Decarbonisation Hubs and The Opportunity for Deep and Rapid Carbon Reduction

As the world seeks to deliver on the complex challenge of building decarbonised energy systems, reducing CO₂ emissions from industrial operations is critical as these account for around 23% of CO₂ emissions, as per data from the International Energy Agency (IEA). Based on the current trajectory, European final energy consumption is not projected to decrease dramatically in the next three decades. Even worse, global emissions data from December 2020 showed a 60 million tonnes increase than the year before. This means our options for reducing CO₂ emission are shrinking, whilst the window of opportunity to prevent the worst effect of climate change is closing.

Efforts must be implemented immediately to start reducing current emissions and accelerate the path to decarbonisation. Efforts must begin using proven technologies and approaches that are ready to move into pragmatic action, while continuing to invest in research and concept creation. Industry has methods for emission-reduction to achieve set climate goals, however, there is currently no business case for private investment. Putting in place the right policy framework can change that.

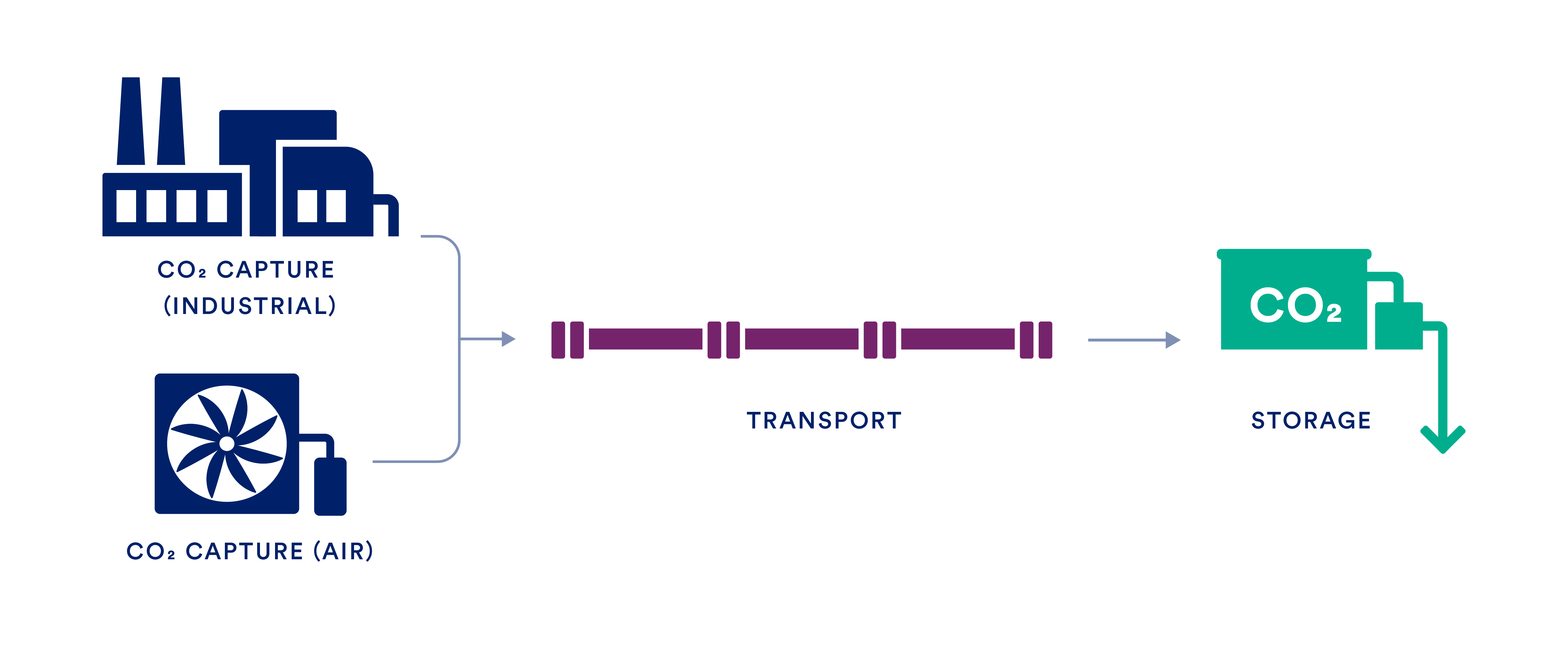

Often misrepresented as a novel technology, carbon capture, removal and storage is a proven carbon reduction approach. This suite of emissions control technologies fits alongside existing infrastructure to prevent CO₂ from reaching the atmosphere. Industry can use this technology to deliver multi-million tonne reductions in CO₂ emissions. The United Nation’s Intergovernmental Panel on Climate Change (IPCC) has given some context to the scale of CO₂ capture required, including the technologies in three of four of its illustrative scenarios. Reaching this will only be possible through the deployment of carbon capture, removal, and storage technologies, and policy endorsement thereof, so that it can deliver on its emission reduction potential at a meaningful scale.

