U.S. clean energy investments: 2025 Quarter 3 analysis

Billions of dollars in federal investments, including tax credits and funds authorized through legislation such as the Inflation Reduction Act and Bipartisan Infrastructure Law, have stimulated private investment in clean energy deployment. Now federal priorities are shifting, narrowing the federal incentives available for climate and clean energy investments. To deploy more innovative energy technologies for U.S. energy security, resilience, and growth, it is crucial to understand how shifts in federal policy and executive actions impact private investment. CATF’s new clean energy investment tracker is designed to do just that.

This tool tracks private investments that have been catalyzed by federal incentives and those that have been canceled while also tracking how changes to federal policy and executive actions impact the range of federal incentives available to projects. The data for this tracker comes from Rhodium’s Clean Investment Monitor combined with CATF’s data and analysis of federal incentives.

Federal incentives may be impacted by legislation and agency actions, which can limit project access to tax credits, grants, and loans. Where CATF has identified federal incentives as impacted by federal actions, the tracker labels project investments eligible for these incentives as “incentive eligibility impacted” (see top dashboard and status filter for investment totals for this label, and project details showing impacted incentives when selecting a project on the tracker to learn more). This label does not mean a project will not move forward, but that federal support is being withheld in some way. This information is essential to understand how federal activities impact private investments.

What’s impacting investments this quarter?

Federal legislation

Through the enactment of the One Big Beautiful Bill Act (OBBBA) in July 2025, many clean energy tax credits were repealed or narrowed by new restrictions and/or accelerated phasedowns. The table below summarizes key changes to the tax credits:

| Tax Credit | Key Changes |

|---|---|

| 45Q Carbon Sequestration | Enhanced Oil Recovery parity included. No change to credit value. Foreign Entity Of Concern (FEOC) restrictions added. |

| 45X Advanced Manufacturing | ‘Stackability’ of integrated components preserved. Wind energy component eligibility terminated for anything produced or sold after December 31, 2027. New subsidy for production of metallurgical coal suitable for steel production. FEOC restrictions added. |

| 45V Clean Hydrogen Credit | Available until January 1, 2028 (previously available until January 1, 2033). |

| 45U Existing Nuclear Credit | Retained for existing nuclear facilities through December 31, 2032. FEOC restrictions added. |

| 45Y Technology Neutral Clean Electricity Credit – Production Tax Credit (PTC) | Terminated for wind and solar facilities placed in service after December 31, 2027. Clean firm technologies eligible for full credit through 2032, followed by a multi-year phaseout. FEOC restrictions added. Wind and solar leasing agreements are not eligible for the credit. |

| 48E Technology Neutral Clean Electricity Credit – Investment Tax Credit (ITC) | Terminated for qualified facilities placed in service after December 31, 2027. FEOC restrictions added. Wind and solar leasing agreements are not eligible for the credit. |

| 45Z Biofuels Credit | Credit extended to December 31, 2029. Special rates for SAF eliminated. Required feedstocks to be from the U.S., Canada, or Mexico. FEOC restrictions added. Eliminated induced land use change contribution to carbon intensity. |

| 48C Advanced Energy Project Credit | If certification is revoked for a project or if a credit is not expanded, that credit amount cannot be reallocated. |

| 30C Alternative Fuel Vehicle Refueling Property Credit* | Terminated after June 30, 2026. |

| 30D EV Credit* | Terminated after September 30, 2025. |

| 25E Used Clean Vehicle Credit* | Terminated after September 30, 2025. |

| 45W Commercial Clean Vehicle Credit* | Terminated after September 30, 2025. |

Executive actions

The following executive agency actions could limit access to many of these tax credits, depending how they are implemented.

