The State Industrial Policy Playbook – A Policy Guide for Low-Emission Heavy Industry

Executive Summary

The industrial sector is a cornerstone of the U.S. economy, employing over 12 million workers and generating $851 billion in annual payroll, but it is also responsible for approximately 12 percent of harmful air pollutants and 23 percent of greenhouse gas (GHG) emissions. While decades of deindustrialization have eroded economic vitality in many regions, strategic investments in low-emission industrial technologies offer an opportunity to invigorate communities, secure high-quality jobs, and strengthen national security by reducing reliance on volatile foreign energy and materials markets.

Key Industrial Subsectors

This report focuses on four high-emitting subsectors which account for about 40 percent of U.S. industrial emissions:

Petroleum Refining

Essential for transportation fuels and chemical feedstocks. Petroleum refining emits carbon dioxide (CO2) primarily from fossil fuel combustion for high-temperature, continuous operations such as distillation, cracking, and reforming. Additional emissions come from hydrogen production, flaring, and venting. Decarbonization requires electrification, low-carbon hydrogen, carbon capture, utilization, and storage (CCUS), and a transition to alternative fuels and feedstocks.

Chemical Manufacturing

Produces key inputs for plastics, fertilizers, and fuels. Major emissions sources are combustion of fossil fuels for process heat, especially in steam crackers, and the use of fossil-based feedstocks, which release CO2 during chemical transformations. Electrification, low-carbon hydrogen, and CCUS are key solutions for reducing emissions.

Cement Manufacturing

Vital for construction. Cement manufacturing emits large amounts of CO2 from two main sources: fossil fuel combustion for kiln heat and the calcination process, in which limestone releases CO2 when it chemically converts to lime. Clean cement offers public health and emissions benefits, achievable through efficiency, CCUS, and alternative production processes.

Iron and Steel Manufacturing

Foundational for infrastructure and vehicles. The traditional blast furnace-basic oxygen furnace (BF-BOF) production method emits CO2 from both coal combustion for heat and as a chemical reducing agent for iron ore. The United States leads in low-emissions electric arc furnace (EAF) steel, but deeper decarbonization requires more scrap recycling, further electrification, hydrogen-based direct reduction, and CCUS.

Technology Pathways

Deep decarbonization of heavy industry requires a portfolio approach that combines mature and emerging technologies:

Electrification

The replacement of emissions-intensive heat and energy sources with electric technologies, ideally powered by affordable, zero- and low-emission electricity. Commercially ready for some processes (e.g., EAFs in steel) and emerging for others. High-temperature heat electrification in cement and chemicals is advancing through pilots.

Carbon Capture, Utilization, and Storage (CCUS)

The capture of carbon emissions with two possible end uses: permanent sequestration, where captured CO2 is stored deep underground in geological formations; or utilization, where CO2 is used as an input in other products or industrial processes. Critical for sectors with process emissions. The United States leads in installed capacity but needs expanded infrastructure and state incentives.

Alternative Production Processes

Fundamentally new methods of manufacturing industrial materials that break from traditional fossil-fuel-based, high-emitting pathways. Innovations such as hydrogen-based direct reduced iron (H2-DRI) and electrochemical cement can achieve near-zero emissions but require substantial investment.

Feedstock Substitution

Replacing conventional raw materials (often fossil-based or emissions-intensive) with lower-carbon, recycled, or bio-based alternatives.Use of recycled scrap, bio-based chemicals, and supplementary cementitious materials can yield immediate emissions cuts.

Alternative Fuels

Energy sources used to replace conventional fossil fuels that, depending upon the life-cycle analysis of emissions, can lower the carbon intensity of generating industrial heat. Biomass, waste-derived fuels, and low-carbon hydrogen can substitute for fossil fuels in high-heat applications, serving as a transitional pathway.

Energy and Materials Efficiency

A range of strategies aimed at reducing the energy and resource intensity of industrial production. Upgrades and process optimization can deliver immediate, cost-effective emission reductions of 10–20 percent in many facilities.

Policy Landscape

Federal Policy Context: Landmark federal investments, such as the Infrastructure Investment and Jobs Act (IIJA) and Inflation Reduction Act (IRA), have catalyzed $142 billion in low-emission energy and industry projects, leveraging tax credits, grants, and procurement standards. However, some funding has been rescinded, and future funding is uncertain, making federal-state policy alignment and state leadership crucial for durable progress.

State Policy Trends: Across the political spectrum, states are advancing low-emission industrial policies driven by shared goals, such as economic growth, job creation, emissions reduction, improving public health, and competitiveness. A diverse range of state-level policies is emerging to meet these objectives, offering practical examples and insights that other states can adapt and replicate to suit their own industrial contexts.

State Policy Toolkit

States have a diverse and expanding toolkit to accelerate low-emission industrial policies; some key measures are outlined below:

- Financial Incentives: Tax credits, grants, and public-private partnerships to close the cost gap for low-emission industry, especially when stacked with federal incentives.

- Targeted Research, Development, and Demonstration (RD&D) Support: Funding for emerging technologies and pilot projects to accelerate commercialization and build in-state expertise.

- Technical Assistance and Workforce Training: State agency- and university-provided roadmaps, technical support, and training to ensure programs reach both large and small enterprises.

- Market-Shaping Demand Policies: State procurement standards, advanced market commitments, and multi-state procurement models to create reliable demand for low-carbon products and de-risk private investment.

- Environmental Product Declarations (EPDs) and Labeling: Increased transparency and enable preferential procurement of low-emission products.

- Contracts for Difference (CfDs) and Preferential Bidding: Mechanisms to provide price stability and reward contractors using low-emission materials.

- Streamlined Siting and Permitting: Centralized processes and shared infrastructure anchors (e.g., port authorities, industrial hubs) reduce project delays and attract investment.

- Strengthened Regulations: Enhanced air quality standards, GHG caps, and extended producer responsibility (EPR) for plastics and chemicals.

Case Studies

This report highlights policy examples from multiple states and features three in-depth case studies of leading states in low-emission industrial innovation:

- Missouri Cement Decarbonization: Targets cement decarbonization through developing a statewide plan to maximize federal funds for clean heat, alternative fuels, and efficiency upgrades, prioritizing near-term emissions cuts and job retention

- Louisiana Carbon Capture Utilization and Storage: Streamlined CCUS laws and regulatory primacy have enabled $23 billion in announced investments and 4,500 expected jobs, but ongoing efforts will be needed to strengthen implementation and build community confidence.

- Colorado Industrial Policies Portfolio: Mandates a 20 percent reduction in industrial GHG emissions by 2030, with refundable tax credits, a Carbon Management Roadmap, and technical assistance, resulting in $1.7 billion in project announcements and 4,900 new jobs from 2022–2024.

Conclusion

States are at the forefront of industrial innovation and uniquely positioned to align federal investment with tailored state action that drives job creation, attracts private investment, and achieves environmental and public health goals. This report offers support for states in developing nuanced low-emission industry strategies tailored to their specific industrial mix, drawing on a combination of near- and long-term policy levers. By deploying financial incentives, demand-side policies, and regulatory standards, states can maximize both economic and environmental returns. These strategies are strengthened by integrated, cross-sector actions, including robust data and monitoring, compliance and accountability, and meaningful stakeholder engagement.

