Key insights on EU CO₂ transport and storage costs from CATF’s new interactive tool

In response to rising carbon prices and national and corporate climate goals, many of Europe’s energy-intensive industrial sites are urgently looking for ways to permanently store their CO2 emissions deep underground. While many geological CO2 storage projects are now at various stages of development, transporting captured CO2 to these locations is not straight-forward for every emitting industrial facility. Identifying the lowest-cost and quickly deployable means of getting CO2 to storage from among a wide range of transport options can prove especially challenging. Clean Air Task Force’s new interactive tool provides insights on this challenge by estimating the cost of transporting and storing CO2 from large industrial emitters in Europe, across multiple transport modes (pipeline, ship, rail, and barge), and under two different storage deployment scenarios.

How the tool works

This new tool incorporates a detailed cost model developed through research led by ETH Zurich, which is applied to CATF’s geospatial network modeling of the most viable pathways linking each emissions source and possible storage sites or CO2 export terminals. For new CO2 pipelines, these pathways are weighted towards existing pipeline rights-of-way, while rail and barge routes follow existing rail networks and navigable inland waterways. Over 1,200 large emitters (over 100,000 tCO2/year) in heavy industry and waste management sectors are evaluated, based on publicly available emissions data from the EU, Norway, and the UK.

In the Planned Storage scenario, only announced large-scale CO2 storage sites are considered – most of which are in offshore locations around the North Sea and in the Mediterranean. The Widespread Storage scenario introduces a wide variety of other possible storage sites, including several onshore locations across Europe, based on smaller announced projects and national studies identifying areas with potentially suitable geology. The tool allows the user to highlight which emitters meet a given cost threshold or use a particular mode of transport in the lowest-cost case. Users can also filter by industrial sector or country for more focused analysis. Given non-cost challenges and longer lead-times facing pipeline deployment in some regions, it is also possible to exclude pipelines from the transport options considered.

Running the numbers: Early insights from putting the tool to work

Under the Planned Storage scenario, limited and mostly offshore storage options make transport and storage costly without pipelines.

