Getting Hydrogen Right for Poland’s Industrial Decarbonisation

About this brief

This brief presents additional recommendations for the updated Poland Hydrogen Strategy (PHS), highlighting that this approach will help deliver rapid emissions cuts today, protect Poland’s industrial base, and lay the foundation for future renewable hydrogen deployment without undercutting broader decarbonisation efforts. It emphasizes the need for Poland to pursue a pragmatic strategy that supports the deployment of other clean hydrogen alternatives, namely low-carbon hydrogen produced with carbon capture and storage (CCS).

Clean hydrogen will be essential for Poland’s transition to a net-zero economy. As Europe’s third-largest producer and consumer of hydrogen, Poland will require significant volumes of clean hydrogen to keep its industrial base active and well-positioned in a net zero economy. Decarbonising this hydrogen will also be critical for meeting wider European Union (EU) climate targets.

Renewable hydrogen will be an essential tool for this long-term transition to net zero but today, the country’s carbon-intensive electricity grid and limited renewable energy capacity make it too costly and intermittent to supply to industry at scale. To avoid delays in industrial decarbonisation, Poland must pursue a pragmatic strategy that supports the deployment of other clean hydrogen alternatives, namely low-carbon hydrogen produced with carbon capture and storage (CCS).

With an updated Polish Hydrogen Strategy (PHS) expected to be published in the coming months, it presents a critical opportunity to design a more comprehensive hydrogen policy framework. Building on CATF’s initial set of recommendations for the updated PHS, this brief digs further, recommending Poland to:

- Prioritise the deployment of clean hydrogen in heavy industry, especially sectors who already use hydrogen, to secure stable, long-term offtake and drive decarbonisation in hard-to-abate sectors where hydrogen consumption is essential.

- Support a staggered approach to deploying different clean hydrogen production pathways that accelerates meaningful deployment, first with the immediate scaling of low-carbon hydrogen in existing offtake industries, while planning for broader renewable hydrogen deployment once Poland’s electricity system is more deeply decarbonised.

- Align clean hydrogen deployment with a cluster-led industrial decarbonisation approach, anchoring low-carbon hydrogen as an important enabler to necessary CCS infrastructure deployment in priority industrial cluster locations, creating the backbone for Poland’s wider industrial decarbonisation.

This approach will deliver rapid emissions cuts today, protect Poland’s industrial base, and lay the foundation for future renewable hydrogen deployment without undercutting broader decarbonisation efforts.

Recommendations

1. Prioritise the deployment of clean hydrogen for industrial decarbonisation needs

As a major EU industrial hub, Poland’s accounts for approximately 710 kilotonnes (kt) of hydrogen per year concentrated across eight major industrial sites1, primarily in refining, fertilisers, and chemicals production.

Almost all this hydrogen is derived from fossil fuels, producing approximately 7.8 million tonnes of carbon dioxide emissions annually (MtCO2eq/pa) 2. Decarbonising hydrogen for these existing hydrogen consumers should be of high priority for clean hydrogen deployment in Poland as they will require a clean hydrogen alternative to decarbonise their operations.

Poland may also seek to deploy hydrogen in further industrial sectors not yet using hydrogen where limited or no other decarbonisation options exist, such as steel. Hydrogen is considered a frontrunner route to decarbonising primary steel production via the direct reduced iron (DRI) method. Poland’s primary steel sector currently operates a capacity of 5Mt of finished steel per annum3 and to decarbonise this entirely with clean hydrogen would require an additional 240kt of hydrogen4.

Existing industrial use alongside possible steel deployment would see significant volumes of clean hydrogen demand, higher than the current nascent market can supply. National policy in Poland must therefore incentivise market ramp up in these lead markets now.

Figure 1: Nine industrial sites for priority deployment of clean hydrogen in Poland

Under the EU Renewable Energy Directive (REDIII), each Member State is mandated to use at least 42% renewable hydrogen in their industry by 2030, rising to 60% by 2035. For Poland, this will require at least 180kt of renewable hydrogen consumption in industry by 2030, increasing to 257kt by 20355, to meet this mandate.

Whilst the 2021 PHS identified multiple possible sectors for clean hydrogen deployment across its economy, it lacks the level of detail needed to chart a path for how Poland can map and implement important projects in priority sectors that will lead to meaningful national emissions reductions.

The upcoming PHS update should therefore prioritise deployment to existing consumption in refineries, ammonia and chemicals production and, where feasible, primary steel production. Prioritising these sectors will kickstart decarbonisation of some of Poland’s most emissions-intensive industries and provide a secure offtake for clean hydrogen producers, whilst also contributing to meet crucial EU targets.

