The EU’s low-carbon hydrogen rules show promise, but lack clarity

As the world’s third-largest hydrogen consumer, getting clean hydrogen right is crucial for decarbonising the EU’s hard-to-abate industries. Finalising the implementation of the methane emission rules will not only provide clarity for investment decisions but also drive rapid progress toward truly low-carbon hydrogen. Here’s why swift action from the European Commission matters.

Following the adoption of the EU Hydrogen and Gas Decarbonisation Directive in 2024, the European Commission was tasked with establishing a methodology – the low-carbon fuels delegated act – for calculating associated greenhouse gas (GHG) emissions from low-carbon fuels, such as hydrogen. This was released on the 8th July 2025; this blog represents our initial thoughts on the benefits as well as the gaps in the methodology.

The methodology put forth by the Commission provides a strong starting point for scaling low-carbon hydrogen production in the EU; however, some concerns remain regarding the accurate sourcing of methane carbon intensity data from the reporting obligations. Once addressed, this will help to ensure the framework enables meaningful emissions reductions while supporting the development of viable low-carbon hydrogen projects.

Clarity on methane reporting obligations is essential to provide assurance on sourcing low-carbon hydrogen

Methane emissions are a significant contributor to the lifecycle emissions of low-carbon hydrogen. The published methodology sets a default upstream methane emission factor of 10.3 gCO₂eq/MJ LHV1 (excluding emissions from LNG), to be used until measured, independently verified data becomes available to the hydrogen producer. This is expected to be made available under the methane reporting obligations2 from 2028, which is likely to draw on methodologies such as OGMP 2.0.

While pragmatic, the default value of 10.3 gCO₂eq/MJ is lower than methane intensities seen in some major supply regions, such as Russia and the United States, where leakage rates are generally higher. The default value should steadily increase as producer-specific data becomes available. However, there appears to be little incentive for suppliers of high-carbon intensity methane to provide measured data if the default value is more favourable.

As noted, the default value does not include emissions from LNG supply chains, which must be accounted for separately. The method for doing so is unclear, as it relies on yet-to-be-defined values from the Methane Transparency Database. Unlike upstream emissions, there are currently no recognised published voluntary methodologies for LNG-related methane emissions.

Emissions from gas pipelines into the EU are not accounted for in the low-carbon hydrogen methodology. This omission is significant, as it risks undermining the climate credentials of low-carbon hydrogen projects using imported gas.

Europe already has access to sufficient volumes of methane for low-carbon hydrogen production

