The EU Methane Regulation has the potential to revolutionize the global energy market, but what would it actually do?

Here’s how the regulation boosts European competitiveness, energy security, and cuts pollution.

What is the EU Methane Regulation?

Global energy markets currently lack quality data on the origins and emissions of fossil fuels, making it difficult for buyers to differentiate between high-emitting and low-emitting energy producers.

The EU Methane Regulation addresses this market failure by harnessing the EU’s considerable buying power to require producers to report this data, thereby creating greater market transparency.

The reporting system will be built gradually over several phases to ensure data credibility and consistency, and, over time, incentivize producers to reduce their methane emissions intensity – translating climate performance into commercial value.

Myth: The EU Methane Regulation will cause energy prices to skyrocket.

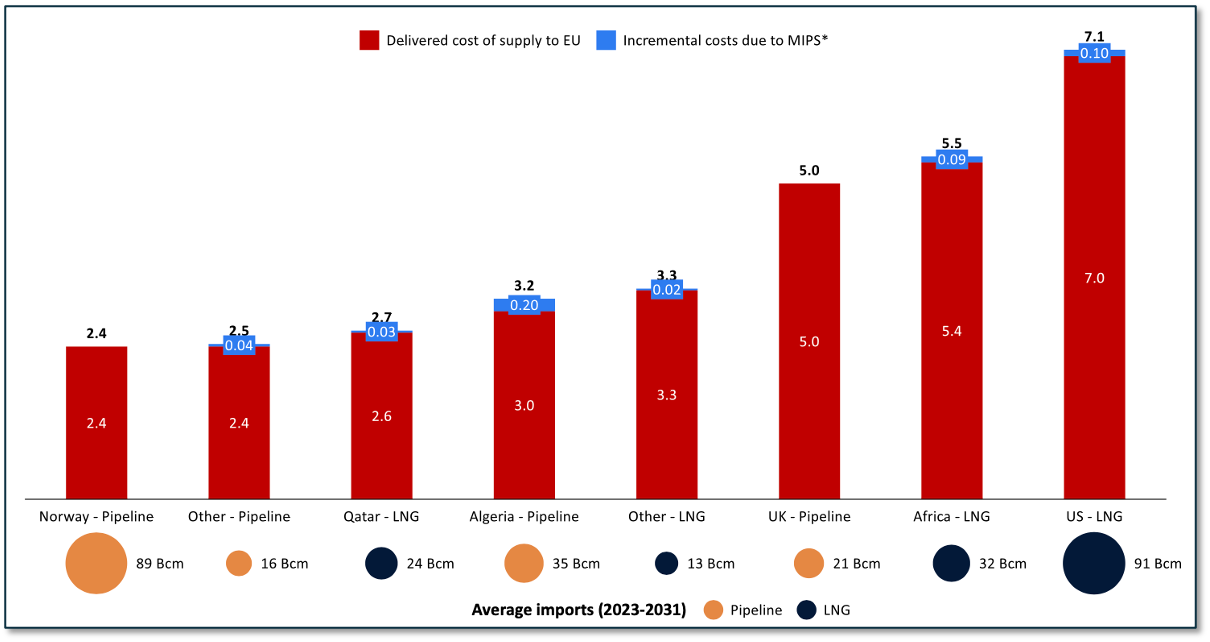

Fact: The EU Methane Regulation will have a minimal impact on oil and gas prices for EU consumers.

There will be minimal impact on oil and gas prices for EU consumers caused by the regulation as new costs (blue line) are low and can be absorbed into profit margins.

Higher costs for exporters usually don’t translate into higher costs for importers and consumers, because most exporters are ”price takers” and not “price makers.”

Exaggerated price impact predictions are a result of artificially modeled scarcity from trade bans that don’t exist. Geopolitical volatility and similar risks will remain the dominant drivers of short-term price shocks.

Europe faces real energy volatility, but the regulation is not what creates that volatility. The regulation does not ban imports, does not require strict physical tracing, and phases in gradually.

