Why claims that the EU Methane Regulation threatens energy supply miss the mark

Lately, a familiar claim has been resurfacing in industry commentary: that the EU Methane Regulation (EUMR) will disrupt Europe’s oil and gas supply and send prices soaring. One prominent example is a modelling study commissioned by International Association of Oil & Gas Producers from Wood MacKenzie.

These claims have gained traction, but they rely on assumptions that don’t reflect the design of regulation or global oil and gas markets. A closer look shows that these projected impacts are largely the result of unrealistic modelling choices, conservative market assumptions, and a basic misunderstanding of what the regulation actually requires.

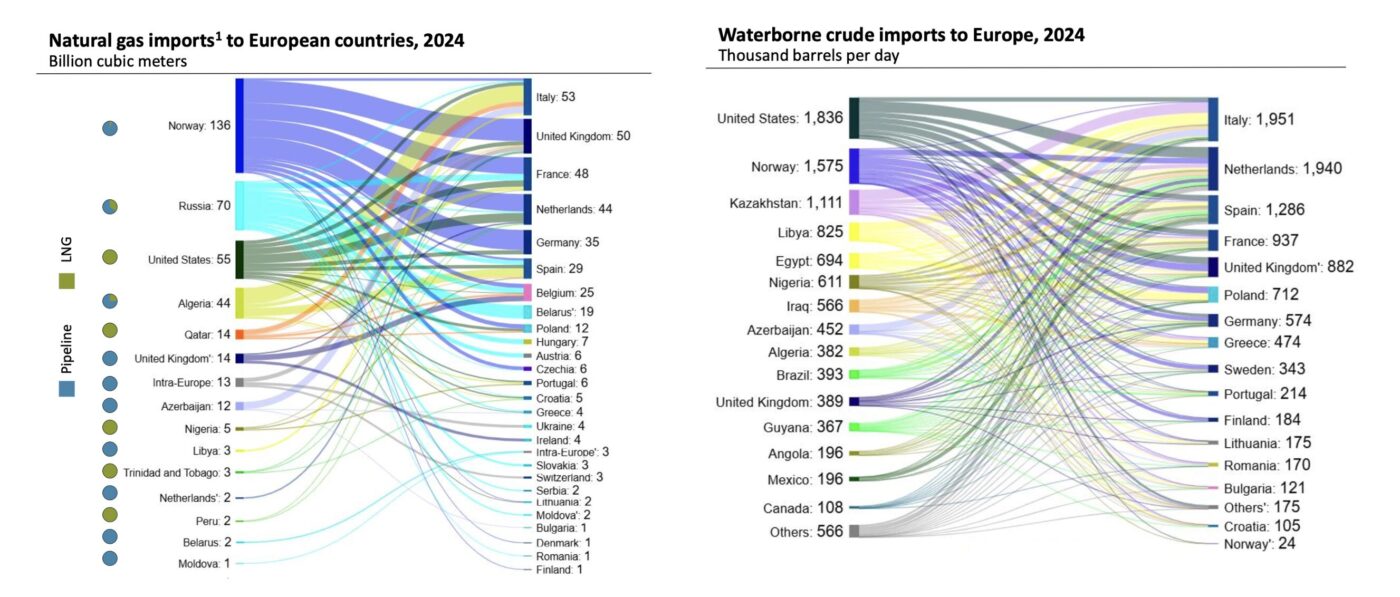

Overview of natural gas and waterborne crude imports into Europe:

1. The regulation doesn’t require molecule tracing

One of the most glaring methodological flaws in the IOGP report is that it assumed that compliance would require very strict “molecule tracing”, tracking individual molecules and volumes through the supply chain to prove their emissions profile. This assumption constraints which supplies are deemed eligible for the EU market in their model.

But at the recent Eurogas Annual Conference, Ditte Jorgenesen, Director General of DG ENER at the European Commission clarified that this level of molecule tracing would not be required, meaning a central constraint driving the modelled supply shock simply will not materialize.

2. The regulation doesn’t ban imports

A second premise of the modelling is that large volumes of oil and gas would effectively be excluded from the European market because they fail to meet methane requirements. This mischaracterizes the regulation.

The EU Methane Regulation does not impose a ban on imports. Its primary focus is on measurement, reporting, and verification (MRV) of methane emissions associated with oil and gas supplied to the EU. Producers are not required to demonstrate immediate best‑in‑class performance in order to maintain market access. Treating transparency obligations as if they were import prohibitions artificially creates a supply shock that the regulation itself does not impose.

3. The model assumes producers will walk away from Europe

The modelling also assumes that a large share of global producers would simply refuse to comply with methane transparency requirements and abandon the European market altogether. This assumption is highly implausible.

