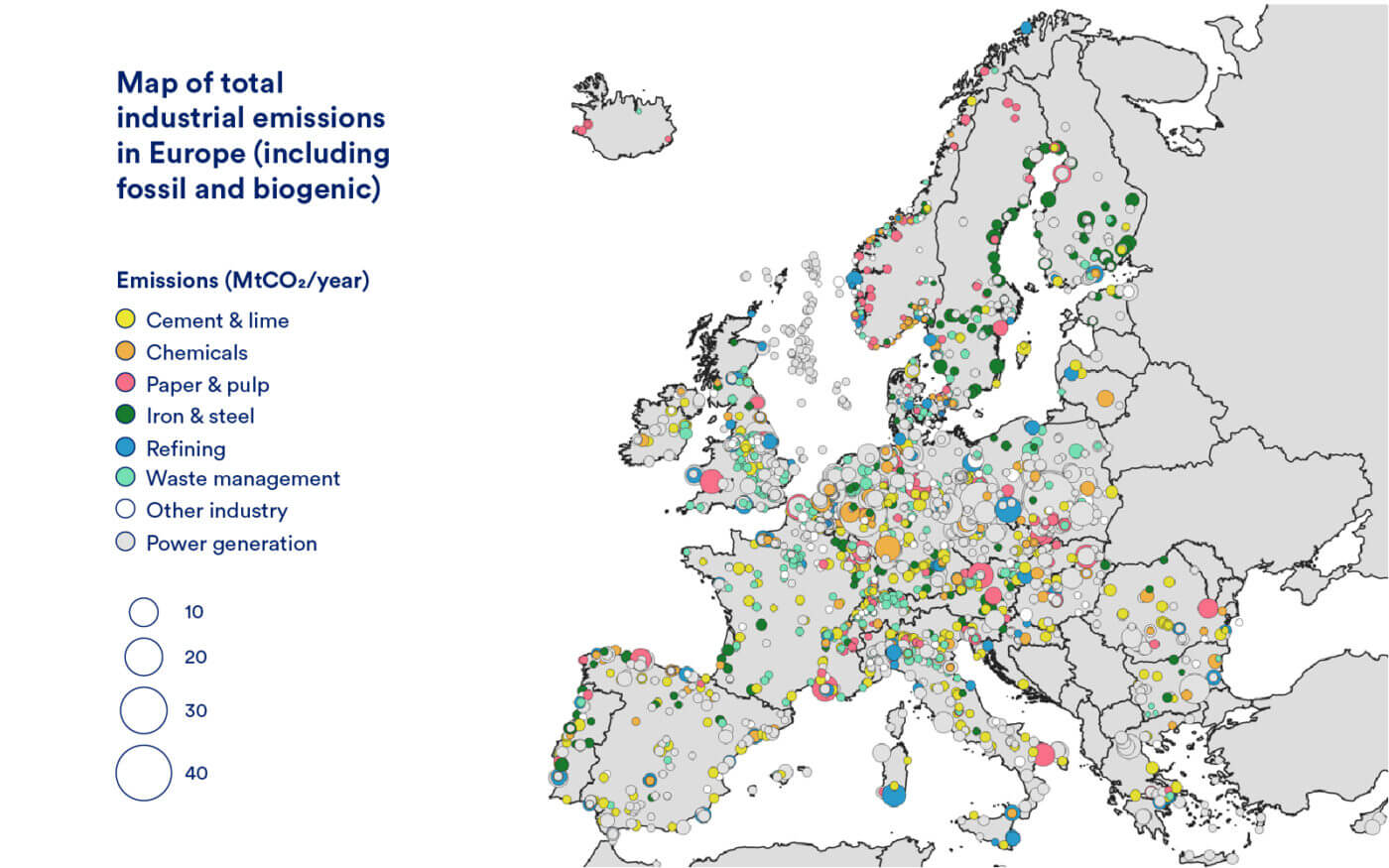

The EU will also need to ensure that all EU regions have access to this much-needed technology at an affordable cost. Currently, most of the storage capacity being developed in Europe is offshore in the UK and Norway, and within the EU primarily in Denmark and the Netherlands. However, industrial emissions that need to be abated occur across Europe.

