Strong EU methane regulations for imported gas can slash methane pollution globally

With the EU’s first bloc-wide methane regulation now entering its final legislative phase, negotiations taking place in Brussels can definitively move the needle on global methane emissions – as long as crucial provisions remain in the final bill. In May 2023, the European Parliament submitted its version of the bill and included several ambitious new measures, including the world’s first import standard for methane intensity from the oil and gas sector.

Clean Air Task Force’s analysis indicates that implementing an EU import standard for oil and gas could reduce a third of global methane emissions from the oil and gas sector and can bring us closer to achieving the Global Methane Pledge goal by 2030.

The European Union (EU) is the world’s largest importer of oil and gas; putting it in a unique position to leverage its buying power and climate ambition to drastically reduce global methane emissions from the oil and gas sector. The EU is working to finalize its Methane Regulation to reduce methane emissions from the oil and gas produced inside the EU; however, considering that the EU imports 90% of the gas and 97% of the oil it consumes1, our estimates indicate that an import standard would reduce 20 times more methane emissions than a regulation covering just domestic EU oil and gas production alone. We estimate that this regulation has the potential to reduce more than 30% of global methane emissions from the oil and gas sector, which represents 7% of all man-made emissions globally. If these reductions are accomplished by 2030, they would represent 20% of the necessary progress towards achieving the Global Methane Pledge.

From an energy security standpoint, the implementation of this legislation to EU imports of oil and gas, could save a total of 90 billion cubic meters (bcm) of gas from being lost and contributing to the warming of our atmosphere. The total gas saved represents almost the entire yearly consumption of Germany (94 bcm2), which is the highest consumer of gas in the EU.

From a purely economic perspective, the amount of gas saved would represent €54 billion in savings to exporting partner countries and €1 billion for oil and gas-producing countries within the EU.

Methane impacts not only our climate but also degrades air quality and increases health risks. At regional scales, methane contributes to air quality degradation by increasing ozone concentrations at ground-level. On a global scale, methane traps 80 times more heat compared to CO2 during the first 20 years in the atmosphere. While methane concentrations and global temperatures continue rising globally, scientists estimate that we will not be able to limit the planet’s warming to 1.5°C without drastic reductions of man-made methane emissions. Reducing methane emissions from the oil and gas industry is the most effective way to limit global warming and improve air quality and human health in the near term.

Altogether, an oil and gas import standard is an unprecedented opportunity, where a single piece of legislation can increase global energy security, decrease associated health risks by improving air quality, and bring large climate and economic benefits in the near term. For more information on how an EU Methane Import Standard could be implemented, read our research on this topic here.

Large methane emissions reduction will only be possible if the EU import standard sets a methane intensity target

Not all the oil or gas is produced in the same way. Emissions of methane associated with their production vary depending on factors such as available technologies, maintenance, leak detection and repair programs, etc. The ratio between those emissions and the total oil and/or gas production is known as methane intensity. Thus, the larger the methane emissions are per unit of oil and/or gas produced, the larger its methane intensity will be.

