Tripartite Contracting for Clean Electricity

Executive summary

Europe needs to accelerate clean energy deployment while simultaneously insulating customers from fossil fuel driven price volatility. Two major gas price crises over the last five years have increased European power prices despite rapid deployment of renewables and raised debates about power market design. While debates about re-designing power markets to reduce gas’s role as price-setter1 remain contested, financing clean energy and hedging customer costs via contracting serves as a market-based solution irrespective of market design.

Europe’s existing long-term contracting landscape is structurally inadequate for the scale of development and hedging necessary. Contracting enables clean energy development financing while also insulating the off-taker from market prices during the hours when the contracted project generates clean electricity. However, contracting today requires significant effort, expertise, and balance sheets that most industrial consumers do not possess. As such, Europe must act to increase the pace and volume of clean energy contracting and make it more accessible to customers.

To enable larger scale clean energy contracting, Europe must develop an easier, inclusive, and market-driven mechanism. The EU’s Affordable Energy Action Plan proposed the concept of tripartite contracts for affordable energy as a tool to deliver the dual outcome of deep decarbonisation and industrial competitiveness. At its core, a tripartite contract is a standardised three-way agreement between a clean energy supplier, a state-backed intermediary, and an industrial energy consumer. Presently, the European Commission facilitates two sectoral tripartite agreements for offshore wind and grids, and storage and is exploring the model for nuclear deployment.2

But Europe needs to think bigger about the role of tripartite contracting. Tripartite contracting has the potential to be a foundational mechanism that enables a larger scale of clean energy contracting. By simplifying contracting and solving for barriers to contracting, government-led tripartite frameworks can aggregate demand at volumes that drive down unit costs while locking in long-term price certainty for more customers. As such, Europe should develop larger scale tripartite mechanisms to enable broad clean energy development and contracting. Scaled strategically, this is not just a procurement tool but a demand-side accelerant that helps increase price stability for its consumers and industries.

This report examines how the implementation of tripartite contracting could deliver cost certainty, and hedge costs for customers.

A government-backed entity, acting as an intermediary market maker, absorbs counterparty credit risk, pools diverse generation technologies to resolve profile mismatch, lowers transaction and shaping costs, and aggregates demand to make participation viable for smaller operators. Beyond simply contract design, broader and periodic tripartite contracting results in large volumes of 24/7 carbon-free energy contracts that de-risk clean energy deployment, increased competition and market liquidity, and support for electricity storage and flexibility markets.

The forthcoming Electrification Action Plan, announced in the Clean Industrial Deal, is the immediate opportunity to embed tripartite contracting and support for contracts like Power Purchase Agreements (PPAs) at the centre of Europe’s industrial decarbonisation strategy.

In this analysis, CATF is setting out an implementation roadmap to bring the tripartite model to scale.

Key actions for an implementation roadmap include:

- Scaling tripartite from sectoral forums to a large-scale contracting mechanism. Today, tripartite agreements operate as coordination forums limited to a handful of technologies and sectors. European governments should recognise the broader opportunity: scaling tripartite contracts into a service that unlocks clean investment, and delivers hedging and firmed electricity portfolios for 24/7 clean power.

- Settling the design of the state-backed intermediary. The EU and Member States should agree whether the intermediary operates as a matching platform, market-maker, investment de-risker, or a combination — and establish the procurement, governance, and risk-allocation frameworks that follow from that choice.

- Strengthening long-term contracting across borders. Resolving outstanding PPA and Contracts for Difference (CfD) design questions and extending EIB guarantee programmes to clean firm generation are prerequisites for delivering 24/7 carbon free energy products. Risk-sharing mechanisms should be adapted for smaller industrial off-takers.

- Deploying pilot programmes to test the tripartite model with industrial facilities and clean energy suppliers. Lessons from these pilots—on procurement design, entity governance, and consumer participation—should be shared across Member States and fed back into the Commission’s framework development. Pilot programmes should be coordinated with proactive grid planning to ensure infrastructure capacity and grid connection is available.

1. The case for tripartite electricity contracts

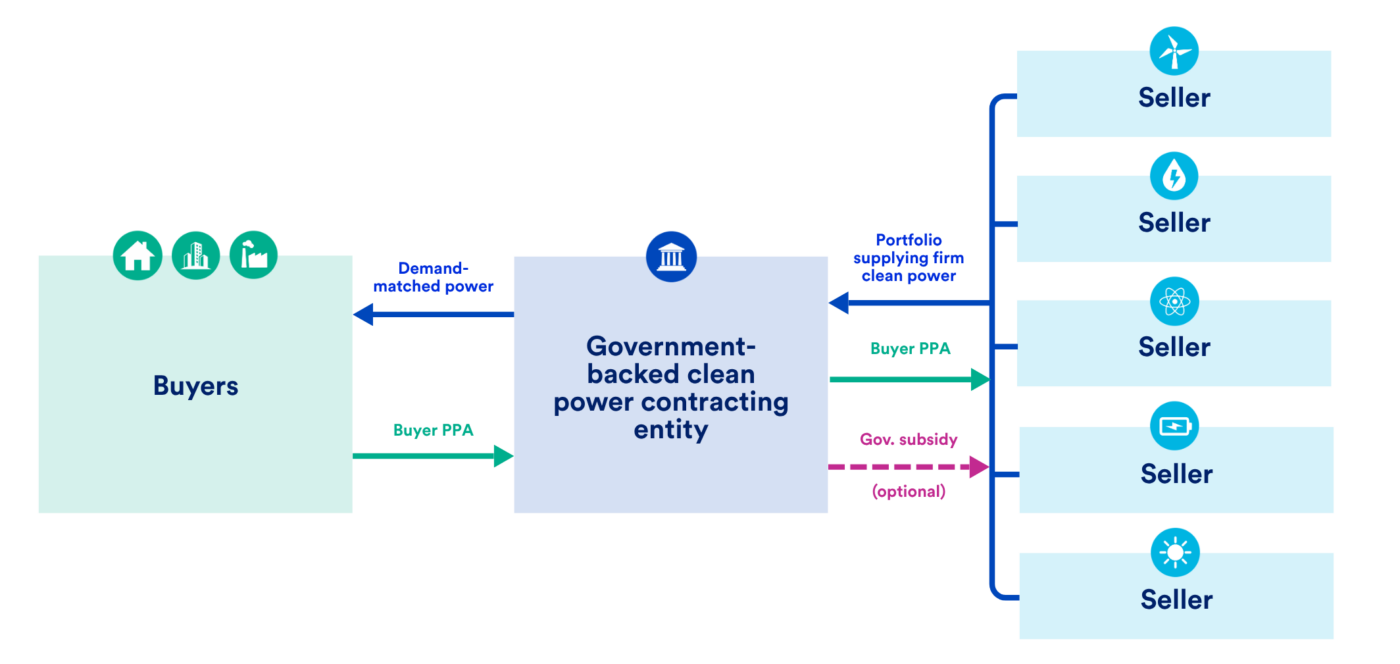

How the tripartite contract mechanism works: connecting two parties through a state-backed intermediary

A tripartite contract is, at its core, a three-way energy agreement between a clean energy supplier, a state-backed intermediary, and an industrial energy consumer. In contrast to a regular bilateral contract, where there is no state-backed intermediary, tripartite contracting is unique in that the state entity sits between the two market parties. The role of the state entity is a market-maker, to reduce the barriers for customers to contract clean energy while increasing the volume of contracting.

In the tripartite contracting mechanism, a state entity exists in between customers and suppliers to procure upstream clean power from developers through long-term contracts (typically CfDs), giving them the revenue certainty needed to invest; and downstream, it offers industrial consumers fixed, predictable pricing through shorter-term contracts (typically PPAs). This architecture enables a state-entity’s capacity, expertise, and creditworthiness to solve structural barriers that bilateral markets cannot resolve on their own.

From a process perspective, the tripartite mechanism would operate as follows. Industrial consumers and Member States first signal their demand and acceptable price parameters, establishing the procurement criteria. The intermediary then leads a competitive procurement process upstream — selecting generators through auction against those criteria. Once contracts are awarded, the central entity transfers structured, standardised electricity products downstream to consumers.

The Affordable Energy Action Plan proposed tripartite contracts to provide a contracting model for industries that cannot access standard PPAs and in parallel, support the bankability of clean energy projects. This approach contributes to developing market liquidity for long-term contracts, provides counterparty creditworthiness, improves hedging opportunities for consumers, and unlocks electrification investment for end-users.3

How the tripartite contracting mechanism works:

- Clean Power Contracting Platform: A state-backed entity sits between generators and industrial consumers, aggregating demand and supply, performing auction-based procurement, and managing risks while providing creditworthiness.

- Clean Energy Supply Procurement: Upstream, the entity procures clean power through long-term contracts (e.g. CfDs) to support development and financing of low-carbon energy and flexibility assets.

- Hedging Costs for Consumers: Downstream, the entity issues short to long-term contracts (e.g. PPAs, forward products) offering consumers price hedging and predictable electricity sourcing costs.

Figure 1: The structure of a tripartite contract.

2. Why tripartite contracting mechanisms matter for Europe

Europe’s existing long-term contracting landscape is structurally inadequate for the scale of its energy transition. Bilateral PPAs, the primary market mechanism, cover only a fraction of installed renewable and storage capacity, and at current pace will finance a small share of the investment needed by 2050. The barriers are compounding: industrial buyers are reluctant to lock in elevated prices over long horizons, renewable generation profiles rarely match consumption patterns, contract complexity excludes smaller firms, and creditworthiness requirements shut out most customers. Meanwhile, forward markets remain too illiquid to hedge the storage and flexibility assets essential for deep decarbonisation. The result is a contracting gap that leaves Europe’s power system over-exposed to spot markets and fossil fuel price shocks.

