Strengthening Lead Markets in the Industrial Accelerator Act

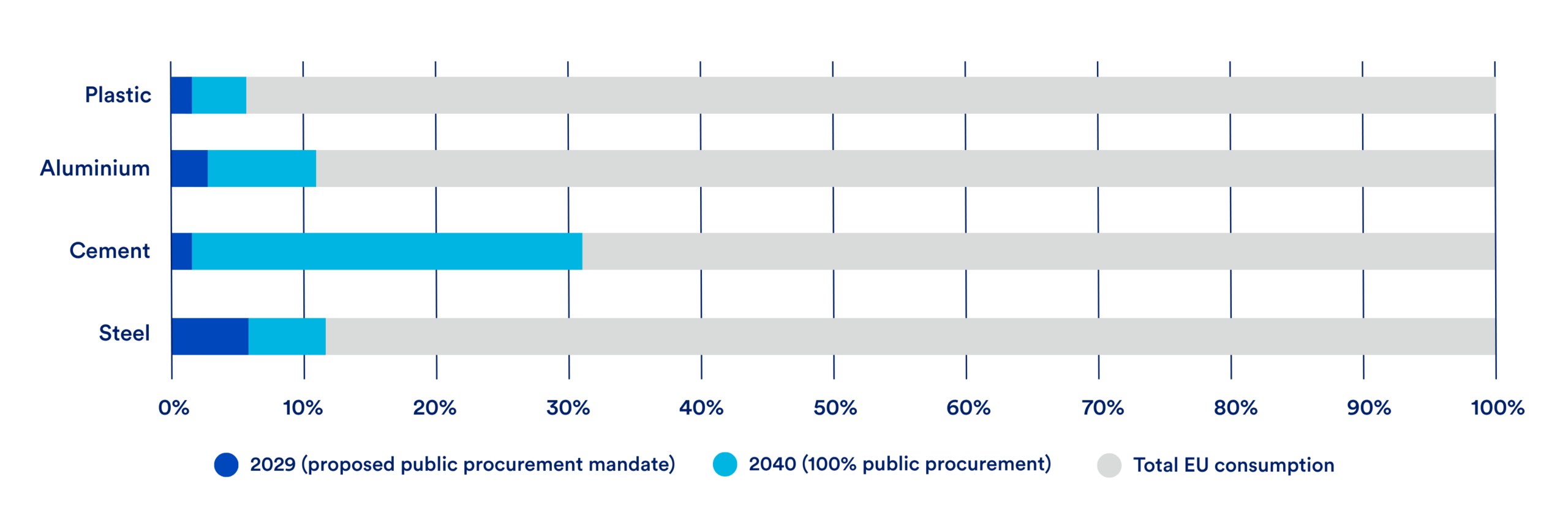

The Industrial Accelerator Act (IAA) is a key opportunity to ensure the EU can maintain a competitive manufacturing industry while also meeting climate goals. The proposed regulation rightly recognises that strong market demand for low-carbon materials will be essential for creating an investable business case for industrial decarbonisation projects. While demand must also be cultivated in the private sector, public procurement has a key role to play in developing lead markets for low carbon products, as it accounts for 14% of GDP in 20191 and an estimated 31% of cement and 11% of steel consumption.2

The current proposal is a positive step in the right direction. However, it would not fully leverage lead markets and would be insufficient to create meaningful demand for low-carbon materials. The Parliament and Council now have the opportunity to strengthen the IAA and ensure it is compatible with the EU’s pathway to climate neutrality and to support competitive and decarbonised industries in the EU.

Key recommendations

Steel

- Increase the 2029 public procurement mandate for low carbon steel to 50% in 2029.

- Adopt a fallback definition of low carbon, set at the level achievable by leading decarbonisation technologies, to ensure the procurement obligations aren’t softened by a weak low carbon threshold.

- Implement a cap on the maximum permissible carbon intensity of steel procured by public entities

Concrete and mortar

- Increase the 2029 public procurement mandate for low-carbon concrete and mortar to 10% in 2029.

- Adopt a fallback low-carbon definition based on the top two tiers of the GCCA concrete standard.

- Implement a cap on the maximum permissible carbon intensity of concrete procured by public entities

Tighten coverage of the public procurement obligations by narrowing exemptions

- Clarify in Article 11(3)(c) that the 25% “disproportionate costs” threshold is assessed against total contract value, not against the incremental cost of low-carbon material inputs.

- Amend Article 12 to raise the EII support-scheme floor from 45% to 75%.

Scope and ambition

- Progressively increase public procurement mandates to reach 100% by 2040

- Expand the scope of public procurement requirements and support schemes:

- For plastics used in construction, include an obligation of 30% by 2029 rising to 100% by 2040.

- Adopt by 2029 a proposal to extend demand side mandates beyond those currently covered under the IAA , especially for chemicals.

- Update Article 16 to replace “sustainable carbon sources” with “low carbon production”.

Capitalise on the potential from the private sector

- Expand demand side obligations into the private sector:

- for construction projects over 1000 m2 of useable floor area by 2032 across low carbon steel, concrete, aluminium and plastics

- For commercial fleet purchases in the automotive sector by 2032 for low-carbon steel and aluminium.

- Adopt a proposal by 2029 to expand the obligation to the fertilisers sector

1. Making the existing requirement ambitious and realistic

1.1. Steel

The IAA’s proposed public procurement quota for low-carbon steel is based on an assessment that new low-carbon steel projects in the EU could deliver an annual capacity of 29.7 Mt by 2030, which would meet 22% of forecasted EU demand in 2030 (134 Mt). This proportion was then rounded up to obtain the quota of 25%. However, this analysis failed to account for the fact that public procurement represents just a small portion of EU steel demand. Therefore, if public entities buy 25% low-carbon steel, that creates demand for only about 3.9 million tonnes of low-carbon steel, which falls far short of the already-planned production capacity and won’t incentivise further low-carbon steel capacity.

The EU steel sector would be better supported through a higher initial public procurement mandate of 50% in 2029: this would equate to a demand of 7.9 Mt, which is readily achievable by the planned new capacity and the decarbonisation options available to the existing fleet.

A. EU low carbon steel production capacity

In 2024, EU demand for steel was met 20% by imports, with EU domestic production supplying the balance: 44% primary steel (made from raw materials) and 36% secondary steel (made from recycled scrap).3 Secondary production has a significantly lower environmental footprint and increasing the share of steel supplied via this pathway can drive significant emission reductions.

Figure 1: EU supply of steel

The IAA Impact Assessment identifies 29.7 Mt/year of ‘committed’ and under construction capacity in the Bloomberg NEF database of decarbonised steel projects, which could be operational by 2029, CATF analysis of this database – shown in Annex 1 – finds 10.15 Mt of new low carbon iron production capacity through the direct reduced iron (DRI) pathway, which could yield up to 12.2 Mt of primary steel. Of this, 8.7 Mt (10.4 Mt primary steel) is currently under construction and likely on track to deliver by 2029; however, only one of these projects is committed to using 100% hydrogen from commissioning, with the others planning a gradual shift from natural gas.

The project database also includes 6.25 Mt/year of additional electric arc furnace (EAF) production capacity which explicitly targets low-carbon primary steel production but are not directly linked to low carbon iron production sites in the EU. These facilities will need to source ore-based metallics with a low carbon intensity and have plans to source iron from abroad or unspecified locations. Only two of these facilities are currently under construction, and there remains some uncertainty over their ability to source green iron inputs.

In total this equates to a likely operational new low carbon production capacity of 13.5 Mt/year based on CATF analysis of the BloombergNEF database, conservatively considering only plants already under construction. Additionally, the 29.7 Mt figure from the commissions analysis likely double counts production from integrated DRI and EAF plants with both iron and steel numbers – included separately in the source database. Beyond this there is a significant pipeline of additional new projects which could progress past FID if demand for their products were realised.