Europe remains one of the largest and most valuable energy markets globally. Producers have strong commercial incentives to retain access, particularly when the requirements involved, measuring and managing methane emissions, are among the lowest‑cost emissions reductions available in the oil and gas sector. In many cases, methane mitigation pays for itself through captured gas, and MRV costs are estimated to be 0.03-0.6% cost of production, and abatement costs estimated to be at 0.7% for gas and between 1.5%-2.5% for crude oil.

Global market trends reflect this reality. Major portfolio players still treat Europe as a core market, not one that they are retreating from. Major Asian LNG buyers, such as JERA, are reserving regassification capacity in Europe to offload cargos and optimize their global portfolios. This signals that they do not see the EUMR as a barrier, and that they recognize the premium the European market still stands to offer.

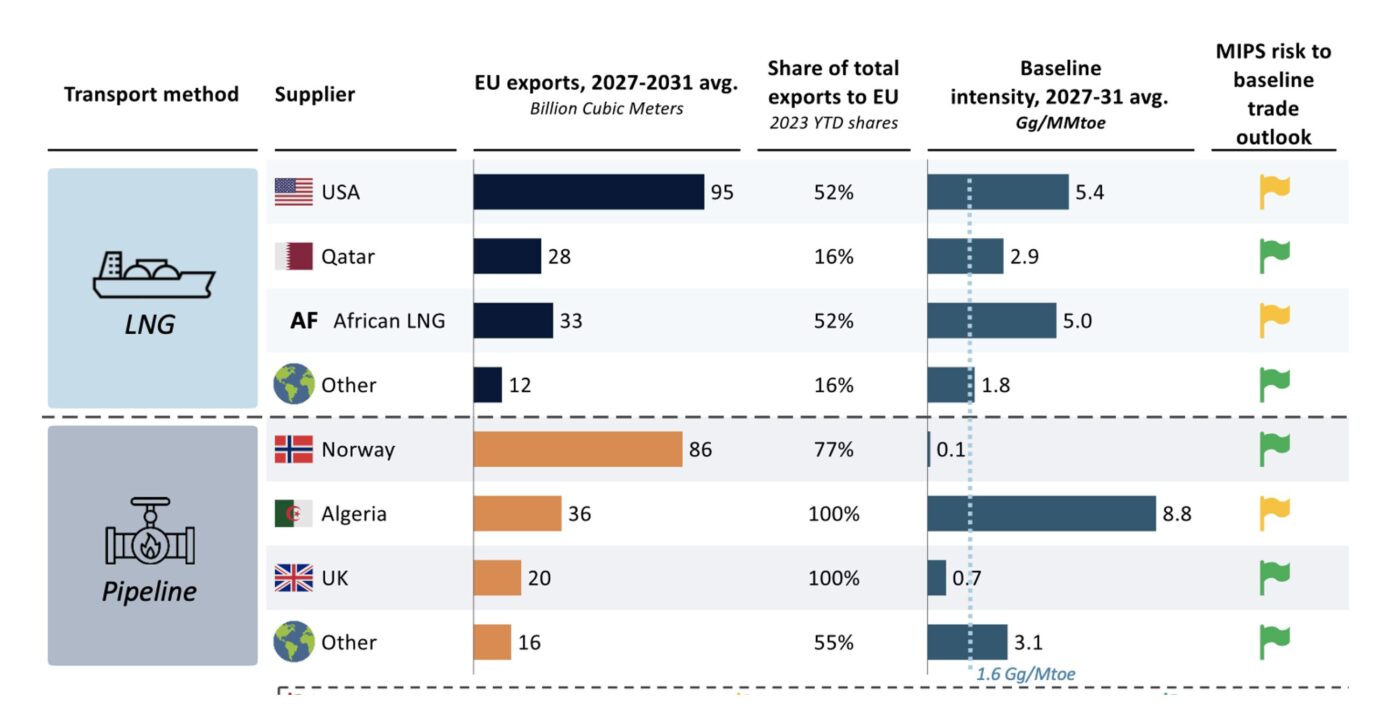

Modelled Trade Diversion of Gas Imports to the European Union:

4. It ignores the EUMR’s phased timeline

The modelling further treats the regulation as if it were imposed all at once, with immediate effects on supply. In reality, the EUMR is explicitly phased. Initial requirements focus on reporting. Verification frameworks are developed over time, and additional measures are introduced later.

This staged approach gives producers several years to adapt their operations, build monitoring systems, and improve methane performance. By failing to account for this timeline, the analysis overstates near‑term impacts and understates the capacity of markets to adjust.

5. Transparency can strengthen (not weaken) energy security

Finally, the analysis frames methane transparency as a threat to energy security, rather than as a potential source of resilience. In practice, the lack of reliable methane data across global supply chains is a structural weakness in oil and gas markets. Over time, greater transparency can strengthen market resilience and benefits producers by translating environmental performance into commercial value.