Tripartite contracting addresses these failures by inserting a state-backed intermediary between generators and industrial consumers. Upstream, the entity pools diverse generation technologies — renewables, storage, clean firm capacity, and demand response — into portfolios that can deliver shaped, firm clean power products that bilateral markets cannot replicate. Downstream, it issues shorter-maturity, competitively bid contracts with low minimum volumes, dramatically lowering entry barriers for smaller buyers. The intermediary absorbs counterparty credit risk through public guarantees, spreads shaping costs across a diversified portfolio, and generates transparent pricing data that can guide anticipatory grid investment. Scaled across Europe, this approach converts fragmented bilateral negotiation into a demand-side accelerant, aggregating volume, compressing costs, and severing industrial consumers’ exposure to the fossil fuel volatility that has defined Europe’s energy crisis era.

Volatile electricity markets hold back a competitive clean economy

Since 2022, European electricity prices remain structurally expensive, reflecting high gas prices and insufficient grid infrastructure.4 This is amplified by inadequate long-term contracting mechanisms, paired with high taxes and levies.

Following the escalation of conflict involving Iran in March 2026, European gas prices (Dutch TTF) averaged €45/MWh in the first week, coinciding with a rise of nearly 50% compared to pre-conflict levels of €31/MWh. As electricity prices remain coupled to gas prices through the merit order, the cost of gas-fired electricity generation across Europe surged by more than 50% in just ten days.5 The rise in fossil fuel prices in the first ten days of the conflict alone cost Europeans an estimated €2.5 billion compared to pre-conflict price levels.

The fundamental restructuring of Europe’s gas supply following the invasion of Ukraine in 2022 has created a new, higher-cost equilibrium due to the structural shift to LNG and has locked in higher gas prices. While LNG imports helped Europe diversify away from Russian pipeline gas, its concentration creates new strategic dependencies, reinforcing the imperative to reduce imported fossil gas in the European power system and accelerate the transition towards homegrown clean electricity generation.6

Expanding renewables, storage, and clean firm capacity progressively reduces gas price exposure

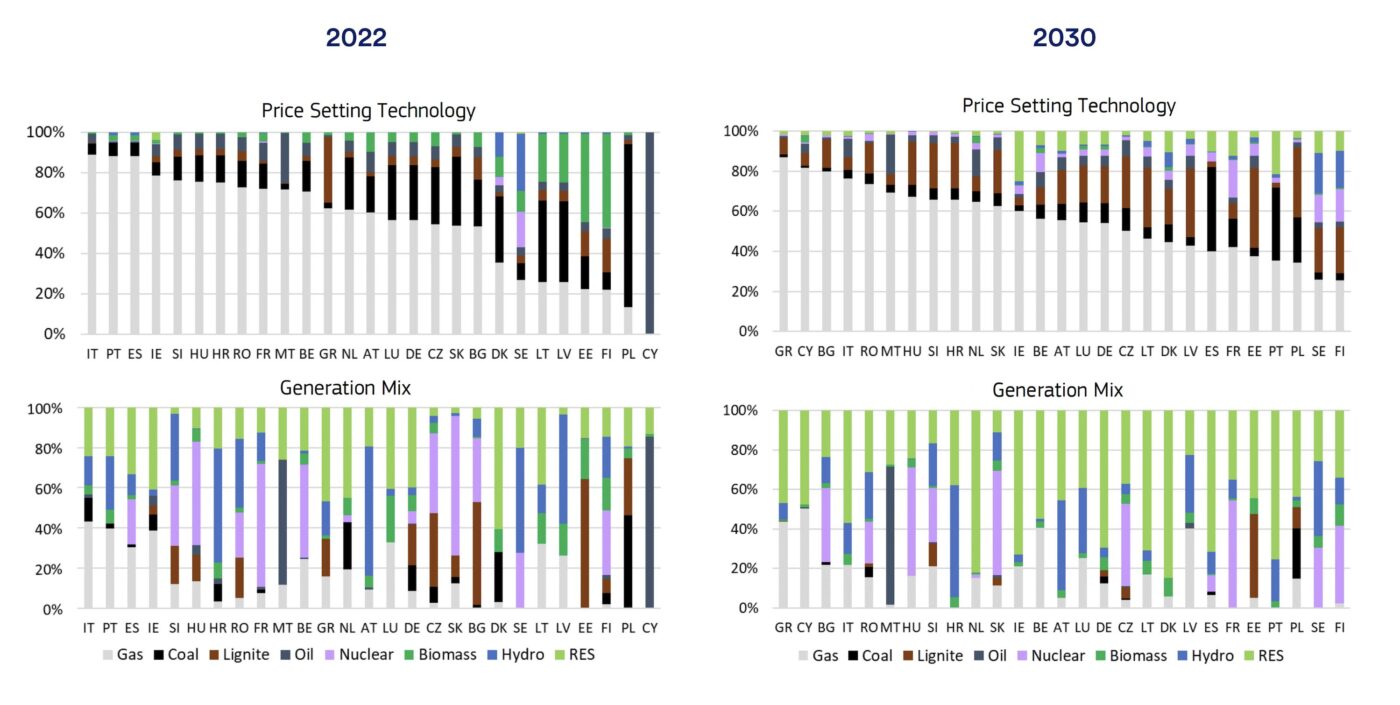

Currently, gas is representing only 20% of the EU’s electricity mix, but it set the marginal price 63% of the time during the 2022 energy crisis peak, a pattern forecasted to persist through 2030 even if renewable targets are met.7 Breaking this pattern requires rapid renewables deployment to meet rising energy demand as well as complementary deployment of storage and clean firm generation capacity — clean technologies that can generate on demand regardless of the weather — to replace gas in the hours renewables cannot cover.

Figure 2: Price-setting technology per EU country vs Generation Mix (METIS Simulation results)

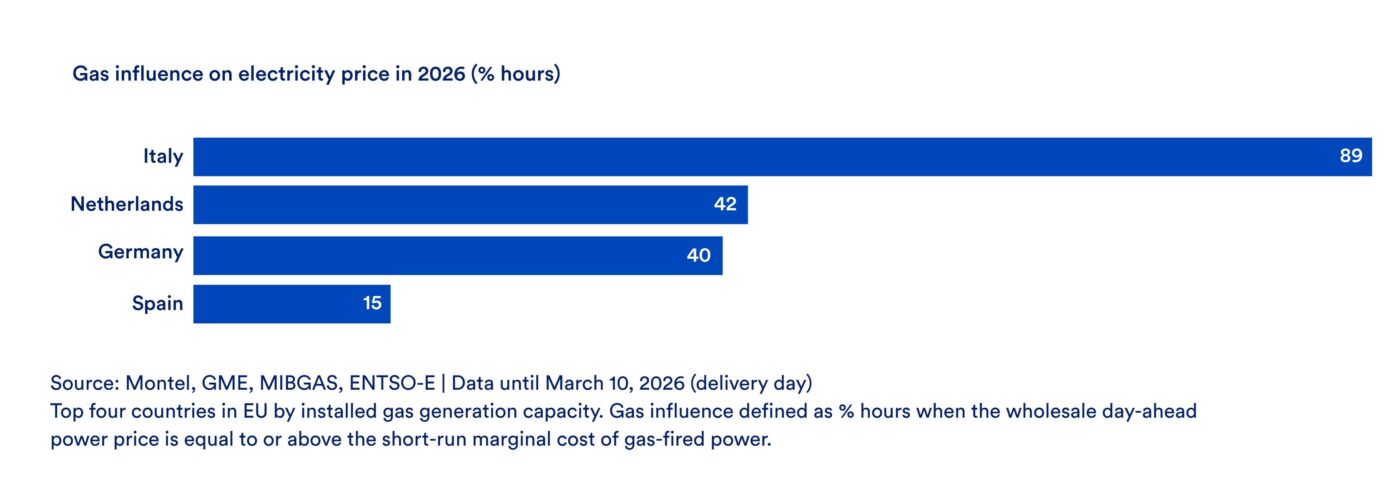

Europe’s excessive reliance on spot markets—both for gas procurement and electricity pricing—amplifies volatility, whilst concentration in gas derivative markets can exacerbate price swings.8 Countries that rely more on gas for power generation — such as Italy and Ireland — are in principle most affected by surging gas prices. In the first week of March 2026, power prices rose to their highest levels of the year in Germany, the Netherlands, Italy and Belgium, while less gas-reliant countries such as Spain, Portugal, France and the Nordics appeared less impacted.9

