U.S. clean energy investments: 2026 Quarter 1 analysis

Federal policy and executive actions have a direct impact on private investments in communities across the U.S. – either hindering investments or catalyzing them. CATF tracks private investments in clean energy projects that are eligible for federal incentives as well as the status of federal policies that may impact them. Each quarter, CATF highlights changes to federal policies and new executive actions and analyzes how these changes have affected investments across U.S. states and districts.

What’s impacting investments in Q1?

Summary: Executive branch implementation was a driving factor affecting energy investments in Q1 2026. These actions continue to underscore the federal government’s impact on energy investment decisions and outcomes. Policy certainty, or lack thereof, continued to remain critical for investment pipelines.

Key takeaways from Q1 2026:

- Electric Power and Industry: Investment increased in Q1, largely driven by just a handful of projects. Announced nuclear and sustainable aviation fuel (SAF) investments, for example, were primarily comprised of one large project per sector. Nuclear, storage, and critical minerals continued to benefit from clear demand signals and supportive federal policies, while fragile policy support for hydrogen, solar, carbon management, and SAF continued to translate into mixed investment outcomes.

- Manufacturing: Actual investments continued to decline for the sixth consecutive quarter. Cancellations decreased from ~$8 billion to $1.5 billion, potentially attributable to a shrinking pipeline of announced project investments over previous quarters, resulting in fewer projects left to cancel, combined with consistent federal policy support for batteries and critical minerals. Investment in critical mineral production is expected to continue increasing in future quarters, following Q1 executive actions that signaled strong federal policy support for growing domestic supply chains.

Federal Policy

Congressional appropriators passed FY26 appropriations bills, which included the energy and water appropriations bill signed into law by President Trump after bipartisan, bicameral negotiations. FY26 appropriations have a topline cut of roughly $1 billion for the Department of Energy (DOE) line items associated with clean energy priorities relative to the FY25 package: a clear decrease in funding levels, but not the level sought by the President’s Budget Request.

Executive Actions

During Q1, the federal government took the following actions signaling strong federal policy support for growing the domestic critical minerals supply chain.

- White House Proclamation on Adjusting Imports of Processed Critical Minerals and their Derivative Products into the United States. Published in January 2026, the White House Proclamation on adjusting imports of processed critical minerals and their derivative products (PCMDPs) determined that the U.S. is too reliant on foreign sources of PCMDPs, which are essential to energy infrastructure. The proclamation is a signal of federal support for increasing domestic capacity in the energy infrastructure supply chain, which could raise prices in the short-term until domestic supply chains mature.

- Export-Import Bank of the United States (EXIM) Project Vault. In February 2026, EXIM approved and launched a direct loan of up to $10 billion for Project Vault, establishing the U.S. Strategic Critical Minerals Reserve, an independently governed public-private partnership that will store essential raw materials in secure facilities across the U.S.

- 2026 Critical Minerals Ministerial. In February 2026, the U.S. signed new bilateral critical minerals frameworks and MOUs with eleven countries, announced U.S. government financing opportunities to support strategic minerals projects, and announced the creation of the Forum on Resource Geostrategic Engagement (FORGE), which will address ongoing challenges in the global critical minerals marketplace.

- Section 301 of the Trade Act of 1974 tariff increases on Chinese imports. Following the Office of the United States Trade Representative 2024 notice of modification to Chinese tariffs imposed under Section 301, tariffs increased on supply chain components relevant for batteries, EVs, wind turbines, and grid technologies starting in January 2026. Non-EV lithium-ion battery tariffs increased from 7.5% to 25%, and natural graphite and permanent magnet tariffs increased from 0% to 25%. This activity builds upon ongoing U.S. trade policy, including tariffs, which are increasingly influencing domestic investments in clean energy technologies and manufacturing. CATF wrote about the potential impacts of recent trade policy here.

Additional Q1 executive actions with energy investment impacts included:

- IRS Notice 2026-15: Guidance to Apply Interim Safe Harbors for Purposes of Determining a Taxpayer’s Material Assistance from a Prohibited Foreign Entity; Other Prohibited Foreign Entity Guidance. In February 2026, IRS released interim guidance with a framework for calculating material assistance cost ratio (MACR), safe harbors, and documentation standards for taxpayers claiming 45Y, 48E, and 45X tax credits to comply with OBBBA’s prohibited foreign entity (PFE) restrictions. Taxpayers can use the guidance to calculate material assistance cost ratios until formal regulations are published, providing some clarity but also introducing increased compliance costs and documentation burdens. Uncertainty remains on PFE definitions, scope of effective control, existing ownership attribution rules, and frameworks for technologies like nuclear and geothermal, topics which are expected to be addressed by IRS later this year.