2. Support a staggered approach to the deployment of different clean hydrogen production pathways

There are several pathways to producing clean hydrogen, but only renewable hydrogen – also known as renewable fuels of non-biological origin (RFNBO) – can be counted towards meeting existing EU hydrogen mandates.

Whilst renewables capacity is expanding, Poland currently has limited renewable energy sources (RES) and use of them to produce renewable hydrogen would put further strain on their deployment. Renewable energy should first be deployed to decarbonise Poland’s highly carbon-intensive electricity grid. Prioritising the displacement of coal in the power sector would deliver greater environmental benefits, avoiding 832gCO₂eq/kWh compared with just 205gCO₂eq/kWh if the electricity were used to displace existing hydrogen supply with renewable hydrogen6.

Even if available RES were prioritised for hydrogen production, there will be significant challenges in meeting the EU renewable hydrogen mandates. For example, the 2030 renewable hydrogen in industry mandate would require 1.6GW of electrolyser capacity be installed across Poland, which will be infeasible to deliver given typical hydrogen project delivery timelines.

Projects will also struggle to provide the stable baseload supply required by industry at least until the grid is sufficiently decarbonised, which is not yet on Poland’s near-term horizon. Yet stability of supply is what these highest-priority hydrogen customers require. The processes that they operate are highly inflexible and lack the ability to ramp up or down frequently around variable renewable hydrogen supply. Whilst solutions such as hydrogen storage or electrolyser oversizing can close some of this gap, they will not be enough to overcome some degree of intermittency and also require significant infrastructure build out, increasing delivered hydrogen costs.

Renewable hydrogen will also remain significantly more expensive than other low-carbon hydrogen alternatives. Poland has the highest costs for pay-as-produced renewable power purchase agreements (PPAs) in Europe and with EU rules limiting eligible electricity sourcing options, renewable hydrogen will depend heavily on these arrangements. Optimising renewable hydrogen production may see a levelized cost of hydrogen (LCOH) at €11.99/kgH2 for a grid connected project and €9.17/kgH2 for an arrangement of the electricity supply via a direct line. Both options are significantly higher than the average cost of grey hydrogen, currently retailing in Europe at just over €3/kgH27. These very high production costs, coupled with the challenges in meeting the baseload demand, make replacing unabated fossil-produced hydrogen with renewable hydrogen in industry an expensive and challenging proposition, which could undermine the competitiveness of Poland’s hydrogen consuming industries.

While some solutions to the renewable hydrogen barriers are available they will take time to implement and scale. To avoid delaying the decarbonisation of industry, Poland must look to alternative clean hydrogen options in addition to renewable hydrogen for a decarbonised supply.

Low-carbon hydrogen – produced through reformation of natural gas with CCS – is an alternative production pathway that can facilitate the decarbonisation of Polish industry, supplying a consistent, reliable and lower cost supply of clean hydrogen. Low-carbon hydrogen projects should be developed in parallel to rapid RES deployment for electricity grid decarbonisation.