SECTION 1

Industrial Landscape

The Industrial Profile

The industrial base is a cornerstone of the U.S. economy. It employs over 12 million workers across nearly 300,000 facilities and generates an annual payroll of $851 billion as of 2022.1 Industrial facilities often serve as economic anchors for surrounding communities, providing not only direct employment but also stimulating local economies through upstream and downstream supply chains. Regional ecosystems of logistics, engineering, and maintenance services provide support to industrial clusters, such as the Port of Houston or the Gulf Coast refining corridor.

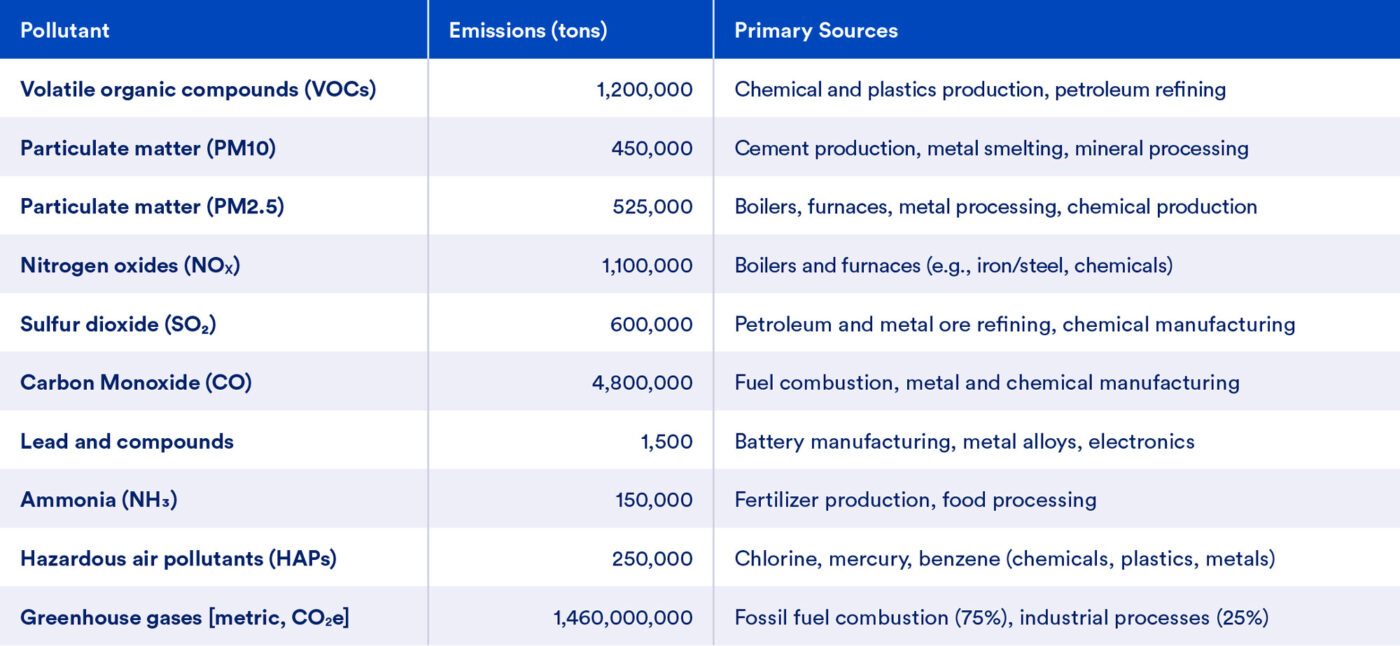

In addition to its economic importance, U.S. industry is a major contributor to air pollution (Table 1). The U.S. industrial sector consists of an array of diverse industries with distinct processes, technologies, and emissions profiles. In 2022, U.S. industrial operations were responsible for approximately 8.8 million tons of criteria air pollutants (including ozone precursors) which is about 12 percent of the U.S. total. Additionally, the sector emitted 1,460 million metric tons (MMT) of carbon dioxide-equivalent emissions (CO2e), or about 23 percent of total U.S. greenhouse gas emissions. When accounting for indirect emissions from electricity use, this share increases to around 30 percent. The sector also consumed 26.7 quadrillion BTU of energy in 2022, making it one of the most energy-intensive parts of the economy. The majority of this was from manufacturing industries (76 percent), followed by mining (12 percent), construction (7 percent), and agriculture (4 percent).2

Unlike the power or transportation sectors, where emissions have declined due to concerted policy and technological progress, industrial emissions have remained steady over the past two decades despite gains in efficiency.3 This challenge results from the inherent complexity of modernizing industrial operations, which often require sustained high-temperature heat, generate process emissions that cannot be abated through fuel- switching alone, and depend on fossil-derived feedstocks in key subsectors such as chemicals, steel, and plastics. Further, effective policy frameworks must be tailored to regional industrial landscapes and recognize the diversity of technological readiness and emissions profiles across subsectors. Lastly, industrial processes vary significantly and require tailored strategies to reduce emissions. Cement, iron and steel, chemicals, and petroleum refining—the four highest emitting industries in the United States4—have very different processes but share similarities, such that each offers distinct challenges to reducing emissions.

Nevertheless, momentum is building for modern and low-emission industrial processes, led by both public investment and private sector innovation.

Table 1: Estimated annual air pollution from U.S. manufacturing (NAICS 31-33), 2022

Sources:

U.S. EPA. 2024. National Emissions Inventory (NEI). Available at: https://www.epa.gov/air-emissions-inventories.

U.S. EPA. 2023. “Toxics Release Inventory (TRI) Program.” Available at: https://www.epa.gov/toxics-release-inventory-tri-program.

Shapiro, J.S. and Walker, R. 2018. “Why is pollution from US manufacturing declining? The roles of environmental regulation, productivity, and trade,” American Economic Review, 108(12), pp. 3814–3854.

National Association of Manufacturers. 2023. U.S. Air Quality Standards and the Manufacturing Sector. Available at: https://documents.nam.org/COMM/NAM_Air_Quality_Standards_Analysis_Web_Version.pdf.

U.S. EPA. 2024. Inventory of U.S. Greenhouse Gas Emissions and Sinks: 1990–2022.

Available at: https://www.epa.gov/ghgemissions/inventory-us-greenhouse-gas-emissions-and-sinks.

Congressional Budget Office. (2024). “Emissions of Greenhouse Gases in the Manufacturing Sector.” Available at: https://www.cbo.gov/publication/59695.

Benefits of Low-Emission Industry

Low-emission industry refers to industrial activities that minimize environmental harm by lowering greenhouse gas emissions and air pollutants associated with a given product end-use category.5 Low-emission industry not only provides emissions reduction and associated health benefits but also supports economic independence and competitiveness for U.S. industries in domestic and global markets that value low-emission products.

Strategic investments in low-emission industrial technologies have the potential to invigorate American industry, particularly in communities that have experienced decades of decline due to deindustrialization. Since 1979, domestic manufacturing employment has decreased from 22 percent of total (non-farm) U.S. employment to just 8 percent as of March 2025.6 This steep reduction in industrial jobs has contributed to the economic stagnation of former manufacturing hubs.7 Low-emission industry can reverse these trends by offering new types of industry, such as manufacturing

facilities for batteries or electrolytic hydrogen production facilities, which offer new opportunities for high-quality, stable jobs in regions that have historically depended on industry. Further, modernizing existing industrial facilities can provide sustained, long-term opportunities for workforce development.