Figure 3: Map of total industrial emissions in Europe

This regional disparity poses challenges for industrial facilities in other regions, requiring long-distance, multimodal CO₂ transport which could cost over €100/t.2 Analysis of CO2 infrastructure deployment scenarios indicates that industries in Eastern and Southern Europe could face up to five times higher costs than those in the North, unless storage is more broadly available across different regions. Shortening average transport distance will reduce CO2 transport costs.3

Figure 4: Different scenarios of CO2 storage scenarios in Europe (CATF 2023)

Deploying clean hydrogen, another key decarbonisation tool, will also require enabling an interconnected network of production, transport, distribution, and storage infrastructure. However, it is important to note that hydrogen molecules cannot be easily, nor cheaply, moved from production to end-use locations. Hydrogen has distinct physical properties that must be taken into account when planning its associated infrastructure. Being less dense and less stable than fossil gas, hydrogen must be compacted or converted to enable efficient and secure handling, which makes its transportation and storage more challenging. Therefore, hydrogen should ideally be produced as close as possible to where it is consumed. Hydrogen Valleys, which integrate hydrogen production, end-use, and connective infrastructure in close location, represent a valuable initiative in this regard. Where local production is not feasible, the EU needs to establish thorough and practical plans for transporting hydrogen, both across the bloc as well as from other nearby regions. Particular consideration should be given to the time required to invest in new and retrofitted transportation infrastructure, as existing infrastructure, such as pipelines, are unable to carry hydrogen in its pure form.4

Transporting hydrogen over long distances and across varied terrains increases costs and further reduces energy efficiency, potentially resulting in significant lifecycle emissions. Importing hydrogen from outside of the EU should therefore be limited to situations where domestic production falls short of meeting the EU’s anticipated demand. It is also important to consider how and where hydrogen would be imported into the bloc. CATF analysis found transporting hydrogen via short-distance pipeline is the most cost-effective and energy-efficient option. However, as mentioned, existing gas pipelines (and other infrastructure) would need to be retrofitted or replaced to be able to carry hydrogen.5 Another viable import pathway would involve transporting hydrogen by ship in the form of uncracked ammonia for direct application as a shipping fuel or in fertiliser production. However, cracking ammonia to release hydrogen is highly inefficient and costly, and therefore should not be incentivised or supported through public funding. Ultimately, the physical realities of hydrogen transportation must form the foundation of all decisions regarding import infrastructure.

5. Market measures

To support the scaling up of clean technologies in Europe, the EU needs to ensure the development of competitive and transparent markets and stimulate the demand for decarbonised products.

For instance, the risks of monopoly and oligopoly are emerging due to CO2 storage being developed by a limited number of entities, predominantly large oil and gas companies, in the North Sea area. A robust CO2 transport and markets regulation is therefore needed to ensure fair access to CO2 storage at reasonable tariffs. Stringent rules on open access to storage, and on fair and transparent pricing have to be put in place to ensure that that bargaining power is more evenly distributed between emitters (including SMEs) and transport and storage providers.

Currently, the market remains largely unregulated in most Member States, with prices decided by transport and storage providers on a customer-by-customer basis. A flexible regulatory framework for CO2 transport, particularly for onshore pipeline networks that are likely to function as natural monopolies, can help prevent excessive tariffs and other access barriers that could hinder the emerging market for CCS, thereby jeopardising the EU’s efforts to scale up this technology. Such a regulatory framework can also help encourage the development of infrastructure that is appropriately sized to meet future demand and leverage economies of scale, while ensuring that upfront investment costs and risks are distributed equitably across the future user base.