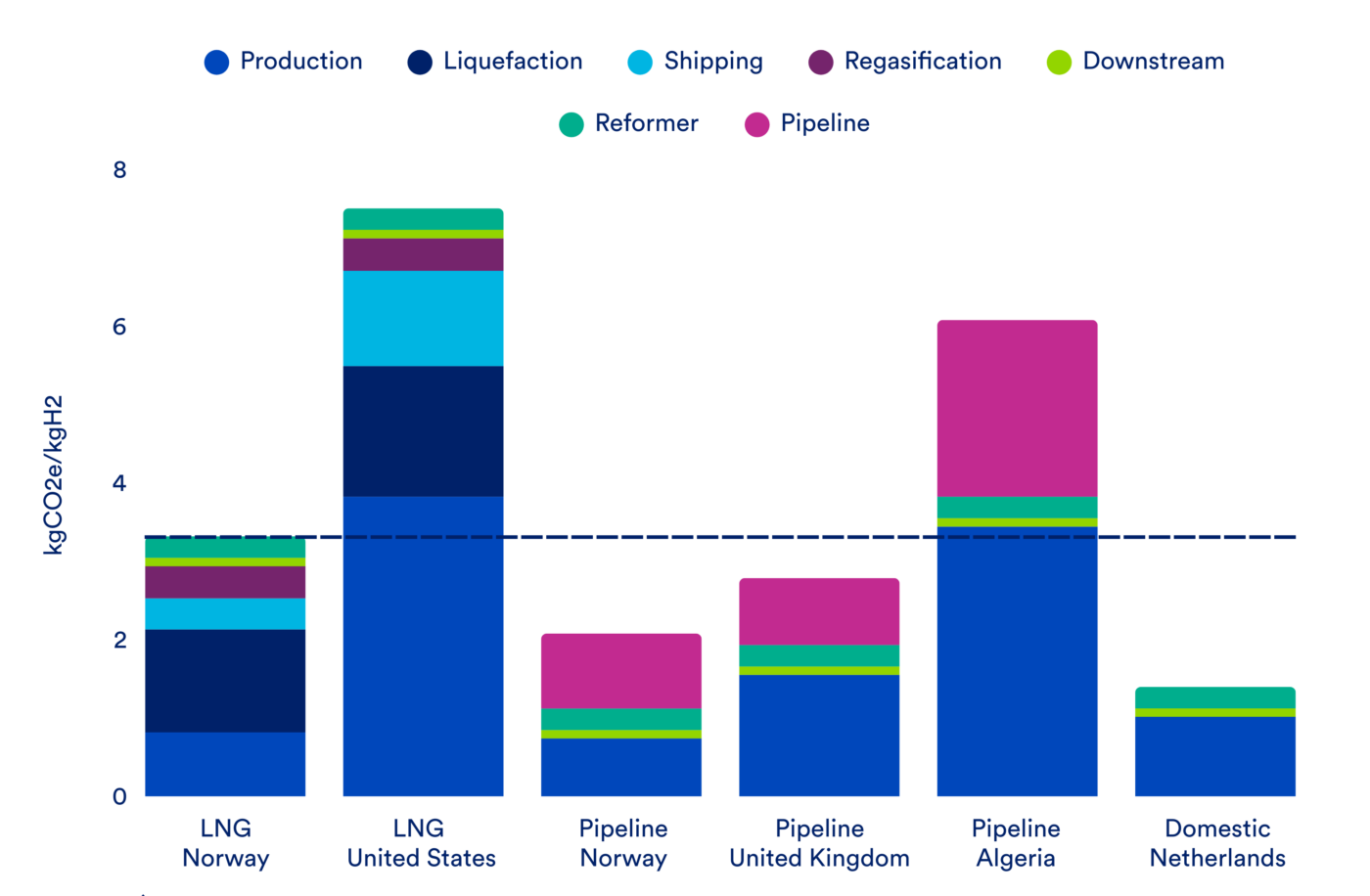

The methodology defines a maximum carbon intensity threshold for low-carbon hydrogen to match the renewable threshold of 3.38 kgCO2eq/kgH2. This is a threshold that can be achieved when low-carbon hydrogen is produced using methane captured domestically and lower carbon intensive imports from regions such as the UK and Norway3, which, between them, export 78 million tons per annum of methane which could produce around 24 Mt of hydrogen far above Europe’s current hydrogen demand.

This will likely result in this methane being sold at a premium, giving an incentive to other methane suppliers to decarbonise their supply chains.

However, as shown in Figure 1, gas imports from other important regions are expected to exceed the low-carbon hydrogen intensity threshold. These issues are not insurmountable if importers take the necessary steps to mitigate emissions, which is true even when using the 20-year Global Warming Potential (GWP)4.

Liquefied natural gas (LNG), which supplied 33% of EU demand in 2024, presents a significant challenge. A recent International Energy Agency report estimated emissions from LNG supply could be reduced by over 60% using today’s technologies5, making most methane import pathways able to comply with low-carbon hydrogen production standards.

Figure 1: Carbon intensity profiles of EU-imported methane6

Low-carbon hydrogen can help drive methane mitigation with the EU’s trading partners

This Delegated Act means that low-carbon hydrogen project developers will be required to source lower-emission methane to be eligible for the ‘low-carbon’ label. This will create a willingness to pay a premium for such methane, incentivising producers and transporters of the gas to further reduce their carbon emissions. Broader market development under the EU Methane Regulation is expected to accelerate this shift.

By incentivising gas with lower methane emissions, the EU can influence global supply chains, encourage innovation, and ensure that low-carbon hydrogen is both an environmentally credible and an economically viable pathway to supporting the EU’s decarbonisation in the coming years.

To better achieve a lower-carbon methane supply chain and provide greater certainty for low-carbon hydrogen project developers, the following measures should be taken:

- Import pipeline emissions should be included in any calculations, with the default values for both LNG and pipeline emissions published in the Methane Transparency Database as a matter of urgency, to provide project developers with clarity on full supply chain emissions.

- In parallel, a methodology should be developed to enable international pipeline owners and LNG shippers to demonstrate their emissions performance more effectively than the default and be recognised for supplying lower-carbon gas to the EU.

- Finally, to encourage the use of measured and reported emissions data over defaults, the EU should consider raising the default value over time, incentivising continuous improvement and discouraging reliance on conservative assumptions.

This blog marks the first in a series covering the viability and market development of different clean hydrogen production pathways in the EU against the backdrop of the existing hydrogen policy framework. Stay tuned for forthcoming posts covering nuclear hydrogen, geologic hydrogen, and more.

1 The default value for methane (excluding combustion) are: CO₂: 4.9 gCO₂ /MJLHV, CH₄: 0.19 gCH4 /MJLHV N₂O: 0.00037 gN2O/MJLHV for a total default value of 10.3 gCO₂eq/MJLHV.

2 Regulation 2024/1787, Article 29.

3 Countrywide methane carbon intensity data is based on International Energy Agency’s (IEA) Methane Tracker and Natural Gas Supply data. It should be noted that the IEA Methane Tracker may significantly underrepresent actual emissions.

4 A 20-year GWP for methane has been assumed of 82.5 kgCO2/kgCH4 vs the 100-year GWP of 28 kgCO2/kgCH4

5 IEA: Assessing Emissions from LNG Supply and Abatement Options.

6 This assumes a 97% carbon capture rate, however this is still credible with a 90% capture rate.