Incremental costs to gas exporters to the EU resulting from the implementation of the methane import standard

Sources: CATF and Rystad Energy. “Impact of an EU methane import performance standard: Impact Assessment Report.” 2023; Trading Economics. “EU Natural Gas”. 2026; EDF & Carbon Limits. “EU MR MRV compliance costs”. 2026

Myth: The EU Methane Regulation threatens energy security.

Fact: The EU Methane Regulation creates regulatory certainty and emissions transparency – strengthening market resilience and energy security.

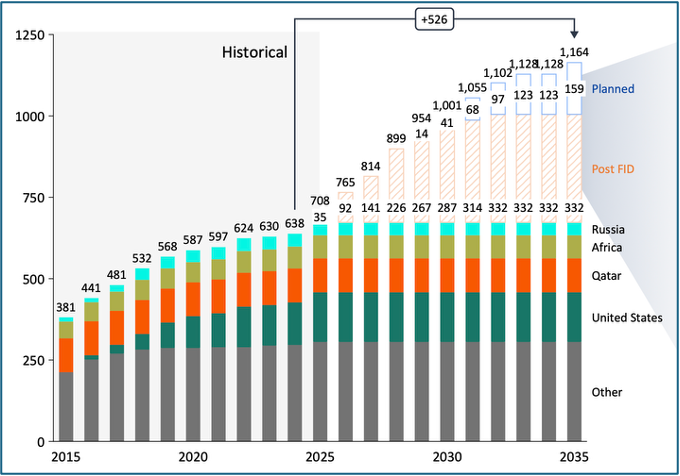

The Methane Regulation doesn’t restrict fuels from entering the EU – it imposes proportionate penalties. Conservative forecasts of volumes of oil and gas from exporters to the EU indicate that by 2027 the volume of OGMP Level 5 volumes will amount to roughly twice EU total demand. Supply additions can reduce baseline market tightness over time, putting downward pressure on prices, but it does not eliminate volatility: geopolitical disruptions and related risks continue to dominate short-term pricing even when capacity is expanding.

Methane waste is wasted energy. The EU Methane Regulation helps make emissions visible, so markets can reward cleaner, more efficient supply. Cutting methane emissions and non-emergency flaring could put 200 bcm of gas on the market, twice Qatar’s annual gas exports.

Global liquefaction capacity by regions and by production start year

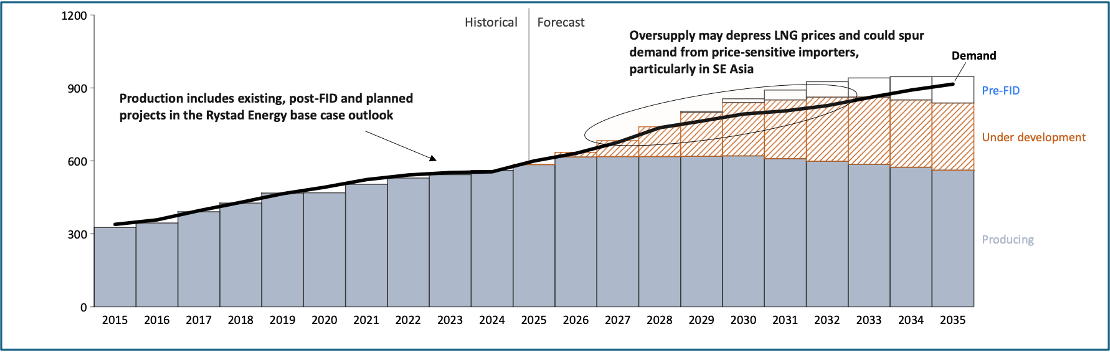

Global LNG demand and production by life cycle (billion cubic meter)

Source: Rystad Energy research and analysis, Global Gas & LNG Market Analysis Dashboard. Prepared for CATF in 2025.

Myth: The EU Methane Regulation harms industry.

Fact: The EU Methane Regulation makes industry more competitive and levels the playing field.

As markets are increasingly flexible, methane performance data makes low-emitting producers more competitive.

As prices converge around the world, environmental performance will become a critical factor that puts them first in line on premium markets.

The rules require producers abroad to meet the same standards in the EU, leveling the playing field around the world.

Source: Rystad Energy research and analysis, Global Gas & LNG Market Analysis Dashboard. Prepared for CATF in 2025.