- Wind project permitting delays at the Pentagon. The federal government continued to slow permitting for clean energy projects, including reported efforts to halt previously routine approvals for wind projects at the FAA and DOD.

- DOT Notice of Proposed Modification of the Waiver of Buy America Requirements for Electric Vehicle Chargers. In February 2026, the U.S. Department of Transportation (DOT) Federal Highway Administration (FHWA) proposed increasing domestic content requirements for EV chargers from 55% to 100%. To receive federal funding, nearly all charger materials would need to be made in the U.S. – a logistical challenge given the realities of the EV supply chain.

- IRS Proposed Rules for 45Z Clean Fuel Production Credit. In February 2026, IRS released proposed rules for the Section 45Z Clean Fuel Production Credit in accordance with OBBBA changes.

Findings

Electric Power

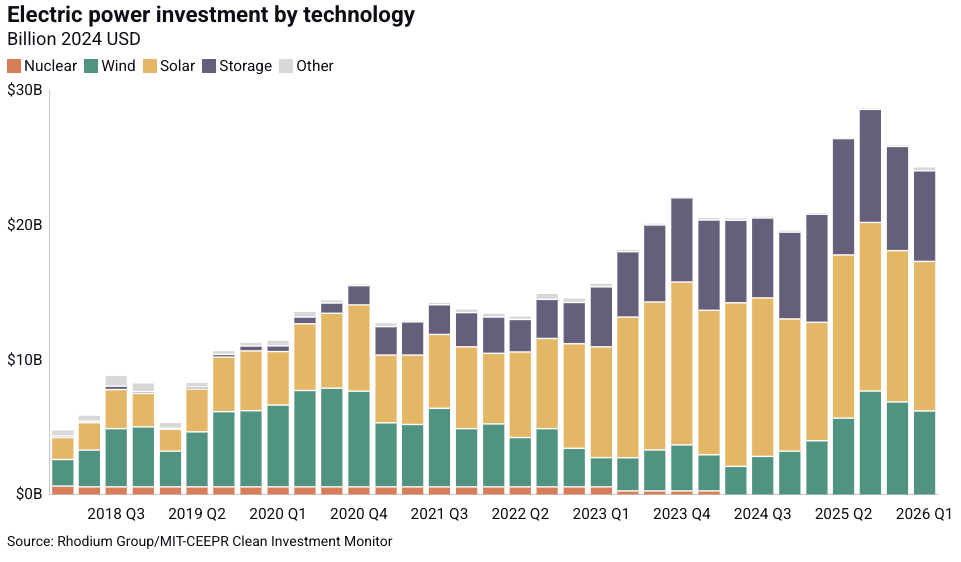

Rhodium Group data shows actual1 clean electricity production investment totaled ~$24B in Q1 2026, comprised of solar ($11.1B), storage ($6.7B), and wind ($6.2B). Announced2 investments totaled ~$60.8B and were mostly comprised of nuclear (~$27B), solar (~$17B), and storage (~$10B) investments.

Figure 1. Actual electric power investment by technology

Solar

Actual Q1 investments totaled ~$11.1B and announced investments totaled ~$17.3B.

Utility-scale solar projects faced accelerated tax credit termination timelines and narrower beginning of construction rules in Q1, and new FEOC/PFE compliance requirements provided by the IRS in Notice 2026-15 (Guidance to Apply Interim Safe Harbors for Purposes of Determining a Taxpayer’s Material Assistance from a Prohibited Foreign Entity; Other Prohibited Foreign Entity Guidance). Project developers have until July 4, 2026, to begin construction or December 31, 2027, to place projects in service to remain eligible for 45Y PTC/48 E ITC tax credits; as those windows narrow, so might new announced investments. In addition, slowed federal permitting for solar and storage projects remains a challenge for the industry, which estimates 36% of planned power is at risk. However, EIA estimates 51% of planned 2026 capacity additions will come from solar, with more than half of new utility-scale capacity planned for Texas, Arizona, California, and Michigan. We will continue to track how sunsetting tax credit eligibility windows impact future quarter investment figures and capacity additions.

Wind

Actual Q1 investments totaled ~$6.2B and announced investments totaled ~$6.4B.

Like solar, windprojects also faced accelerated tax credit termination timelines and tightened beginning of construction rules in Q1, and new FEOC/PFE compliance requirements provided by the IRS in Notice 2026-15 (Guidance to Apply Interim Safe Harbors for Purposes of Determining a Taxpayer’s Material Assistance from a Prohibited Foreign Entity; Other Prohibited Foreign Entity Guidance). Project developers have until July 4, 2026, to begin construction or December 31, 2027, to place projects in service to remain eligible for 45Y PTC/48 E ITC tax credits; as those windows narrow, so might new announced investments. In addition, federal actions to delay permitting of wind projects has escalated to a DOD de facto ban on all new wind projects, though the DOD policy has been challenged in court.