Upgrading or building new low-emission industrial facilities can also substantially enhance a state’s fiscal health. Such projects grow the local tax base, contribute to property and payroll taxes, and often lead to additional private investment. Further, global and domestic industrial competitiveness increasingly depends on low- emission products, which offer a competitive advantage and premium prices to U.S. industries if they utilize clean technologies. As global and domestic buyers demand low-emission products, states with forward-thinking industrial policy will be best positioned to retain and attract advanced manufacturing operations.

Low-emission industry also has strategic national importance. Reducing dependence on foreign fossil fuel supplies and imported materials enhances U.S. energy and materials security while reducing exposure to volatile global market prices. Industries such as steel and cement play essential roles in defense, infrastructure, and energy system resilience. This makes their emissions reduction not just an environmental imperative but a matter of national security. Targeted state and federal support are critical to help industries modernize and reduce pollution. Recent federal investments have driven major progress in low-emission industry and competitiveness. However, near-term political uncertainty threatens to delay capital investments, making state-level action discussed in this report even more important to ensure stability and maintain momentum.

Pillars of U.S. Industry

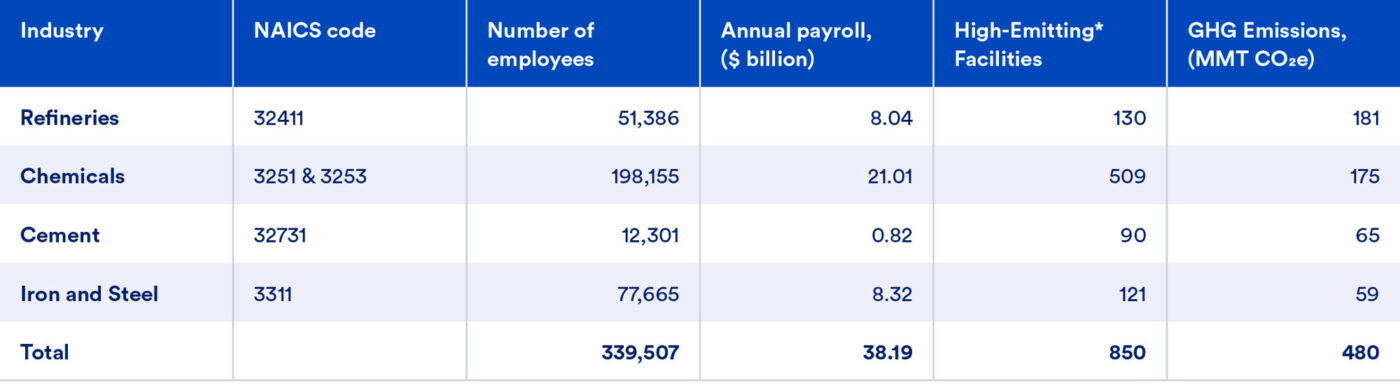

Though industrial activity spans many sectors and influences emissions reduction across the economy, this report focuses on four key industries, referred to as industrial subsectors—chemicals, refineries, cement, and iron and steel—due to their outsized contributions to both economic output and greenhouse gas emissions. These industries are foundational to the U.S. economy, as they employ approximately 340,000 workers and serve as essential inputs to a wide range of downstream sectors.8 Together, they account for approximately 40 percent of total U.S. industrial emissions, making them critical to any serious emissions reduction effort.9 Beyond their emissions profiles, their technological and operational characteristics also present overlapping challenges, including reliance on high-temperature processes, substantial process emissions, and intricate supply chains—often concentrated within large, integrated industrial complexes. Moreover, these subsectors tend to have limited viable product substitutes, are frequently exposed to international trade pressures, and are often situated in politically and economically strategic regions. These factors make them both high-impact and politically salient targets for tailored, state-level low-emission industry policies.

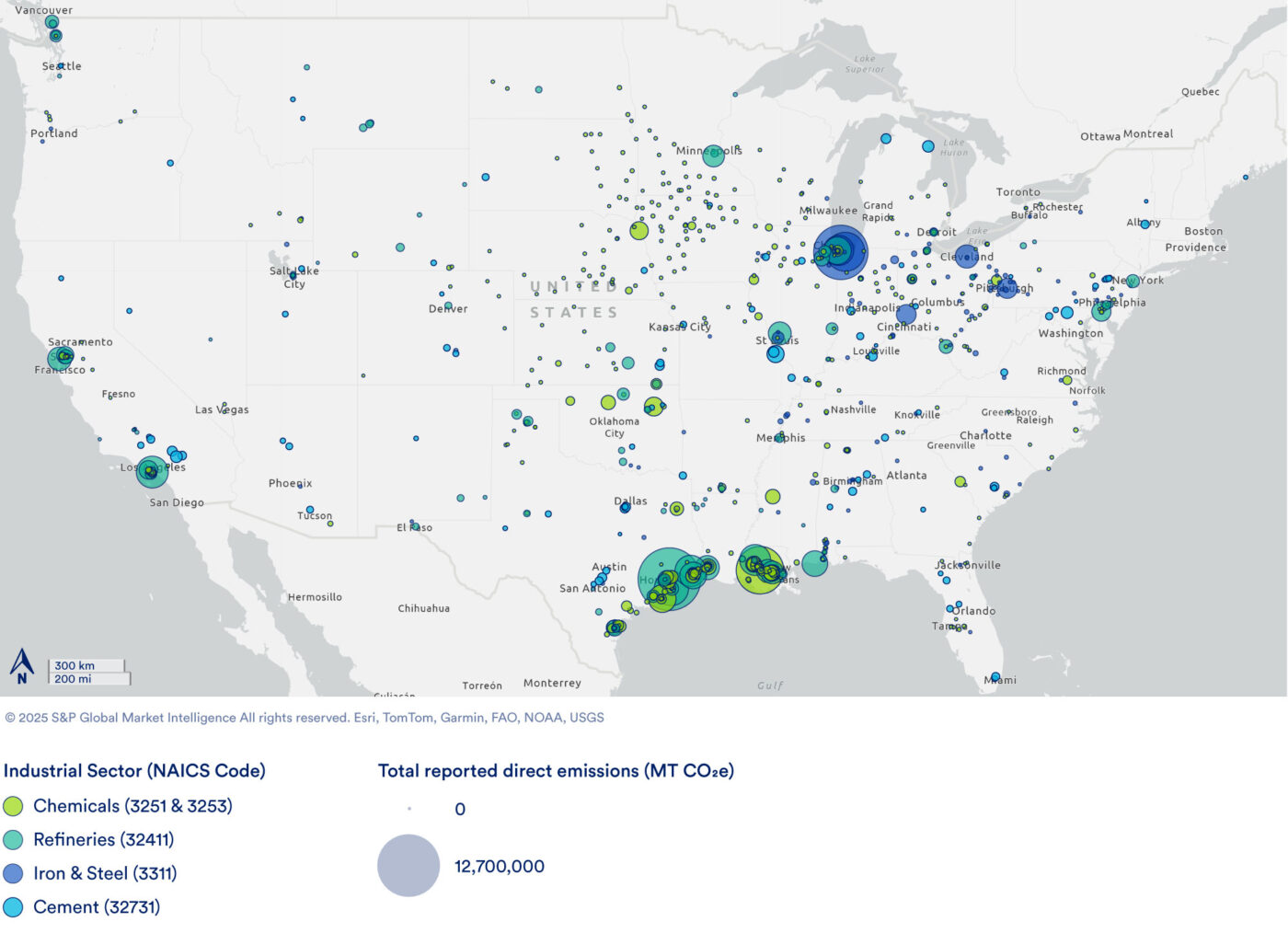

This section provides a high-level description of the industrial processes constituting each subsector and describes the major products, types of facilities, and types of industrial equipment for each. The scope of each subsector is classified according to their designation within the North American Industry Classification System, or NAICS.10 Table 2 summarizes key economic and environmental data for each of the four subsectors, including the number of employees, annual payroll, total number of high-emitting facilities, and annual greenhouse gas emissions. Figure 1 illustrates the distribution of facilities across the United States, categorized by industry sector. The size of each marker signifies the magnitude of direct greenhouse gas emissions.