Figure 3: Gas influence on power prices varies by EU country

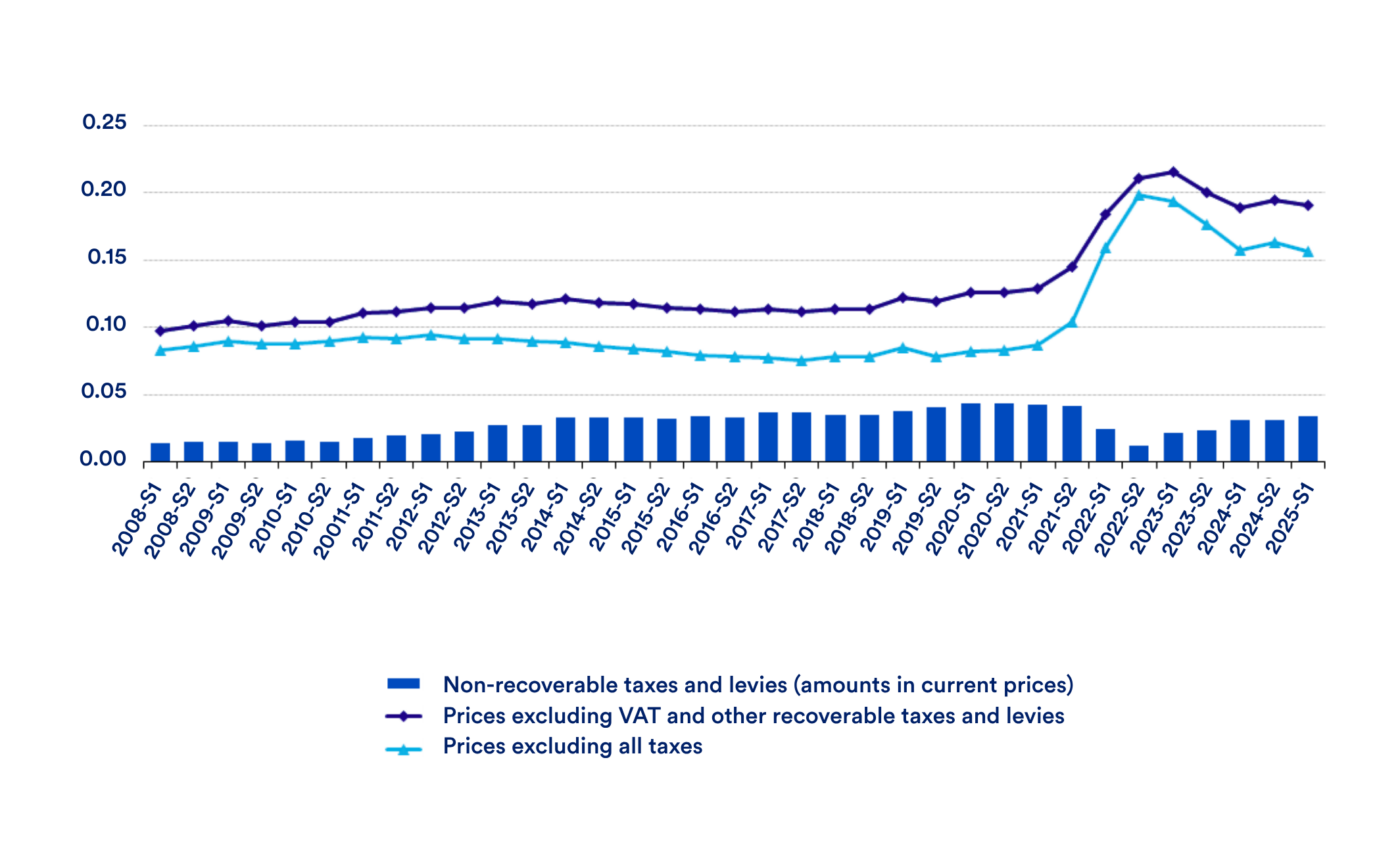

Figure 4: Development of electricity prices for non-household consumers, EU, 2008-2025 (€ per kWh)

While the grid remains a bottleneck for the energy transition, both the delay of supply connection and the growing network tariffs during infrastructure buildout exacerbate the affordability and competitiveness problem of electricity prices for industry and consumers in Europe. Grid congestion compounds the problem: over 12 TWh of renewable electricity was curtailed in the EU in 2023 due to inadequate grid capacity, causing 4.2 million tons of unnecessary CO₂ emissions.10 This curtailment not only wastes clean energy but also creates underperformance risks for electricity contracts and delays Europe’s decarbonisation goals. In order to address the urgent need for facilitated grid access and accelerated cross-border and national transmission and distribution grid deployment, the European Commission proposed a Grids package in December 2025, starting off a targeted revision of the Renewable Energy Directive, the Electricity Market framework, and the TEN-E Regulation.

Scaling and de-risking long-term contracts is a critical part of the solution

To scale a more electrified economy, generation and storage developers, conversely, require long-term revenue certainty to justify investment. While clean electricity generation developers seek long-duration contracts, buyers prefer shorter commitments due to potentially sustained high prices and limited predictability.11 This mismatch constrains liquidity in markets offering contract durations beyond three years and prevents investment in capital-intensive assets.12 Clean firm generation technologies—such as nuclear energy (including SMRs and advanced reactors), next-generation geothermal, and carbon capture—face commercialisation barriers including early-stage project costs, policy gaps, and exclusion from some clean energy incentive frameworks. To unlock the benefits of these technologies — namely of reduced infrastructure buildout needs and lower total decarbonisation costs— policies and markets must value their dispatchable attributes.

Without forward revenue commitments, developers face greater exposure to wholesale market volatility, which increases financing costs, deters investment, and ultimately threatens system adequacy. This requires policy interventions and developing market platforms to pool demand between generators and off-takers, combined with guarantee schemes (e.g., via EIB and National Banks), to mitigate counterparty risks and broaden access to SMEs.

One of the key reform recommendations of the Draghi report following the 2022/2023 crisis has been to promote bilateral long-term contracts to prevent wholesale markets from acting as amplifiers of price fluctuations. Broadly adopted long-term contracting would directly reduce the need for crisis-era public subsidy programmes, since industry would no longer be fully exposed to spot price volatility, and governments would not face political pressure to intervene with expensive and unsustainable relief measures. During the 2022 energy crisis, governments implemented electricity price revenue caps ranging from €40/MWh to €180/MWh depending on technology and market. Spain and Portugal introduced agas price cap mechanism (€40-65/MWh), limiting the bids of gas-generators in Spain and Portugal and suppressing wholesale power prices from June 2022 through May 2023. European governments spent €60 billion on crisis-related electricity subsidies in both 2022 and 2023.13

At the same time, long-term electricity contracts are important enablers for clean energy generation projects and their bankability.

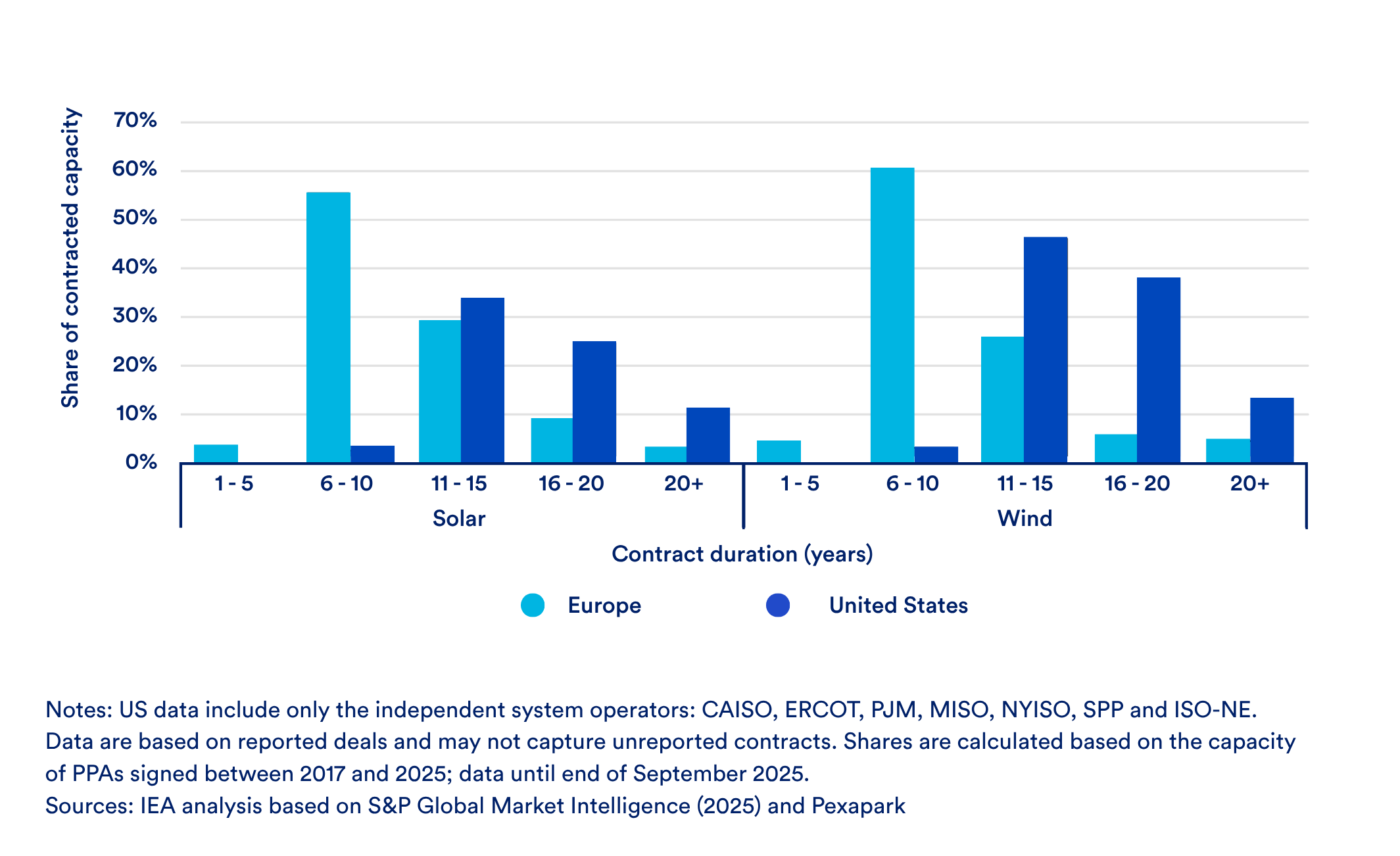

Figure 5: Share of solar and wind power purchase agreements in Europe and the United States by contract duration, 2017-2025

The EU Electricity Market Design revision of 202414 acknowledged that well-functioning short-term markets needed completion with longer-term signals to de-risk volatility from external factors and unlock flexibility potential. The market practice on forward markets offers limited support for long-term renewable or nuclear energy investments, and is better suited to cater for short (month-ahead) or medium-term needs.15 Long-term electricity markets bridge structural gaps by offering diverse contract types tailored to different participants’ needs. PPAs and two-sided Contracts for Difference (CfDs) are emerging as key enablers of renewable and nuclear energy deployment, ensuring price stability, and improving the financial viability of new projects. The electricity market reform introduced obligations for Member States to promote PPAs and ensure these instruments are available, including state guarantees to cover PPA off-taker default risk.16 These contracts typically span 5-10 years or longer periods (up to 20 years in current practice), providing price predictability that supports project financing and meets different hedging needs. For industrial buyers, long-term contracts protect against price shocks, provide predictability and therefore mitigate competitiveness risks. The recent energy crisis highlighted PPAs’ value as hedging instruments.

