Making hydrogen work for Poland: Four insights from our expert roundtable in Warsaw

As Europe’s third-largest producer and consumer of hydrogen, Poland will need clean hydrogen to keep critical industry active and well-positioned to meet climate goals. But the country has deployed almost no renewable hydrogen today.

With looming regulatory reforms and deadlines, Poland has reached a crossroads and must decide the right path to clean hydrogen implementation that is fit for the country’s needs.

To better understand the challenges facing hydrogen deployment in Poland, CATF and Reform Institute recently co-hosted a roundtable in Warsaw. The event gathered stakeholders from across government and industry as a crucial touchpoint to dig into exactly how Poland can scale clean hydrogen without slowing its net-zero progress or undermining competitiveness. Below are some key insights from our conversations.

Hydrogen policy does not yet align with industrial reality

Poland’s current hydrogen demand is concentrated in heavy industry, notably in refineries and chemicals production. Other heavy industrial sectors such as primary steel production will likely also need clean hydrogen to decarbonise energy-intensive operations.

Under EU REDIII mandates, Poland is expected to consume at least 180 kilotonnes (kt) of renewable hydrogen per year in its industry by 2030, five times the current renewable hydrogen production of the entire EU. The unprecedented rate of deployment needed in just four years is set against a backdrop of national conditions ill-fitted to producing the volumes of hydrogen needed at a competitive price. The country’s carbon-intensive electricity grid and limited, expensive renewable energy makes it too costly and intermittent to supply to industry at scale.

This was underscored in the roundtable discussions, as national industry representatives stressed the risk of losing their competitive edge if forced to switch to renewable hydrogen at its current price and availability.

“We [Poland] need more flexibility on decarbonisation pathways to maintain competitiveness while meeting climate goals.”