Table 2: Summary of economic (2022) and emission data for subsectors of interest (2023)

Sources: U.S. Environmental Protection Agency, Facility Level Information on GreenHouse gases Tool (Available at https://ghgdata.epa.gov/ ghgp/main.do?site_preference=normal); U.S. Census Bureau, County Business Patterns, 2022 (Available at https://www.census.gov/programs- surveys/cbp/data/tables.html).

Figure 1: Chemicals, refining, cement, and iron & steel facilities direct emissions (MT CO2e)

Petroleum Refining

The petroleum refining industry11 processes crude oil into many products including petrochemical feedstocks and essential fuels such as gasoline, diesel, jet fuel, and biofuels that are crucial for transportation and commerce. Refining involves heating crude oil in distillation columns to separate it into various fractions based on their boiling points. Subsequently, processes like cracking and reforming transform heavier fractions into lighter, more valuable fuels. Reforming processes rearrange molecular structures to improve fuel quality, while hydrocracking uses hydrogen under controlled pressures and temperatures to break down large hydrocarbon molecules into smaller, more valuable molecules. Key units include steam methane reformers (SMRs), fluidized catalytic crackers (FCC), catalytic reformers, and hydrocrackers.Petroleum refining supports the U.S. economy by providing essential fuels fundamental to trade, transportation, and overall economic activity. Refineries employ approximately 51,000 workers nationwide, stimulate broader economic activities, and are critical to economic and energy security.12 According to the U.S. Bureau of Labor Statistics’ National Employment Projections, nationwide employment in the petroleum and coal products manufacturing industry is expected to decrease by three percent between 2023 and 2033.13 Texas, Louisiana, California, Illinois, and Washington are the top five states with the highest emissions from the refining sector. Together, these states account for 71.5 percent of the 181 million metric tons of carbon dioxide equivalent (MMT CO2e) emitted by refineries in 2023. Emissions from on-site hydrogen production at refineries are included within the refining sector totals.

Table 3 shows the top five states and emissions quantities. For the purposes of this analysis, petrochemicals are considered distinct from refinery products; they are included as part of the chemical manufacturing industry since they are often produced on the site of a chemical plant using standard chemical manufacturing processes.14

Table 3: Top five states with highest direct GHG emissions from the refining sector (NAICS 32411) (Metric Tons CO2e)

Chemical Manufacturing

The chemical manufacturing industry15 produces essential chemical building blocks used in numerous products, including plastics, fertilizers, and synthetic materials. Primary products include the following:

- Petrochemicals such as plastic precursors (ethylene and propylene) and cyclic aromatics like benzene, toluene, and xylene (BTX)

- Industrial gases including hydrogen

- Fertilizers including ammonia and urea

- Chlor-alkali chemicals

- Ethanol

- Other organic and inorganic chemicals

Facilities typically use large reactors and energy-intensive processing equipment, including distillation columns, steam methane reformers (SMRs), steam crackers, and electrolyzers. Chemical manufacturing typically involves converting raw materials such as natural gas, petroleum, and minerals to a variety of products through chemical reactions and separations under controlled temperature and pressure conditions. For example, steam methane reformers produce hydrogen from natural gas; steam crackers transform hydrocarbons into petrochemicals such as ethylene; and electrolyzers split molecules such as sodium chloride into chlorine and sodium hydroxide. This subsector is vital to the U.S. economy, supporting industries such as agriculture, automotive, construction, pharmaceuticals, and consumer products. It also employs a substantial workforce—approximately 198,000 jobs—and significantly contributes to U.S. exports.16,17 According to the U.S. Bureau of Labor Statistics’ National Employment Projections, nationwide employment in the chemical manufacturing industry is expected to increase by 2.7 percent between 2023 and 2033.18 Texas, Louisiana, Iowa, Oklahoma, and California are the top five states with the highest emissions from the chemicals sector. Together, these states account for 73.8% of the 175 MMT CO2e emitted by chemical manufacturing facilities in 2023. Table 4 shows the top five states and emissions quantities.

Table 4: Top five states with highest direct GHG emissions from the chemicals sector (NAICS 3251 & 3253) (Metric Tons CO2e)

Cement Manufacturing

The cement manufacturing industry19 produces Ordinary Portland Cement (OPC), masonry cement, and other hydraulic cements. Cement acts as the critical binding agent in concrete and is essential to construction projects such as roads, bridges, and buildings. The production process involves crushing limestone and minerals, heating them in pre-calciners and rotary kilns to form clinker, and grinding the clinker into cement powder.

In cement manufacturing, crushed limestone and other minerals are heated in rotating kilns at high temperatures (approximately 1450°C) to produce clinker—a precursor to cement. During this calcination process, limestone emits carbon dioxide as it decomposes. The resulting clinker is cooled, ground, and mixed with additives such as gypsum to produce cement.

Concrete is the most widely used building material globally. Cement manufacturing employs approximately 12,000 workers nationwide, underpinning a large construction industry critical to both state and national economies.20,21 According to the U.S. Bureau of Labor Statistics’ National Employment Projections, nationwide employment in the nonmetallic mineral manufacturing industry as a whole is expected to increase by 2.5 percent between 2023 and 2033.22 Texas, California, Missouri, Florida, and Alabama are the top five states with the highest emissions from the cement sector. Together, these states account for 45.1% of the 65 MMT CO2e emitted by cement manufacturing facilities in 2023. Table 5 shows the top five states and emissions quantities.

Table 5: Top five states with highest direct GHG emissions from the cement sector (NAICS 32731) (Metric Tons CO2e)

Iron and Steel Manufacturing

The iron and steel manufacturing industry23 produces essential materials fundamental to construction, infrastructure, transportation, and manufacturing.

Steel is primarily made through two methods:

- Blast Furnace-Basic Oxygen Furnace (BF-BOF): Converts iron ore into steel using coke as a fuel and reductant. Although energy-intensive, it produces high-quality steel, including for automotive and infrastructure use.

- Electric Arc Furnace (EAF): Primarily melts recycled steel scrap using electricity.

Steel production via BF-BOF begins by converting iron ore into molten iron using coal-derived coke in blast furnaces. This molten iron is then refined into steel using oxygen in basic oxygen furnaces. In contrast, EAF steelmaking involves melting scrap metal with electric arcs, substantially reducing emissions and energy use compared to traditional methods.