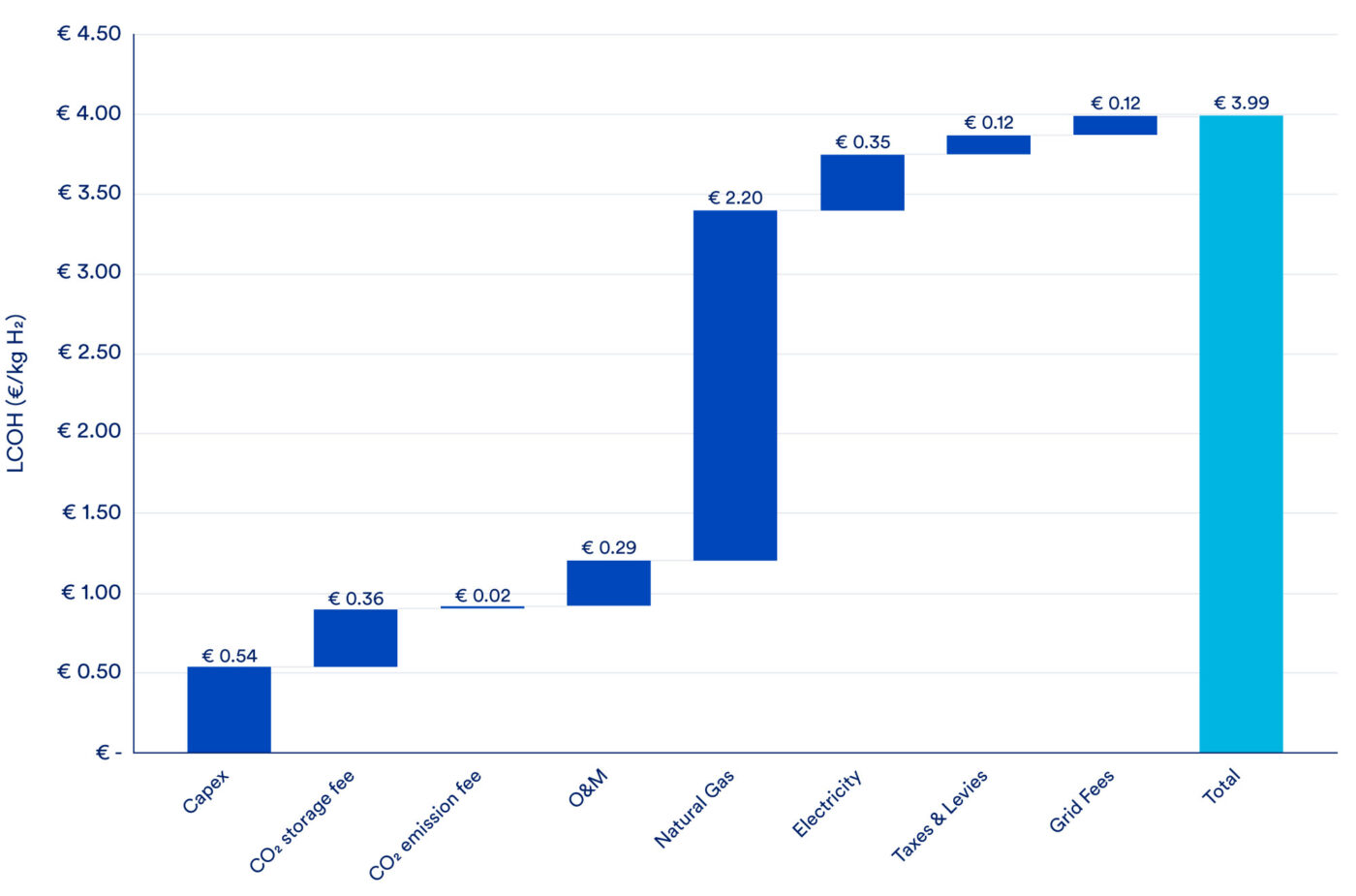

Low-carbon hydrogen can be produced at prices significantly lower than renewable hydrogen in Poland. Figure 2 shows the potential LCOH of Polish low-carbon hydrogen with a modelled cost of €3.99/kgH28, driven primarily by the cost of procured natural gas. At present this is slightly higher than unabated hydrogen due to the additional CO2 storage costs and electrical and natural gas demands from the CO2 capture, treatment and compression process. However, as the EU Emissions Trading System (ETS) carbon price increases and free allowances are phased out this price differential will likely level out or make low-carbon hydrogen more cost-competitive.

Figure 2: LCOH waterfall chart for low-carbon hydrogen production in Poland

Polish low-carbon hydrogen can achieve meaningful emissions reductions in line with EU rules by sourcing lower carbon-intensive natural gas for production and achieving high CO2 capture levels (i.e., 97%). In practice, high carbon capture rates may be challenging to achieve when retrofitting CCS onto an existing facility. To overcome this, projects leveraging lower capture rates should source lower carbon intensive grid electricity to ensure a compliant emissions profile of the produced hydrogen9.

At present, only renewable hydrogen is eligible to meet EU hydrogen mandates under REDIII, despite the European Commission setting a methodology for acceptable low-carbon hydrogen production pathways10. With these standards now in place, low-carbon hydrogen can achieve similar emissions reductions, but developing it at a meaningful scale will be severely hampered unless it can be counted toward EU hydrogen decarbonisation targets.

The EU eligibility criteria lack the nuance needed to support Member States like Poland who face significant challenges in scaling renewable hydrogen production and yet require substantial hydrogen volumes to decarbonise their industries. A technology-neutral, emissions-focused approach to hydrogen production would unlock faster and more cost-effective decarbonisation opportunities in a manner that will not come at the detriment to either wider national decarbonisation or industrial competitiveness.

