Congress’s cuts threaten America’s technology progress

The Trump administration has signaled its support for carbon capture and storage (CCS), nuclear energy, and next-generation geothermal as pillars of an economic and security future. To accomplish this vision, however, the federal government needs to address key gaps that are preventing the commercialization of its own energy breakthroughs.

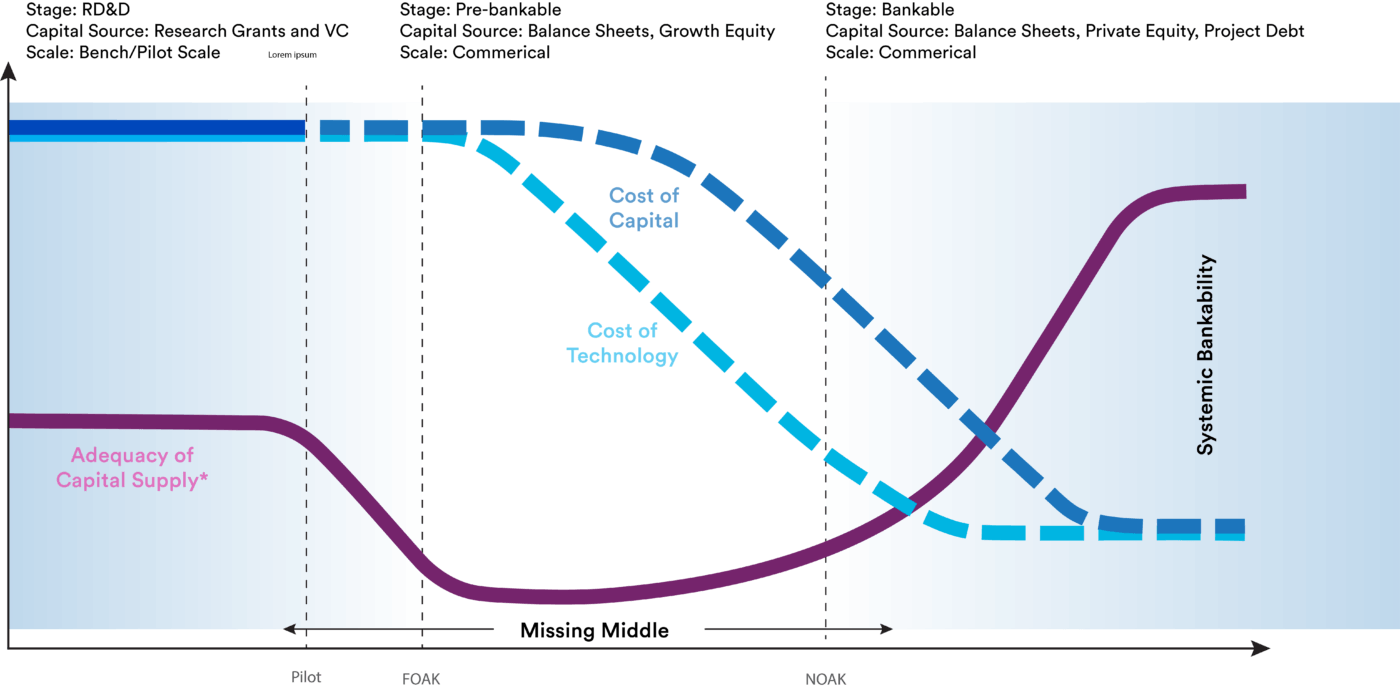

Many new energy infrastructure technologies in the U.S. face a structural investment gap that stalls their commercialization, often referred to as the “missing middle.” Addressing that gap is essential to enable private investment and markets to takeover and scale a technology.

The federal government has addressed this gap in the past when technologies aligned with national strategic priorities. SpaceX, for example, benefited from direct procurement and funding by the Department of Defense and NASA. Shale gas drilling innovation, in another example, benefited from targeted federal research and development and tax credits. These were strategic investments by the U.S. government that, in addition to pre-existing conditions, created entire industries worth hundreds of billions of dollars in economic value.