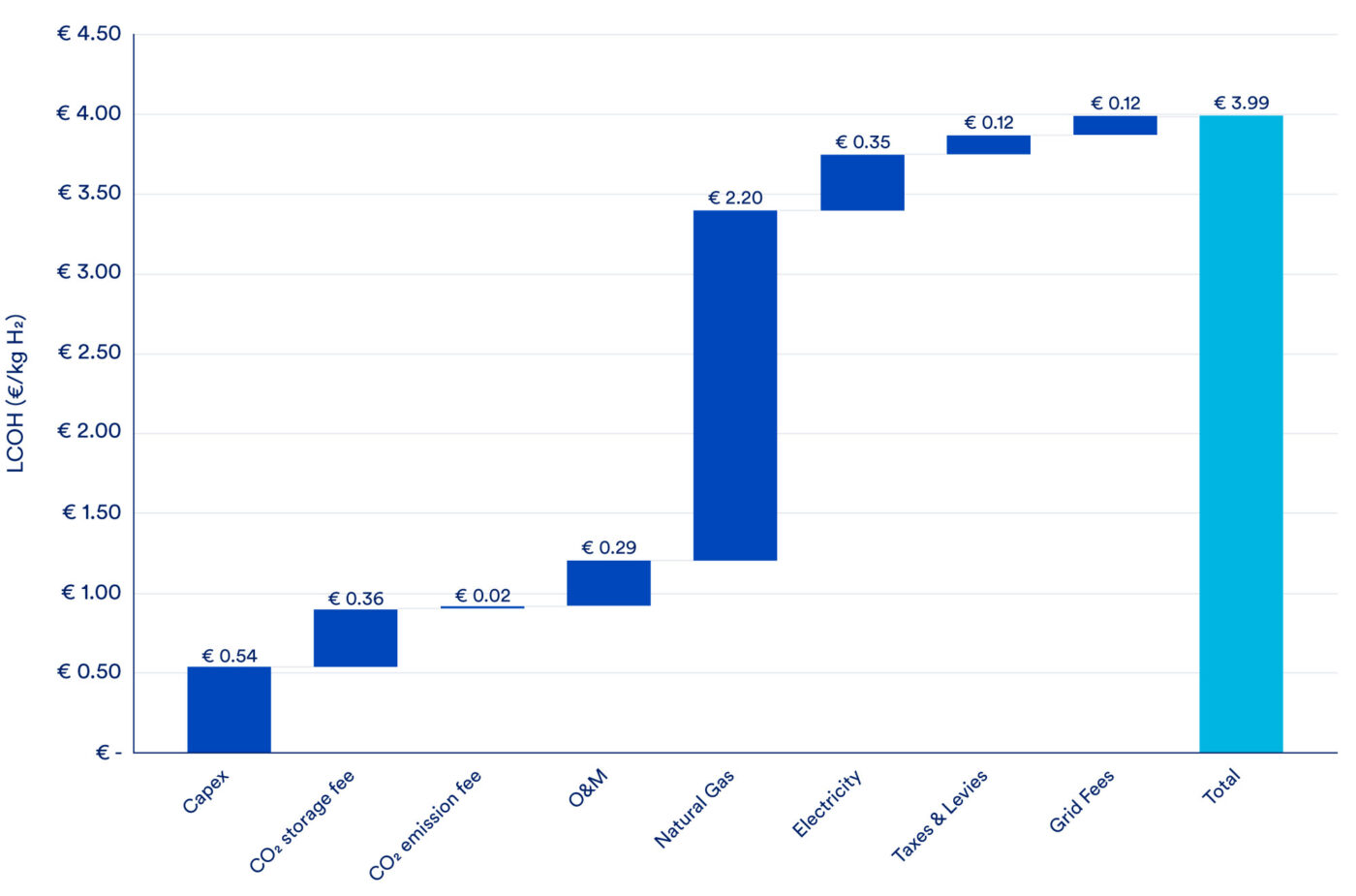

CATF’s modelling underscores that whilst renewable hydrogen will be vital in the long term for Poland’s decarbonisation, it is currently too expensive and scarce for Poland’s heavy industry needs today. Instead, low-carbon hydrogen with carbon capture and storage (CCS) offers a reliable, lower-cost alternative for industry that can start cutting emissions now and align better with broader industrial decarbonisation efforts. Such efforts will also buy time to decarbonise Poland’s carbon-intensive grid by using available renewable assets to achieve deeper emissions cuts.

Figure 1: Levelized Cost of Low-Carbon Hydrogen Production in Poland

Stakeholders broadly agreed that low-carbon hydrogen and CCS will be indispensable in the transition phase. The success of hydrogen deployment in Poland will depend on integrated infrastructure, consistent funding, public administration capacity and policy flexibility.

Industrial clusters are the launchpad

By prioritising low-carbon hydrogen deployment in the near term, Poland can associate a revised clean hydrogen strategy much more closely with its broader industrial decarbonisation policy planning.