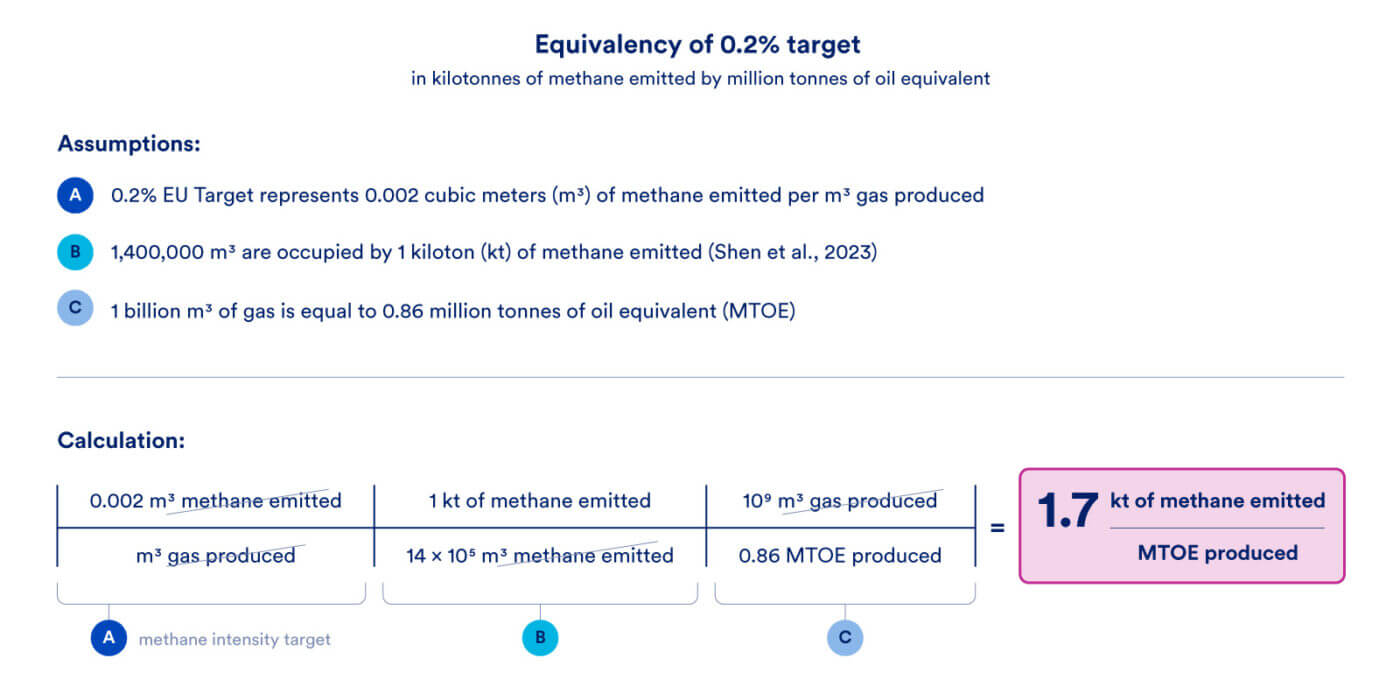

There are various definitions for methane intensity, some consider upstream methane emissions and production, while others consider emissions and production of oil and gas. The European Parliament is currently considering a methane intensity threshold for imports of 0.2%, which is based on a target established by the Oil and Gas Climate Initiative (OGCI)3. This definition was developed specifically for upstream gas production with the intention to estimate the methane lost to the atmosphere rather than taken to the market. Such definition can also be applied to mostly gas-producing countries. However, for countries or companies where the main product is oil, the result of calculating their methane intensities using this definition will produce unrealistically large values. In this context, setting up a target that intrinsically produces higher values for a specific industry could jeopardize its enforceability, be prone to criticism and present a high risk of invalidating the part of the legislation that could have the highest impact on global climate. Consequently, the development of a methane intensity target that accounts for methane emissions from the production of both oil and gas is needed.

With such an important regulation at stake, we suggest a threshold of 1.7 kilotonnes (kt) of methane emitted per million tonnes of oil equivalent (MTOE), which is equivalent to 0.2% on an energy basis, setting a more even playing field for oil and gas producing counties and companies.

How were the threshold, total emissions and associated impacts calculated?

The new methane intensity target for oil and gas production of 1.7 kt of methane emitted per MTOE is based on the 0.2% emission target established by OGCI. However, in order to be applied to both, oil and gas production, energy units are used instead of volume units. For this calculation, the intensity target of 0.2%, expressed as cubic meters (m3) of methane emitted per m3 of gas produced, was converted to kilotonnes of methane emitted per m3 of gas produced. Then, the volume of gas produced was converted to tonnes of oil equivalent, which is the quantity of the energy contained in a ton of crude oil. After those conversions, the value obtained was 1.7 kt of methane emitted per MTOE.

This new methane intensity target was used to estimate the emissions reduction on 20 EU trading partners significantly tied to the EU market assuming that their total methane emissions are abated enough to meet the new target. We note that Russia was not considered in this calculation as it is not expected to provide gas to the EU after 2027. For selecting the 20 countries, we considered only countries that export to the EU more than 10% of their oil production or 5% of their gas production. This consideration was made assuming that if a country exports less than the thresholds mentioned, they could easily opt to sell their product elsewhere in the world, rather than export to the EU and potentially pay a fee and/or have to invest in new technology to abate methane emissions in their supply chain4.