How do PPAs work:

Power Purchase Agreements (PPAs) represent the primary market mechanism for this purpose. PPAs are long-term contracts between electricity buyers—utilities, corporations, and public entities—and sellers, typically structured to finance new capacity, hedge price exposure, or meet decarbonisation targets. While originally used primarily for renewable electricity access to comply with corporate sustainability commitments, PPAs now serve critically as protection against future price fluctuations. For industrial consumers, this hedging function addresses operational cost uncertainty directly, enabling electrification investment decisions with predictable returns.

PPAs have a longer-term perspective than forwards and futures17, allowing them to meet different hedging needs. These contracts are typically signed for durations between five and 10 years or longer periods (up to 20 years) in the current practice.18 Contract length can depend on a variety of factors, including the technology type, the availability of alternative options to de-risk investments over the long term, as well as whether the PPA aims to finance a new asset or stabilise revenues for an existing one.19 The longer the PPA term, the fewer contracts are signed, particularly after 10-15 years, as seen in Europe and the United States, while the contract duration of solar and wind PPAs has generally exceeded five years in Europe.20

The PPA market has grown five-fold since 2018.21 The growth of bilateral long-term contracting creates competitive pressure on both supply and demand sides. Renewable developers compete to offer attractive long-term prices to industrial off-takers, whilst consumers gain alternatives to traditional utility supply contracts.

However, renewable and storage PPAs signed in 2024 represented only 3% of installed capacity for these technologies in Europe.22 Only 13 Member States are considered mature PPA markets, while seven EU countries are still classified as emerging PPA markets.23 A range of legal and regulatory, informational, and economic barriers limit the broader uptake of private, or decentralised, procurement of long-term contracts.24 The PPA market faces barriers like credit-worthiness requirements of buyers, lack of knowledge and in-house capacity of SMEs for signing PPAs, accounting rules and the implementation of guarantees of origin frameworks of corporate buyers across the EU are not well harmonised. Committing to long-term contracts at current price levels, combined with the proliferation of negative price hours of renewable generation assets impacts the profitability of pay-as-produced25 contracting for developers and off-takers.26

PPAs require industrial buyers to provide creditworthiness guarantees for long-term commitments, yet many industrial facilities cannot offer the credit security that generators require. This credit barrier is particularly acute for smaller and medium-sized industrial operators.27 Even where buyers can meet creditworthiness requirements, a further barrier remains: renewable generation profiles rarely match a buyer’s consumption pattern in either volume or hourly shape. Managing that mismatch adds cost and contractual complexity that smaller buyers cannot absorb.

Multi-buyer PPAs represent a particularly promising model to expand access for smaller consumption volumes but remain challenging to execute due to the complexity of aligning different consumer types on PPA profiles, electricity sharing features, and contract exit conditions.28

As the PPA market matures, there is a need for standardisation and platform development to further enhance competition by reducing transaction costs and broadening market access beyond large corporate off-takers. At current pace, PPAs will cover only 13% of RES investment needed by 2050, together with CfDs 33%29, even though they are crucial for financing and electrification.

Contracts for Difference (CfDs) offer a complementary mechanism. The EU Electricity Market Design (EMD) reform established two-sided CfDs as the default support mechanism for all new low-carbon capacity, including nuclear.30 Unlike PPAs, CfDs are two-way contracts where both parties bear price risk: the buyer – governments – pays a fixed strike price to the seller for contracted volume, whilst the seller compensates the buyer based on the market reference price.

Whilst two-way Contracts for Difference (2w-CfD) have primarily supported renewable generation, their application to storage and grid infrastructure remains underdeveloped despite these assets’ essential role in enabling high-renewables systems. Storage provides the flexibility necessary to balance variable renewable output, whilst grid infrastructure connects generation with demand centres. Both require long-term revenue certainty to justify capital-intensive investments. In practice, the implementation of the requirements of market-responsiveness and the combination of 2w-CfDs with PPAs have raised practical questions.31 Risks arise from cross-subsidisation (where public support enables artificially favourable PPA terms for private off-takers), PPA market distortions (altered pricing dynamics compared to purely market-based products), and reduced wholesale market liquidity if substantial volumes are diverted to bilateral contracts rather than organised markets.32 To mitigate these risks, the Commission recommends that beneficiaries select PPA off-takers through competitive bidding processes with low minimum offtake volumes (e.g., 1 MW), reasonable contract lengths (approximately 5 years), and open participation for retail suppliers and cross-border entities.33

Recognising obstacles in bilateral contracting, different policy mechanisms have already been implemented to facilitate and/or incentivise the development of PPAs.

Examples of existing initiatives

The European Investment Bank (EIB) has launched a €500 million pilot program with the European Commission to act as a counterparty for part of the PPAs undertaken by companies34, Under this programme, the EIB provides counter-guarantees through partner banks, covering part of the off-taker’s payment risk. The scheme is technology-neutral, open to SMEs, mid-caps, and energy-intensive industries, and can be combined with national guarantee frameworks. It can also support multi-buyer PPAs, allowing groups of SMEs to jointly contract clean electricity and strengthen their collective bargaining position.

Separately, the EIB operates dedicated de-risking instruments under InvestEU and related packages that support project finance for wind, solar, storage, and grid components.35 These instruments target the supply side, improving the bankability of generation and infrastructure projects by reducing technology and construction risk for developers and lenders.

France established a public guarantee fund for industrial PPAs in 2023, supporting onshore wind and solar projects with minimum contract durations of 10 years.36 Such mechanisms reduce barriers and enable industrial participation in long-term electricity markets.

Spain provides an instructive example of policy-driven PPA market development. The market operator OMIE launched standardised 5–10-year PPA contracts for baseload and solar profiles in 2022, whilst Royal Decree 1106/2020 mandates that large electro-intensive users consuming over 1 GWh annually source at least 10% of their consumption through minimum 5-year PPAs.37 Spain’s public guarantee scheme has proved transformative: the country now accounts for 23% of total European renewable PPA capacity.38

Building on successful these practices in Spain, France39 and Italy40, the European Commission endorses tripartite agreements as a bankability tool also in its Strategy for the development and deployment of Small Modular Reactors (SMR) for nuclear deployment, demonstrating its applicability beyond renewables.41

The European Commission adopted recommendations on removing barriers to the development of power purchase agreements and other energy purchase agreements, calling Member States to allow for entities, mandated by Member States, to resell part of the capacity supported by 2w-CfDs, to any consumer, including across borders, by means of PPAs awarded via competitive bidding processes, with maturities of about five years.42 Member States should ensure that there are no barriers to developing market platforms for aggregation for PPAs and that their use by market participants remains voluntary. Also, Member States should reduce barriers to multi-buyer PPAs, and facilitate the signing of those contracts in the framework of any State-backed guarantee. These recommendations can be widely addressed by implementing tripartite contracts. Further, the Commission recommends that designated competent bodies in Member States should issue guarantees of origin to be issued and transferred, in line with EU standards, with time granularity down to market time unit, reflect the bidding zone in which the generation has taken place and can be exchanged across borders.

From creating a framework to developing a contracting tool

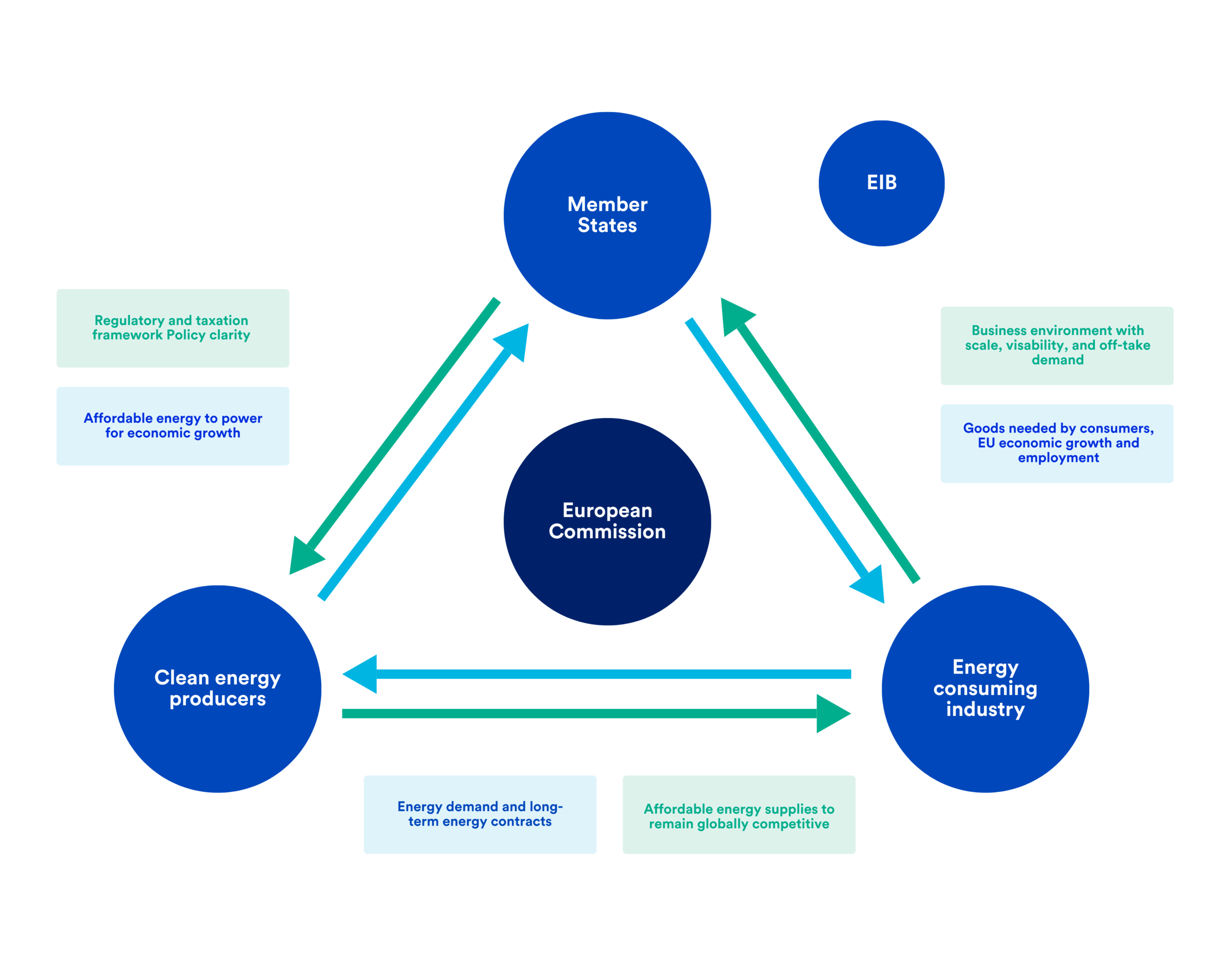

The EU’s Affordable Energy Action Plan proposed the concept of tripartite contracts for affordable energy as a tool to deliver the dual outcome of deep decarbonisation and industrial competitiveness. Figure 6 shows the European Commission’s vision of a tripartite forum and its policy objectives.