Prioritising rapid low-carbon hydrogen development, particularly for heavy industry users, in the updated PHS will enable stable and cost-competitive clean hydrogen supply without compromising wider decarbonisation efforts. Further, Poland could play a leading and constructive role in ongoing discussions on the existing EU hydrogen framework, highlighting the needs and benefits of recognising all demonstrably low-carbon production pathways as credible clean hydrogen sources, to speed up the transition and lower the costs. Greater flexibility on eligible production pathways would allow Poland to decarbonise its hydrogen demand, advancing EU-wide energy and climate goals more efficiently.

3. Align clean hydrogen deployment with cluster-led industrial decarbonisation

As the EU’s fifth largest emitter of greenhouse gases (GHG)11, Poland’s heavy industrial base contributes significantly to national CO2 emissions. But with EU ETS free allowances being phased out, there is an immense task to reduce industrial emissions over the next decade.

It is widely recognised that CCS will be needed to decarbonise some hard-to-abate sectors, such as cement and lime, iron and steel, and refining, as signalled in Poland’s updated National Energy and Climate Plan (NECP)12. However, its effectiveness depends greatly on timely deployment at scale. To facilitate this, CO2 transport and storage (T&S) infrastructure should be first deployed in regions where high-emission industries are located within close proximity, known as an ‘industrial cluster’. By clustering emitters, shared infrastructure can be deployed at scale, driving down costs and spreading the high capital infrastructure expense across multiple industrial users. This not only reduces the CO2 storage costs, but also creates a backbone for wider industrial decarbonisation while maintaining competitiveness.

With the EU’s Net Zero Industry Act (NZIA) mandating minimum carbon storage development by 203013, T&S infrastructure development needs to start now. Poland has initially focused much of its CCS efforts on exporting CO2 to offshore North Sea storage projects14. CATF analysis highlights that Poland has even wider CCS potential if it leverages onshore storage closer to capture points, which can achieve lower costs than offshore, leveraging over 15Gt of total potential storage capacity resources15.