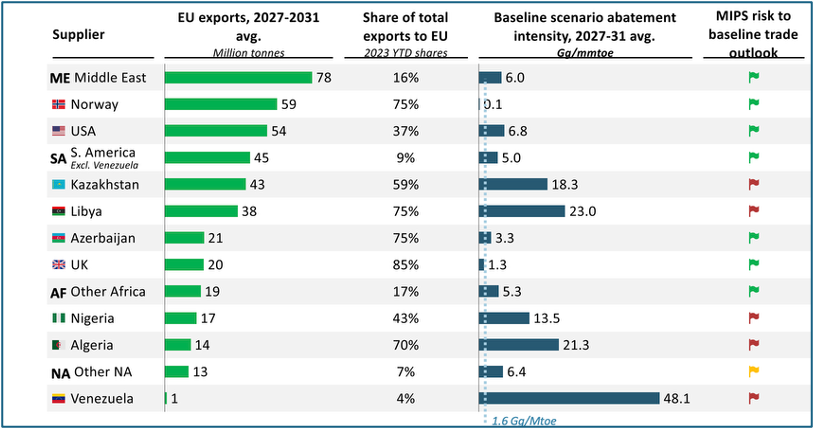

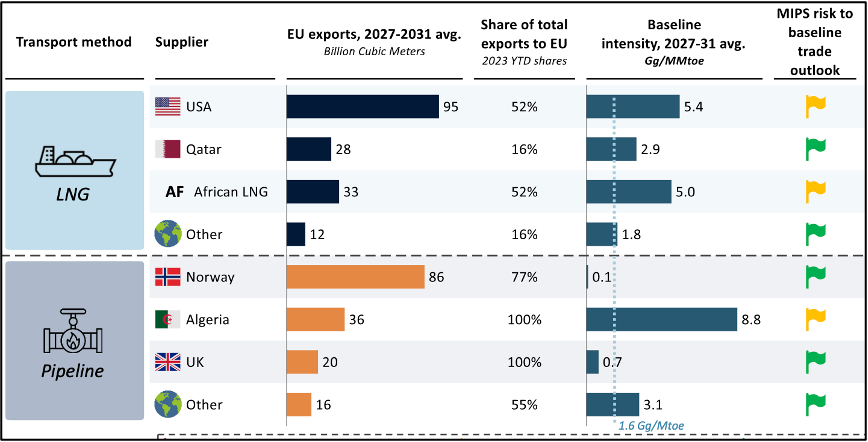

Myth: The EU Methane Regulation will push exporters away from Europe.