Figure 6: A tripartite contract for affordable energy for Europe’s industry.

A state entity acting as an intermediary within a tripartite agreement and as a central counterparty to both generators and industrial consumers, could guarantee contract performance. This approach could substantially expand PPA and CfD accessibility, enable access to long-term contracts, and support the development of 24/7 clean electricity products for industrial consumers.

The European Commission currently facilitates two sectoral tripartite agreements through a framework coordination forum of stakeholders, however, they have caveated from the term “contracts” to agreements. But Europe needs to think bigger about the role of tripartite contracting. Tripartite contracting has the potential to be a foundational mechanism that enables a larger scale of clean energy contracting.

The tripartite concept removes barriers to PPAs and broadens the off-take base by providing public guarantees to SMEs and centralising long-term contracts at a public agency or contracting platform. The platform acts as the sole counterparty for PPAs and/or contracts-for-difference (CfDs), absorbing the off-take risk for generators while reducing barriers for development.43 The current fragmentation of national CfD approaches — in eligible technologies, reference prices, and auction design — limits the cross-border potential that tripartite contracting at EU scale could unlock. The coordination of CfD design is therefore not a technical nicety but a prerequisite for the model to function across Member States.

Upcoming tripartite contracts in the EU

The first two sectoral tripartite agreements were launched on September 5, 2025, as part of the EU’s Affordable Energy Action Plan (February 2025). The fora foster high-level coordination of clean energy procurement:44

Structure and Participants: Drafts for both tripartite agreements have been prepared by the Commission in engagement with interested parties, industrial associations, Member States, the EIB, ENTSO-E and, EU DSO Entity. The European Commission facilitates the agreements by providing regulatory clarity, supporting access to EU funding, through the Technical Support Instrument and regional cooperation mechanisms. Industrial consumers commit to providing transparent information on electricity demand and visible, forward-looking off-take signals.

Initial Sectors:

- Offshore Wind & Grids: Private sector draft commitments include developer and supply chain obligations to ensure project development. Member States commit to ensuring the coordination of offshore wind tenders and grid procurement schedules at regional level, providing a transparent and long-term project pipeline extending beyond 2040, harmonising auction criteria in line with the Net-Zero Industry Act, and deploying de-risking tools such as CfDs and PPAs.

- Energy Storage: Private sector draft commitments include system operators improving grid visibility for storage technologies and providing clear locational signals, and renewable and storage developers committing to scale up hybrid projects and deploy storage in a grid-friendly manner. Member State draft commitments include accelerating the assessment of non-fossil flexibility needs, setting national targets for demand response and storage for 2030 in line with the Electricity Regulation45, and removing barriers to market access, including double taxation.

Future Expansion: The Commission is assessing applications in other sectors including biomethane (announced in the roadmap to phase out Russian energy imports), energy efficiency, nuclear energy, and data centre energy integration—signalling that this sectoral approach will expand beyond wind and storage. So far, there have not been commitments to anchor the agreements into concrete contracting tools, but rather to keep them as high-level frameworks for enhanced stakeholder dialogue.

Call for Participation: All Member States are encouraged to engage directly with the Commission to ensure active participation in drafting and concluding the first two agreements, expected to be finalized for signature in mid 2026.

The sectoral tripartite agreement drafts are an important proof of concept. Whether they translate into a replicable model for industrial electrification will depend significantly on how the Commission approaches the forthcoming Electrification Action Plan to embed tripartite contracting in the broader policy framework and on whether PPA reform, CfD design guidance, and EIB instrument design move in step with it.

Why tripartite contracts matter for industrial consumers: Solving the cost certainty problem

The central entity’s ability to pool diverse generation and storage technologies upstream means it can offer downstream contracts that better match industrial baseload profiles at lower cost than bilateral contracting. Through competitive bidding and reselling multiple contracts, the intermediary is spreading shaping costs —the expense of matching variable renewables to baseload demand — across a larger portfolio rather than leaving each consumer to manage them individually. By procuring electricity from multiple generation technologies, e.g. intermittent renewables, clean firm capacity, storage, and industrial demand response, the central entity creates a market for 24/7 clean energy that bilateral contracting cannot replicate. This bundling of generation, storage, and flexibility reduces costs compared to each party contracting separately, with service procurement informed by system modelling to reflect changing reliability and flexibility needs.

This is particularly valuable for storage and flexibility assets, whose revenue streams are too illiquid and fragmented to be hedged in current European markets.46 The central entity could contract flexibility assets upstream and use this flexibility to issue shaping products to the market.47 Managing that mismatch adds cost and contractual complexity that smaller buyers cannot absorb — and is precisely what an intermediary which is pooling multiple technologies can resolve. In 2024, only 10% of PPAs in the EU were hybrid contracts bundling several technologies, including storage assets.48 Via tripartite contracts the shaping and balancing risks could be shifted to the intermediary and baseload or shaped PPAs providing a fixed delivery profile could be more accessible.

The state backing eliminates counterparty credit risk for both clean generation and grid projects, as well as the risk of disruption of offtake by the industrial consumer. Market price signals and performance requirements (e.g., energy efficiency, flexibility) could be built into awarded contracts.

Key benefits for industrial consumers:

- Fixed electricity prices provide cost certainty over long periods.

- State backing reduces counterparty credit risk.

- Pooling multiple technologies reduces shaping costs.

- Baseload needs portfolios that provide firm clean power and hedging against volatility.

- Transparent pricing develops broader voluntary markets over time.

These benefits depend on the well-designed procurement processes of the entity.

The state intermediary can leverage competitive bidding processes to select both upstream generators and downstream off-takers, driving down costs through competition on both sides of the market. For downstream consumers, the state entity can issue PPAs with maturities of approximately five years through competitive auctions with low minimum offtake volumes (e.g., 1 MW) and open participation for retail suppliers and cross-border entities.49 By pooling multiple installations with complementary generation profiles upstream, the intermediary creates more uniform products that better match consumer baseload needs whilst minimising shaping costs. The competitive allocation of contracts through open, transparent, and non-discriminatory bidding processes lowers the costs of developing generation capacity and ensures that contract prices reflect electricity’s long-term value for the system.50

This approach maximises revenues for developers, thereby keeping required state support to a minimum, whilst simultaneously offering consumers more favourable terms than they could negotiate individually. The state backing removes credit risk premiums that would otherwise inflate bilateral contract prices, particularly for small and medium-sized enterprises.

Why tripartite contracts matter for the market: Shaping investment

Long-term revenue certainty unlocks investment in renewables, storage, and clean firm capacity — creating the supply for new industrial load. Tripartite agreements can therefore de-risk clean energy deployment: coordinated and pooled procurement of clean energy simplifies procurement for small- and medium-sized customers, expands market competition to reduce costs, enables portfolios of resources to supply firm power, and results in public data that can guide anticipatory grid investment.

24/7 clean firm power is not purchasable by most European industrial consumers today. Unlike variable renewables, clean firm technologies — including geothermal, nuclear, and sustainably sourced biomass — can generate power on demand regardless of weather. Many clean firm technologies lack the forward contract markets that would make them financeable at scale. The shift toward deep decarbonisation also relies heavily on flexible resources, particularly energy storage and demand response, to counteract the intermittency and seasonality of variable renewable energy (VRE) resources.51 Investors in storage and flexibility assets are exposed to risks they cannot hedge, because forward derivative markets for ancillary services remain highly illiquid in Europe.52

The real value of storage — its ability to generate revenue across multiple market services simultaneously, often called ‘value stacking’ — cannot be captured when the markets for those services only exist in the short term.53 When risk markets are missing, modelling consistently shows less investment in renewables and storage and a consequential shift toward less capital-intensive fossil technologies, distorting the energy mix away from what deep decarbonisation requires.54 This market failure is structural, and is difficult to resolve by incremental improvements to bilateral contracting alone. The tripartite model could address non-commercialised technologies and missing markets for hedging balancing and shaping costs by pooling generation profiles under PPAs and CfDs.

When an industrial buyer signs a bilateral wind PPA, they are buying an output profile — not firm power. Managing the gap between that profile and their actual consumption requires separate shaping contracts,55 storage arrangements, and balancing exposure, each of which adds cost and complexity. The tripartite model shifts that burden from individual buyers to the central entity, which can spread shaping costs across a large and diversified portfolio. Shaping costs become distributed across, significantly reducing the per-unit cost.

When the central entity pools supply, it aggregates clean firm capacity alongside wind, solar, and storage into a single portfolio. This pooled approach creates a genuinely 24/7 clean energy product by using storage and demand flexibility to manage the variability of renewables, while clean firm power provides reliability. The result is not just cheaper procurement — it is a genuinely different product: firm, clean power that industry can plan capital investment around.