Major products include flat steel (coils, plates), long steel (pipes, beams), and ferroalloys (such as ferromanganese, ferrochromium, and ferrosilicon). Key equipment comprises BF-BOFs, EAFs, direct reduced iron (DRI) furnaces, and rolling and casting equipment. The steel sector is essential for domestic infrastructure projects, automotive manufacturing, and national security with approximately 78,000 employees.24,25 According to the U.S. Bureau of Labor Statistics’ National Employment Projections, nationwide employment in the iron, steel, and ferroalloy manufacturing industry as a whole is expected to increase by 3 percent between 2023 and 2033.26

Indiana, Ohio, Pennsylvania, Alabama, and Illinois are the top five states with the highest emissions from the cement sector. Together, these states account for 80.8% of the 59 MMT CO2e emitted by iron, steel, and ferroalloy manufacturing facilities in 2023. Table 6 shows the top five states and emissions quantities.

Together, these four subsectors are vital to the U.S. economy. They are major employers, provide essential products for everyday life, and are integral to countless other industries. Technological innovation and state policies are creating effective pathways to reduce emissions from these industries while maintaining economic competitiveness.

Table 6: Top five states with highest direct GHG emissions from the iron and steel sector (NAICS 3311) (Metric Tons CO2e)

SECTION 2

Technology Pathways

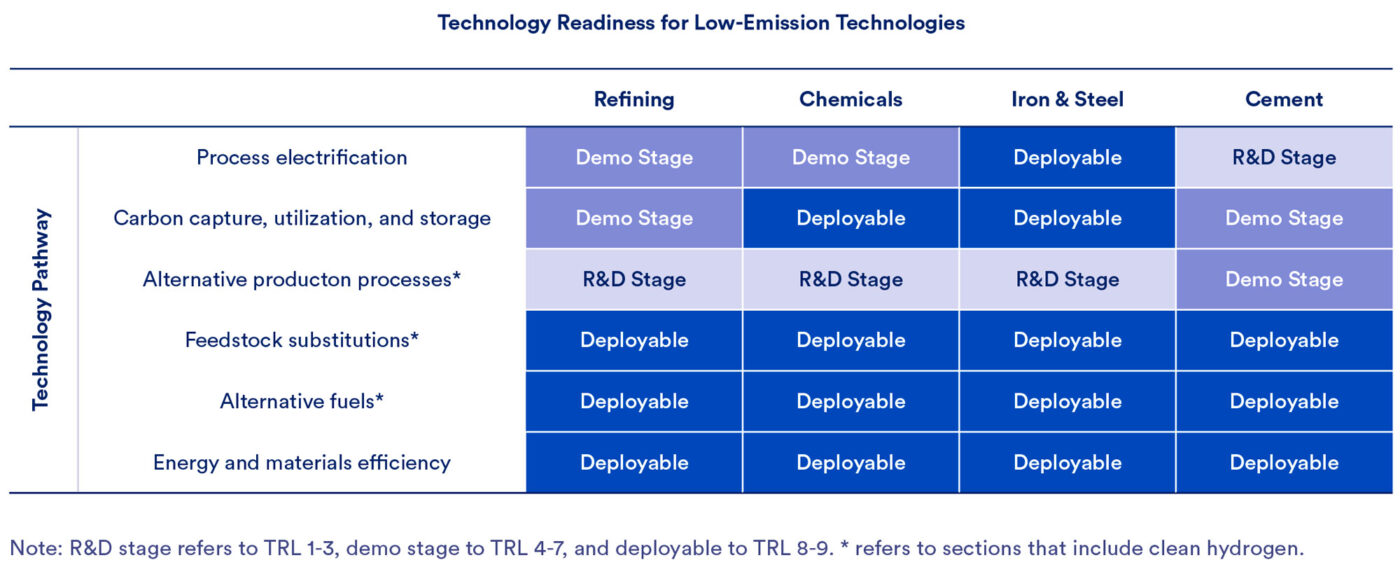

Technological innovation helps to ensure industry remains competitive in a low-emission economy. This section explains the leading technology pathways, their current development status, and their relevance within each of the four subsectors considered in this report. The development status of a particular technology is indicated by its Technology Readiness Level (TRL), which provides a standardized scale from 1 to 9 to assess its market maturity, where TRL 1 indicates basic research and TRL 9 reflects a technology fully proven and operational in commercial applications.27

While TRLs are a useful measure of technical maturity, they may not account for critical real-world deployment factors such as input supply, infrastructure readiness, or market conditions. As such, policies must address not only technical scaling but also the economic, logistical, and regulatory barriers that shape the pace and success of low-emission technology deployment. Table 7 summarizes clean technology pathways and their readiness for heavy industry. For subsector-specific details on each technology pathway, refer to Appendix B: Clean Technology Pathways – Subsector Detail.

Table 7: Technology pathways for low-emission industry, with subsector mapping

Process Electrification

Process electrification refers to the replacement of emissions intensive heat and energy sources with electric technologies, ideally powered by affordable, zero- and low-emission electricity. This strategy is central to low-emission industry because it enables emissions reductions across sectors without fundamentally altering end products. In many cases, it can also dramatically reduce or eliminate other non-greenhouse gas air pollutants associated with combustion of fuels and feedstocks, thereby improving health outcomes in surrounding communities. The pace of reducing emissions in the electricity sector and current access to zero- and low-emission electricity varies widely across regions due to differences in state policies, resource availability, and infrastructure constraints; nonetheless, in many grid regions today (and more in a future, higher renewables electric grid), process electrification will result in substantial GHG emission reductions.28

While electrification can offer substantial emissions abatement (particularly when coupled with zero- and low-emission electricity), it faces practical challenges in many industrial settings, including high-temperature requirements, retrofitting costs, and increased electricity demand. Electrification technologies range from mature solutions, such as Electric Arc Furnaces (EAF) in steelmaking, to early-stage innovations such as electric kilns for cement and electric steam crackers for chemicals. Industrial heat pumps are commercially mature (TRL 9) and highly effective for heating applications typically below 200°C but are generally not suitable for the high-temperature demands of heavy industry.29 Most heat requirements in sectors such as cement, steel, chemicals, and refining exceed this threshold, necessitating the application of existing technologies such as resistive, induction, plasma, or microwave heating within the industrial sector.

While TRLs for electrification vary widely by application, with decreasing emissions intensity of the electrical grid and supportive infrastructure investment, electrification represents a transformative pathway for industrial emissions reduction.30

Carbon Capture, Utilization, and Storage

Carbon capture, utilization, and storage (CCUS) refers to the capture of carbon emissions with two possible end uses: permanent sequestration, where captured CO₂ is stored deep underground in geological formations; or utilization, where CO₂ is used as an input in other products or industrial processes. This report uses the acronym CCUS to refer generally to both types of carbon capture projects. CCUS is a critical tool for industrial emissions reduction, especially in sectors with unavoidable process emissions or limited alternatives for fuel-switching. While not a one-size-fits-all solution, CCUS can enable continued operation of existing facilities while substantially lowering their emissions footprint.

There are three main types of CCUS technologies:31,32,33

- Pre-combustion capture removes CO₂ before fuel is burned, typically through a process that gasifies fuel to produce hydrogen and CO₂, such as in hydrogen and ammonia production.

- Post-combustion capture scrubs CO₂ from flue gases after combustion and is widely deployable as a retrofit solution across many industrial sectors.

- Oxy-combustion burns fuel in pure oxygen, resulting in a more concentrated CO₂ stream that simplifies capture but requires more specialized equipment.