There is additionally an existing fleet of EAF facilities – producing predominantly secondary steel from recycled scrap – with an estimated capacity of approximately 88 Mt4, which can achieve significant emission reductions through using renewable electricity and biogenic carbon sources. There are already two EU EAF facilities certified to produce steel products that meet LESS class A – the second highest band possible – at the Georgsmarienhutte EAF plant operated by GMH Gruppe5 and production from Peiner Trager GmbH.6

If taken together this equates to almost 100 Mt of potential low carbon steel production capacity in the EU which could be achieved through new build primary steel capacity and the procurement of renewable electricity in secondary steel plants. This far exceeds the potential demand from even the most ambitious of public procurement policies.

B. A low-carbon steel definition

With the process to develop low-carbon definitions under the ESPR and CPR still underway, defining low-carbon steel under these regulations creates a risk that the IAA procurement mandates could be drastically weakened if a less ambitious definition of low carbon is adopted. For example, the classes of environmental performance proposed by the JRC in its April report for five representative iron and steel products under ESPR would consider almost all current EU steel production as “low carbon”, a definition which would be highly detrimental to the industries decarbonisation efforts and result in the procurement mandates proposed within the IAA being entirely meaningless.

The IAA should therefore establish an interim definition of low carbon for steel, by reference to an existing internationally recognised standard providing a robust and credible low carbon threshold set at the level achievable by the best leading decarbonisation technologies. Upon entry into force of the relevant ESPR or CPR delegated act, its definition shall replace the interim definition, provided that it is no less stringent than the interim.

The Impact Assessment advised the use of a sliding scale approach to defining low carbon – as shown in Figure 2 – following the approach widely supported by industry and currently used in existing frameworks such as the IEA proposal and the Low Emissions Steel Standard (LESS). Adopting such an approach as an interim definition – for example, LESS with the top two bands defined as low carbon – would unlock the investment needed in leading low carbon production projects.

C. Setting the target and capping carbon intensity

Set against the expected capacity of new low-carbon primary and secondary steel and the decarbonisation potential of the existing secondary fleet, the IAA’s proposed 25% requirement will fall short of the demand signal the market needs. The mandate should be raised to 50% in 2029, creating demand for around 7.9 Mt of low-carbon steel – achievable under a definition equivalent to the top two LESS classes. Eurofer’s support for a 50% procurement obligation indicates industry will accept a target at this level.7 The target should rise further in later years as EU low-carbon capacity grows – Section 3.1 details a suitable growth rate.

The IAA should also place a cap on the CO₂ intensity of steel used in publicly procured steel-based products. A share-based target governs only the low-carbon portion; the remainder stays eligible however carbon-intensive it is. A cap closes that gap by screening out the highest-emitting steel on the EU market – notably coal-based DRI and output from the most carbon-intensive sites.

1.2. Concrete, mortar and cement

The EU produces just over 160 Mt of cement and consumes around 150 Mt of cement annually, of which over half is delivered as ‘ready-mix’ concrete to be used at construction sites.8 Owing to the highly emissions-intensive production of clinker – the main constituent of cement – the sector is associated with 120 million tonnes of CO2 emissions distributed over 200 facilities (around 4% of total EU emissions).9

The proposed IAA quota would require 5% of publicly procured concrete and mortar to be low carbon by 2029, including the clinker and cement used to produce them. Given that public procurement is estimated to account for 31% of cement demand,10 this quota would amount to around 2.3 Mt of annual cement production capacity.

A. EU low-carbon cement production capacity

The carbon intensity of cement can be reduced both by developing less carbon-intensive production pathways of clinker and reducing the clinker content of the cement blend.

Approaches to reducing the energy-related emissions from cement clinker kilns include improving energy efficiency, switching to lower-carbon fuels, and electrification. EU cement plants currently use around 50% alternative fuels (30% waste-derived and 20% biomass) and the sector targets 95% by 2050.13 Several technologies to electrify kiln heating are also being trialled in the EU. However, as around two thirds of kiln emissions are process emissions, associated with CO2 from limestone calcination, and cannot be avoided by electrification or fuel switching, CCS is the only route to reaching very low levels of embodied carbon for clinker. CCS is a relatively high-cost process, estimated to increase the cost of cement by at least 90%.11

Reducing demand for carbon-intensive clinker is therefore an important, lower-cost strategy for decarbonising cement and concrete products, which can complement strategies to decarbonise clinker. Established clinker substitutes based on waste materials such as fly ash and blast furnace slag are now being supplemented by new facilities for the dedicated production of calcined clay – a clinker substitute which is around a quarter as carbon intensive and the key ingredient in a blend known as limestone calcined clay cement (LCCC or LC3). However, there are regulatory and technical limits on how much clinker substitute can be used. The average clinker content of cement in the EU is around 70%; industry association Cement Europe has targeted a reduction to 60% in its net-zero roadmap12, while other projections indicate a ratio of 40% could be achievable.13Some emerging low-carbon cements offer very low or zero clinker content, including Ecocem’s ACT technology (typically 15-25% clinker) and Hoffmann Green Cement’s clinker-free binders. These products use proprietary blends of limestone, calcined clays, blast furnace slag and other components, and target combined output of around 3 Mtpa by 2030 (Table A.2, Annex 1). Some commonly used clinker substitutes, such as fly ash and blast furnace slag, are expected to become less available as the EU phases out coal power and conventional steel production, increasing the importance of materials with greater potential to scale, such as calcined clay.14

The proposed IAA quota of 5% is informed by an analysis of the project pipeline for CCS-equipped cement plants, as well as the projected production of calcined clay and other unspecified clinker substitutes.

There are only two examples globally of CCS operating at large scale on commercial cement plant, including the Brevik cement plant in Norway (0.4 MtCO2/year captured, amounting to 50% of total emissions).15 A larger facility is under construction at Padeswood cement in the UK, which would capture 95% of the cement kiln emissions (0.8 MtCO2/year).16 There are also over 30 known proposals in the EU to deploy CCS at cement plants, at varying stages of development.17 Of these initiatives, 17 large-scale projects are supported by the Innovation Fund18 and four in France and Denmark also benefit from national funding support (Annex 1).19

Based on the announced timelines and estimated production volumes, total cement production from these funded CCS projects could reach over 15 Mt annually by 2029 and 28 Mt by 2032 (Annex 1).20 However, many projects are behind schedule due to remaining funding gaps and delayed access to CO2 storage. A significant increase in CO2 storage capacity in the EU should be realised by 2030, due to the Net-zero Industry Act mandate on oil and gas producers to provide 50 Mt of annual CO2 injection capacity.21 Realistically, very little CCS-enabled cement production is likely to be operational in the EU by 2029, beyond non-EU production from Brevik (0.5 Mtpa of low-carbon cement22) and Padeswood (~0.82 Mtpa of low-carbon clinker23). However, the project pipeline suggests production could scale up rapidly in the early 2030s.