Shared systems of CO₂ transport infrastructure and geologic storage will enable the necessary scale through the build out of CO₂ reduction hubs. The hub approach enables collaboration and the sharing of infrastructure. This connects multiple CO₂ capture sites at industrial facilities to secure geologic storage locations using shared pipeline transport networks, enabling faster implementation of carbon capture, removal, and storage. When applied at scale, this technology can take energy-intensive processes towards a decarbonised future. This is crucially important as industrial sectors employ millions of people globally, so decarbonising high-value industries such as, iron and steel, chemicals, refinery and cement helps maintain local jobs that provide a range of products that are essential to everyday life.

However, slow uptake of these facilities is due to the high cost of the emission reduction technology and only by closing this funding gap through public-private partnerships can we see significant infrastructure build-out.

Informing policy makers of the benefits of carbon capture, removal, and storage is an ongoing process and policy endorsement will enable wide scale uptake of CO₂ reduction and its benefits.

Building decarbonised industries also requires the inclusion of hydrogen, which has been highlighted as playing a key role in decarbonisation. For this to occur, there needs to be room for hydrogen production and deployment as a fuel source with the government giving industry the green light to retrofit existing hydrogen production facilities with carbon capture equipment. This will enable industrial sectors to reduce carbon emissions with specific focus on building CO₂ capture and storage infrastructure, which will also be the enabling framework for expanded hydrogen usage and the infrastructure used by green hydrogen in the future.

A realistic climate strategy that achieves deep decarbonization must ensure that technology commercialization is at the centre of policy strategy, where the private and public sector can collaborate for wide scale deployment. Endorsing a diverse set of decarbonisation methods allows build-up of infrastructure and the direction of resources towards proven decarbonisation methods. This means harmonized and specific policy and funding mechanisms that enable wide scale uptake of technologies, as well as support for retrofitting existing industrial plants.

Decarbonisation hubs can be interconnected into a CO2 Network

A hub approach has many advantages, which include interconnected transport systems that collect CO₂ from multiple capture sources for delivery to shared storage locations. These shared decarbonisation hubs enable emissions from different industrial activities to utilise a shared network infrastructure and gain access to secure geologic storage facilities.

Shared infrastructure with access to available storage capacity means emitting industries can access the CO₂ network service with greater ease, with minimised administrative barriers since activities are already licensed within the network. This enables industry to plan projects focused on carbon reduction activities rather than needing to invest into the full chain of carbon capture, removal and storage. This is especially important since suitable geological storage does not exist in every European country, therefore a shared service for transporting and storing CO₂ will provide industrial sites across Europe the ability to reduce emissions.

Network effects are well understood. Coordination of investments creates additional linkages, yielding commercial synergies that enable faster uptake as it is more cost effective to build large infrastructure facilities for CO₂ transport and storage rather than multiple smaller ones.

Industry actors have planned industrial hubs, networks and clusters that demonstrate CO₂ capture, transport and storage infrastructure for deep emission reductions in industrial production of iron, steel, cement, and chemicals. Countries with funding and policy support have been able to initiate first mover projects, allowing industry to begin to invest in net-zero infrastructure whilst maintaining critical economic and social functions.

For example, in Norway and the UK national policy has provided government subsidies for specific projects and enabled industries to initiate planning of projects. The Netherlands and Denmark have also committed to using carbon capture, removal and storage to achieve national emission reduction targets which has also seen project activity emerge.

In Norway, Northern Lights will be Europe’s first CCS operating hub demonstrating a cross-border, open-source CO₂ transport and storage infrastructure network offering companies across Europe the opportunity to store their CO₂ safely and permanently deep under the seabed. Additionally, a cluster of energy intensive companies are working together to build a CO₂ network in Teesside in the United Kingdom. The role of carbon capture, removal, and storage has been emphasised by the UK government as a key decarbonisation strategy, with national targets for deployment and financing instruments, enabling industry to provide a solution for their carbon emissions through planning CCS hubs. In the Netherlands, a storage hub is planned in the Port of Rotterdam to provide a CO₂ service for the transport and storage of captured CO₂ from various companies. The final investment decision is due in 2022.

Whilst these first mover projects are positive demonstrations of what is achievable, government efforts so far have not provided the framework to develop a market system for carbon capture, removal and storage to decarbonise industry on a mass scale. It is important to further develop these into a regional strategy and action through partnerships that include joint deployment targets, regional hubs, clusters and key project opportunities for carbon capture, removal and storage as well as a joint regional atlas for permanent CO₂ storage.

Policy mechanisms are now needed for government and industry to work together to achieve wide scale decarbonization of industrial activities.

Policy support is needed to drive expansion of decarbonisation hubs

Adding carbon capture, removal and storage applications to industrial facilities consumes additional energy and adds to the cost of production, which is partly why it has been especially challenging to develop an effective funding model. It is well understood that it provides a cross-sector pathway to net-zero emissions, however, we need wide scale uptake – that is not possible without considerable investment support.

But this is not a problem unique to carbon capture, transport and storage.