Proposed EPA Rule: Reconsideration of the Greenhouse Gas Reporting Program (GHGRP). On September 12, 2025, EPA proposed to permanently remove program reporting obligations for 46 of 47 source categories of the GHGRP. EPA’s proposal also includes permanently removing the natural gas distribution segment of the petroleum and natural gas source category (subpart W) and suspending reporting of the remaining nine subpart W segments until reporting year 2034. The Treasury Department and IRS rely on the GHGRP to administer Section 45Q Carbon Sequestration Tax Credits, Section 45V Clean Hydrogen Tax Credits, and Section 45Y Clean Electricity Tax Credits. Revising the GHGRP as proposed could hinder compliance with tax credit reporting requirements reliant on GHGRP data, and therefore the ability to claim the credits, unless IRS regulations are revised, and/or sufficient alternatives for measurement, reporting, and verification (MRV) and lifecycle analysis (LCA) are implemented.

Prohibited Foreign Entities (PFE)/Foreign Entity of Concern (FEOC) provisions. FEOC is shorthand for a type of tax provision that restricts entities with ties to certain countries considered national security threats from claiming or otherwise benefiting from federal clean energy tax credits. Previously, the IRA applied FEOC restrictions only to the 30D clean vehicle credit. OBBBA expanded upon IRA’s FEOC definition and created two new categories of Prohibited Foreign Entities (PFEs): (1) Specified Foreign Entities and (2) Foreign Influenced Entities. PFE/FEOC restrictions added by OBBBA apply to six energy tax credits: 45U, 45Y, 48E, 45X, 45Q, and 45Z, increasing compliance burdens and impacting projects claiming those credits, including enhanced geothermal and advanced nuclear. Treasury and IRS have yet to publish implementation guidance, contributing to industry uncertainty on compliance. A recent market analysis found that industry preparation is underway, but only 38% of firms surveyed describe themselves as “fully prepared” to comply with PFE/FEOC rules for 2026.

DOE announced project funding cuts and additional cuts being considered for existing awards. DOE canceled federal cost-share funding for hundreds of existing grant awards. In May and early October, DOE announced it was rescinding awards (grants and loans). Another leaked list, yet unconfirmed by DOE, was reported later in October. These nationwide funding cuts impact industrial and transportation sectors, near-term infrastructure deployment of solar and wind and grid resiliency projects, as well as methane pollution reduction investments. It is currently unknown which projects will ultimately proceed without the relied upon federal cost-share from DOE. Private sector and state level cost-share investments into these projects also face risk.

Findings

The majority of federal incentives driving private investments are impacted by recent federal activities, including OBBBA tax credit provisions, uncertainty in Treasury’s approach to PFE/FEOC implementation, EPA’s proposed GHGRP rollback, and DOE’s announced and reported cancellations of funding.