B. Existing labels for low-carbon cement and concrete

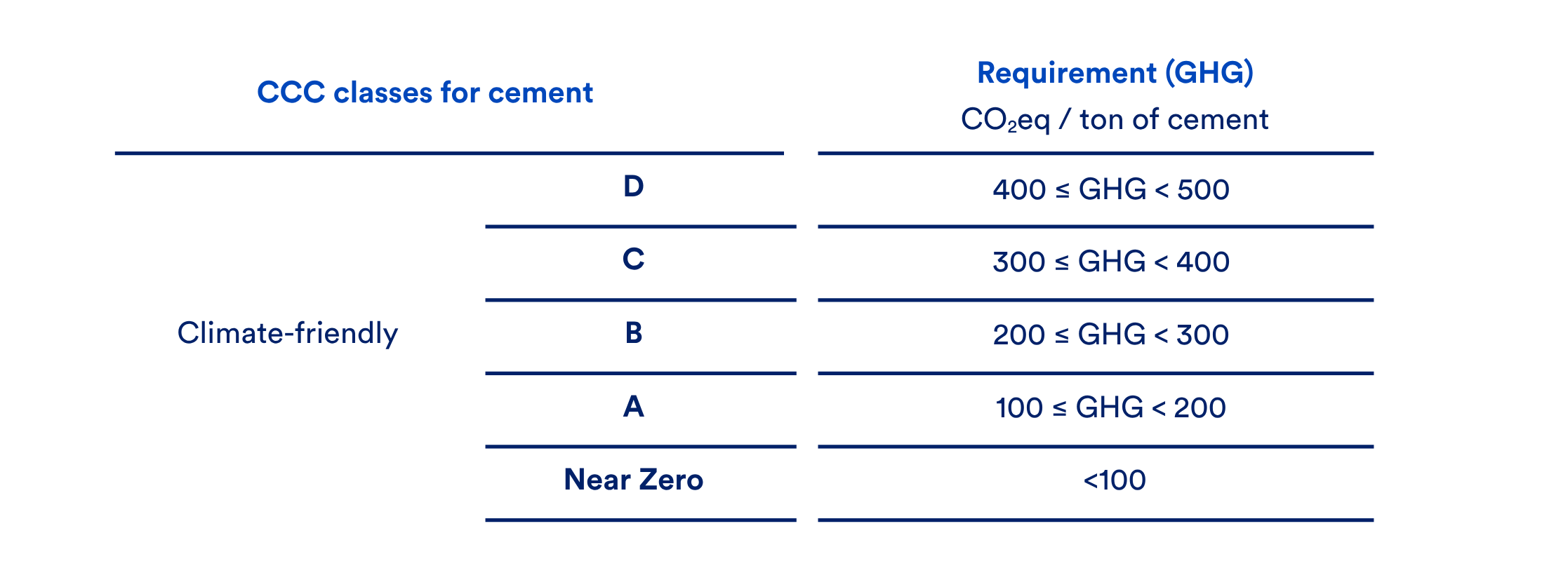

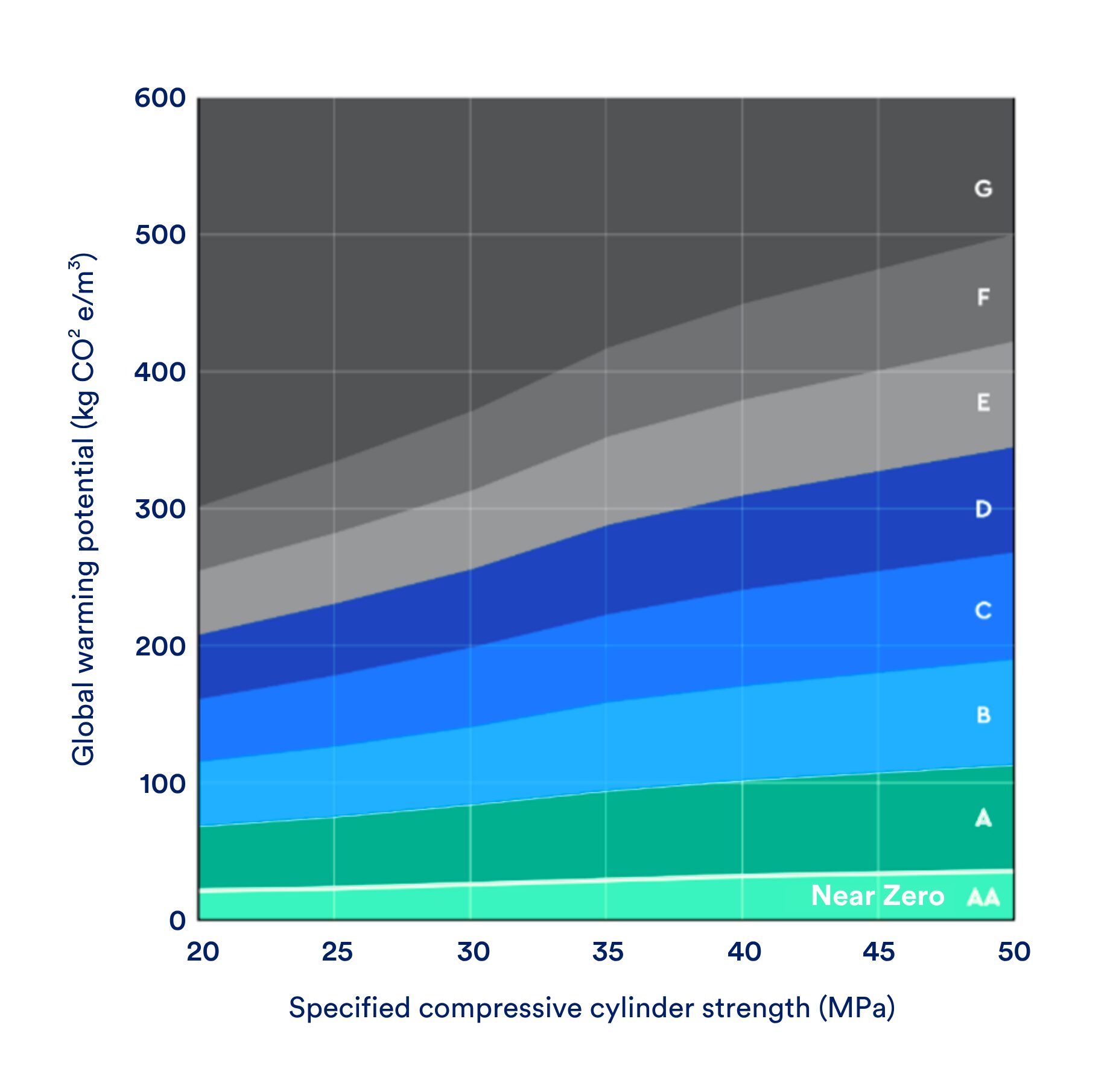

There are several voluntary labelling systems to indicate the carbon intensity of cement, which can usefully inform the definition of ‘low carbon’ applied in EU legislation. In 2022, the IEA put forward a banded rating system, with a sliding scale approach based on clinker content, which has also been adopted by the Industrial Deep Decarbonisation Initiative.24 Modification of this by Germany’s VDZ has applied the bands, without the sliding scale, based on the thresholds for a clinker content of 70%.25 The Global Cement and Concrete Association have adapted the bands for concrete at various strength grades (Figure 3).26 Use of a concrete standard allows for a wider range of pathways to reach a low-carbon product, including reducing cement content.27

Figure 2. VDZ emissions intensity ranges for near zero and low emission cement production.26

Figure 3: GCCA Global ratings for concrete.28

Most cement sold in Europe today achieves only moderate emissions reductions through limited clinker substitution. Nearly 50% of cement sold on the EU market is ‘CEM II’(a blend with at least 6% clinker substitution, between categories C to E of the IEA cement scale). More ambitious lower-carbon cement types such as CEM III (containing at least 36% blast furnace slag) remain less than 10% of the market29, but can achieve as low as band B. More novel cement blends such as Ecocem ACT and Hoffmann Green binders report carbon intensities within or close to band A.30

Major producers including Holcim and Heidelberg Materials have committed to reducing the carbon intensity of their products by 2030, but their targets still fall short of near-zero cement production, with Holcim targeting 420 kgCO2 per tonne of material, and Heidelberg targeting 400 kg per tonne (the top of band C of the VDZ standard).31

C. Recommendations for a low-carbon cement: concrete definition and future targets

The impact of the 5% procurement target proposed by the IAA depends significantly on how ‘low carbon’ is defined. For the target to support the long-term transition of the cement sector to net zero, it is vital for this demand signal to support both low-clinker blends and investment in CCS-equipped facilities, many of which are currently struggling to advance to a final investment decision under existing incentives alone. If the definition is too weak, the target may simply encourage limited clinker substitution rather than the near-zero technologies needed for full decarbonisation.

We therefore propose that low-carbon be strictly defined as corresponding to the Near-zero and A bands of the IEA and VDZ cement scales and the AA and A bands of the GCCA ratings for concrete, or equivalent.

Based on this definition, we would propose increasing the procurement target to 10% in 2029, which is equivalent to 4.6 Mtpa of cement (assuming an average cement content in concrete). This demand could be met by the current project pipeline, if CCS-decarbonised clinker from the first European projects is used in combination with novel low- and zero-clinker cements. The revision of the EN cement and concrete standards32 will facilitate market access for these new, low-clinker cement blends and alternative binders, helping expand the supply of low-carbon concrete.