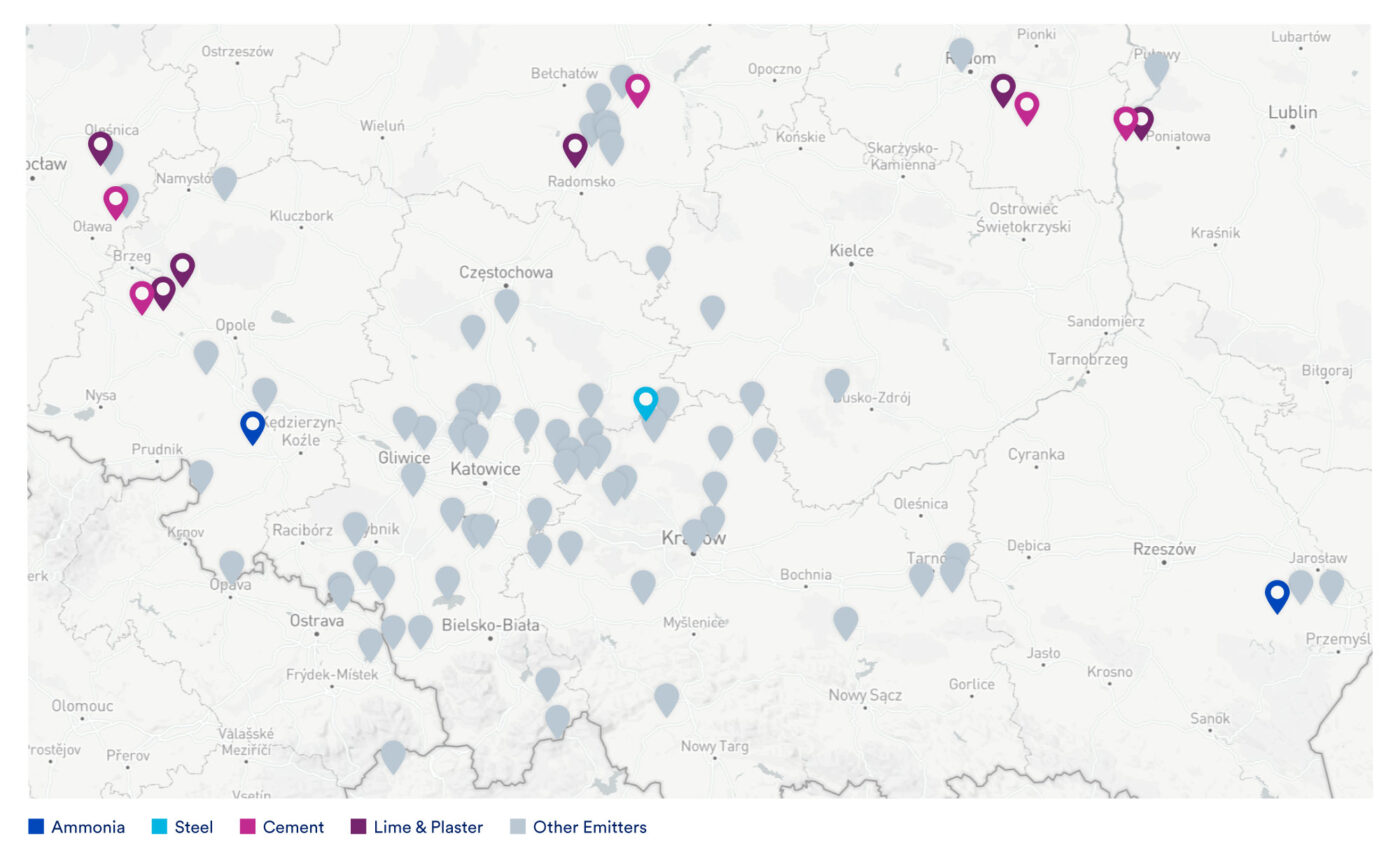

Low-carbon hydrogen projects can play a central role in supporting CCS development by acting as anchor emitters within industrial clusters, enabling the scaling of CO2 T&S infrastructure and Poland meeting its NZIA storage development mandates. One example is the Silesia-Opole region in Southern Poland (figure 3). This highly industrial zone is home to much of the cement, lime and plaster production in Poland, industries where CCS is critical for decarbonisation, as well as two major existing hydrogen users and Poland’s only operational primary steel manufacturing facility. This clustered industrial demand for both clean hydrogen and CCS makes it an ideal candidate for deploying region-wide CO2 T&S.

Figure 3: Potential CO2 sources for an industrial cluster in southern Poland

Poland should therefore prioritise assessing and identifying the highest priority industrial cluster locations where CCS and clean hydrogen are required and implement a harmonised strategy for carbon management and clean hydrogen for industrial decarbonisation across its national policy framework, embedded within the NECP, PHS, and CCUS strategy.

Footnotes

- Other Polish hydrogen consumers exist but they operate at significantly smaller volumes than these major users.

- Three facilities operated by Grupa Azoty in Poland produce urea for which process CO2 is captured as a feedstock, this is not accounted for in estimated sectoral GHG emissions.

- Based on Eurofer data that accounts for plant closures.

- Based on a hydrogen demand rate of 53.5 kgH2per tonne of crude steel.

- Due to the EU REDIII definition of industrial use excluding hydrogen used to produce transport fuels in refineries the RFNBO target of 180kt is smaller than 42% of current demand.

- An average carbon intensity for electricity from coal generation has been taken from the 180 operational lignite and hard coal plants in Poland (Instrat, 2023). Environmental impact of deploying RFNBO based on a grey hydrogen carbon intensity 11 kgCO2e/kgH2 (Roy, et al. 2025)

- September 2025 average figures.

- The LCOH for low-carbon hydrogen is highly dependent upon natural gas costs and to a lesser extent CAPEX, LCOH could be in the range of €2.51-5.78/kg.

- For example, a 5% lower carbon intensive grid would help balance a 95% capture rate and a 36% lower carbon intensive grid to balance a 90% capture rate.

- The EU Low Carbon Fuels Delegated Act (2025) sets the rules for compliant low-carbon hydrogen production.

- EEA, 2023.

- Draft National Energy and Climate Plan for 2030 with a perspective to 2040 – version submitted for further consideration at the level of the Council of Ministers in July 2025.

- The NZIA introduced the obligation for certain EU-based oil and gas producers to contribute to the Union objective of reaching 50 million tonnes of CO2 injection capacity in the EU by 2030. Commission Decision 2025/1749 identified Orlen as having a pro-rata share of this equivalent to 4.1MtCO2pa of operational CO2 injection capacity by 2030.

- Such as the ECO2CEE project that will capture emissions from the refining and cement plants in Płock and Kujawy in northern Poland.

- The recently announced draft regulation from the Minister of Climate and Environment (MKiŚ) amending the rules on permissible regions for the underground storage of CO2 should help to unlock these resources. This is scheduled for publication on 1 January 2026.