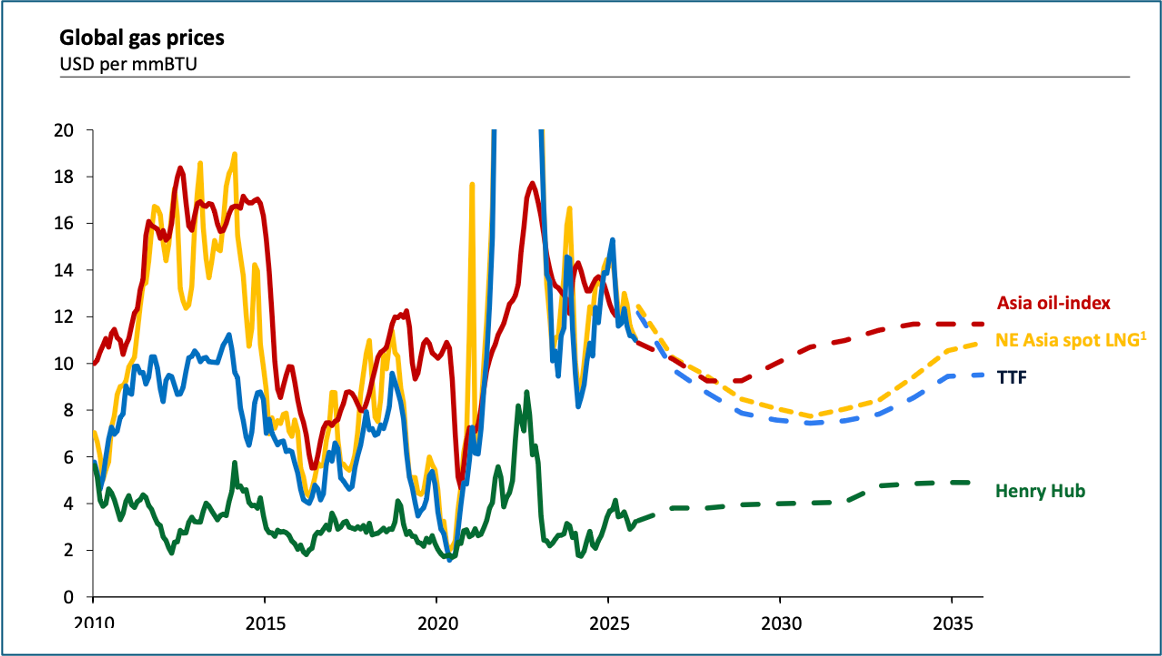

Fact: Exporters won’t walk away from customers paying some of the highest prices.

Isolated LNG cargo redirection to Asia reflects short-term arbitrage, not structural market shift. Major portfolio players still treat Europe as a core market, not one that they are retreating from. Major Asian LNG buyers, such as JERA, are reserving regassification capacity in Europe to offload cargos and optimize their global portfolios. This signals that they do not see the EUMR as a barrier, and that they recognize the premium the European market still stands to offer. Many exporters, such as in the U.S., need to export to Europe to recoup long-term investment costs for LNG expansion.

Trade flow analysis of top crude exporters to the EU

Trade flow analysis of top gas exporters to the EU

Source: CATF and Rystad Energy. “Impact of an EU methane import performance standard: Impact Assessment Report.” 2023.

Resources

EU Methane Regulation Penalties: Why Proportionate, Phased Penalty Regimes Pose No Energy Security Risks

The European Commission drafted a recommendation that would suspend penalties under the EU Methane Regulation for importer obligations due in 2027, 2028, and 2029. The stated justification is that legal uncertainty around penalty regimes, exacerbated by the Strait of Hormuz crisis, risks trade diversion of LNG cargoes away from the EU and is hampering the conclusion of new long-term supply contracts.

Unfortunately, both pillars of that justification fail upon examining the evidence.

Media Memo: The EU Methane Regulation in the Context of Energy Security and Competitiveness

This note provides context for journalists reviewing claims that the EU Methane Regulation could significantly disrupt energy supply or competitiveness. A growing body of analysis indicates that many of these concerns rely on assumptions that do not reflect how the regulation is structured or how energy markets function in practice. Evidence instead shows the regulation improves transparency and performance while supporting Europe’s vital decarbonisation pathway and maintaining stable supply incentives in addition to pursuing the already ongoing buildout of renewable energy.

Proposed Certification Criteria for Implementation of the EU Methane Emissions Regulation

As implementation of the EU Methane Regulation begins, strong certification criteria ensures competent authorities can prevent misreporting and ensure the Regulation achieves its climate and market objectives. In this brief, CATF provides a set of criteria that can be used to evaluate whether the environmental attributes reported by importers meet the EU Methane Regulation requirements and are grounded in credible evidence.

How ‘Following the Money’ Can Track Fossil Fuels Across the Supply Chain

Credibly tracking the origins and associated emissions of fossil fuels across the supply chain is increasingly critical to meet new standards, such as those set by the EU Methane Regulation. Trace-and-claim systems can track where gas is produced – and its associated emissions – by following gas along commercial pathways, providing an effective solution to meet the EU’s new standards and reduce emissions.

The Impact of EU Methane Import Performance Standard

This report shows that a phased methane import performance standard could be implemented as early as 2027, and would reduce emissions associated with oil and gas imports by at least 1.9 million tons per year. The report shows that the standard would have minimal price impacts for natural gas, and not pose any risk to EU energy security.

Methane Intensity for Oil and Gas Production

This report reviews the various formulae that have been used to calculate methane emissions intensity, with extensive discussion of the advantages and disadvantages of the various approaches.

Sign Up

Stay up to date on methane pollution prevention in Europe

"*" indicates required fields