The country emissions for this calculation are based on two different methodology approaches: bottom-up (IEA Methane Tracker 20235, base year 2021 without including “satellite-detected” emissions data6) and top-down emission estimates derived from satellite observations (Shen et al., 20237, base year 2019). We estimate a total reduction of 24 million tons of methane emissions, which includes emission reductions inside the EU and for its trading partner countries. This value corresponds to the average of the total emissions reductions from both approaches.

This estimate represents the best-case scenario, whereby the selected countries exporting to the EU would take measures to ensure that all their production meets the methane intensity target. The full reduction potential will ultimately depend on how an intensity standard is developed and enforced, however if evaluated at the country level or based on national default emissions factors, exporting countries and companies would be incentivized to ensure all production meets a set intensity target. Additionally, if producers choose to abate emissions and ensure a significant portion of their exports meets an intensity standard, it would likely require taking abatement measures across wider operations. This would inevitably impact the intensity of oil or gas exported elsewhere.

Finally, using the total methane emission reduction, we estimated the corresponding volume of gas that would be saved and the economic benefit from it. For the first estimate, we considered a methane content in natural gas of 0.98 and a flaring efficiency of 91%9. Since the available top-down emissions do not report disaggregated emissions from flaring, we only used bottom-up estimates for this calculation. We estimated that a total of 90 bcm of natural gas would be saved if the EU implements an import standard that considers a methane intensity of 1.7 kt of methane emitted per MTOE. This total gas saved represents almost the entire yearly consumption of Germany, which is the highest consumer of gas in the EU. Moreover, it would represent savings to exporting partner countries of €54 billion and €1 billion for oil and gas producing countries within the EU.

Conclusion

As EU legislators work to finalize the Methane Regulation in the coming weeks, this analysis shows that policymakers have an exceptional opportunity to cut a third of global emissions in the oil and gas sector with an import standard, and reduce over 20

imes more emissions than a regulation covering production in the EU alone. These emissions reductions – more than double the annual gas consumption of France and Spain combined – create climate, energy security, health, and economic benefits, making an import standard one of the most crucial provisions in the Methane Regulation.

With methane concentrations continuing to rise annually, and just two months left to COP28, the EU’s leadership in the fight against methane emissions is critical. A bold Methane Regulation – the EU’s first rules on methane emissions in the energy sector – will not only reflect the EU’s commitment to achieving the Global Methane Pledge, it will also set the level of ambition for partners moving in the same direction. As the largest importer of oil and gas in the world, the EU is uniquely placed to catalyze global progress on methane and climate change, but doing so will require it to look beyond its borders.

1 European Commission, Proposal for a Regulation of the European Parliament and of the Council on methane emissions reduction in the energy sector and amending Regulation (EU) 2019/942, 2022.

2 Commission européenne, Quarterly report on European gas markets, https://energy.ec.europa.eu/system/files/2022-04/Quarterly%20report%20on%20European%20gas%20markets_Q4%202021.pdf

3 Oil and Gas Climate Initiative, https://www.ogci.com/methane-emissions/methane-intensity-target

4 An exception was made for countries with oil exports lower than the thresholds mentioned if the volume exported was higher than 15 million barrels. This exception was taken considering that high volumes of oil or gas cannot be easily marketed in other regions and that EU oil and gas imports are expected to increase in the near future, as the EU expects to end remaining oil imports from Russia by 2027. Therefore, the EU will need to buy oil from other exporting regions that have enough capacity to cover its high demand.

5 IEA Methane Tracker 2023, https://www.iea.org/reports/global-methane-tracker-2023

6 This consideration was made in order to exclude top-down estimates that were included into IEA Methane Tracker emission estimates since 2020.

7 Shen et al., 2023. National quantifications of methane emissions from fuel exploitation using high resolution inversions of satellite observations. https://www.nature.com/articles/s41467-023-40671-6

8 Alvarez et al., 2018. Assessment of methane emissions from the U.S. oil and gas supply chain. https://www.science.org/doi/10.1126/science.aar7204

9 Global Methane Tracker, Documentation 2023 Version, https://iea.blob.core.windows.net/assets/48ea967f-ff56-40c6-a85d-29294357d1f1/GlobalMethaneTracker_Documentation.pdf