Procurement processes could be designed to reward portfolios that pool renewable generation with clean firm capacity, storage, and demand response to enable 24/7 clean power delivery. While a competitive design ensures that technology-neutral procurement ensures lowest-cost clean energy mix, storage and flexibility can become integrated parts of the clean energy solution.

Shaping products could take the form of financial derivatives for defined wind or solar generation profiles or time-shifting products complementing outputs to meet PPA profiles, backed by flexible resources like storage and demand-side response. These facilitate hedging PPA risks and help with PPA uptake.56 New products could be envisaged to grant the opportunity for PPA signatories to cover shaping risk against remuneration. Utility-scale batteries could further enhance complementarity by allowing solar power to keep discharging into morning and evening peaks when solar production is low and demand is high.57

In Italy, GME acts as a central contracting entity for batteries, and offer downstream ‘virtual batteries’ through time-shifting products.58

In 2025, Italy is launching a 50 GWh new storage capacities tender, called ‘MACSE’. Upstream, the mechanism grants a regular fixed remuneration to storage assets (batteries first, and pumped-hydro at a later stage). Selected capacities in the mechanism must, in return of the fixed remuneration, be available to GME. They can obtain additional remuneration on the Dispatching Services Market (MSD, the ancillary services market), but have repay a share to Terna, the Italian TSO (80-95%).

The flexible capability procured would then be sold to consumers in the form of ‘time-shifting products’ on the forward and spot markets. These time-shifting products will offer consumers means to efficiently manage their shaping costs by using the contracted ‘virtual batteries’. The ‘time-shifting products’ will be traded by GME on a specific platform, as illustrated below, open to consumers and to batteries not participating in the scheme. On this platform, storage capacities will be pooled to offer standardised virtual batteries.

Standardised virtual batteries allow buyers the possibility to use a virtual storage asset as if it was theirs to store and sell electricity. GME is to define the contracts based on underlying batteries performance and volumes, reference area, and validity of the contracts (from daily on multi-annual).59

Product maturity would also impact which consumers may wish to contract with the intermediary, as shorter multi-year contracts could appeal to a wider base of consumers, including retail suppliers and small non-residential consumers. Forward products, with typically shorter maturities than PPAs, sold in advance and for more granular delivery windows, could also grant more flexibility to the central entity to hedge its upstream contracts under CfDs.60

3. Design considerations and safeguards

Entity design: Role and structure

Defining clearly what role the intermediary entity will play — or which combination of roles — is the single most consequential design choice, since it determines procurement structure, governance, risk allocation, and the scope of eligible participants downstream. Member States can structure this combination in several ways. A well-designed central entity that pools supply, increases competition on both sides of the market, and removes credit and complexity barriers should, over time, bring contract prices down. The cost predictability this creates will flow beyond direct off-takers to their supply chains and subcontractors, supporting the competitiveness of European industry as a whole.

The state entity’s role in combining two-sided Contracts for Difference with Power Purchase Agreements represents a particularly powerful mechanism for managing system costs. By procuring CfDs upstream, the state hedges its exposure to spot price volatility. Simultaneously, it can issue standardised PPA products downstream to consumers, including those in other Member States. This intermediary function creates opportunities to optimise risk allocation and cost distribution.61

The intermediary entity could take different forms —or a combination thereof:

A. Centralised matching platform with guarantor function

An entity operating under a simple ‘auction-as-a-service’ model could be envisaged, where a central entity links up buyers and sellers on a centralised platform. This model grants a light-touch role to the central entity, as risks and costs would be fully transferred to the buyer.

B. Investment de-risker

An investment de-risker (Electrification Bank)62 absorbs specific commercial and financial risks—such as technology, demand, or counterparty risk—to make clean energy projects bankable and attract private capital that would otherwise avoid long-term commitments.

C. Active market-maker or clean generation aggregator

A market maker in electricity markets is an entity that regularly offers to buy and sell a minimum amount of power products at prices that are not too far apart, often in exchange for a fee. This helps keep prices available at all times and makes trading cheaper and easier for other market participants.63

The ultimate goal of these design choices is not institutional architecture for its own sake — it is lower, more stable electricity prices for European industry and reducing bankability challenges for clean energy suppliers. The platform must operate on competitive principles: generators and infrastructure developers compete to supply the platform, while industrial consumers compete for contract allocation. Time-limited support ensures state backing diminishes as markets mature, with the goal of catalytic market creation rather than permanent intervention.

The central entity should procure or facilitate procurement of clean power through long-term contracts (e.g., CfDs) upstream to support development of low-carbon energy and flexibility assets. Downstream, it could issue short to long-term contracts (e.g., PPAs, forward products) with fixed or predictable pricing over 10-15 years, offering consumer hedging against price volatility.

De-risking interventions like state backing long-term contracts for storage and flexibility providers with guarantees could fill missing long-term markets for non-commercial system-serving innovations that are currently sold only in short-term markets.

State guarantee schemes and EIB support have so far been structured around individual generation technologies rather than the portfolios that 24/7 procurement requires. An instrument designed to de-risk a solar project cannot de-risk the hybrid solar-storage-geothermal portfolio that a tripartite auction might select. Designing instruments that reflect how clean energy actually needs to be procured — across technologies, not within them — is a precondition for tripartite contracts to reach their potential.

A related design question concerns the permanence of the tripartite model. Tripartite contracts are best understood as a permanent market feature with periodic procurement cycles — rather than a temporary crisis instrument — since the structural barriers they address, particularly for smaller industrial operators, are unlikely to dissolve as markets mature. The competitive auction structure is phase-out by design. Each successive procurement round drives down the clean firming premium as learning curves reduce technology costs, as more developers gain experience assembling hybrid portfolios, and as standardised products lower transaction costs for buyers. What requires active state intermediation today — assembling a portfolio of renewables, storage, and clean firm capacity into a bankable, priced product — will become progressively more replicable by private actors as the market deepens. The central entity’s role should therefore shift over time: from active market-maker and risk-absorber in early rounds, to a backstop guarantor for those the bilateral market still cannot reach in later rounds, to ultimately a standards-setter and liquidity anchor once private 24/7 clean energy products become genuinely available at scale.

This trajectory should be built into the model’s governance from the outset, with explicit review mechanisms that assess bilateral PPA market depth at defined intervals and adjust the scope of tripartite intermediation accordingly. The goal is catalytic market creation, not permanent substitution. Participation should remain voluntary throughout: industrial consumers who can access bilateral PPAs directly should be free to do so, and the tripartite mechanism’s success should ultimately be measured not by the volume it intermediates indefinitely, but by the degree to which it has made its own full scope unnecessary.

The framework should define which consumers access long-term contracts. This means, tripartite contracts could potentially target only specific industrial groups (e.g., vulnerable consumers, strategic industries) to unlock defined clean electrification investments while preserving competitiveness.64

As an example for demand pooling, the Innovation Fund’s Clean Heat Auction (IF25 Heat Auction) represents the first EU-wide auction targeting decarbonisation of industrial heat production, covering technologies including heat pumps, electric boilers, solar thermal, and geothermal across all industrial sectors. Its administrative design, aimed at keeping participation accessible to smaller industrial operators, offers useful precedent for how the entity could operate and how the tripartite contracting frameworks could approach simplicity of access.65

From a governance perspective, the central entity could be a public entity (possibly regulated) or a regulated private third-party operating for profit, leveraging trading, PPA, and market-making experience. The state entity itself can sell portions of CfD-backed electricity as shorter-term PPAs (approximately five years), providing hedges for developers requiring long-term investment commitments whilst offering customers who cannot commit to 15-20 year contracts more accessible shorter-term products. These could be awarded through competitive bidding processes open to suppliers and consumers, including across borders, with careful attention to maintaining market liquidity through financial rather than physical settlement structures where appropriate. This layered approach to contract maturity, long-duration CfDs upstream, medium-duration state-intermediated PPAs downstream, accommodates different participants’ risk tolerances whilst maintaining efficient market functioning.66 Standardisation of the downstream product risks recreating the very barriers that the model is trying to remove as different sectors carry different legal requirements and risks, but efforts towards a standard product and contract framework will be essential for the scalability of tripartite agreements.

Regardless of structure, the entity’s mandate, regulation, and incentives must be clearly defined and aligned with EU policy objectives.

Preventing market distortion and crowding-out

The EU Electricity Regulation leaves several CfD design implementation issues open, especially regarding safeguards that can mitigate crowding-out effects.67 Currently, designs risk ‘overcrowd’ other types of contracts which creates reduced market activity and less competitive pressure.68 Appropriate reference price indexes and settlement volume profiles still pose challenges, but improved state-driven CfD designs are emerging that embed dispatch incentives through reference price mechanisms, forming best practice for enhanced contracting. Alternative approaches such as financial CfDs and yardstick CfDs decouple payments from physical output, reducing dispatch distortions and applying capability-based rather than generation-based remuneration approach. As part of the Grid Package of December 2025, the European Commission issued comprehensive guidance on the design of two-way Contracts for Difference (2w-CfDs), providing Member States with detailed recommendations to optimise these increasingly important support mechanisms for clean energy investments. As 2w-CfDs become the mandatory default support scheme for new renewable and nuclear capacity under the reformed Electricity Market Design, their proper design is critical to ensuring they lower rather than raise overall system costs whilst accelerating decarbonisation. For instance, if badly designed, their price fixing can distort dispatch incentives or consumer price signals, and their referencing on the day-ahead market can drain liquidity from other markets. Enhanced contract design could take into account a reference price of settlement volumes and avoiding CfDs ‘crowding out’ private contracts.69

The recent guidance of the European Commission establishes fundamental principles that Member States should apply when designing 2w-CfD schemes, in order to make them more flexible and prevent inefficient generation that burdens the system.70 To implement these principles effectively, CfD designs, regardless of asset type, ideally incorporate locational incentives to maximise system value and minimise congestion. This requires coordination with long-term system planning to ensure infrastructure investments align with decarbonisation pathways whilst maintaining efficient price signals for optimal siting decisions. The development of hybrid installations, that combine generation assets with battery storage, is a mean to optimise scarce grid connections and accelerate project development.71

The contracting entity should enable bundling of multiple technologies in single contracts and complement rather than replace private PPA markets to avoid crowding out voluntary PPAs and other types of contracts. CfDs can reduce incentives for generators to align maintenance with market conditions, weakening market signals to avoid outages during periods of tight supply. This also reduces incentives for system-friendly asset design. Ensuring that support mechanisms maintain a sufficient link to market outcomes is critical to promote efficient investment and reliable system operation.