Most importantly, a relatively steep increase in the target for future years is necessary to reflect the expected scale-up of low-carbon production in the early 2030s, particularly as CO2 storage becomes more broadly available. We propose an increase to 30% of publicly procured concrete and mortar by 2032. However, lowest-cost decarbonisation of the construction sector will also require rationalisation and reduction of the use of clinker, cement, and concrete to deliver the same outcomes in the built environment.33

The IAA should also implement an additional cap on the acceptable CO2 intensity of publicly procured concrete, which would primarily promote the uptake of lower-clinker cement blends. A precedent for this approach is set by Ireland’s policy to require public construction projects to use cement grades with a minimum of 30% clinker substitution.34 Greater uptake of lower-carbon cement and concrete products should also be incentivised by overarching limits on the embodied carbon of buildings, which can be established under the EPBD.

2. Tighten coverage of the public procurement obligations by narrowing exemptions

2.1. Apply cost exemptions at the project level

Article 11 (3) (c) allows the public procurement obligations for low carbon materials to be avoided where their application would result in “disproportionate costs,” with cost differences exceeding 25% presumed to meet that threshold. It should be made explicit that this provision applies to total contract value, not to the change in cost of the underlying energy-intensive materials.

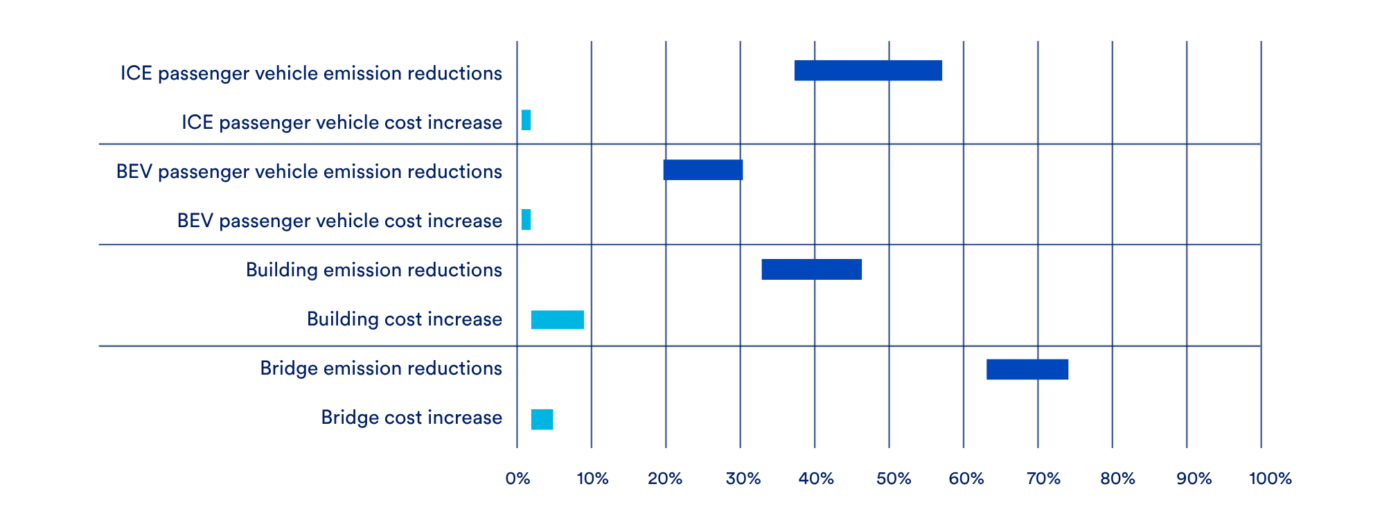

Across both construction and the automotive industry, the additional cost of the low-carbon materials is minor compared to the overall project costs, while offering significant overall emission reductions. In the construction sector, steel and cement can account for 82% of total embodied emissions of infrastructure projects such as bridges, while only accounting for 10% of project costs (Figure 4).35 Replacing the steel and concrete used with low-carbon versions can therefore dramatically cut emissions by 63%-74% while only increasing costs by 2-5%.

Across the building sector, emissions associated with concrete, steel and aluminium account for around 55% of the embodied emissions associated with construction36, lower than in infrastructure due to the more diverse range of materials used. Targeting mandates for the use of low-carbon materials across these three energy intensive materials can reduce building emissions from the construction phase by 33%-46% while cost impacts range between 2-9%.37

Similarly, using low-carbon steel and aluminium in an internal combustion engine passenger vehicle would reduce the cradle to gate emissions by 37-57%; the same replacement in a passenger electric vehicle would see cradle to gate emissions reduction of 20-30%, with the decrease being due to the carbon footprint of the battery. In both cases, the impacts on costs would be around 1-2%.

Figure 4: Cost impact and emissions reductions from low carbon materials across automotive and construction38 39

Article 11(3)(c) should be amended to clarify that the cost differential is assessed against total contract value, not the cost of the underlying low-carbon material input. Article 11(3)(b) already provides for exemption where supply is genuinely unavailable.

2.2. Require 75% of eligible supported expenditure to meet the procurement obligations

Article 12(1) requires Member States to apply the low-carbon requirements to public support schemes representing at least 45% of the total national budget allocated to schemes covered by Part II of Annex II. A majority of the relevant scheme budget – up to 55% – can therefore be placed outside the scope of the obligation, substantially weakening the demand signal across the support-scheme channel.

The threshold should be raised to 75%. This would ensure substantive coverage of national support-scheme spending while preserving Member State discretion to exempt schemes where exclusion is objectively justified – for example, schemes with award values too small to make compliance proportionate.

3. Expand the scope for public requirements

3.1. Increase Green Public Procurement Mandates Over Time

Meeting the EU’s 2050 climate neutrality goals ultimately requires the market for low-carbon industrial products to scale to meet total demand. The IAA is central to making this happen, but only if the lead market it creates grows continuously over time. A fixed market share is insufficient to drive the scale of low-carbon uptake the IAA is aiming to achieve – procurement obligations need to ramp to full coverage of public demand rather than settle at a static level, before private sector obligations layer in to carry the transition into the mainstream market.

The IAA can deliver this by progressively raising public procurement obligations from currently proposed levels to 100% by 2040. This level of ambition is critical given the EU’s commitment to 90% emissions reductions by 2040, which cannot be met without meaningful progress towards reducing the carbon intensity of energy-intensive materials consumed in the EU. It is also achievable: a clear, long-term trajectory of this kind gives industry the demand certainty needed to unlock investment in low-carbon production across steel, aluminium, concrete and plastics.

Figure 5: Lead market share from proposed low carbon lead market obligations – assuming stable demand to 204540

By progressively raising the public procurement requirement to 100% by 2040, the EU can expand demand from the initial, limited quantities in 2029 as the EU’s production capacity scales. This could grow demand for low carbon materials to cover around 11-12% of the total EU demand for steel and aluminium and 31% of cement in 2040, equating to approximately 47 Mt of low carbon cement demand annually and 16 Mt of low carbon steel.