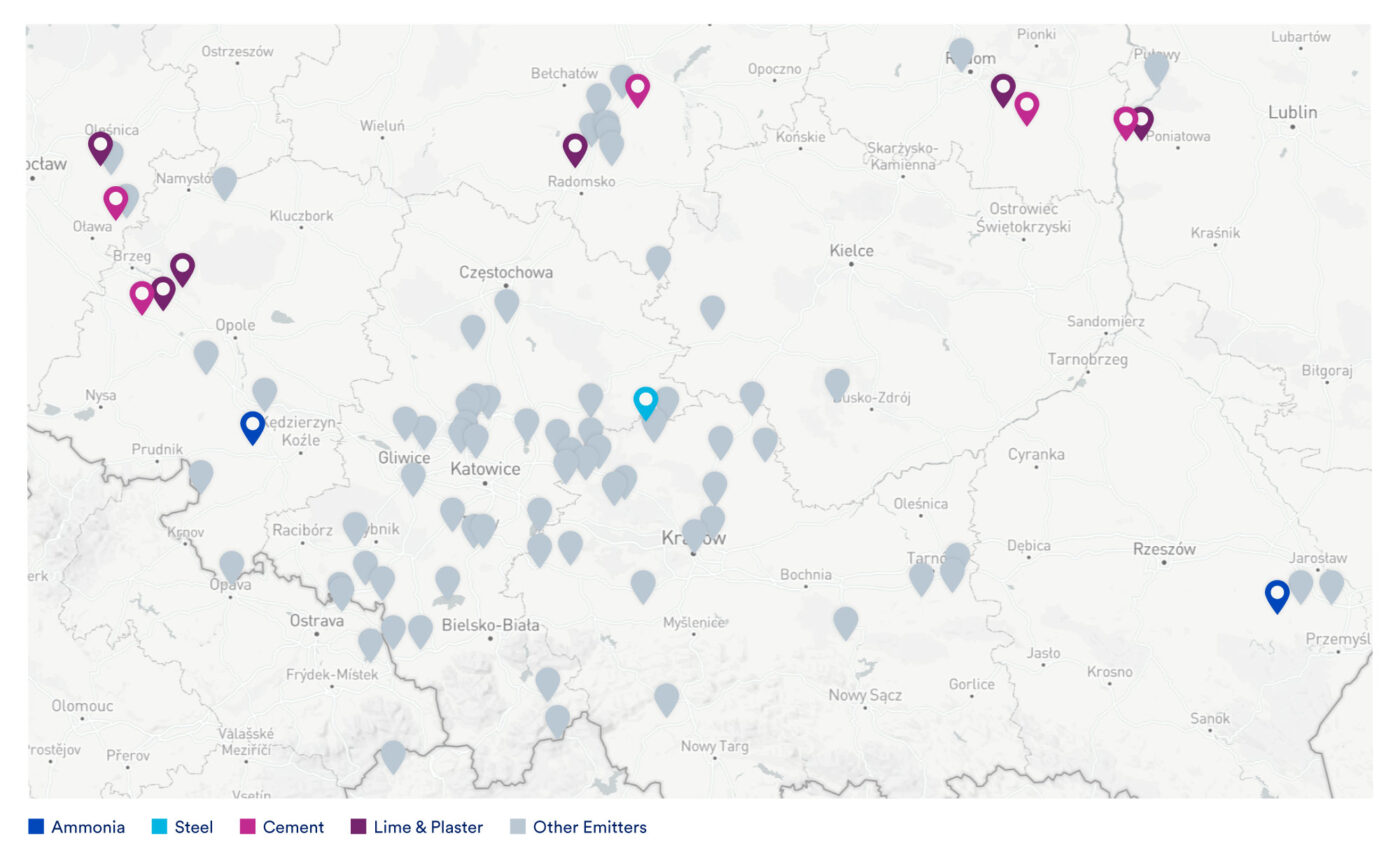

Industrial clusters — where several CO2 emitters are located in close proximity – can lead the way. Low-carbon hydrogen can act as a key emissions source within CO2 transport and storage infrastructure planning and contribute towards meeting broader carbon management targets. Coordinating clean hydrogen and CCS deployment in these regions will cut costs and deliver results faster.

Figure 2: Silesia-Opole Industrial Cluster in Southern Poland

Stronger coordination between national hydrogen and carbon management strategies can help identify priority sites and streamline the necessary infrastructure and funding. As highlighted frequently across the discussions, Poland has limited domestic funds to dedicate to hydrogen upscaling and what funds are available through the EU prioritise hydrogen production pathways that do not yet work in the Polish context. Approaching decarbonisation funding through an overall emissions reduction lens, rather than by technology, will create a more level playing field between different decarbonisation options designed around industrial cluster needs.

“… the focus should be on reducing greenhouse gas emissions not on a specific decarbonisation pathway, don’t focus on colour but outcome.”

Focus on emissions reductions, not colours

Despite the promising opportunity of low-carbon hydrogen with CCS in Europe, current EU hydrogen rules only count renewables-based electrolytic hydrogen – or ‘green’ hydrogen – as eligible for meeting hydrogen-based targets, which risks leaving countries like Poland behind.

Balancing these climate obligations with industrial competitiveness is a challenge, given that Poland’s heavy industries remain central to its economy and employment. Stakeholders echoed that total CO2 emissions reductions should be the priority for hydrogen deployment, rather than a prescriptive production pathway. Such an approach would enable companies to deploy the most cost-effective emission reduction methods based on local conditions and enable Member States like Poland to meet its energy and climate mandates.

Europe cannot truly decarbonise without action in Poland. Therefore, targets must correspond – rather than contradict – with real emissions reductions needs. Yet, participants voiced that this is currently not the case and the existing hydrogen regulatory landscape risks increasing the cost burden on industry, slowing deployment of clean hydrogen and failing to meet the required levels of emissions reductions. This coupled with institutional capacity gaps at the ministerial level emphasised the need for:

- Revision of EU regulations to create a more technologically neutral playing field for hydrogen, making it easier for Member States to execute at the national level around national conditions.

- Strengthening national-level capacities thorough better institutional coordination and clear accountability mechanisms, adequate staffing, and established, mandatory review processes.

An opportunity for course correction

The Polish Hydrogen Strategy, adopted in 2021, focused on developing new hydrogen markets and demand, particularly where it was not yet being used. Experts agreed that Poland’s hydrogen strategy must reflect national conditions, industrial priorities, and physical constraints. Simply mirroring EU targets at the national level without considering adaptation to the local context leads to inefficiency and policy confusion.

A clear, evidence-based Strategy should define priority use cases, timelines, and responsible institutions, situating the deployment of clean hydrogen within wider industrial decarbonisation strategies.

Key takeaways:

- Integrate hydrogen into industrial decarbonisation plans: The Polish government must take advantage of the forthcoming Hydrogen Strategy update to incorporate hydrogen efforts into its national industrial decarbonisation policy and plans. It should also ensure that hydrogen targets are aligned across policies, including PEP2040 and the updated National Energy and Climate Plan (NECP).

- Enable flexibility and technology neutrality: Member States like Poland need flexibility to meet hydrogen, carbon management, and industrial decarbonisation mandates through a technology-neutral approach. The EU must enable this by revising policies now to allow timely planning and deployment.

- Balance ambition with economic realism: Policy design must reconcile climate objectives with industry needs, fostering industrial clusters, and maintaining flexibility in policy implementation.

Review the presentations from Clean Air Task Force and Reform Institute.