Storage

Actual Q1 investments totaled ~$6.7B and announced investments totaled ~$9.7B.

Actual and announced investments in Q1 remained steady while installations represented the strongest Q1 on record, totaling 9.7 GWh, a 32% increase compared to Q1 2025. Unlike wind and solar, energy storage retained clean electricity investment tax credit eligibility without early termination. FEOC/PFE guidance released by IRS provided a relatively workable framework and safe harbor for energy storage systems.

Industry outlook and demand for battery storage is favorable with over 610 GWh projected to be installed by 2030, driven by data center growth, global fuel market instability, and state storage targets. Federal approvals will play a key role in realizing those projections, with SEIA estimating 467 solar and storage projects totaling 101 GW and 36% of new planned capacity is vulnerable to stalled permitting processes and delays or cancellations due to conflicting administration priorities.

Nuclear

Actual Q1 investments totaled ~$0 and announced investments totaled ~$26.7B.

Q1 announced investments surged to $26.7B, all attributable to Project Matador, a 17GW hybrid energy and data infrastructure campus in Carson County, Texas, which plans to deploy four Westinghouse AP1000 reactors. New and existing nuclear projects continue to be eligible for 45Y/48E (new projects) and 45U (existing projects) tax credits, but interim FEOC/PFE guidance released by Treasury did not address the nuclear supply chain, continuing to inject uncertainty for how the nuclear industry will demonstrate compliance with the new tax rules. We expect additional investments in future quarters as federal support continues and industry works to scale and meet national and state deployment goals.

Industry

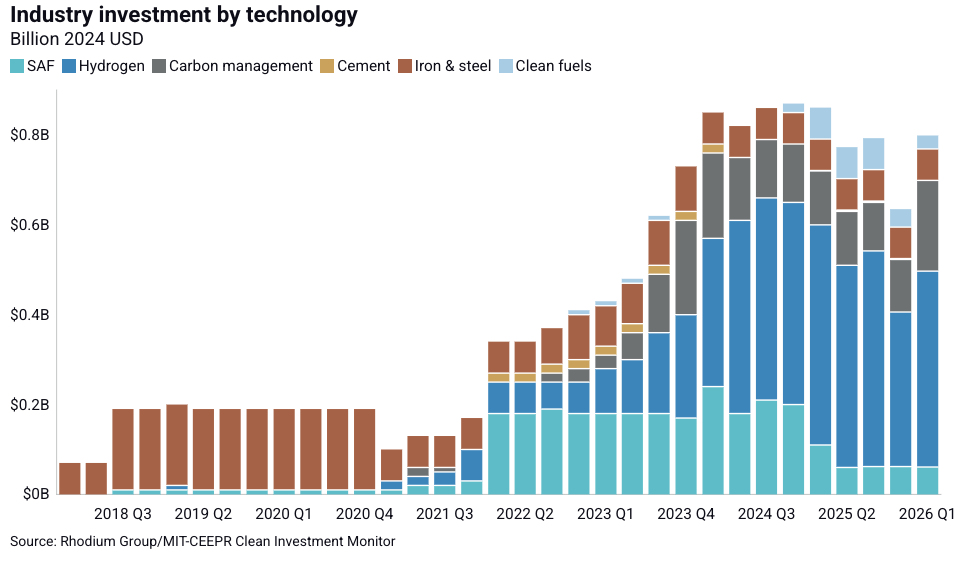

Rhodium Group data shows actual industry investment totaled ~$1B in Q1 2026, comprised of hydrogen ($435.6M), carbon management ($201.7M), iron & steel ($65.7M), SAF ($60M), and clean fuels ($28.5M). Announced industry investment totaled ~$1.5B, comprised of SAF ($1.4B) and carbon management ($87.5M).

Figure 2. Actual industry investment by technology

Hydrogen

Actual Q1 investments totaled ~$435.6M and announced investments totaled ~$0.