3.2. Plastics in construction

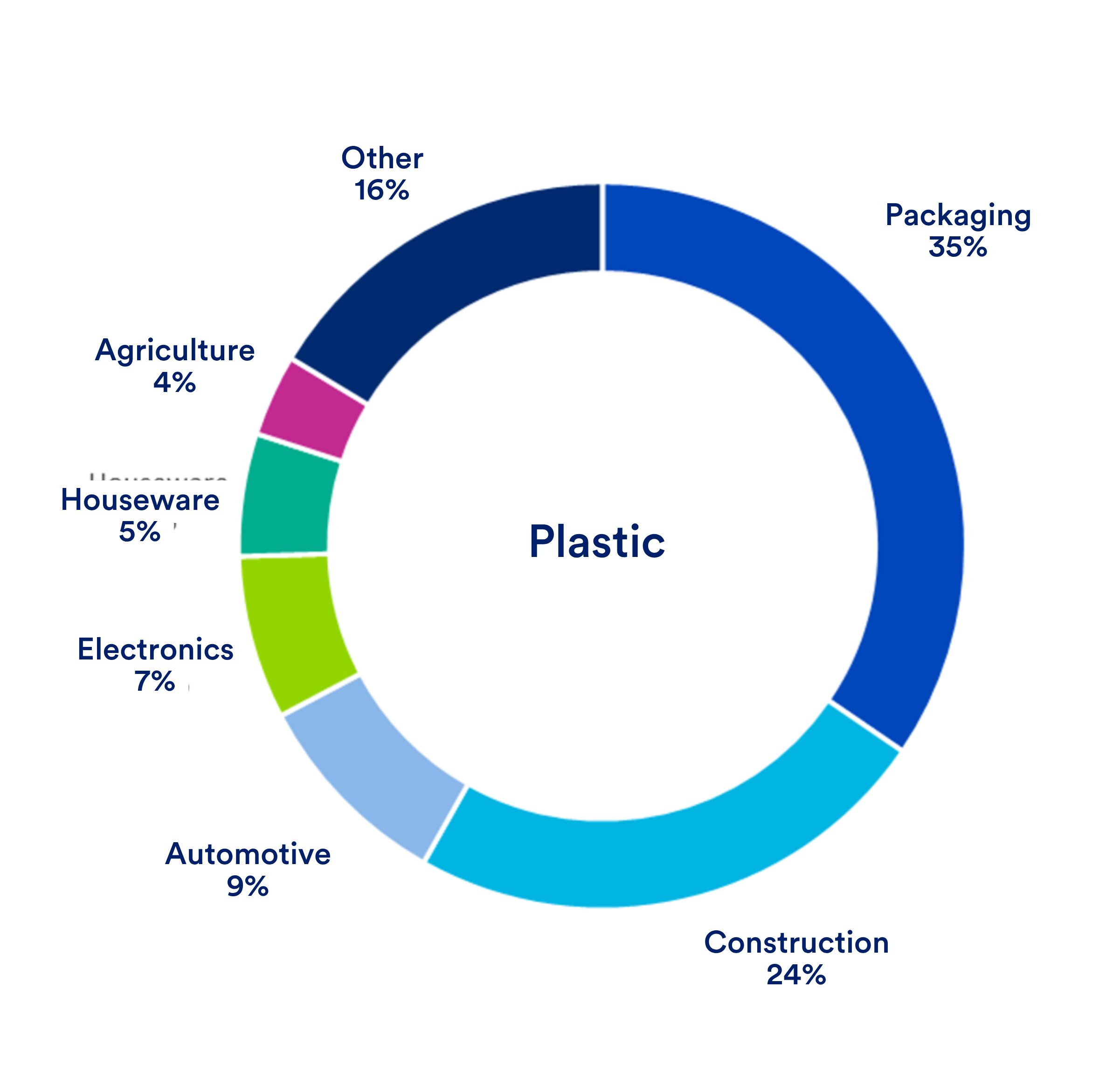

The EU consumed 56.2 Mt of plastics in 2024 of which almost all (54.6 Mt) was produced in the EU.41 This consumption accounted for an estimated 24 MtCO2e42 in greenhouse gas emissions and was from a range of end-use sectors (Figure 6). The construction sector accounted for 24% of plastic demand concentrated across just three applications – pipes, insulation and window/door frames – which together accounted for 60% of demand from the construction sector,43 equivalent to 8 Mtpa of plastic.

Figure 6: Plastics demand by downstream sector44

Given that public procurement accounts for around 40% of EU construction, procurement of plastics in these three product categories represents an ideal starting point for mandating uptake of low-carbon plastics. An initial public procurement and support scheme obligation of 30% should be targeted, creating an estimated demand of 1.1-1.7 Mtpa of low carbon plastic, which could be further developed with expansion into the private construction sector and other downstream sectors over time.

Current EU demand is mostly met through fossil fuel-derived plastics, with lower carbon options such as recycled and bio-based materials supplying 20% of production capacity. This is mostly in the form of mechanical recycling which supplied 10.6 Mt of lower carbon plastic in 2024. Meeting the 2029 demand from the proposed procurement mandate would be equivalent to just 10-16% of current low-carbon plastics production capacity. The implementation of Digital Product Passports (DPP) under the CPR, expected for some plastic construction products by 2028 and 2029, will enable tracing of the material inputs and readily enable construction entities to ensure procured materials were compliant.

The inclusion of plastics within the lead market provisions is supported by the industry, with both Plastics Europe45 and the wider chemicals association Cefic46 calling for stronger action.

3.3. Broaden Article 16 to cover all low carbon production pathways

Extending demand-side measures to chemicals under a delegated act could be a valuable addition to the IAA. As drafted, Article 16 limits this to materials derived from sustainable carbon sources defined in Article 3(16) as “biomass that complies with the sustainability criteria laid down in Article 29 of Directive (EU) 2018/2001, waste and carbon from capturing carbon dioxide emissions”

This prioritises input feedstock rather than emissions reductions, excluding a number of low-carbon chemicals production pathways including electrification of processes, use of low-carbon hydrogen and deployment of CCS. These are all important decarbonisation approaches which, alongside recycling and increased use of circular feedstocks – such as sustainable carbon sources – are identified as decarbonisation pathways for the chemicals sector in the IAA Impact Assessment. The narrow scope of the proposed Delegated Act therefore risks driving deployment of decarbonisation approaches in a non-technology-agnostic manner.

Article 16 should therefore be reworded to enable a range of decarbonisation options replacing “sustainable carbon sources” with “low carbon production”.

4. Expanding procurement mandates for low-carbon materials into the private sector

4.1. Private construction projects over 1000 m2

While public procurement and public support schemes represent an important initial lead market for low-carbon products, the bulk of demand originates in the private sector, which represents 89% of steel demand and 69% of cement. The IAA should progressively introduce private sector mandates starting from 2032, to add the scale public procurement alone cannot provide and allow demand-side mechanisms to play a role in sectors where public entities are not major players

The construction sector is a major user of steel, cement, aluminium and plastic and makes an ideal market to extend the already proposed public sector mandates into the private sector. Extending mandatory low-carbon material requirements to private construction projects exceeding 1000 m² of useful floor area would substantially increase the scale of the lead market, and reflects the threshold used for mandatory global warming potential reporting in the Energy Performance of Buildings Directive (EPBD).47 At this threshold, around 50% of EU buildings would be covered – commercial, industrial, logistics and multi-unit residential construction – without placing an unnecessary administrative burden on smaller projects.48

It should be noted that the IAA’s public procurement obligations apply only to works contracts above €5.4 million, which is the threshold set by the Public Procurement Directive (PPD).47 The proposed private sector threshold of 1000 m2 useful floor area will not align directly with this cut-off. The total cost for private projects at 1000 m2 is highly variable, with construction costs varying significantly between regions and building type; a typical Western European CBD office with this floor area could range from €3.2 to €4.3 million.48 This threshold therefore represents a pragmatic approach, matching the initial threshold used in the EPBD rather than targeting exact equivalency with the public procurement obligations.

A requirement for private construction above 1000 m2 should come into force by 2032, with procurement mandates for low carbon-materials starting from 5% across steel, cement, aluminium and plastics, and growing to 100% by 2045.

4.2. Automotive sector

The majority of steel used in the construction sector (typically over 75%) are ‘long’ products, such as rebar, beams, and rails, whose production is dominated by secondary steel from electric arc furnaces. Creating a lead market for the – much harder-to-abate – primary steel production capacity in the EU will require measures which reach beyond public procurement. The automotive sector is the EU’s next largest steel-consuming sector after construction (20% of total demand) and predominantly uses ‘flat’ steel products which have a greater reliance on carbon-intensive primary production pathways.51

Given the cost increase of using low-carbon steel would add less than 2% to the final cost of a vehicle, the automotive sector is a prime candidate for a lead market for low-carbon, primary steel, which can support the business case for the hydrogen-based DRI projects now being progressed in the EU. However, the currently proposed coverage of the IAA is unlikely to make a significant impact in the sector. The Impact Assessment estimates that public procurement of passenger vehicles accounts for 0.5-3.5% of demand, which would – at most – cover ~0.9 Mt of flat steel production.

