H.R. 1 expands 45Z clean fuel production credit for conventional biofuels while cutting sustainable aviation fuel tax credit

H.R. 1, the so-called “One Big Beautiful Bill” Act (OBBBA), enacted on July 4, 2025, expands the 45Z Clean Fuel Production Credit (45Z) by extending it through 2029 and loosening eligibility requirements associated with transportation fuels’ carbon intensity (CI). Simultaneously, amendments to the 45Z credit within H.R. 1 dramatically reduce the maximum per-gallon credit value available to sustainable aviation fuel (SAF) producers: from $1.75/gallon to $1.00/gallon. Together, these and other changes to 45Z are expected to: (1) cost taxpayers $25.7 billion from FY25-34 (despite repealing the higher credit value for SAF), (2) expand tax credits for conventional biofuels that already benefit from other federal support and have limited greenhouse gas (GHG) emission reduction potential, and (3) limit federal incentives for domestic production of innovative fuels like SAF. 45Z as modified will not decrease GHG emissions of domestic fuel or promote production of domestic clean fuels.

Background

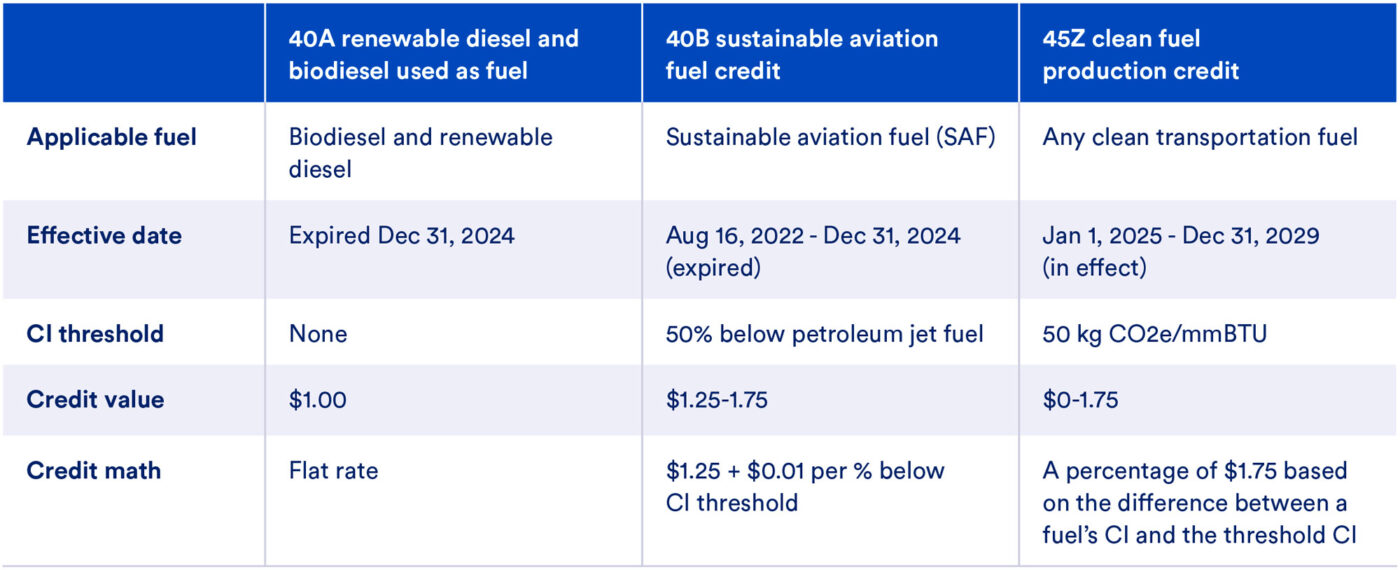

Congress created 45Z in the Inflation Reduction Act (IRA) of 2022. The IRA set the maximum credit value at $1.00/gallon for eligible clean fuels, which included those with a CI of less than 50 kg CO2e/mmBTU produced in calendar years 2025-2027. Additionally, SAF was granted a higher maximum credit value of $1.75/gallon. Congress also required the tax credit to be adjusted annually for inflation. Fuels that earned other tax credits, like 45V (hydrogen production) or 45Q (carbon sequestration), were not allowed to stack these credits with 45Z. When the IRA was passed, the Joint Committee on Taxation (JCT) estimated that the 45Z credit (in place from 2025-2027) would cost about $2.9 billion over FY25-28.