To balance state budget exposure from upstream CfDs, the central entity should issue long-term contracts downstream to consumers, hedging market price exposure into fixed or predictable cost structures. This arrangement grants stability and visibility to both consumer and state budgets while limiting public financial exposure over time as markets mature.72

Managing legal and contractual risks

Long-term contracts create counterparty risks that require explicit provisions on liability, consumer recourse, force majeure allocation, insurance requirements, and dispute resolution. When suppliers or developers fail to deliver—due to delays, technical issues, or insolvency—the legal framework must clearly specify how this affects industrial consumers’ claims and remedies. State backing can mitigate some risks, but the framework must be transparent about which risks remain with consumers versus the state, building confidence through equitable risk distribution.

Granular accounting and supply-demand matching

Clean electricity cannot be physically traced once injected into the grid, so Energy Attribute Certificates, such as Guarantees of Origin (GOs) verify renewable sourcing. While current GO frameworks lack harmonisation across Europe73 and operate on annual accounting, supporting 24/7 clean electricity commitments would need GOs that shift to hourly time information, enabling precise hourly matching of production and consumption. This allows industrial consumers to verify procurement granularly, supports decarbonisation targets, creates flexibility incentives, and demonstrates the viability of 24/7 clean electricity procurement.

Cross-border PPAs face legal and financial risks due to differing regulatory frameworks. TSOs must provide multi-annual long-term transmission rights and collaborate regionally to allocate more capacity to markets early. Harmonisation of the Guarantees of Origin system across Europe, particularly regarding information required by registries, is essential for cross-border deal facilitation.74 European countries should also ensure that Guarantees of Origin can be exchanged across borders to facilitate cross-border PPAs.

Standardised contracts and exchange platforms with voluntary PPA templates would lower transaction costs and enable secondary trading. These infrastructure elements—harmonised data standards, hourly accounting, and standardised contracts—are prerequisites for efficient tripartite contracting at scale.75 Hedging effectiveness relies on hourly matching effectiveness, which has real value in increasingly volatile markets.

Complementary conditions

Electricity could and should be cheaper than it currently is.While tripartite contracts improve market liquidity and cost predictability by solving the bankability issue for industrial consumers, they cannot entirely address high electricity prices. Required solutions include reducing the relative tax and levy burden on electricity, ensuring a predictable and meaningful CO₂ price. These remain essential levers for decarbonisation policy and Member States seeking to restore industrial competitiveness.

ETS costs account for approximately 4–9% of final electricity bills for industrial consumers, depending on each country’s carbon intensity of generation.76 The taxation burden on electricity – the average rate of VAT on electricity which was 18% in 202477 – therefore dwarfs the impact of carbon pricing.

Addressing these taxation inequities by using flexibilities under the Energy Taxation Directive represents an important near-term priority for Member States. The Citizens Energy Package includes calls for action for Member States to carry out tax reviews and making full use of the flexibilities in EU legislation, and considering full or partial targeted reductions of excise duty rates on electricity for energy-intensive industries and VAT reductions for the installation of heat pumps.78

Further, the EU needs to swiftly align on predictable and meaningful CO₂ prices, as well as address grid congestion and unlock curtailed cheap electricity.

To further guide progress, the European Commission’s forthcoming Electrification Action Plan and the Heating and Cooling Strategy should further support these objectives. The Commission announced to set an electrification target, propose action to lower the electricity-fossil fuels price ratio and measures to accelerate the uptake of electrification solutions, such as through a market-based instrument on heat pumps, and address barriers for electrification of the economy, including phasing out fossil fuel subsidies.79 These will be presented with a broader energy package that will aim to reduce the relative tax and levy burden on electricity in contrast with fossil fuels.80

4. Implementation roadmap

The success of the tripartite model depends on deliberate choices on how the central entity is designed, how existing instruments like PPAs and CfDs are strengthened to support it, and how grid and electrification planning are brought into alignment with its needs. he tripartite model will only reach its potential if the conditions it depends on — institutional, contractual, and infrastructural — are built in parallel. Key actions are required from the EU and Member States across multiple policy domains.

EU Actions

Develop and finalise the tripartite contracting framework in genuine co-design with Member States.

- The Commission should build on its existing sectoral tripartite forums — for offshore wind and grids, for storage and data centre integration — by moving them from coordination platforms toward operational contracting mechanisms. This requires working directly with Member States, the EIB, ENTSO-E, DSOs, and industry associations to align on the structure of the state-backed intermediary, and the design of upstream and downstream procurement. A large-scale firming and hedging mechanism should evolve from this, anchored in clarity on the intermediary’s mandate — whether it operates as a matching platform, market-maker, investment de-risker (‘Electrification Bank’80), or some combination of the three. Done well, it delivers all three objectives Europe needs from contracting: revenue stability that unlocks clean investment, hedging that shields industry from volatility, and firmed portfolios for 24/7 clean power.

Strengthen PPA access as a direct complement to tripartite contracting.

- The tripartite model builds on bilateral markets rather than replacing them, and barriers to PPA uptake constrain the primary long-term contracting instrument for most industrial consumers. The recent Commission Communication on removing barriers to the development of PPAs is a welcomed step, given the wide range of market shortcomings identified. However, additional measures for broader PPA uptake be foreseen in the forthcoming Electrification Action Plan, delivering on the Commissions’ commitment to work with the EIB on promoting PPAs in a technology-neutral manner, as stated in the Action Plan for Affordable Energy and the Nuclear Illustrative Programme. The EIB’s PPA guarantee programme should extend its current scope, which covers wind, solar, and hybrid projects to include clean firm generation and brownfield energy technologies and adapt risk-sharing terms for smaller industrial off-takers, for whom standard commercial conditions remain prohibitive.

Mobilise private capital alongside public instruments.

- While developing tripartite contracts, the Commission should work with the EIB Group and other financial institutions to secure concrete commitments linked to specific sectors, with a view to crowding in private investment. Public instruments are most effective when they de-risk the first transactions rather than substitute for private capital over the long term. The forthcoming Electrification Action Plan should include short-term capital and operating support for heating applications where long-term cost competitiveness is foreseeable but not yet realised — particularly for high-temperature heat pumps and electric boilers, where the investment case remains sensitive to current electricity-to-gas price ratios. These policies should complement the Industrial Accelerator Act, which aims to create demand through lead market expansion.

Member State Actions

Implement the enabling regulatory framework.

- Member States should prioritise the full implementation of the Electricity Market Design Reform and address structural barriers that sit within their direct control. Two-sided CfDs are now the default support mechanism for new low-carbon capacity, and the Commission’s December 2025 guidance on their design is a welcome step. But design shortcomings remain, particularly around their alignment, flexibility and reference price mechanisms, and the risk of CfDs crowding out private PPAs. Member States need to structure competitive procurement to avoid distortions, to make sure that CfDs complement, not crowd out, PPAs and other market-based contracts, so tripartite agreements can support buyers and contract volumes. Building on the Commission’s April 2026 guidance on removing barriers to the development of power purchase agreements and other energy purchase agreements, Member States should allow for entities that resell capacity supported by 2w-CfDs, to any consumer, including across borders, by means of PPAs awarded via competitive bidding processes. Member States should reduce barriers to multi-buyer PPAs and ensure that there are no barriers to developing market platforms for aggregation for PPAs while their use by market participants should remain voluntary. Resolving the outstanding PPA and CfD design questions will affect the functioning of tripartite contracts. Further, designated competent bodies should issue harmonised guarantees of origin, with time granularity down to market time unit, and that reflect the bidding zone in which the generation has taken place and exchangeable across borders.

Launch pilot tripartite contracts and build the necessary trading infrastructure.

- Building on existing models in France, Spain, and Italy, Member States should begin deploying pilot programmes to test the tripartite model with industrial facilities and suppliers. Lessons from these pilots — on procurement design, entity governance, and consumer participation — should be shared actively across Member States and fed back into the Commission’s framework development. Where Member States decide to develop state-backed guarantees, they should ensure appropriate coordination with the EIB’s counter-guarantee lending instrument to support midcaps and larger corporates to sign corporate PPAs with renewable energy suppliers.

Integrate grid and electrification planning, and bring grid projects into the tripartite forum.

- Grid connection delays and congestion are not separate from the tripartite agenda, they are central to it. Lengthy and fragmented grid connection approval processes frequently delay electrification projects, increasing capital risk and making fossil-based alternatives comparatively more attractive. Member States should move to proactive grid planning that anticipates industrial electrification demand and incorporate in their adequacy assessments forward-looking industrial load scenarios. Member States need to align procurement schedules for generation and grid projects, publish transparent grid hosting capacity maps that direct industrial investment to locations with available capacity, and fast-track permitting for projects that form part of designated clean industry clusters.

Footnotes

- Natural gas often sets the marginal price in power markets, meaning gas price spikes amplify power market prices to unsustainable highs.

- https://energy.ec.europa.eu/news/commissioner-jorgensen-announces-first-2-sectorial-tripartite-contracts-2025-09-05_en

- Compass Lexecon, Reviving Europe’s Industrial Power: How to boost competitiveness through energy. 2024 p 53

- European Environment Agency, Fossil fuel subsidies in Europe. 2025: European Environment Agency.