Further coverage may be associated with publicly supported vehicle purchase schemes with the impact assessment estimating a 70.1% market coverage under public support schemes. However, this assumes all corporate purchases – 60% of sales – would fall under publicly supported schemes. While corporate vehicle purchases do receive tax benefits, it is unclear how general corporate vehicle tax treatment (VAT reduction, benefit in kind tax, depreciation write-offs) would fall within the scope of public support schemes that the IAA can operationalise with low-carbon material conditions. The origin of the 10.1% of private car sales assumed to receive support is also unclear – but appears to assume that around 50% of car sales in 2029 will be BEV, such that the 20.2% of privately purchased BEV sales receiving consumer subsidies equates to roughly 10.1% of all car sales. This assumes the portion of subsidised BEV sales remains fixed through to 2030, which may not hold true as absolute BEV volumes rise and Member States taper consumer purchase incentives. As such it is unlikely that anywhere near this 70.1% coverage would be achieved in practice and the ultimate impact on driving demand for low carbon materials will fall far short of what could be achieved.

Within the automotive industry, procurement mandates should therefore be considered for the private sector by placing the obligation on private fleets to procure vehicles made with low carbon steel and aluminium alongside the requirements applied to publicly supported schemes. The Commission’s own impact assessment treats 60% of sales – the corporate share – as falling within the scope of public support schemes, so a direct obligation on private fleet purchasers would simply ensure that the demand signal the IAA already assumes is, in practice, delivered. This would provide clear demand signals for low-carbon flat steel products, support the decarbonisation of primary steelmaking, and give the automotive sector a defined trajectory for the growing demand for vehicles made with low-carbon materials.

Recent amendments under the Automotive Package introduced an optional low-carbon steel credit from 2035, allowing manufacturers to offset a capped share of their fleet emissions through the use of EU-made low-carbon steel. This by itself is insufficient, due to its optional nature, late activation date, inapplicability to zero-emissions vehicles, and focus on just steel meaning it is unlikely to generate demand at the scale needed to drive industrial transformation.

4.3. Expansion to other sectors

We recommend that large construction projects (>1000 m2) and private fleets in the automotive sector should be seriously considered for inclusion in the initial regulation, as an important signal that ambitious lead markets for energy-intensive products will extend beyond public procurement.

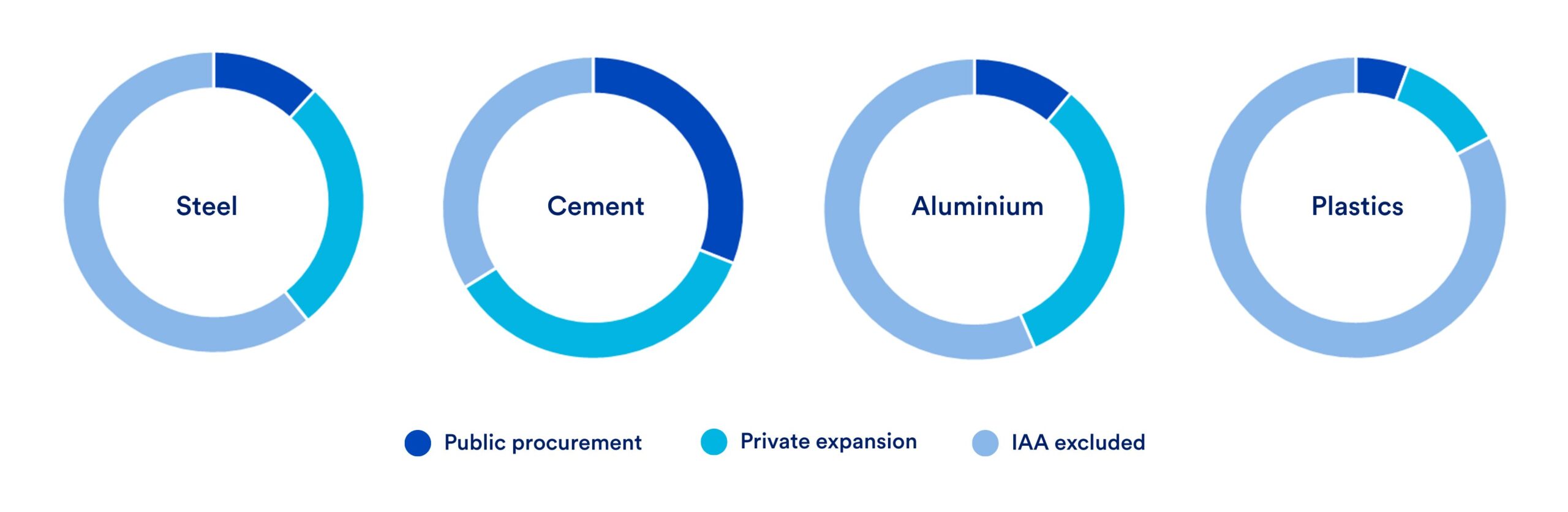

Figure 7: CATF proposed covered demand across energy intensive materials

The measures proposed within this brief will create meaningful demand for low-carbon materials across steel, concrete, aluminium and plastics, but will not by themselves be sufficient to cover the entire market demand for these products. The proposed coverage across construction and automotive sectors covers between 17% to 66% of the total demand across the four materials included, as shown in Figure 7.

By 2029, the Commission should assess the impact of other potential sectors where private sector measures could effectively build demand for these materials and, if appropriate, present a proposal by 2029. If the private construction and automotive cannot be included in the Regulation, they should be prioritised for assessment by the Commission, with a proposal by 2029. Assessment of the automotive sector should also consider other relevant legislative where requirements for low-carbon steel and aluminium could be incorporated. Furthermore, as the EU’s largest demand sector for plastics, an assessment of an expansion to the packaging sector should also be considered.

5. Expansion to other energy-intensive products

The IAA also fails to develop low carbon lead market demand across the remaining energy intensive materials of chemicals (other than plastics), pulp and paper, refineries, glass, ceramics and non-ferrous metals (other than aluminium).

This leaves a significant gap with most emissions from the production of energy-intensive materials not covered by lead market measures. We would therefore propose that by 2029 the Commission should bring forward a proposal to further extend demand-side mandates beyond those currently covered under the IAA. Of these sectors, creation of a viable lead market for fertilisers could be particularly impactful.