The IRA made other changes to federal biofuel tax credits, including eliminating the biomass-based diesel credit, the second-generation biofuel credit, and other alternative fuel tax credits with the intent of replacing them with the technology-neutral 45Z Clean Fuel Production Credit. In addition, the IRA created the standalone 40B SAF tax credit, available in calendar years 2023-2024 (i.e., the two-year period before 45Z became operative). Fuels that reduced lifecycle GHG emissions by at least 50% could earn a credit of $1.25/gallon, up to $1.75/gallon on a sliding scale for each percent reduction in GHG emissions. Beginning in 2025, 40B was folded into 45Z, maintaining the maximum rate for SAF of $1.75/gallon.

Table 1: IRA fuel tax credits

Significant H.R. 1 Amendments to 45Z

One of the most significant changes to 45Z within H.R. 1 is a provision excluding emissions associated with indirect land use change (ILUC) from a fuel’s CI score. Ignoring ILUC can decrease CI scores of certain land-intensive conventional biofuels like corn ethanol and soy biodiesel by ignoring up to 20-25 g CO2e/MJ, yielding higher per-gallon tax credits for these fuels. ILUC-related GHG emissions are generated from land use conversion (e.g., clearing grasslands or forests – releasing carbon in the process – to replace food production on lands converted to biofuel crops) and other market-mediated effects not directly related to the biofuel crop. ILUC-related GHG emissions of biofuels derived from feedstocks that do not require dedicated land, such as agricultural and forestry residues and wastes, or feedstocks that may improve land systems (e.g., winter crops on seasonally fallow land, perennials on marginal land) may be more favorable and may be indirectly affected by this change if it encourages the continued reliance on conventional biofuel feedstocks.

In addition, H.R. 1 stripped the special SAF rate of $1.75/gallon, dropping it to $1.00/gallon to match all other clean fuels. This modification limits the incentive for domestic investment in new or expanded SAF facilities. SAF is still expensive to produce, as it is a nascent industry, and requires more support than other clean fuels to reach commercial scale. Many SAF producers factored the $1.75/gallon credit value into their business models and are now facing serious risks to investment and production capacity with the newly lowered credit value. SAF production facilities are currently positioned in states ranging from California to Montana with expansion planned in the West, South, Northwest, and Midwest in coming years. However, it is not clear how much of the planned expansion will proceed, as project developers around the country reckon with these changes.

The Joint Committee on Taxation (JCT) estimated that the new 45Z, including H.R. 1 changes, will cost taxpayers $25.7 billion through its expiration in 2029. When the IRA was passed, JCT estimated that 45Z would cost about $2.9 billion over four years. The significant expansion in cost from the 2022 estimate to the 2025 estimate is not tied to an increase inpublic benefits (such as reduced emissions); rather, the order-of-magnitude increase in cost results from Congress’s decisions to weaken the law’s carbon accounting requirements and allow a broader set of conventional biofuel producers to claim the credit.