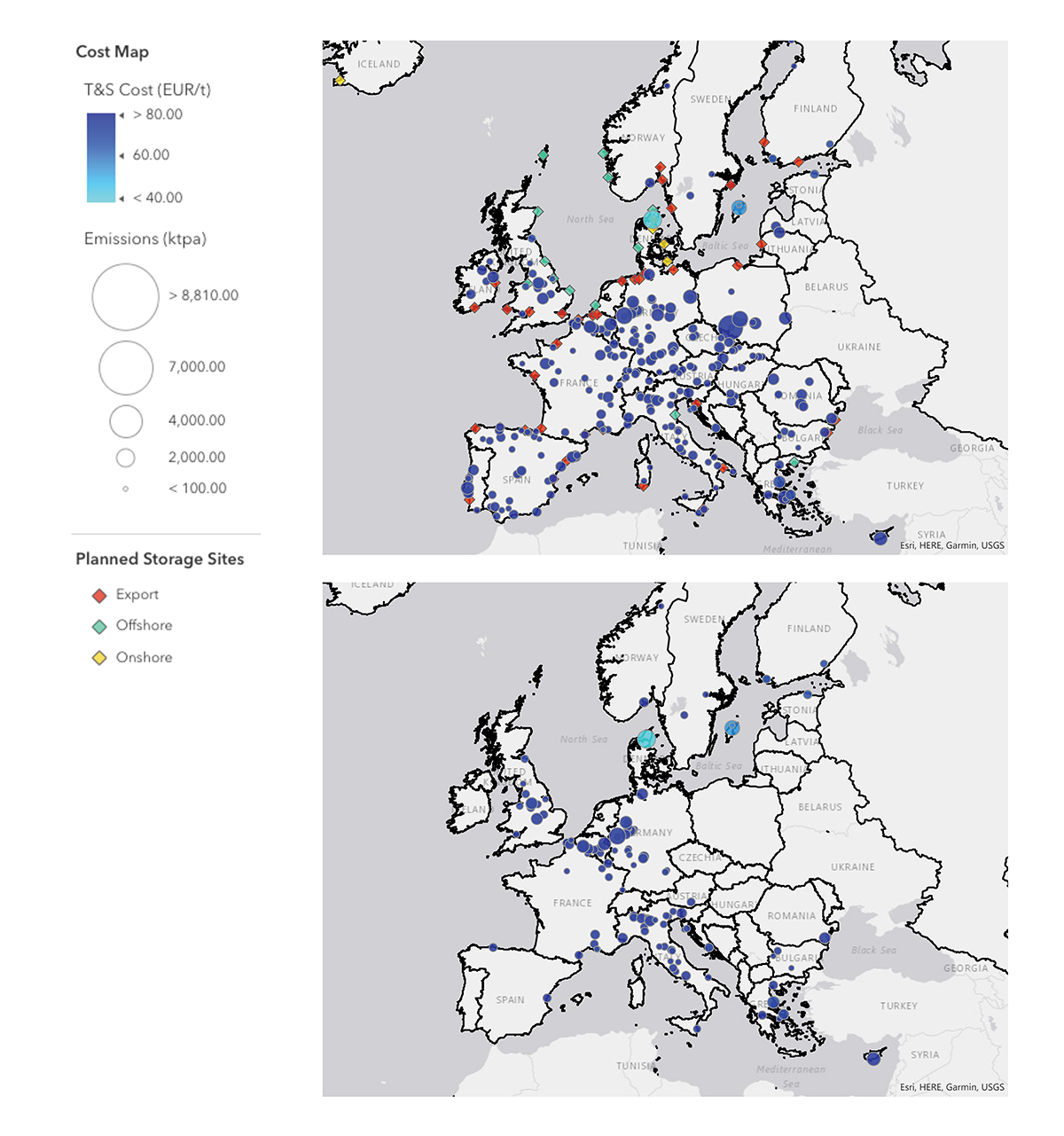

Figure 1. Top: 279 cement and lime plants (blue circles) assessed in the cost tool under a ‘Planned Storage – no pipelines’ scenario, shown with offshore and onshore storage sites and CO2 export points. Bottom: The 117 facilities reaching costs of under €100/t in this scenario.

The example output in Figure 1 shows 279 cement and lime plants assessed under the Planned Storage scenario, together with the identified offshore storage, onshore storage, and export hubs. In this ‘highest cost’ scenario, with pipeline transport excluded, transport and storage costs range from €34/tCO2 to as high as €209/tCO2, with a median cost of €106/t. These high costs reflect the fact that most currently planned storage sites are offshore – which comes at a cost premium – and concentrated in a few areas, making them expensive to reach by dedicated rail, barge, or ship connection from many parts of Europe. Only 42% of the cement and lime plants manage to reach transport and storage costs of below €100/t, and these are largely close to the North Sea and Mediterranean storage sites or on inland waterways that allow barge access to Rotterdam (Figure 1). A few large, coastal emitters are also able to make this threshold, and inland facilities with access to Denmark’s planned onshore storage sites benefit from the lower costs.

Figure 2. The 79% of cement and lime plants which face costs of less than €100/t when CO2 pipelines are enabled.

Allowing pipeline deployment for this sector lowers the costs significantly, particularly for facilities which are relatively close to storage sites and within industrial cluster regions. Now, 79% plants face estimated transport and storage costs of less than €100/t (Figure 2). However, pipeline costs vary linearly with distance, while rail costs depend largely on the volume transported, so longer pipeline routes can still face high costs. Pipeline costs per tonne CO2 also increase significantly when small volumes are transported, meaning many isolated, small emitters still favour rail in this scenario. In many parts of Europe, CO2 pipelines are likely to be built to be shared by several emitters in many parts of Europe, and plans for such networks are well underway. The tool accounts for this by applying spatial statistics to identify regions with high concentrations of industrial emitters; in these areas, even smaller emitters are allowed to harness economies of scale and assume the use of pipelines of at least 1 Mtpa in size.

In the Widespread Storage scenario, expanding onshore storage options dramatically cuts transport and storage costs.