5.1. Fertilisers

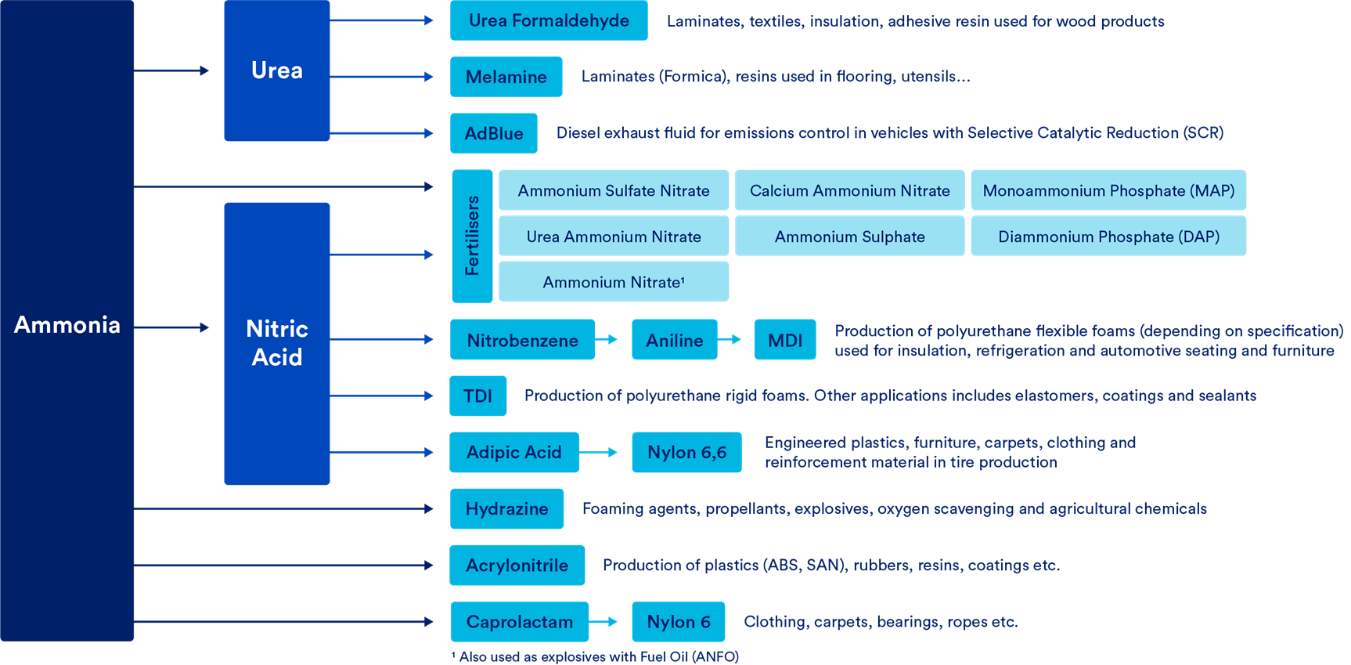

The EU produces around 17 Mt of fertilisers annually by mass of nutrients, of which roughly 72% are nitrogenous.52 These nitrogenous fertilisers dominate the sector’s emissions footprint, almost entirely because of ammonia synthesis – the Haber-Bosch reaction in which hydrogen is combined with atmospheric nitrogen. Ammonia is the critical input not only for fertilisers but for a range of downstream chemicals (Figure 8), and its production is concentrated across approximately 31 EU sites. Production of ammonia accounts for 1.9 Mt of hydrogen demand annually – roughly 26% of total EU hydrogen consumption – almost all of which is currently produced via unabated steam methane reforming.53

Figure 8: Ammonia value chain

There are a range of decarbonisation options available to reduce emissions associated with the production of ammonia. CCS retrofit is unusually well-suited to ammonia plants because the existing SMR process already separates a concentrated CO₂ stream prior to the synthesis loop, removing the most expensive step in carbon capture. This pathway addresses roughly two thirds of process emissions, with the remainder – primarily process heat – requiring electrification or fuel switching. Alternatively, the hydrogen input can itself be replaced with a low-carbon option produced through electrolysis with renewable electricity or reformation of natural gas with CCS.

What is missing is the demand for low-carbon products which could enable low carbon project investments. The EU chemicals sector is ageing, with analysis suggesting around 58% of EU primary chemicals capacity, including ammonia, requires reinvestment by 2035 and global modelling suggests ammonia alone will absorb 60% of the chemical sector’s additional cumulative Capex by 2050.54 Including fertilisers in the IAA with a proposal by 2029 for a demand side mandate could unlock demand and steer investments into low carbon production.

6. Conclusion

By ensuring long-term clarity on a growing procurement requirement, establishing ambitious and credible targets alongside clear definitions for low-carbon steel and cement, and expanding its scope to include additional strategic sectors, the IAA could play a central role in building the lead markets the EU needs to support an efficient and competitive industrial transition. Predictable demand signals and harmonised standards would help de-risk investment in clean industrial production, accelerate the commercialisation of low-carbon technologies, and strengthen confidence across supply chains.

This represents a major opportunity for the EU to reinforce its industrial competitiveness while advancing its climate objectives. A stronger IAA could help create the market conditions needed for European manufacturers to scale up low-carbon production, retain industrial capacity within Europe, and compete effectively in an increasingly global race for clean technologies and materials. At the same time, it would support emissions reductions in some of the most carbon-intensive sectors of the economy and contribute to the EU’s broader decarbonisation agenda. However, these outcomes will only be achievable if the IAA is sufficiently robust in both ambition and design.

Annex 1 – Low-carbon material project pipeline

Table A.1. Proposed and operational CCS projects in the European cement sector which have received Innovation Fund (IF) or national funding support.55

| Cement CCS project | Plant name | Country | Estimated low-carbon cement production (Mtpa) | Stated commissioning date | Notes on status, funding and access to storage |

|---|---|---|---|---|---|

| Brevik | Brevik | Norway | 0.5 | 2025 | Operational. 50% capture of 1 Mtpa output |

| Padeswood CCS | Padeswood | UK | 1.0 | 2029 | Under construction. |

| Go4Ecoplanet | Kujawy | Poland | 2.4 | 2027 | IF project. Likely to be delayed to post-2030. |

| K6 | Lumbres | France | 1.0 | 2028 | IF project. Likely delayed post-2029 |

| Carbon2Business | Lagerdorf | Germany | 1.6 | 2028 | IF project. Some CO2 will be utilised. |

| Accsion | Aalborg | Denmark | 3.0 | 2028 | IF project and shortlisted for Danish funding. Delivery by 2030 possible at the earliest. Linked to Greenstore onshore storage site, which targets operation by 2030. |

| Go4zero | Obourg | Belgium | 2.3 | 2028 | IF project. Currently on hold. |

| Olympus | Milaki | Greece | 1.4 | 2029 | IF project. Linked to Prinos storage site, which is expected to operate by 2030. |

| Ifestos | Titan Kamari | Greece | 3.0 | 2029 | IF project. Linked to Prinos storage site, which is expected to operate by 2030. |

| Anrav | Devnya | Bulgaria | 1.2 | 2030 | IF project. Expected to rebid with new storage site, close to the plant. |

| Gezero | Geseke | Germany | 1.0 | 2030 | IF project. |

| CO2llect | Rüdersdorf | Germany | 1.4 | 2030 | IF project. |

| Kodeco | Koromacno | Croatia | 0.5 | 2030 | IF project. Linked to Ravenna storage site, which is expected to operate by 2029. |

| Vaia | Montalieu | France | 1.5 | 2030 | IF project. Linked to Ravenna storage site, which is expected to operate by 2029 (but also requires inland transport). |

| Anthemis | Antoing | Belgium | 1.2 | 2030 | IF project. |

| CarboClearTech | Martres Tolosane | France | 0.8 | 2030 | IF project. Linked to Pycasso storage site, which is expected to operate by 2032. |

| AirvaultGoCO2 | Airvault | France | 1.0 | 2031 | IF project. |

| CPT01 | Campulung | Romania | 1.6 | 2031 | IF project. Associated with onshore storage site nearby, at an early stage of development. |

| DREAM | Rezzato-Mazzano | Italy | 1.5 | 2031 | IF project. Linked to Ravenna storage project, which is expected to operate by 2029. |

| Capt4Climate | Saint-Pierre-la-cour | France | 1.6 | 2032 | France GPID project. |

Table A.2. Calcined clay and other low-carbon cement projects in the EU.

| Calcined clay project | Country | Capacity (tpa) | Expected commissioning date |

|---|---|---|---|

| Saint-Pierre-la-cour (Holcim) | France | Up to 500,000 | Operational from 2023. |

| La Malle (Holcim) | France | Not stated | Operational from 2021. |

| Cížkovice | Czech Republic | Not stated | From 2026. |

| Xeuilley (Vicat) | France | 120,000 | Operational from 2024. |

| Saint-Maximin (NeoCem) | France | 200,000 | From 2025. Full capacity by 2030. |

| Q-CEM Ghent (Heidelberg Materials) | Belgium | Targeting scale up to 200,000 | Operational from 2026. |

| Futurecem | Denmark | Not stated – pilot scale | Operational from 2021. |

| Hoffmann Green Cement Bournezeau H1 and H2 | France | 400,000 | 2023 |

| Hoffmann Green Cement H3 | France | ~500,000 (based on combined H1,2,3 target of 1 Mtpa) | 2027 |

| Ecocem ACT Dunkirk | France | 300,000 | From 2026 |

| Ecocem ACT expansion (Fos-sur-Mer and Dunkirk) | France | 1,900,000 (including existing Dunkirk capacity) | From 2028 and 2030 |