Clean hydrogen projects continued to face a lack of policy certainty and unclear demand/offtake signals. Investments increased slightly for clean hydrogen projects in Q1 2026, the majority of hydrogen investments in two fossil-based hydrogen projects with carbon capture in Texas and Indiana, and one electrolytic hydrogen project in Utah. However, clean hydrogen projects continue to face hurdles in accessing the 45V tax credit, namely the restrictive 2027 “begin construction” deadline and the proposed rollback of GHGRP Subpart W, along with continued uncertainty around federal support for clean hydrogen projects (including hydrogen hubs) by DOE or Congress. One example of policy uncertainty translating into investment disruptions is the March 2026 Woodside Energy announcement that the start of CCS ammonia production at its Beaumont New Ammonia facility in southeast Texas, which was originally intended to begin in the second half of 2026, will be delayed indefinitely.

Similar investment trends will likely continue in the near term under existing federal policy, including both project investments and cancellations. Industry perspective on hydrogen is shifting towards integrated, project-level solutions rather than a standalone energy solution to develop and deploy, as exemplified by the trend of large project-specific investments in the chemical and fertilizer industries.

Carbon Management

Actual Q1 investments totaled ~$201.7M and announced investments totaled ~$87.5M.

DOE funding freezes, rescissions, reallocation of IIJA funds to coal-based power plants, and EPA’s GHGRP rollback proposal continued to affect carbon management deployment and create industry certainty, despite OBBBA retaining and enhancing the 45Q tax credit for carbon sequestration.

Q1 actual investments included continued progress on the FOAK Carbon TerraVault I project, which completed its final steps necessary to begin CO2 injection. The first injection of CO2 that would have otherwise been emitted occurred in May 2026, marking California’s first operational CCS project.

In future quarters, we will track whether the DOE retained and modified list of projects, released after Q1 2026 ended but that includes CCS and DAC hubs, will result in actual investments in carbon management. We will also continue to track Treasury’s 45Q Carbon Capture Sequestration interim guidance, released in December 2025, and potential regulatory updates from Treasury, which could give more certainty for industry to be able to access 45Q credits.

Sustainable Aviation Fuel (SAF)

Actual Q1 investments totaled ~$61M and announced investments totaled ~$1.4B.

IRS’ proposed regulations for the 45Z Clean Fuel Production Credit included clarity on OBBBA’s lifecycle emissions accounting, registration requirements, and eligibility standards for clean fuel and SAF producers. The rule also included new compliance costs for developers.

SAF projects continued to be negatively impacted by economics following OBBBA’s changes to the 45Z tax credit structure that reduced the $1.75/gallon rate for SAF to $1.00/gallon, in addition to the shortened eligibility window of the 45V hydrogen production tax credit. SAF investments accounted for 94% of industry investments in Q1 2026, but those investments are attributable to a single project (more below). This investment represents a significant decrease in actual investments compared to last year, 46% lower than Q1 2025 before OBBBA reduced the tax credit available to SAF.

The project comprising the Q1 SAF investments is Southern Energy Renewables’ plan to develop a new bio-methanol and SAF production facility in St. Charles Parish, Louisiana. Helping drive the project is a combination of state-level incentives, including access to Louisiana’s FastStart workforce development program, a $1M performance-based state grant for infrastructure improvements, and the state’s Industrial Tax Exemption program.

Recent geopolitical uncertainty is bringing more attention to SAF, as a means of countering feedstock supply risks; it will be worth watching how the market responds as conflicts evolve. Congress is also considering whether to reinstate the special tax credit rate for SAF, which would increase domestic support and unlock investments in future quarters.