In addition, fostering greater demand for low-carbon materials, products, and technologies is essential. Public procurement, which accounts for approximately 14% of the EU’s annual GDP, could play a pivotal role in this effort. Currently, most procurement procedures prioritise the lowest price as the award criterion. Integrating sustainability, quality, and resilience as key considerations – potentially through the review of the Public Procurement Directive – could stimulate demand for decarbonised products and encourage industries to invest in innovation and scale production. This approach is also consistent with the recommendations of the Draghi report on the role of targeted market creation in advancing the EU’s competitiveness and climate goals.

Market intervention will also be needed for clean hydrogen, as it is unlikely to be available in sufficient amounts and at competitive prices to allow for scaling in the foreseeable future. Policymakers should therefore aim to direct the limited supply to sectors that need it most. The EU might need to reconsider its approach to building a clean hydrogen market: rather than leaving the allocation of produced hydrogen to market forces, robust demand estimates should be calculated for priority end-use sectors. This would support the setting of more realistic clean hydrogen targets and help identify priority off-takers for clean hydrogen producers to engage with. Additionally, steps should be taken to ensure market stability and improve its sustainability prospects once subsidised support is phased out.

As a matter of priority, existing unabated hydrogen generation in sectors like fertilisers and chemicals production should be replaced by clean hydrogen. Secondly, as hydrogen begins to be used in new applications, it should be directed towards those sectors where it can cut the most carbon emissions in a cost-effective manner, like steel manufacturing, shipping and aviation. Using hydrogen for residential heating and fuelling cars lacks reasonable justification, therefore it should be discouraged by policy in favour of other options for their decarbonisation.

Furthermore, it is critical that the EU ensures that any natural gas used to generate hydrogen – or other energy products – is accompanied by rigorous measures to reduce any associated methane emissions emitted by the production, transportation, or delivery of the natural gas. Methane is a greenhouse gas that traps 80 times more heat than CO2 over a 20 year timespan, causing rapid, short-term warming that could push us over irreversible climate tipping points. Consequently, if any natural gas consumption is foreseen in the energy mix for the EU’s industry, it will be impossible to move closer to its climate targets without rigorous methane mitigation efforts.

Due to methane’s near-term warming impacts, using blue hydrogen generated with unabated natural gas could result in a higher overall EU GHG emissions footprint, and slow down progress as opposed to accelerating it. To avoid this risk, the EU should build interlinkages between the Clean Industrial Deal and the performance standards in the EU’s Methane Regulation, as well as the Regulation’s obligations on imported fossil fuels. As these rules and thresholds still need to be finalised in the coming years, it will be important to ensure that they are fit for purpose for the sourcing of energy products like hydrogen.

Figure 5: CATF ranking of potential clean hydrogen end use sectors

6. Affordable and reliable clean energy access

The Clean Industrial Deal must secure a stable supply of clean and affordable energy, to support the transition of EU industries while maintaining competitiveness.

Europe faces a dual challenge: decarbonising its energy system while meeting rising electricity demand as much of its clean firm power capacity will age and require replacement by 2050.

Renewable energy sources, such as wind and solar, will be critical and the EU will need to deploy as much of these as possible. However, clean firm power – sources that can generate electricity on demand, regardless of weather or time of day, with minimal greenhouse gas emissions – provides important complementary benefits. Clean firm options can significantly enhance decarbonisation efforts in the EU.

Clean firm power reduces the need for fossil fuel back-up generation and for overbuilt capacity of wind and solar. A system dependent solely on wind and solar energy must account for seasonal variations that include many multi-day or even monthly periods of shortage. This challenge is exacerbated by the fact that fluctuations in wind and solar output are often correlated, increasing the risk of significant shortfalls. Currently, in times of shortage, unabated fossil energy is used. While overbuilding renewable capacity has been proposed to address some of these concerns, it would be very costly and face serious land-use limits in Europe.