To accomplish current U.S. energy innovation goals, the administration has an opportunity to catalyze commercialization of technologies. First, it needs to be careful not to remove key incentives for emerging technologies that are slated to be cut in the recent House budget reconciliation bill. Beyond that, it should evaluate how the federal government can address nine conditions – characterized in a new systemic bankability framework – needed to accelerate energy technology commercialization. needed to accelerate energy technology commercialization.

The “missing middle” gap

America faces a commercialization gap. Broadly speaking, commercializing large energy infrastructure technologies involves advancing a technology from small-scale research and development (R&D) to widespread commercial-scale deployment. To bridge these end points, technologies need to deploy often costly commercial-scale projects over time that improve the technology, reduce costs, and instill a high degree of confidence in investors that projects can deliver predictable returns.

In practice, however, there is a structural investment gap referred to as the “missing middle” that slows the formation of this bridge. Unlike software startups that can prototype quickly and cheaply, energy infrastructure technologies require large-scale pilot projects that have no natural investor. Demonstration projects require a scale of investment that is too large for venture investors, but too risky for institutional investors. At this stage, the combination of risk and investment scale that has no suitable investor (i.e., a “missing middle”) and technology progress stalls (Figure 1).

Establishing systemic bankability to enable private markets to scale innovation

Together with industry and academics, Clean Air Task Force has outlined nine conditions that need to be established to scale energy infrastructure technologies. Widespread and pervasive existence of these conditions results in systemic bankability – access to large- scale institutional capital that enables speed and scale of deployment.

The nine conditions to establish systemic bankability include:

- Construction cost overrun risk: The risk that the construction costs projected at the time of final investment decision get significantly inflated during the construction period.

- Technology performance risks: Risks related to the technology or overall project not performing as expected at FID, including lesser output than expected or higher operating costs than expected.

- Revenue adequacy risk (volume and price) risks: Risks related to whether the project will earn the necessary amount of revenue to satisfy financial obligations.

- Regulatory certainty: Risks related to predictability and efficient implementation of policies relevant for the financial performance of the project, including permitting complexity and timelines.

- Access to enabling infrastructure networks: Whether a project can access the necessary infrastructure networks for its operations and performance. Networks may be electricity transmission, fuel pipelines, carbon dioxide pipelines and storage, and others.

- Social acceptance: Refers to the social license to locate and operate a project within its community.

- Robust supply chains: Refers to the robustness of the supply chains necessary to build and operate a project.

- Access to commercial insurance: Whether the project can access commercial insurance to insure its financial performance.

- Adequate delivery system: Refers to whether there is enough labor to build and operate a project. Examples include financial deal processing capacity and engineering, procurement, and construction management, and skilled operating labor.

Through a variety of potential mechanisms, the U.S. government can help establish these conditions until private markets take over. Notably, many mechanisms exist beyond direct (e.g., grants) and indirect incentives (e.g., tax subsidies), including government procurement, regulatory reforms, insurance, and more. Without these conditions, technologies will not scale rapidly.

The path forward

Energy infrastructure technologies like nuclear, geothermal, and CCS technologies won’t commercialize through market forces alone – they need the same strategic support that created America’s aerospace and hydraulic fracturing industries.

Recent actions by the Trump administration and Congress are having mixed impacts on the ability for technologies to overcome the “missing middle” and achieve system bankability. For most, these actions have largely reduced the ability to overcome market gaps. Proposed cuts to tax credits in the House’ reconciliation draft undermine revenue adequacy for nuclear, geothermal, and CCS projects, and the ceasing of the Department of Energy’s grant and loan programs will reduce the crowding-in of private investment into the “missing middle” gap. In contrast, the administration’s recent executive orders on nuclear regulatory reforms and deployment only partly address the “missing middle” for new nuclear but overall are insufficient to drive new nuclear deployment.

Going forward, the U.S. government will need to address all nine conditions of systemic bankability for its strategic technologies. This includes, but is not limited to, additional executive orders accelerating deployment and improving bankability conditions, and empowering the Department of Energy to help finance early-stage pilot and demonstration projects.

Congress and the administration can choose American energy leadership or technological dependence: invest in bridging the missing middle or surrender America’s innovation advantage.