Manufacturing

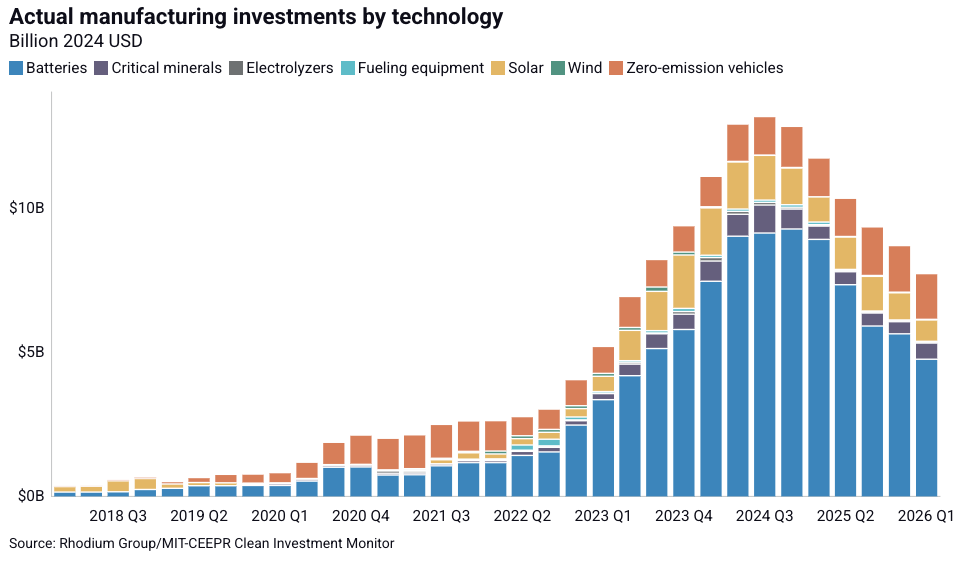

Rhodium Group data shows actual manufacturing investment totaled ~$7.7 billion in Q1 2026, a decline from the ~$9 billion recorded for Q4 2025 and for the sixth consecutive quarter. Battery manufacturing investment continued leading most actual investments totaling ~$4.8 billion, followed by zero emission vehicles (~$1.6 billion), solar ($736.6 million), and critical minerals (~$563.6 million). Critical minerals investments increased slightly from Q4, indicating favorable conditions for technologies and projects with long-term demand signals and strong alignment with federal supply chain priorities.

Actual manufacturing of solar, for example, is facing hurdles despite the U.S. onshoring the entire supply chain last year; the industry needs access to solar components and basic infrastructure materials like steel that are challenging to access through current trade policy. Battery storage actual investment has declined, however, actual production is increasing: Q1 2026 set a record for battery energy stationary storage installations at 9.7GWh. Actual manufacturing investment in battery storage is expected to continue in future quarters as the U.S. grows its domestic capacity to meet its energy storage needs. Industry is also shifting existing production from EVs to energy storage amid current policy headwinds for EVs and a growing demand for energy storage for data centers and the grid. Notably the energy storage sector has committed to invest $100 billion in American grid batteries, indicating continued manufacturing investment should be anticipated to build in future quarters.

Figure 3. Actual manufacturing investment by technology

Project cancellations were significantly lower in Q1 2026 than in Q4 2025. In Q4 2025, Rhodium Group analysis identified ~$8.4 billion in cancelled manufacturing investments across batteries, zero emission vehicles, and critical minerals sectors. In Q1 2026, cancelled manufacturing investments totaled ~$1.5 billion across solar and zero emission vehicles sectors. Solar represented the highest Q1 cancellations (~$1 billion), yet manufacturing investments are expected to continue amid policy uncertainty from tariffs and new restrictions on tax credits from FEOC/PFE still being implemented. The decrease in cancelled investments in Q1 may be attributable to a shrinking project pipeline following steady quarterly declines in announced investments (as shown in Figure 4 below) and consistent federal policy support for batteries and critical minerals.

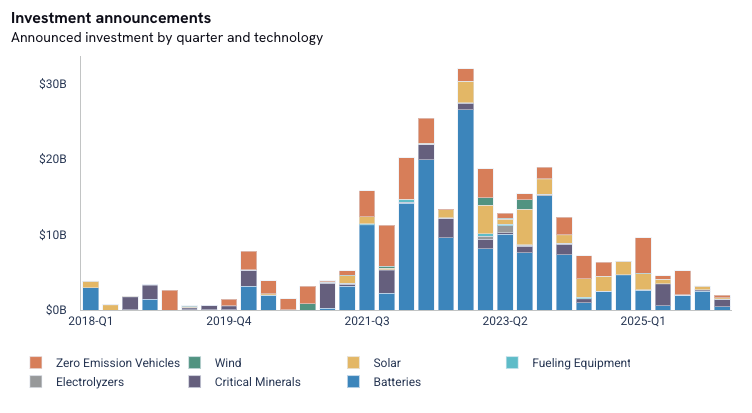

Figure 4. Manufacturing investment announcements by technology

Federal government support is leading to increased announced investments in critical minerals. Whereas other announced investments have declined, due to a combination of shifts toward production and lowering demand amid lessening federal support, critical mineral investment announcements are increasing. We expect these announcements to increase in future quarters, as the federal government continues to support critical minerals, investing in critical mineral companies and even taking equity stakes. However the recent international policy approach toward securing processed critical minerals from other countries, as noted above, recognizes that much of this supply chain will still be dependent on other countries rather than full domestic production.

1 Announced investment is the total reported or estimated investment amount for a facility or project.

2 Actual investment is the real dollars spent in the given quarter on retail purchases or new facility construction. Rhodium estimates actual investment by distributing the total investment proportionally over the construction window, based on either reported completion time (when available) or modeled completion time based on the average of past investments in that technology category. Rhodium conservatively assumes a facility advances through construction stages only when we can identify evidence of a groundbreaking. If evidence is lacking, facility timelines are adjusted accordingly, with start dates pushed back.