Small Modular Reactors (SMRs) represent a potential technology to provide zero-emissions, safe, and dispatchable power amid intensified efforts to reduce carbon emissions and ensure energy security. With their small size (up to 300 MW per unit), simplified modular design, and the potential for factory production, SMRs are expected to serve new types of industrial electricity and heat consumers, such as steel mills, aluminium smelters, chemical plants, off-grid mining and refining facilities, electrolysers, and as replacement for retiring coal power plants. In addition to heat, SMRs are anticipated to deliver zero-emissions baseload power, and are also capable of adjusting their output to some extent, enabling it to support an energy system increasingly reliant on variable renewables. However, for SMRs to significantly bolster industrial competitiveness, a cohesive set of EU-led measures will be needed, beginning with the introduction of a comprehensive EU SMR Strategy.

7. Support for innovative technologies

According to the International Energy Agency,7 about 35% of the emissions reductions required to achieve net zero by 2050 will come from technologies that are not yet available on the market. Innovation must therefore be a cornerstone of the Clean Industrial Deal. Technologies like fusion and superhot rock geothermal energy have the potential to provide nearly limitless clean firm energy, but they require significant public support to reach commercial viability.

Superhot rock geothermal is a visionary energy generation pathway that aims to harness very high-temperature geothermal resources beneath the earth’s surface. The pathway is deserving of public support and investment as it could tap into a zero-carbon, firm, energy-dense and renewable energy source, available everywhere with minimal land use. With strategy and robust funding, superhot rock energy could provide terawatts of locally sourced zero-carbon baseload power within a few decades, importantly contributing to the EU’s climate and energy security objectives. Early research into superhot rock energy was enabled by the EU’s Horizon programme, but further public investment is needed to mature the tools, equipment, and methods required and conduct a successful pilot demonstration. The US, Iceland, Japan, and New Zealand have all taken steps to bring this technology to demonstration, whereas in the EU there is no coherent effort towards this goal.

Similarly, Europe had been leading on fusion plasma science and technology, but is now at risk of lagging behind, as the US and the UK are taking the lead in building fusion prototype machines. While the EU is the largest contributor to the ITER project, where 35 countries are working together to prove the scientific and technological feasibility of fusion as a future energy source, ITER is not going to produce electricity and is not designed to lead to electricity production.

To accelerate the development of these high-potential innovative solutions, the EU must develop clear strategies, prioritise long-term R&D funding, establish public-private partnerships, and promote international collaboration.

8. Addressing the funding gap

The Draghi report emphasised the need for substantial investments to scale up clean technologies in Europe, referencing €750-800 billion in annual funding required to support the transition.

When it comes to the investment case for CCS, projections7 indicate that, despite carbon pricing, many emitters will still face a shortfall, with total costs in excess of €100/tCO₂. Similarly, recent project updates have highlighted the challenge of producing clean hydrogen at a cost competitive with fossil-based alternatives. In Europe, the average price for unabated hydrogen is around €3.5/kg, whereas the average price for electrolytic hydrogen is €6.5-7.5/kg – a price differential that significantly hinders market development. To address these challenges, support mechanisms must be established to create a viable business case for deploying these technologies. Funding for early-mover projects is an essential enabler of clean technology development that the EU urgently needs to accelerate.

This large-scale investment will need to combine public funds, at the EU and national level, and private sector funds. The amount available at the EU level will depend on the Multiannual Financial Framework negotiations and a broad consensus among Member States will be required to agree a budget fit for transition needs. The Recovery and Resilience Facility (RRF), currently the largest source of EU grants and loans for decarbonisation, will end in 2026, creating a major gap in funding for the green transition, estimated to be about €180 billion between 2024 and 2030. A solid EU budget will be crucial to ensure that Member States with more limited fiscal capacity are not left behind.