The United States currently leads the world in installed CCUS capacity, with 19 commercial-scale facilities with combined capture capacity of 22 million tonnes per annum (MTPA) in operation and over 200 MTPA in announced projects as of 2024.34,35 Full deployment on industrial applications will require expanding CO2 transport networks, potentially 30,000 to 96,000 miles of pipeline, and accelerating the permitting and development of underground storage, e.g., Class VI wells. Federal incentives such as the section 45Q tax credit and funding from the IIJA36 and IRA37 are already driving billions of dollars in investment and enabling project deployment in sectors including cement, refining, hydrogen, and steel. The U.S. Department of Energy (DOE) estimates the United States will need to capture and store between 400–1,800 MTPA of CO2 annually by 2050 to stay on track for net-zero goals.38,39

Alternative Production Processes

Alternative production processes refer to fundamentally new methods of manufacturing industrial materials that break from traditional fossil-fuel-based, high-emissions pathways. These technologies aim to eliminate or drastically reduce combustion-related and process emissions by rethinking both the chemical inputs and physical steps used in production. Examples include hydrogen-based directly reduced iron (H2-DRI) in steelmaking, electrochemical cement production, and non-fossil feedstock-based chemical processes.

While not yet widely commercialized, these innovations hold the potential to deliver deep emissions reduction, often approaching zero emissions when powered by clean electricity. Scaling these processes will require extensive investment in new infrastructure, low-carbon feedstock supply chains, and long-term market transformation, but they represent some of the most promising avenues for reducing emissions in hard-to- abate industrial sectors.40

Alternative production pathways for heavy industry have the potential to reduce costs relative to traditional processes by leveraging technological advancements that can be rapidly scaled. While these new methods are still emerging, pilot projects are crucial for gaining experience and achieving learning-related cost reductions. The potential for cost savings depends on the technology’s complexity; as shown in Figure 2, simpler, modular technologies such as electrochemical processes (Type 1) tend to have higher learning rates with more rapid cost declines, whereas more complex, customized systems such as CCUS (Type 3) may only realize moderate savings due to their complexity and customization needs.

Figure 2: Framework for understanding potential of energy technologies to achieve learning-based cost savings

Feedstock Substitutions

Feedstock substitution involves replacing conventional raw materials (often fossil-based or emissions-intensive) with lower-carbon, recycled, or bio-based alternatives. This pathway targets process emissions that arise from chemical reactions intrinsic to many industrial processes (e.g., calcination in cement or reforming in chemicals) without necessarily requiring a complete redesign of production systems. Substitutions can include waste- derived inputs such as fly ash,41 slag, or biomass residues; non-carbonate minerals such as magnesium silicates; or carbon-neutral inputs such as captured CO₂ or low-emissions hydrogen. These substitutions may serve multiple roles: reducing the emissions intensity of inputs, altering chemical pathways to avoid CO₂ release, or enabling downstream electrification.

While some feedstock substitutions are already in widespread use (e.g., scrap steel in steelmaking and fly ash and slag in cement), others remain in early stages of research and demonstration. The TRL for feedstock substitution ranges widely from TRL 4 to 9, depending on the material, process integration needs, and market availability.41 As such, feedstock substitution serves as both a near-term emissions reduction tool and a long- term enabler for deeper industrial transformation.

Alternative Fuels

Alternative fuels are energy sources used to replace conventional fossil fuels that, depending upon the life- cycle analysis of emissions, can lower the emissions intensity of generating industrial heat—a major source of direct emissions across heavy industry. These include biomass-derived fuels, certain waste-derived fuels, some renewable natural gas (RNG), low-emissions hydrogen, and low-emissions-hydrogen-derived fuels.43 The emissions reduction potential of alternative fuels depends considerably on their life-cycle emissions, local availability, and compatibility with existing infrastructure. In some cases, they can be blended with fossil fuels to incrementally reduce GHG emissions or, with more extensive retrofits, fully displace traditional fuels. The role of alternative fuels is especially important in high- temperature applications that are difficult to electrify in the near term. Their deployment can serve as both a transitional bridge and a long-term complement to deeper decarbonization technologies.

While some waste-derived fuels and conventional biofuels are already commercially available and widely used in some industries (TRL 8–9), the availability of advanced biofuels, low-emissions hydrogen, and synthetic e-fuels are still developing and face infrastructure, supply chain, cost, and efficiency barriers.44,45 TRLs for the use of alternative fuels vary by application and while useful for gauging technical maturity, do not fully capture real-world scalability. Even technologies nearing commercial readiness may face significant constraints related to fuel supply, infrastructure buildout, and energy inputs. For example, bioenergy (solid, liquid, gaseous) pathways in some regions may be constrained by the availability of sustainable biomass and related supply chains, while low-emission hydrogen-based fuels depend on access to clean electricity, electrolyzers, carbon capture equipment, sequestration facilities, and/or supportive delivery infrastructure.

Energy and Materials Efficiency

Energy and materials efficiency encompass a range of strategies aimed at reducing the energy and resource intensity of industrial production. This includes equipment upgrades (e.g., high-efficiency motors, heat exchangers), process optimization (e.g., improved controls, heat integration), and better use of materials (e.g., reducing overdesign, extending product life, circularity). These measures are generally low- cost, commercially mature (TRL 9), and often deliver immediate emissions reductions without requiring major changes to core production methods.46,47

While individual interventions typically yield modest reductions, their cumulative potential is substantial, particularly when deployed alongside other emissions reduction strategies. Efficiency improvements also reduce demand on electricity and fuel infrastructure, making them a foundational enabler of broader industrial transformation. Importantly, materials efficiency measures such as reducing waste, increasing recyclability, or extending product lifetimes can also reduce embodied emissions, especially in sectors such as cement and steel where product demand is closely tied to infrastructure development.48,49 However, investments in efficiency alone may inadvertently extend reliance on emission intensive systems by improving their economic viability and can trigger rebound effects where efficiency gains are offset by increased production or consumption. Furthermore, efficiency measures on emissions-intensive processes, while valuable, cannot alone achieve complete emissions reduction.

SECTION 3

U.S. Policy Landscape

Over the past several years, the United States has experienced unprecedented growth in low-emission industry, fueled by the extensive technological innovation, landmark federal investments, and a surge of state-level policy mechanisms. In a highly uncertain federal political environment, states across the political spectrum are advancing a diverse array of industrial innovation strategies to drive economic growth, enhance competitiveness, and accelerate emissions reductions. This section examines the current federal and state policy context, highlighting bipartisan trends and the interplay between national initiatives and state-led action.

Federal Industrial Policy Context

From 2021 to 2024, the United States saw historic investment in clean industry and manufacturing, largely driven by the bipartisan Infrastructure Investment and Jobs Act (IIJA) and the Inflation Reduction Act (IRA).Between August 2022 and May 2025, as many as 2,369 new large-scale, low-emission energy and industrial facilities had opened across the U.S., attracting $321 billion in private capital investment.50,51,52 The IIJA and IRA targeted the full innovation pipeline and spurred investment through funding for research and development, pilot projects, and demonstrations; expanded tax credits; cost-sharing and loan programs; and new federal offices for implementation. The initiatives are supported by federal, state, and local governments, national labs, certification organizations, and industry partnerships, reflecting the cross-sector coordination needed to scale low-emission solutions.53

More recently, Congress and the administration took steps to remove or weaken many clean energy tax credits and programs in these laws, by passing H.R.1. The law accelerates phase-outs for wind, solar, and hydrogen tax credits, imposes stricter domestic content and sources rules on all energy tax credits, and rescinds all unobligated funding for IRA programs. Additionally, the future of previously obligated funds remains uncertain due to administrative capacity constraints and the forthcoming federal appropriations process.