Take electric cars. Government support for the cost and installation of charging networks was required to encourage adoption. Initial investment support is needed to install the enabling infrastructure that kickstarts a new market, by de-risking projects and ensuring public acceptability. Individual incentives and infrastructure availability encouraged the private sector to scale-up production and consumers to buy electric vehicles (EV). For example, Norway’s government leadership has seen the build out of its EV market, introducing a joint ventures scheme with the private sector whereby the local government paid companies to set up and operate charging stations. Other examples include Germany, where electric vehicle subsidies have been extended and in the Netherlands, where EV subsidies increased in 2021.

Government policy commitment sends a positive investment signal to the private sector to initiate the build out of a new market and encourage the scaling up of production through investment security.

Similar policy support and investment is needed for the carbon capture, removal and storage market to be activated and replicate the cost curve that other new climate technologies followed. Specific support is needed for the next batch of hubs, and to address capital flows and markets separately.

Whilst several success factors have aligned to have demonstration projects develop in Europe, we do not yet have a roadmap for widescale deployment. We have seen some funding commitments, the EU Emissions Trading System (ETS) being driven up, net zero targets, rising penalties on CO₂ emission and favourable business models which have enabled these projects and created gateways for a CO₂ market. However, replicating this across Europe requires policy makers to set predictable conditions. Industry has now turned towards governments for support to grow decarbonisation networks at the appropriate pace and scale.

Network implementation of decarbonisation hubs

A smart roll out of decarbonisation networks is required for carbon capture to take off in a meaningful way. Policy makers must respond to industry, who have the means to decarbonise but need a framework for implementation. This means certainty of the role of these technologies and methods in a decarbonised future with harmonised endorsement for carbon capture, removal and storage as a carbon reduction method, so that industry can plan for widescale uptake. Policy needs to address both the development of at-scale CO₂ transport and storage infrastructure, and provide capture technology deployment incentives for facilities to capture their carbon.

- Financial Incentives. Specific financial incentives supporting implementation and build out of CO₂ transport and storage infrastructure is needed. Whilst the EU Innovation Fund is driving some investment by providing capital support for innovative technologies, these funds are shared across a range of technologies, so the amount is not sufficient for full-scale commercialization of carbon capture, removal and storage. With the first round of applications is oversubscribed, additional capital grants that provide specific funding of carbon capture, removal and storage projects could be helpful. Moreover, the Trans-European Energy Networks Regulation (TEN-E) is critical for transboundary CO₂ transportation networks and establishing cross-border CO₂ infrastructure in Europe. Whilst it is encouraging to see that the European Commission has signaled support for carbon capture, removal and storage as a net-zero method for industry to undertake in its proposal to include cross-border CO₂ pipelines, the framework is incomplete since the entire value chain of carbon capture and storage is not recognized by the TEN-E. This means including support for all CO₂ transport options and the geologic storage of CO₂. This is especially important for the hubs and cluster design of projects as captured CO₂ may need to cross several country borders in Europe to reach storage sites. To enable a market system for carbon dioxide capture and storage the EU policy framework must allow and enable for all parts of the value chain, to provide certainty for project development and incentivize investment by showing government commitment to the necessary infrastructure. Investment into capture carbon capture as well as the infrastructure to transport and store CO₂ is needed so geologic storage resources can be accessed by member states.

- ETS Integrations. Policymakers must find ways to bridge the gap between actual operating costs of carbon capture, removal and storage and the current price of the European Emission Trading System. This kind of policy support is needed to incentivize investment in carbon capture in the near-term. These can be awarded based on reduced CO₂ emission reduction, such as for example through carbon contracts for differences. CFDs have successfully supported the commercialization of renewable energy technologies in the form of feed-in tariffs and set a pathway to integrating innovation objectives climate policy.

- Targets and timelines. Clear targets for industry to reduce emissions with timelines for deployment and required volumes for deployment of carbon capture, removal and storage. Targets must be supported by established greenhouse gas accounting for carbon removal approaches, incentivized by certificates for carbon removal will provide transparency.

- Higher carbon prices. Policymakers must continue to push for much higher carbon prices whilst carbon, capture removal and storage is not commercially viable. Although the EU Emissions Trading System (ETS) has put a price on carbon and built the world’s first major carbon market, it is not trading high enough to incentivize uptake without complementary policies, as outlined above.

Conclusion

Europe can fulfil the transformative potential of its energy industry by setting standards, models, and regulations that the rest of the world follows.

The European Commission has committed funding to six CO₂ transport and storage network projects in five European countries. Critical success factors are aligned for Europe [PDF] to benefit from the potential of hubs. The next step is providing the market with a business model and revenue support mechanism to stimulate private investment into widescale projects uptake. Innovative models that minimize projects risks for long-term-capital funding materially de-risk projects and encourage private investors who are guided by aligning existing legislation with climate targets.

A greenhouse gas emissions reduction of at least 55% by 2030 compared to 1990 levels has been set by the European Council – achieving this goal depends on the measures implemented. The roadmap needs to be met by political commitment, and coordination is essential to maximise economies of scale and carry-over benefits across countries and regions. Most decarbonisation pathways state the need for carbon capture, removal and storage, meaning we need to set the foundations for market uptake. These systems will be the key backbone infrastructure needed for at the necessary scale of a decarbonised market, creating an industry in its own right.