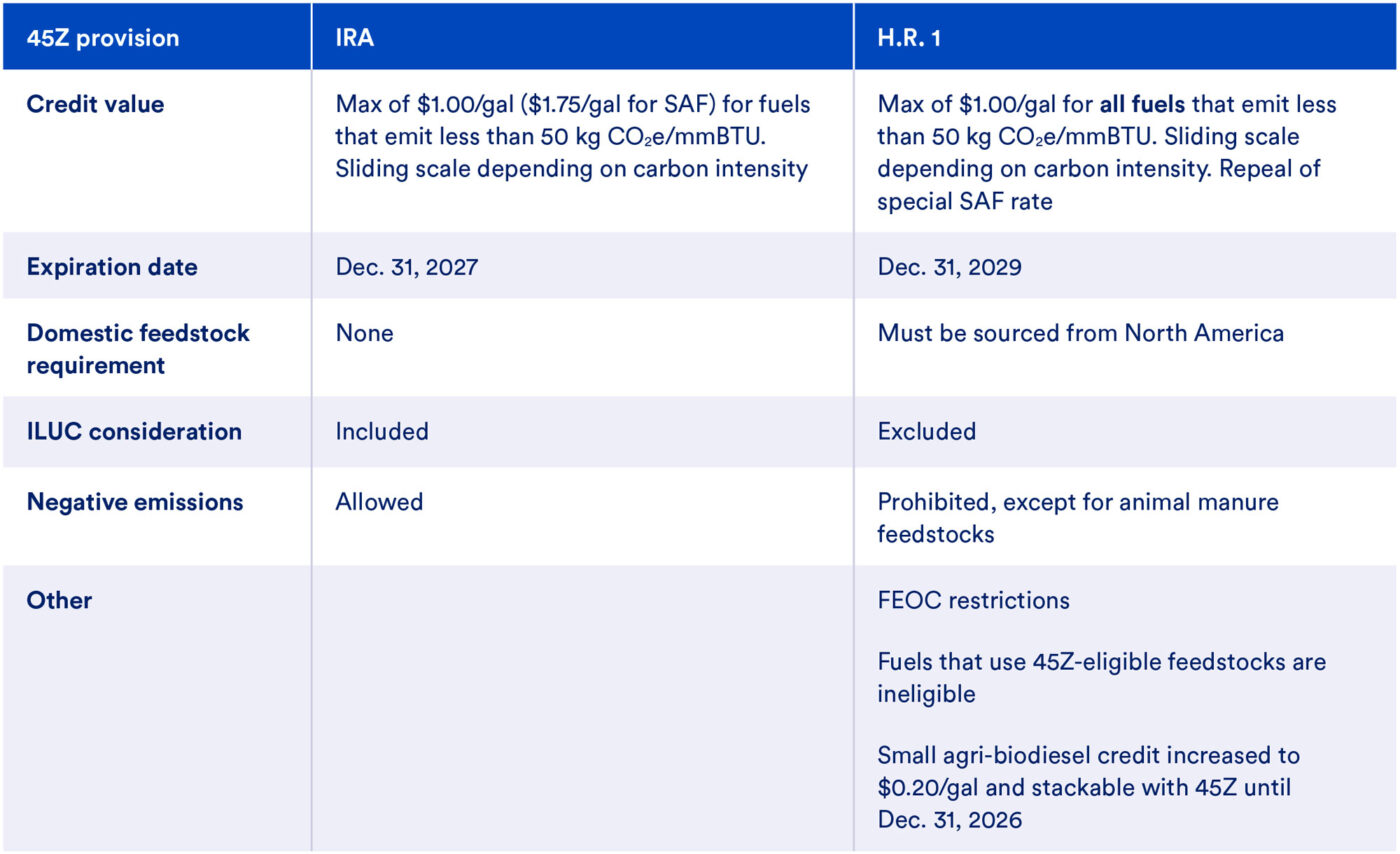

Table 2: Summary of 45Z modifications in H.R. 1 compared to the IRA

Impacts of 45Z Modifications

The changes made to 45Z will cost taxpayers more while undermining U.S. competitiveness, innovation, and climate progress.

H.R. 1 changes to 45Z will benefit:

- Domestic corn ethanol and soy biodiesel industries, with more gallons of current conventional biofuel production eligible for the tax credit at higher per-gallon tax credit rates compared to those under the IRA version of 45Z, mainly due to the new version’s directive against counting ILUC emissions. Increased production of corn ethanol and soy biodiesel could occur at the margin due to 45Z incentives, but domestic corn ethanol consumption growth is constrained by infrastructure, limited purchases of high-ethanol fuel blends, and flat or declining gasoline consumption nationwide. The corn ethanol industry could experience growth if domestic alcohol-to-jet (ATJ) fuel production scales, however the new 45Z disincentivizes this industry, which is still in early stages of development. Even without significant volumetric growth, these industries will benefit from higher per-gallon subsidies.