Table A.3. Low-carbon steel projects in the EU.54

| DRI project | Company | Country | Planned output, iron (Mtpa) | Status | Plans for fuel |

|---|---|---|---|---|---|

| Boden Phase 1 | Stegra | Sweden | 2.1 | Under construction. Operational from 2026. | 100% green H2 |

| Flachstahl SALCOS | Salzgitter | Germany | 2.1 | Under construction. Operational from 2027. | Natural gas, H2 ramp up 2027-2030 |

| Duisburg | ThyssenKrupp | Germany | 2.5 | Under construction. Operational from 2027. | Natural gas, H2 ramp from 2028 |

| Dillingen Power4Steel | Saarstahl | Germany | 2 | Under construction. Operational by 2028/2029. | Natural gas, H2 from 2029 |

| Fos-sur-Mer GravitHy | France | France | 2 | Under development. Expects FID by 2027. | 100% green H2 |

| Gällivare | SSAB | Sweden | 1.35 | Under development. | 100% green H2 |

| Hamburg | ArcelorMittal | Germany | 0.1 | Demonstration plant under construction. Operational from 2026. | 100% green H2 |

| Total green iron output assuming natural gas phase out (Mtpa) | 10.15 (8.7 under construction) | ||||

| EAF and electric smelter projects | Company | Country | Planned output, steel (Mtpa) | Status | Source of iron |

|---|---|---|---|---|---|

| Boden Phase 1 | Stegra | Sweden | 2.5 | Under construction. Operational from 2026. Targets 5 Mtpa by 2030. | Boden H2-DRI |

| Oxelösund | SSAB | Sweden | 1.2 | Under construction. Operational from 2026 | Eventually from planned Gällivare DRI |

| Gijon | ArcelorMittal | Spain | 1.1 | Under construction. Operational from 2026. | Pig iron and undetermined DRI sources. |

| Lulea | SSAB | Sweden | 2.5 | Under construction. Operational from 2029. | Eventually from planned Gällivare DRI |

| Duisburg electric smelter | ThyssenKrupp | Germany | 2.5 | Under construction. Operational from 2029 | Duisburg DRI |

| Linz | Voestalpine | Austria | 1.6 | Under construction | Pig iron and HBI from Corpus Christi DRI (USA) |

| Donawitz | Voestalpine | Austria | 0.85 | Under development | Pig iron and HBI from Corpus Christi DRI (USA) |

| Dillingen | Saarstahl | Germany | 1.75 | Under development | Dillingen DRI |

| Volkingen | Saarstahl | Germany | 1.75 | Under development | Dillingen DRI |

| Flachstahl SALCOS | Salzgitter | Germany | 1.9 | Under development | Flachstahl DRI |

| Piombino | Metinvest | Italy | 2.7 | Under development | DRI from iron ore in Ukraine – new DRI furnace will be required. |

| Total potential green steel assuming phase out of carbon-intensive inputs | 20.35 (9.8 under construction) | ||||

Footnotes

- Sapir et al. (2022) Green public procurement: a neglected tool in the European Green Deal toolbox?

- Wyns, T., Kalimo, H. and Khandekar, G. (2024) Public procurement of cement and steel for construction – Assessing the potential of lead markets for green steel and cement in the EU. Brussels School of Governance.

- EU production was split 55% primary, and 45% secondary

- Eurofer, European Steel in Figures 2025. Determined with production values and average asset utilisation rate.

- LESS Certificate – Georgsmarienhutte GmbH

- LESS Certificate – Peiner Trager GmbH

- Eurofer: Industrial Accelerator Act position paper, 2026.

- Cement Europe (2025) Key facts and figures (2023 data)

- Sector emissions from CaptureMap by Endrava (Accessed 2026). Total emissions from EEA Greenhouse gases – data viewer.

- IAA Impact Assessment

- CATF (2025) The role for carbon capture and storage in decarbonising Europe’s cement sector.

- Cement Europe (2025) From ambition to deployment

- DETOCS project website

- Cement Europe (2025) From ambition to deployment.

- Heidelberg Materials (2025) Press release, 18 June 2025

- Padeswood CCS project website

- CATF CCS Map Europe

- European Commission Innovation Fund projects

- Direction générale des Entreprises Sept projets lauréats; Global Cement Aalborg Portland wins CCS tender. The Danish project and two of the three French projects are also Innovation Fund recipients.

- List of Innovation Fund projects. Where not stated, cement production capacity is estimated from facility emissions data from CaptureMap by Endrava, assuming 0.6 tCO2/t cement.

- Article 23 watch: Article 23 Explainer

- Brevik produces 1 Mtpa of cement and captures half the CO2 emissions. Heidelberg Materials use a mass balance approach to allocate all the emissions savings to half the output, creating 0.5 Mtpa of ‘near-zero’ cement.

- DESNZ (2025) Summary Business Case for Padeswood Carbon Capture Usage and Storage (CCUS) Project. Notes a clinker production capacity of 820,000 tonnes per year.

- IEA (2022) Achieving net zero heavy industry sectors in G7 Members

- VDZ introduces a new CO2 label for cement

- Higher strength concrete generally implies higher cement content and therefore more challenging decarbonisation.

- Assuming typical cement content (0.17 kg/kg) and emission intensity of non-cement components, the CO2 intensity of concrete in kg/m3 is around 0.45 × the CO2 intensity of cement in kg/t of cement.

- GCCA, 2025. Global Ratings for Concrete.

- Cement Europe (2025) Key facts and figures; MPA The concrete centre (2025) Standards for concrete.

- https://www.ecocemglobal.com/en-ie/act/act-the-solution/; https://www.ciments-hoffmann.com/en/solutions/h-ukr/

- Cement Europe (2025) From ambition to deployment.

- Heidelberg Materials (2022) https://www.heidelbergmaterials.com/en/pr-24-05-2022; Holcim (2023) https://www.holcim.com/media/media-releases/2023-climate-report

- Commission Implementing Decision C(2025) 4828 on a standardisation request to CEN as regards cement, lime and other hydraulic binders in support of Regulation (EU) 2024/3110

- Shanks et al. (2019) How much cement can we do without? Lessons from cement material flows in the UK.

- Procurement guidance for public bodies: Reducing embodied emissions in construction

- Subraveti et al, 2023.

- CATF analysis based on Figure 25 in Ramboll, 2023. Shares estimated from the A1-A3 production-stage stacked bar.

- World Economic Forum, 2023.

- CATF analysis based upon Subraveti et al, 2023, World Economic Forum, 2023, BCG, 2022, Ramboll, 2023, Transport Environment, 2025.

- Vehicle impacts consider aluminium and steel. Building impacts consider aluminium, steel and cement. Bridge impacts consider steel and cement.

- Including the addition of a procurement mandate on plastics as outlined in section 3

- Plastics Europe, 2025.

- Deloitte, 2025. Mobilizing consumer demand for sustainable investments

- Impact assessment report on the IAA proposal

- Deloitte, 2025. Mobilizing consumer demand for sustainable investments

- Plastics Europe, 2026.

- Cefic, 2026.

- Article 7(2) of the revised Energy Performance of Buildings Directive (2024/1275)

- Data is lacking on the portion of new construction which has a useable floor area greater than 1000 m2. An estimate was developed based upon the share of existing building stock which is non-residential and residential apartment blocks: Buildings Performance Institute Europe, 2011.

- Article 4 of Directive 2014/24/EU, as amended by Delegated Regulation (EU) 2025/2152

- Turner & Townsend: Regional Construction Cost Performance, 2024.

- Eurofer (2025) European steel in figures. The automotive sector accounts for over 30% of flat product demand, and is the single biggest user of these products.

- Fertilizers Europe, Industry Facts and Figures, 2023.

- CATF, Hydrogen in EU Industry, 2025.

- IAA Impact Assessment pg 168.

- https://www.catf.us/ccsmapeurope/

- Based on CATF analysis of the BloombergNEF database of steel decarbonisation projects.