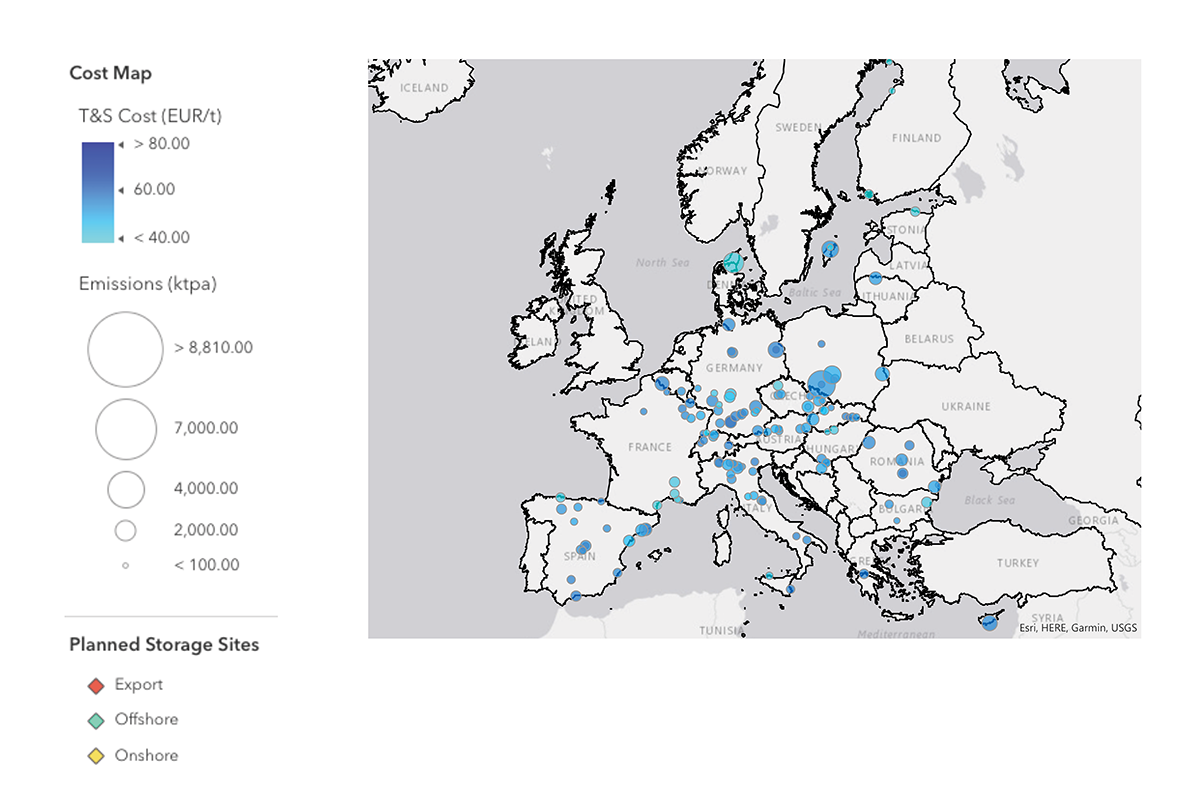

Figure 3. In the Widespread Storage scenario, 50% of cement and lime plants reach costs of under €60/t, when excluding pipeline transport.

The most significant cost reductions are obtained in the Widespread Storage map, which is shown for the same cement and lime sector facilities in Figure 3. Nearly all the plants now come in at under €100/t, and 50% benefit from costs under €60/t. Allowing the use of pipelines puts 90% of plants under this €60/t threshold, with a median cost of €38/t. For some Member States, including Austria, Germany, and Poland, developing the onshore storage considered in this scenario will require regulatory changes, which in some cases are already well underway. However, it is important to note that there is significant uncertainty around the true potential of certain geological areas where limited data is currently available, and a more accurate picture will rely on dedicated characterisation efforts. While onshore storage presents different challenges to offshore developments, frontrunner projects such as the Denmark’s onshore licences and Hungary’s Danube Removals project are showing that it is a viable option for Europe.

The cost tool clearly highlights the marked cost benefit that more widespread storage can bring, due to the inherent reduction in CO2 transport distances and the usually lower cost of subsurface work in an onshore environment. On the other hand, offshore projects in the North Sea and Mediterranean often promise very large total capacities and are at a relatively advanced stage of development.

Industrial clusters and multimodality should guide infrastructure planning and development

It is clear that large pipeline networks will likely be needed to link Europe’s emissions intensive industrial heartlands to large storage hubs at an affordable cost. Identifying regions and industrial clusters that could support Europe’s CO2 backbone is the first step in prioritising where pipeline infrastructure should be developed. Spatial clustering analysis from the tool indicates that about 50% of Europe’s cement and lime facilities are located in ‘industrial corridors’ – areas with significant concentration of industrial facilities; for other sectors, clustering is even more pronounced: about 75% of chemical plants are contained in industrial corridors. These clusters could serve as important first-mover nodes with trunklines to activate a wider CCS pipeline network.

A broader CO2 infrastructure system would need to integrate pipelines with other transport modes. A multimodal CO2 transport network provides facilities with a wider set of options to reach storage, enabling scale economies and competition to reduce unit transport costs, enhancing network resilience and, in certain cases, allowing for the reuse and redevelopment of existing assets such as ports. There is emerging consensus that a flexible and multimodal CO2 transport system should guide infrastructure planning and development. Results from the tool indicate non-pipeline options are expected to be the lowest cost for nearly 20% and 14% of industrial emitters across the Planned and Widespread Storage scenarios respectively, even when pipeline development is allowed. Ensuring multimodality will require harmonised regulatory frameworks that ensure open access and cross-border interoperability, coordinated infrastructure planning, and additional incentives to derisk infrastructure investments.

Reality check

This tool is intended to provide an overview of the cost challenges facing some of Europe’s industries as they look to decarbonise through carbon capture and storage, as well as highlight the potential for more rational deployment of transport and storage infrastructure to bring about significant cost savings. A detailed cost assessment of CO2 transportation will be highly case specific and depend on numerous local factors such as the ability to reuse pipelines, rail and port terminals, and offshore infrastructure. Depending on how CO2 transport services are regulated, capture projects may incur a non-discriminatory network usage cost rather than a cost which varies with distance.

The costs derived by the tool may appear high for many emitters under the most likely near-term scenarios, which partly reflects the limited consideration of economies of scale through large, shared pipeline infrastructure, but also the recent high inflationary period and a generally conservative choice of cost estimates. However, the results are also in broad agreement with early indicators from frontrunner transport and storage services and initial feedback from industry. To help bring down these costs and establish a resilient transport network, EU and Member State policy should:

- Focus on accelerating storage site development in new, emissions-intensive regions;

- Develop a regulatory framework and deployment plan for cross-border pipeline networks and multimodal infrastructure; and

- Coordinate and de-risk investment in shared infrastructure such as CO2 trunklines and shipping terminals.

CATF intends to continue updating and improving the CO2 transport and storage cost tool, and welcomes further input from stakeholders and researchers in the sector.