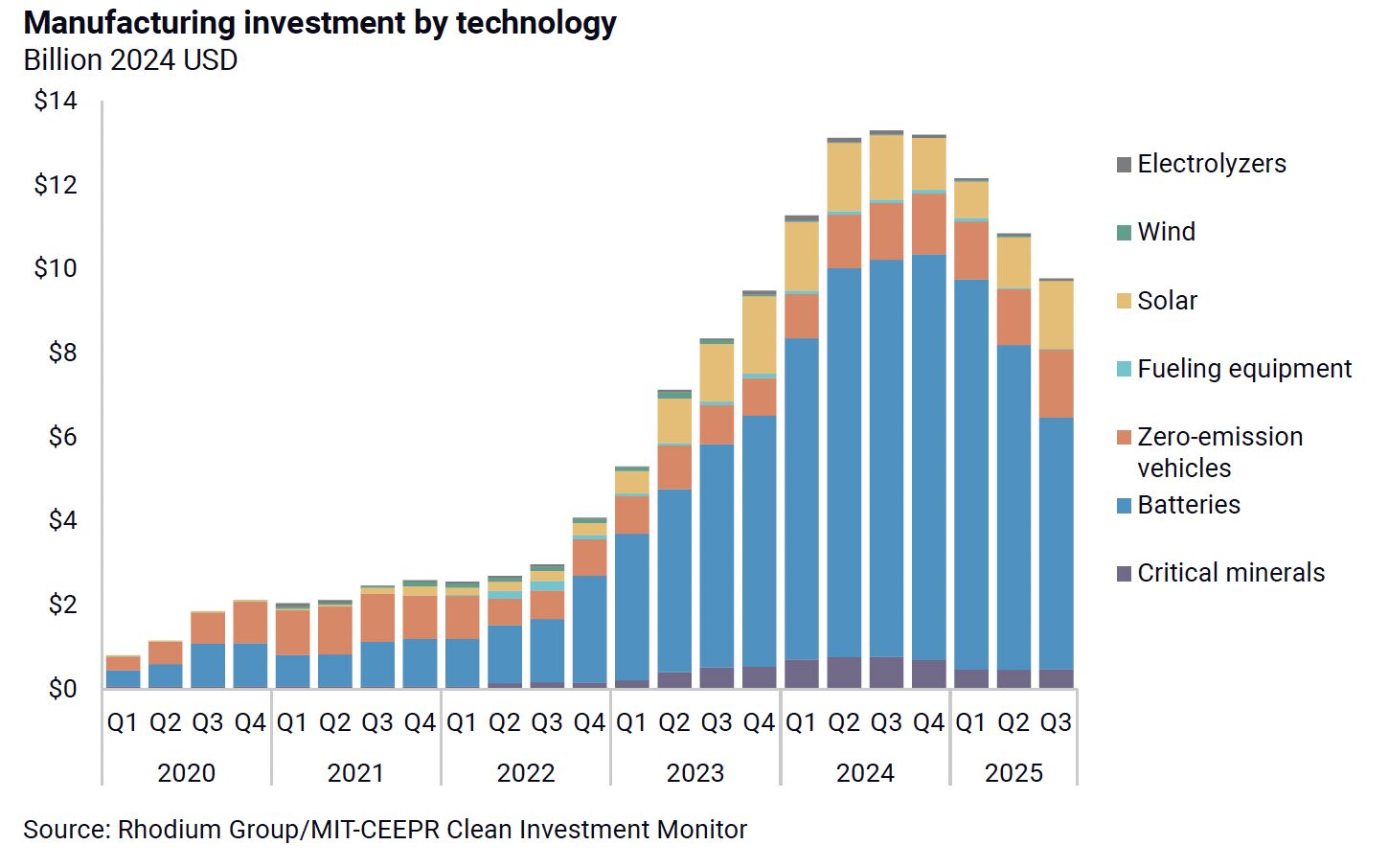

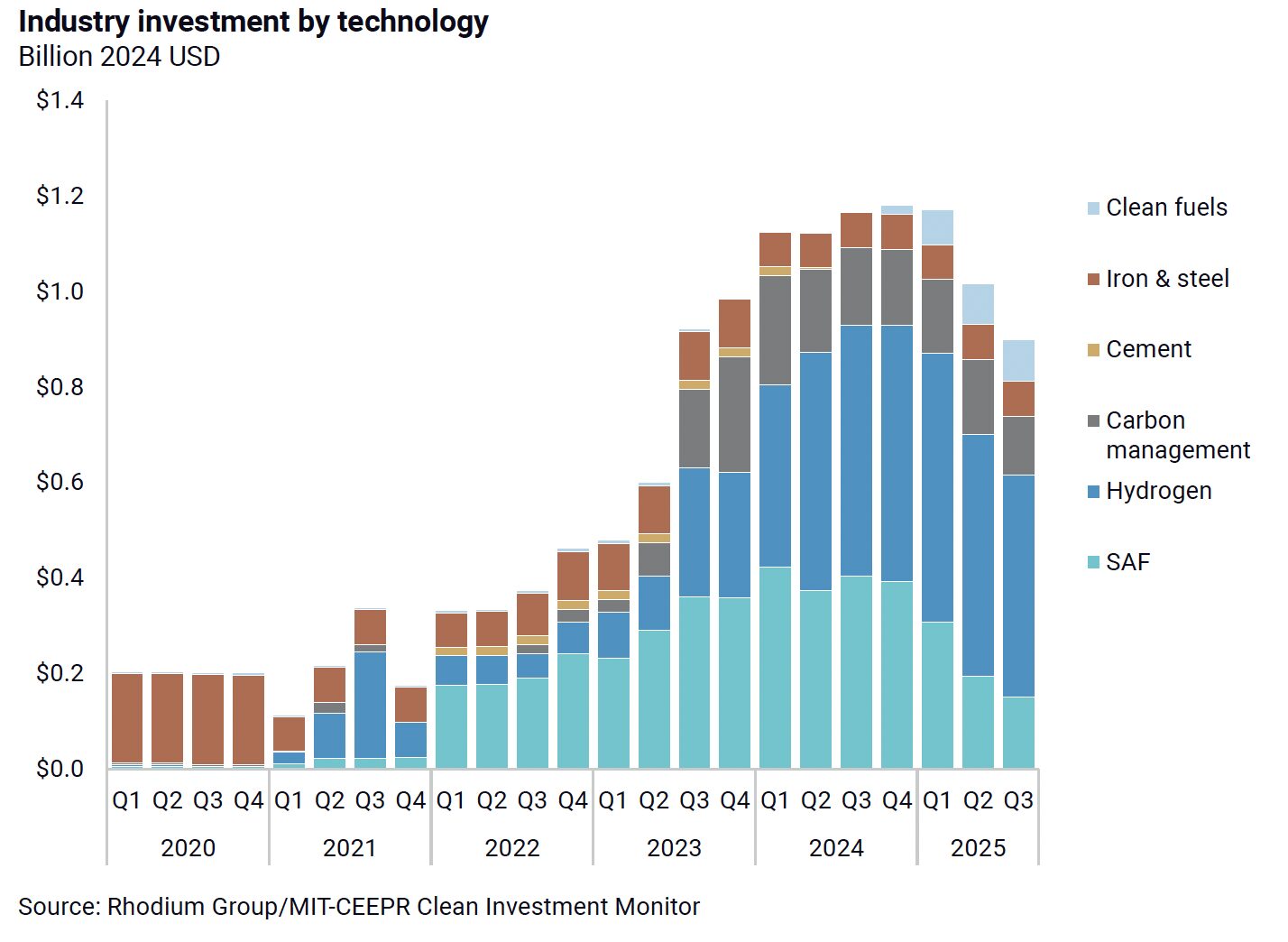

Sectors impacted by these federal actions include electric power, manufacturing, and energy and industry, which include transportation throughout. In Q3 2025, new manufacturing investment totaled $10 billion in actual investment and project cancellations totaled $2 billion, mostly from the cancellation of battery manufacturing projects. New energy and industry sector investment totaled $25 billion in actual investment in Q3, and project cancellations totaled $2 billion, primarily solar, storage, and hydrogen projects.

Read on for a few sector snapshots of how federal activities are currently impacting investments.