Several new initiatives have been recently announced to address the funding gap, notably the European Competitiveness Fund, the Clean Energy Investment Strategy, and Sustainable Transport Investment Plan. While the Innovation Fund has provided much-needed capital and operational cost support for demonstration projects in sectors such as hydrogen and CCS, decarbonisation technologies require support across all technology readiness levels (TRLs), using tailored mechanisms. Funding must therefore go beyond first-of-a-kind technology demonstrations for key decarbonising technologies. A dedicated clean technology deployment fund will be essential. The Competitiveness Fund could fulfil this role, but it will need to be carefully designed to balance technology openness with sufficiently targeted interventions to ensure impact.

The role of the European Investment Bank (EIB), the largest multilateral financial institution in the world and one of the largest providers of finance for climate action, is also crucial. Although the EIB Group’s Climate Bank Roadmap 2021-2025 commits to supporting various innovative low-carbon energy technologies, including CCS, nuclear fission and fusion, the EIB funding for these projects has lagged in practice. As noted, a broader range of clean technologies must be supported to address diverse contexts and maximise the chances of a successful transition. The Draghi report calls on the EIB to ‘take on more and larger high-risk projects, making greater use of the EIB Group’s own financial firepower’. Pilot demonstrations of superhot rock systems are a prime example of high-risk, high-reward projects that could be supported by EIB backing.

The establishment of new Important Projects of Common European Interest (IPCEI) in strategic sectors and technologies could also be key. IPCEIs have a track record of accelerating industrial production and unlocking private investment, as demonstrated in sectors like microelectronics, and batteries.

The EU should also make better use of its existing budget. As it stands, funding is spread across different mechanisms, which can be challenging to navigate. Improved coordination, potentially under one-stop-shops where project developers can find all funding opportunities and support in one place, could simplify application procedures and reduce bureaucracy. Efficient funding allocation is also key – auction-based models, carbon contracts for difference, or loan guarantees can be helpful in this respect. The concept of “auctions-as-a-service” could improve operational efficiency and, with appropriate safeguards, maintain free competition within the EU Single Market.

In the context of constrained public funds, all public funding allocations should be guided by clear climate benefits or strategic reasoning, with priority given to carbon abatement potential and cost-effectiveness. Projects without a clearly demonstrated case should not receive funding. A lifecycle perspective must also be applied, accounting for emissions and dependencies across the entire value chain. For instance, strategies such as hydrogen blending, synthetic methane, or synthetic diesel for light-duty vehicles are neither economical, nor effective for decarbonisation and should not be supported with precious public funds.

9. Building international partnerships

The geopolitical context has changed significantly over the last years and global competition for clean technology markets is growing. Strengthening collaboration on clean energy goals with non-EU governments will be essential for enhancing EU competitiveness and energy security. Such partnerships can help diversify energy sources, reduce reliance on high-carbon imports, and foster innovation in clean technologies.

On CCS, closer cooperation will be required with the UK and countries around the Mediterranean Sea to ensure efficient CO2 transport across borders. Similarly, stronger clean hydrogen cooperation will be required with the EU southern neighbourhood in the case where imports make sense from a technoeconomic perspective.

1 McKinsey (2020). How the European Union could achieve net-zero emissions at net-zero cost. https://www.mckinsey.com/capabilities/sustainability/our-insights/how-the-european-union-could-achieve-net-zero-emissions-at-net-zero-cost

2 CATF and Carbon Limits (2023), The cost of carbon capture and storage in Europe, https://www.catf.us/ccs-cost-tool/

3 CATF and ElementEnergy (2023), Unlocking Europe’s CO2 Storage Potential: Analysis of Optimal CO2 Storage in Europe, https://www.catf.us/resource/unlocking-europes-co2-storage-potential-analysis-optimal-co2-storage-europe/

4 DNV (2024)

5 MIT Climate (2023)

6 IEA – Net Zero by 2050 Roadmap www.iea.org/commentaries/net-zero-by-2050-plan-for-energy-sector-is-coming

7 IEA. (2023). CCUS policies and business models. https://iea.blob.core.windows.net/assets/d0cb5c89-3bd4-4efd-8ef5- 57dc327a02d6/CCUSPoliciesandBusinessModels.pdf