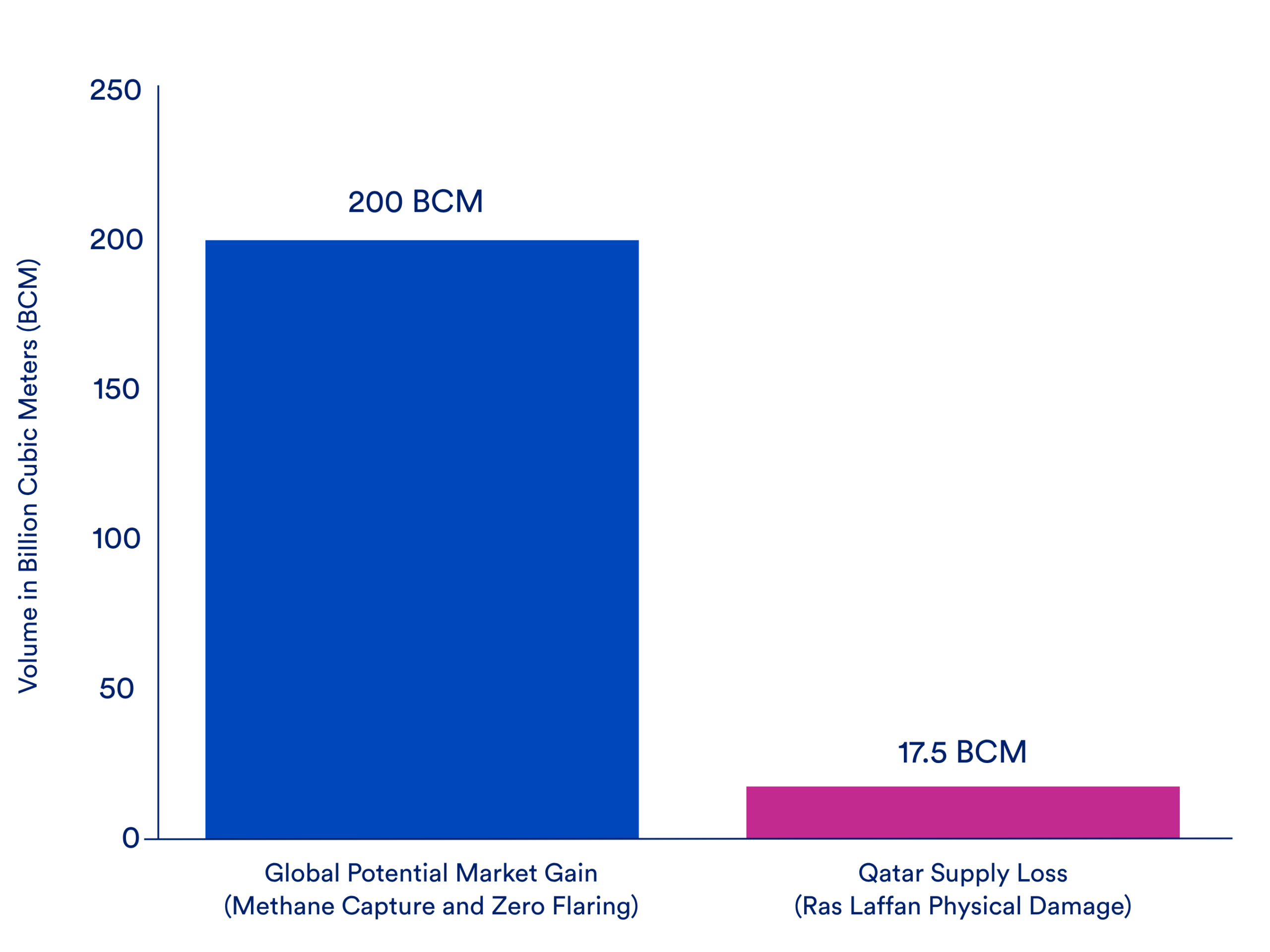

Improved measurement and verification also help identify emissions risks, reduce wasteful gas losses from leaks and venting, and improve the overall efficiency of oil‑associated gas production. The IEA estimates that 100 BCM of gas can be brought to market by cutting methane emissions. Another estimated 100 BCM of gas can be brought to markets if non-emergency flaring is cut. This is roughly equivalent to double the annual gas exports of Qatar every year.

Putting estimated global potential market gains in perspective:

In summary

Claims that the EU Methane Regulation will trigger an energy security crisis rely on assumptions that don’t hold up under scrutiny. Aspects of the methodology either do not line up with either the text of the regulation or the way oil and gas markets respond to new rules.

The EUMR does not restrict imports, instead it ramps up over time, focusing first on transparency, measurement, reporting, and verification. Most importantly, the regulation does not require the strict molecule level-tracing assumed in the IOGP report, which underpins much of the predicted supply disruption.

By making emissions visible through reporting, EU’s methane regulation can turn avoidable gas losses into an energy security solution. Keeping this regulation strong is the best way to cut a potent source of greenhouse gas emissions, improve market transparency, and translate environmental performance into commercial value.