Though the future of these programs is uncertain, IIJA initiatives relevant to low-emission industry include the following:

- New offices within DOE, such as the Office of Clean Energy Demonstrations and the Sustainable Manufacturing Initiative, created to promote early-stage research, development, and demonstration, and facilitate the technology-to-market process.54

- $6.3 billion for the Industrial Demonstrations Program to support the demonstration of emerging technologies at commercial scale. 18 of the 31 projects have been canceled as of May 30, 2025.

- $2.54 billion for carbon capture demonstration projects. two of the three full-scale demonstration projects which were awarded in 2024, have been canceled by DOE as of May 30, 2025.55

- $937 million for carbon capture large scale pilot projects. As of May 30, 2025, 3 of 4 projects awarded in 2024 were cut by DOE.

- $7 billion to create regional clean hydrogen hubs, which aim to accelerate clean hydrogen production for use as dispatchable power, energy storage, and reducing emissions in heavy industries and transportation. 7 hubs have been announced, each focusing on different clean hydrogen production methods56 and industrial users such as refining and fertilizer production.

- $2.1 billion for carbon dioxide pipelines were allocated through the Carbon Dioxide Transportation Infrastructure Finance and Innovation Program—via federal loans, loan guarantees, grants, and administrative expenses, thereby reducing financing risks and encouraging private sector investment. The first $500 million tranche opened in May 2024, but no applications were received by DOE.

- Numerous policies that support advanced and lower- carbon materials, including $310 million in grants for state and local procurement.

The IRA included policies that promote industrial innovation at the state level,57 including the following:

- $100 million through 2026 to the Environmental Protection Agency (EPA) for a voluntary low-carbon labeling program for construction materials, developed in collaboration with the Federal Highway Administration (FHWA) and the General Services Administration (GSA).

- Grants and technical assistance to manufacturers for measuring and disclosing embodied carbon in products, in addition to $2.15 billion in IRA funding through 2026 for the use of low-carbon materials in federal buildings.

- $975 million to support emerging sustainable building materials technologies.

- $1.2 billion for road construction materials with substantially lower emissions than traditional options under FHWA’s Low Carbon Transportation Materials Program.

- $5.8 billion for DOE to assist eligible entities in purchasing, installing, or retrofitting advanced industrial technologies in energy-intensive industries such as steel, cement, and chemical production. DOE prioritizes projects based on expected pollution reductions and community benefits. These funds, available through 2026, are expected to be used alongside private funds and those from IIJA to support a total of 33 projects.

- Greater incentives for CCUS, namely a higher 45Q tax credit for captured CO2 from $50 to $85 per ton for projects that permanently sequester CO2. This credit now applies to industrial emitters with a reduced capture threshold from 25,000 to 12,500 metric tons of CO2 and extended the credit through 2032.58

- Expansion of several other tax credits relevant to the industrial sector, including the 45V production tax credit for low-emission hydrogen, the 45Z clean fuel production credit for alternative biofuels and biodiesel, and the 48C advanced energy project credit, which includes a category of industrial or manufacturing retrofits.59

Additionally, the federal government started working to enhance rules governing the pipeline transport of CO2. Over 5,000 miles of CO2 pipelines are already in operation under federal and state oversight, though expansion will likely be needed to support widespread industrial use of CCUS and move CO2 safely from source to geologic storage. Under the Biden administration, the Department of Transportation’s Pipeline and Hazardous Materials Safety Administration proposed new safety standards for CO2 pipelines; the rulemaking process has since stalled.

Though IIJA and IRA have helped significantly increased the number of planned projects, the future of federal support for these investments remains uncertain, leading to delays and cancelations of low-emission energy, industry, and infrastructure projects.60,61,62