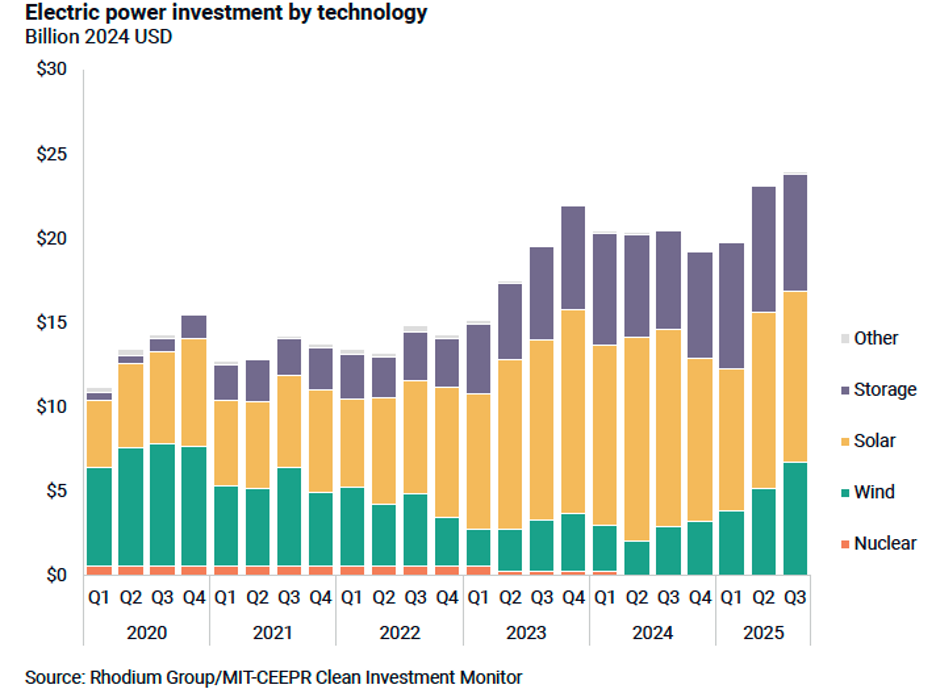

Electric power

Solar and wind

Utility-scale solar, together with storage installations, accounted for most clean electricity investments, and wind investments increased over 30% from the previous quarter. This is partly driven by projects accelerating timelines to fit within narrowed eligibility timelines, which is accelerating timelines, distorting supply chains, and raising costs but not driving new projects. However, recent federal actions are driving deep uncertainty for these industries with still unknown consequences for private investments in solar and wind. In particular, OBBBA narrows the time horizons for wind and solar projects (to commence construction by July 4, 2026, or be placed in service by December 31, 2027) to access the 45Y and 48E tax credits, eliminates eligibility for wind components sold after December 31, 2027 for 45X tax credit access, and creates uncertainty related to PFE/FEOC implementation. Uncertainty in solar investment will also have implications for battery investment and deployment, even if incentives for battery technologies remain largely intact.

Additionally, while most solar and wind projects are on private land, they can be sited on federal lands or otherwise require federal permits. Recent executive actions, such as the U.S. Department of the Interior Secretary’s Order prioritizing permits based on an energy project’s capacity density and the requirements for the Secretary of the Interior to personally sign off on solar and wind projects on federal lands could severely limit the solar and wind sectors’ ability to secure necessary permits. The administration has also taken several steps to slow or stop the development of offshore wind projects, which require federal approvals as they are sited in federal waters. The administration issued a halt on project approvals – a move a federal judge recently deemed unlawful – and has issued stop work orders on projects already under construction. These tax credit and permitting uncertainties upend the federal policy environment for solar and wind projects.

Looking ahead

DOE’s October project cuts announcement and additional project awards being considered for termination will likely affect wind and solar investments. EPA recently terminated the $7 billion Solar for All program within the Greenhouse Gas Reduction Fund. These cuts are a withdrawal of federal support for communities across the country that applied for and received funding support to invest in these technologies.

Fueling equipment and zero emission vehicles

While zero emission vehicle supply chains drove manufacturing investments in Q3 2025, these investment numbers were likely tied to investors taking action prior to the September 30, 2025, termination of 30D Clean Vehicle, 25E Previously-Owned Clean Vehicle, and 45W Commercial Clean Vehicle tax credits. OBBBA’s PFE/FEOC restrictions apply to the 45Y, 48E, and 45X tax credits that incentivize investment in the EV manufacturing supply chain – including critical minerals and batteries – creating investment uncertainty in those sectors while the industry waits for Treasury to release guidance that explains how they are implementing FEOC restrictions. The additional narrowing of the 48C Advanced Energy Project credit and the June 30, 2026, termination of the 30C Alternative Fuel Vehicle Refueling Property credit creates further uncertainty for future investments in fuel fabrication, fueling equipment, and EVs.

Separately, the administration continues to withdraw federal support for zero-emission vehicles and charging infrastructure. In addition to actions earlier this year to delay the release of funds for EV charging stations, the October DOE project cancellations further target EV supply chains for producing low-carbon fuels, building EV charging and freight corridors, and electrifying heavy-duty and public transit fleets.