- Soy-based renewable diesel production is especially likely to benefit from higher per-gallon tax credits. As a mature and expanding industry, soy-based renewable diesel does not need taxpayer funding. Biodiesel and renewable diesel are also more expensive than diesel fuel, so unless oil prices increase significantly, production will likely be dictated largely by existing biofuel policies mandating a certain level of consumption each year, such as the federal Renewable Fuel Standard (RFS) and California’s Low Carbon Fuel Standard (LCFS), not by the availability of 45Z credits. As a result, taxpayer dollars are not actually needed to incentivize production of these fuels, making changes to 45Z a windfall for conventional biofuels.

H.R. 1 changes to 45Z will disadvantage:

- Taxpayers, since billions of dollars are expected to be spent annually on duplicative tax credits for carbon-intensive, mature biofuels that would be produced anyway under policies like the RFS and LCFS, which already mandate biofuel consumption. 45Z’s expansion and extension is unlikely on its own to spur additional job growth or economic investment in new production facilities nationwide.

- Industry investment in innovative fuel production, including companies investing in high-paying jobs across the country to produce fuels for growing markets such as SAF and fuels utilizing clean hydrogen to produce clean ammonia, methanol, etc.

- U.S. competitiveness and economic growth, since financial incentives will be shifted toward existing, mature industries like soy-based renewable diesel – an inefficient use of taxpayer dollars – instead of toward new, innovative fuels that generate significant economic growth, business investment, and international investment opportunities.

- U.S. positioning as a global leader in SAF production, because companies will likely shift planned SAF investments to other countries, given the decreased financial incentives for domestic SAF production and uncertainty around federal policy.

- Climate and environment, with less stringent carbon intensity reduction requirements for 45Z-eligible fuels and less funding directed at much-needed clean alternatives like SAF. The statute no longer requires consideration of the emissions resulting from the potential conversion of carbon-rich land like forests and wetlands which could occur withincreased corn- and soybean-based biofuel production. The production of conventional biofuels now subsidized by 45Z is also associated with worse water, air, and soil quality and diminished wildlife habitat.

Issues to Watch

With statutory changes to 45Z included in H.R. 1, the next step is for the U.S. Treasury and Internal Revenue Service (IRS) to issue new guidance relating to the implementation of those statutory changes. Some issues to watch over the coming months include:

- How the removal of ILUC considerations within 45Z carbon intensity scores will be implemented at Treasury/IRS.

- Whether and how Treasury/IRS or Argonne National Lab’s GREET model will incorporate certain farming methods (known as Climate Smart Agriculture, or CSA) such as no-till farming into CI scoring for 45Z. This is generally a way for biofuels to reduce their CI scores. There is a lot of uncertainty around the impacts of certain CSA practices, while others can be accurately estimated. Depending on the type of CSA practices that are credited, the implementation of those practices, and their incorporation into CI scores, the environmental benefits of biofuels could be improved or further eroded. Nothing in H.R. 1 authorizes Treasury to reduce a fuel’s carbon intensity score based on CSA practices. The biofuel industry has advocated for their broad inclusion in 45Z. CATF supports the inclusion of highly certain practices with quantifiable impacts, such as enhanced nitrogen efficiency fertilizers and reduced fertilizer use.

- Final Renewable Volume Obligations issued by the Environmental Protection Agency for calendar years 2026 and 2027, which will dictate U.S. biofuel consumption as part of the RFS mandate. In June 2025, EPA proposed significantly higher mandates for biomass-based diesel consumption for 2025 and 2026.

- Investment in clean, innovative fuels such as SAF, methanol, and ammonia with 45Z SAF tax credit maximum value reduced by 43% in H.R. 1. SAF production expansion announcements across the U.S. may also be affected by H.R. 1’s drastically shortened availability timeline for the 45V Clean Hydrogen Production Tax Credit.

U.S. fuels policy should support innovative fuels to reduce emissions and grow the U.S. economy. H.R. 1’s changes to 45Z fail to deliver either of those objectives. Instead, they will cost taxpayers billions to subsidize mature industries with limited public benefit.