- Rosslowe and Petrovich (2026), Latest Energy Shock Reminds Europe of Its Risky Gas Reliance, Ember, 13 March 2026

- By 2025, the United States accounted for 61% of the EU’s LNG imports, establishing a dominant supplier position. Source: Piria, R., Szulecki, K., Lentschig, H., and van Schaik, L., Europe’s Selective Blindness on Gas: US LNG and the Limits of Supply Diversification. Ecologic Institute, Norwegian Institute of International Affairs, and Clingendael Netherlands Institute of International Relations.

- Draghi Report (2024), Chapter on Energy.

- Draghi Report (2024), citing ESMA evidence on gas derivative market concentration

- Ember, Latest energy shock reminds Europe of its risky gas reliance, March 2026.

- RESource Corporate PPA Guide, 2025

- Why the sustainable provision of low-carbon electricity needs hybrid markets, Jan Horst Keppler Et al

- IEA, Electricity Market Design, Building on strengths, addressing gaps. 2025. P 108

- https://energy.ec.europa.eu/topics/markets-and-consumers/electricity-market-design_en

- ACER, Progress of EU Electricity wholesale market integration – 2025 Monitoring Report, 2025.

- https://energy.ec.europa.eu/topics/markets-and-consumers/electricity-market-design_en

- Forward contract: a bilateral agreement to buy or sell an asset at a specific moment in time, for a predetermined price. Future contract: an agreement to buy or sell an asset at a specific moment in time, for a predetermined price.

- European Commission, Commission Recommendation on the design of two-sided contracts for difference for electricity. C(2025) 6701 final, 19 December 2025.

- IEA, Electricity Market Design, Building on strengths, addressing gaps. 2025 P 59

- IEA, Electricity Market Design, Building on strengths, addressing gaps. 2025. P 59

- European Commission, Tripartite Agreements Information Note (2025)

- IEA, Electricity Market Design, Building on strengths, addressing gaps. 2025. P 66

- Commission Recommendation of 22.4.2026 on removing barriers to the development of power purchase agreements and other energy purchase agreements.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. p 44f. Report commissioned by CATF.

- Pay-as-produced PPAs transfer the volume risk to the offtaker who is exposed to production and profile risk, which can be significant in the context of variable renewable production assets.

- Commission Recommendation of 22.4.2026 on removing barriers to the development of power purchase agreements and other energy purchase agreements.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. p 44. Report commissioned by CATF.

- RESource Corporate PPAs, Solarpower 2025

- European Parliament, Overview of the diffusion of PPAs and CfDs across Member States, 2026. Figure 3.

- Article 19d(1) of the Electricity Regulation requires that direct price support schemes for investment in facilities for new generation of electricity from renewable or nuclear generation take the form of 2w-CfDs as of 17 July 2027 (or 17 July 2029 for offshore renewable installations connected via hybrid interconnectors). It further stipulates that participation of market participants in such schemes should be voluntary. Article 19d(2)(a) and (b) of the Electricity Regulation clarify that 2w-CfDs need to ensure that the supported installations act in a ‘market-responsive’ way, whereas Article 19d(2) (e) and (5) of the Electricity Regulation establish conditions on how revenues stemming from the clawback mechanism should be used by the State. Furthermore, Article 19a(5) and (6) of the Electricity Regulation furthermore clarify the possible interplay between 2w-CfDs and PPAs. Article 19d of the Electricity Regulation also contains provisions on the avoidance of undue distortions to competition and trade in the internal market (Article 19d(2)(d)), the level of remuneration protection (Article 19d(2)(c)), penalty clauses in the case of early contract termination (Article 19d(2)(f)) and the Member States’ right to exempt small-scale installations from the provisions under Article 19d(1) of the Electricity Regulation (Article 19d(6)).

- European Commission, Commission Recommendation on the design of two-sided contracts for difference for electricity. C(2025) 6701 final, 2025.

- European Commission, Commission Recommendation on the design of two-sided contracts for difference for electricity. C(2025) 6701 final, 2025.

- In the case of renewable installations, these are mostly dealt with using the CEEAG and the recently approved CISAF. In the case of nuclear installations, the analysis is performed directly under Articles 107 and 108 TFEU.

- Pan-EU Power Purchase Agreement Guarantee LE, May 2025

- EIB Group and BNP Paribas sign new securitisation transaction to support French small businesses and mid-caps, 16.02.2026

- Compass Lexecon, Reviving Europe’s Industrial Power: How to boost competitiveness through energy. 2024, p 54.

- Compass Lexecon, Reviving Europe’s Industrial Power: How to boost competitiveness through energy. 2024 p 54. Compass Lexecon analysis based on Spain’s Royal Decree 1106/2020; 2024 data from the European platform for corporate renewable energy sourcing. Note: Country-level contracted PPA capacity data is as of end of November 2024 and the figure shows countries with a PPA capacity of at least 1 GW.

- Compass Lexecon, Reviving Europe’s Industrial Power: How to boost competitiveness through energy. 2024 p 54

- Compass Lexecon, Reviving Europe’s Industrial Power: How to boost competitiveness through energy. 2024 p 54.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. p 68. Report commissioned by CATF.

- European Commission, EU SMR Strategy, 2026

- Commission Recommendation of 22.4.2026 on removing barriers to the development of power purchase agreements and other energy purchase agreements.

- Compass Lexecon, Reviving Europe’s Industrial Power: How to boost competitiveness through energy. 2024 p 53

- Tripartite agreements for affordable energy for EU’s industry Information note from the European Commission, 14.10.2025

- Regulation (EU) 2019/943 of the European Parliament and of the Council of 5 June 2019 on the internal market for electricity

- Contract design for storage in hybrid electricity markets , Farhad Billimoria.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. p 66. Report commissioned by CATF.

- Commission Recommendation of 22.4.2026 on removing barriers to the development of power purchase agreements and other energy purchase agreements.

- European Commission, Commission Recommendation on the design of two-sided contracts for difference for electricity. C(2025) 6701 final, 2025.p. 22.

- European Commission, Commission Recommendation on the design of two-sided contracts for difference for electricity. C(2025) 6701 final, 2025.p. 12.

- Reforming European electricity markets: Lessons from the energy crisis, Natalia Fabra

- Contract design for storage in hybrid electricity markets , Farhad Billimoria.

- Contract design for storage in hybrid electricity markets , Farhad Billimoria

- Why the sustainable provision of low-carbon electricity needs hybrid markets, Jan Horst Keppler et al.

- “Shaping” describes balancing variable output to match demand patterns.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms,2025. p 69. Report commissioned by CATF.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. p 69. Report commissioned by CATF.

- For more information on the MACSE mechanism, see: EC (2023) State Aid SA.104106 (2023/N) – Italy. Support for the development of a centralised electricity storage system in Italy. Available here. Detailed rules: Terna (2024) The MACSE Regulations and related annexes currently in force. Webpage. Available here. See market commentary here: Green Dealflow (2024) Italy’s MACSE auction will reshape the Italian storage market. Available here.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. p 68. Report commissioned by CATF.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms,2025. p 70. Report commissioned by CATF.

- European Commission, Commission Recommendation on the design of two-sided contracts for difference for electricity. C(2025) 6701 final, 19 December 2025, p. 21

- A design suggestion with these characteristics under the name Electron Bank is currently developed by EnergyTag.

- IEA, Electricity Market Design, Building on strengths, addressing gaps. 2025. P 66

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. p 70. Report commissioned by CATF. A range of costs and risks associated with the support for clean energy deployment and/or shaping and balancing for downstream users can be borne by the central entity. For instance, while the upstream long-term contracts could be ‘pay-as-produced’ contracts, the shaping costs of the downstream contracts could be borne by the public central entity.

- European Commission, Innovation Fund 2025 auctions attract almost €10 billion of bids from European industry for decarbonisation support, 20 March 2026.

- European Commission, Commission Recommendation on the design of two-sided contracts for difference for electricity. C(2025) 6701 final, 19 December 2025

- Crowding out occurs when contracts dominate a market so extensively that private competitors cannot operate profitably, reducing voluntary market participation and innovation rather than complementing it.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. p 49. Report commissioned by CATF.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. p 7. Report commissioned by CATF.

- European Commission, Commission Recommendation on the design of two-sided contracts for difference for electricity. C(2025) 6701 final, 2025.

- European Commission, Commission Recommendation on the design of two-sided contracts for difference for electricity. C(2025) 6701 final, 2025. The approval of 2w-CfD schemes is done in line with State aid rules.

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. Report commissioned by CATF.

- Not all European countries are part of the European Energy Certificate System (EECS) aiming to standardise national schemes. A number of countries only hold an observer status in the Association of Issuing Bodies (AIB) which set up the EECS, such as Poland, Romania, Moldavia, Bulgaria, Ukraine or the UK. Harmonisation of the certifications can help track clean energy production, particularly in a growingly interconnected European market.

- Corporate PPA guide, SolarEurope

- Compass Lexecon, Accelerating the deployment of clean power technologies to reliably decarbonise Europe through enhanced planning and contracting mechanisms, 2025. p 47. Report commissioned by CATF.

- Arlia, D. and Hutchinson, J. (2026), “Drivers of electricity prices across households and energy-intensive industries and their importance for the EU’s decarbonisation objectives,” ECB Economic Bulletin, Issue 1/2026.

- Ember Energy (2026), Latest Energy Shock Reminds Europe of Its Risky Gas Reliance, March 2026

- Citizens Energy Package (COM/2026/115), March 2026

- AccelerateEU, Affordable and Secure Energy through Accelerated Action, COM(2026) 370 final, Brussels, 22 April 2026.

- The Clean Industrial Deal: A joint roadmap for competitiveness and decarbonisation

- A design suggestion with these characteristics under the name Electron Bank is currently developed by EnergyTag.

Credits

Authors:

- Kasparas Spokas – Director, Electricity Program, CATF

- Lea Romm – Associate, Europe Policy, Electricity, CATF

{kind=link}