Energy and industry

Sustainable aviation fuel

Investment in sustainable aviation fuel (SAF) technology continued to decline in Q3 2025. While OBBBA extended the 45Z tax credit through 2029, it dramatically reduced the maximum per-gallon credit value available to SAF producers from $1.75/gallon to $1.00/gallon, limiting the incentive for domestic investment in new or expanded SAF facilities. OBBBA also amended 45Z to require feedstocks to be from the U.S., Canada, or Mexico. The SAF industry had been positioned to expand, but these changes create new uncertainties for the domestic SAF industry.

Hydrogen

Q3 2025 hydrogen investments also declined from Q2, but hydrogen investments still comprised the majority of industry sector announcements. Subsequent quarters are likely to illustrate more of the impacts from recent federal actions, such as the OBBBA’s 45V Clean Hydrogen Credit phasedown (terminating the credit for projects that begin construction after December 31, 2027, instead of the original phaseout in 2033).

EPA’s proposed rollback of the GHGRP could impact the ability of carbon-based hydrogen projects to claim 45Q or 45V, and hydrogen projects seeking to claim 45V. The proposed delay of subpart W until reporting year 2034 would negatively impact the ability of taxpayers to receive higher incentives for better performance (i.e. lower-emissions hydrogen production) and potentially render some projects uneconomical. Carbon-based hydrogen projects can opt to claim either 45V or 45Q Carbon Sequestration tax credits; if the GHGRP is rolled back and data from subpart W is no longer available, 45Q may be the better route, but 45Q also relies on GHGRP to verify tax credit eligibility.

DOE’s announced hydrogen funding cuts in October, and the additional cuts being considered, are destabilizing for the U.S. hydrogen sector and may further alter 2025 Q4 investment data for the hydrogen sector. The announced cuts and additional cuts under consideration include eliminating federal cost share for all of the Regional Clean Hydrogen Hubs as well as 76 other hydrogen projects that support the buildout of a domestic hydrogen industry. It is unclear if projects will be able to move forward without federal cost share; at least one Hydrogen Hub announced it would pause activities in response to recent changes, including DOE’s decision to cut federal funding. Exxon announced it was halting plans for its blue hydrogen facility in Baytown, Texas – a project selected to receive up to ~$322 million in federal-cost share from DOE that was terminated in the spring.

Carbon management

Q3 2025 carbon management investments were slightly lower than Q2 levels. While OBBBA maintained the 45Q Carbon Sequestration tax credit and even included parity for enhanced oil recovery, other recent federal actions, including EPA’s proposed GHGRP rollback and DOE project cuts, have contributed to industry investment uncertainty.

Recent reporting indicates that Treasury and the IRS plan to issue guidance by the end of 2025 to clarify how taxpayers can verify their projects by an independent engineer or geologist to meet the 45Q credit requirement for tax year 2025. Until that guidance is finalized, there will be no way for taxpayers to substantiate 45Q claims if the GHGRP is eliminated.

Federal incentives have helped launch a new wave of carbon management investment in key industrial sectors, including refining, chemicals, steam methane reforming, steel, and cement. However, DOE’s October project cancellations included a major portion of their carbon management portfolio, including coal, natural gas, and power sector demonstrations; FEED studies; point-source capture pilots; and direct air capture (DAC) hubs. These DOE actions may impact Q4 2025 investment data and beyond if CCS and carbon removal developers validate equipment and deploy projects abroad rather than at U.S. facilities. In an example that may shed light on Q4 2025 investment data, U.S.-based startup Carbon Capture Inc. announced it was relocating the company’s first commercial DAC pilot project from Arizona to Alberta, Canada due to better incentives and a more stable regulatory environment and citing DOE’s project cancellations. Check back next quarter to see how federal and executive actions have impacted projects across the U.S. and visit the clean energy investment tracker here.