State Industrial Policy Context

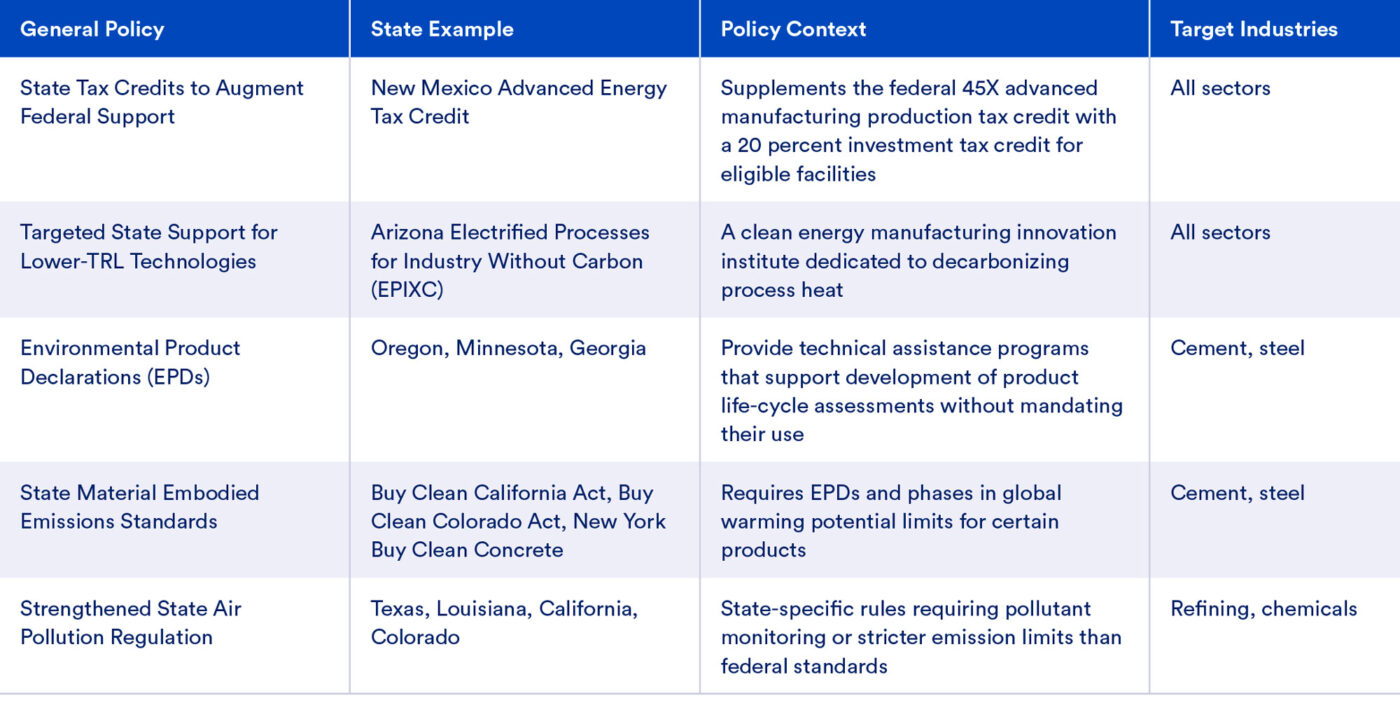

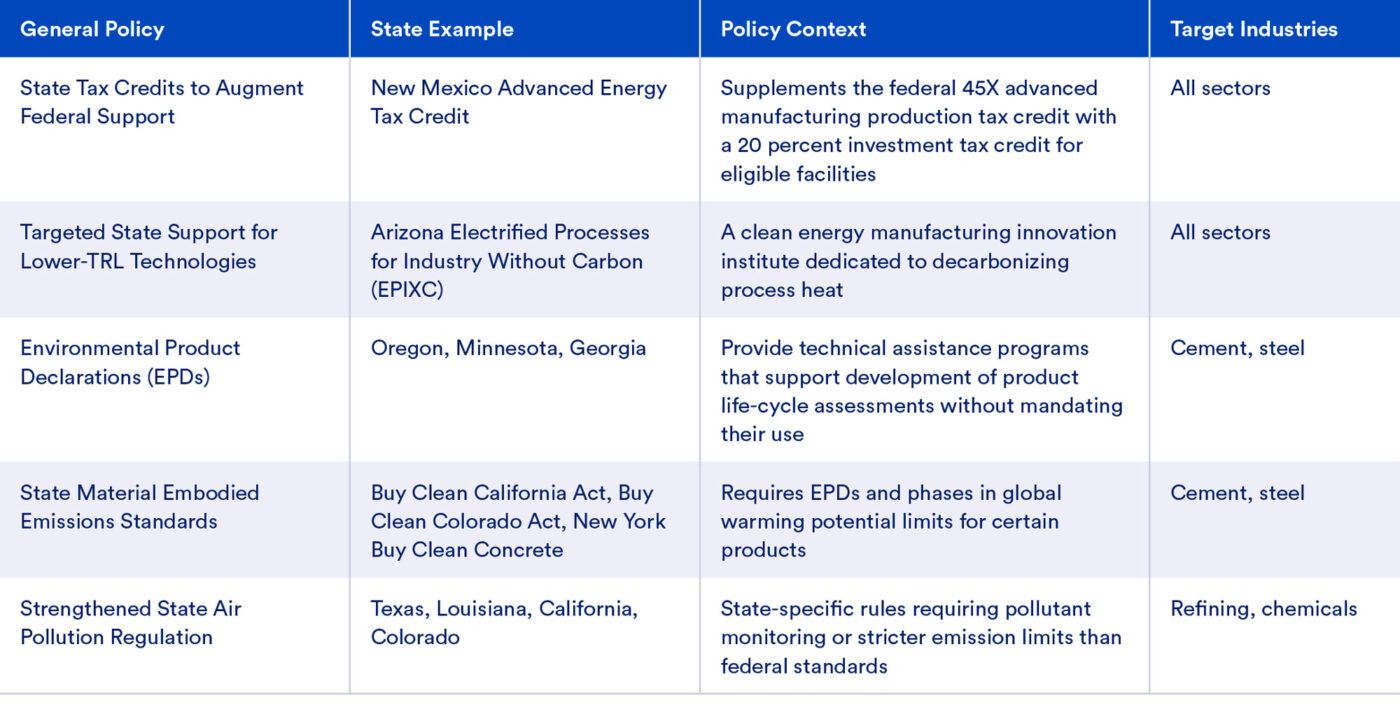

States are advancing a variety of low-emission industry policies that support economic growth and emissions reduction, achieving bipartisan objectives such as economic development, competitiveness, and technology innovation. Throughout this section, state- specific examples illustrate the diverse range of policies currently being adopted. Table 8 below highlights several of these, offering insights and lessons that can guide other states in effectively designing and implementing policies tailored to their unique industrial contexts.

Table 8: State-specific examples of low-emission industry policy leadership

SE C TION 4

State-Led Policies for Modernizing Heavy Industry

States have a diverse and expanding toolkit to accelerate low-emission industrial innovation that they can tailor to their unique economic landscapes and industrial bases. Because the industrial sectors covered in this report are primarily geographically concentrated in politically conservative states, it is critical that industrial policies be designed with those contexts in mind. This section explores the leading policy options—ranging from direct financial support and market-shaping demand policies to regulatory streamlining—that states are leveraging to drive innovation, stimulate demand for low-emission products and materials, and enable practical action across heavy industry. Appendix C outlines all policies covered in this section. For each policy discussed, the report describes how, and examples of where, the policy has worked and identifies key design considerations. Each policy is categorized by its type (legislative and/or administrative), timeline for adoption and impact (near- term: 1-2 years, medium-term: 3-7 years, and long-term: 7+ years), and level of public funding required (modest, moderate, and high).

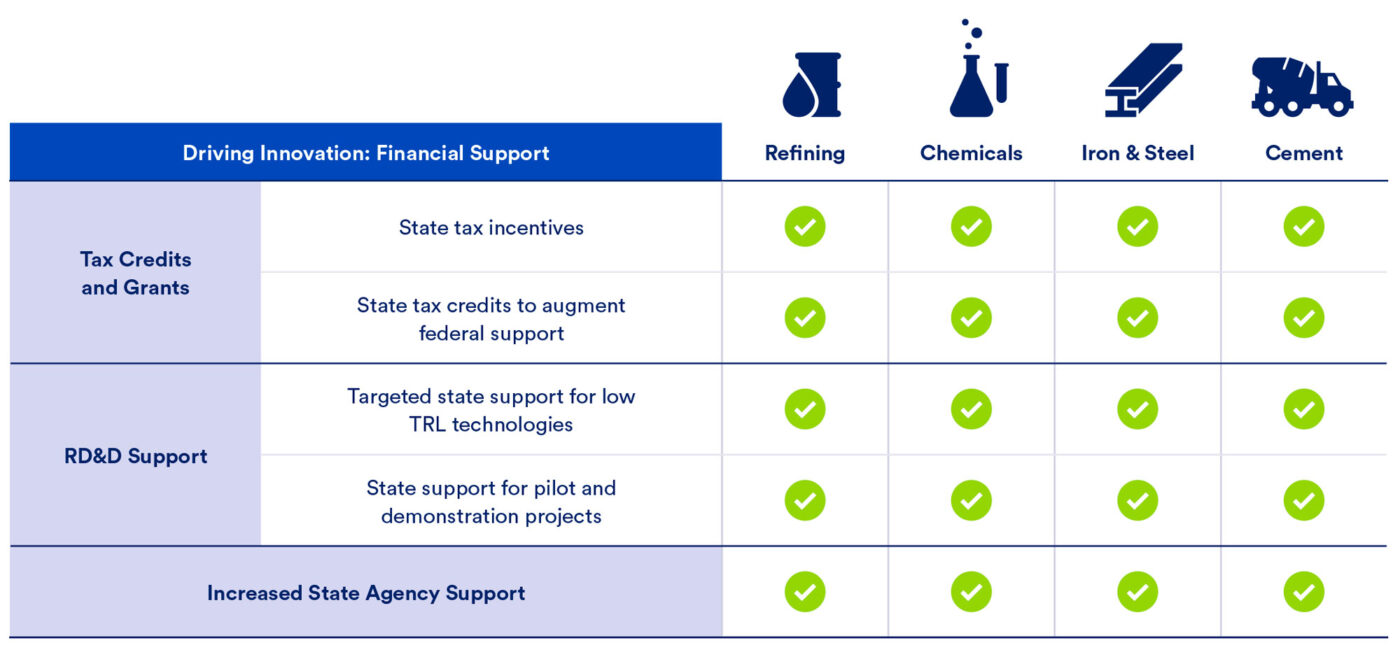

1. Driving Innovation: Financial Support

Targeted financial support helps unlock industrial innovation by de-risking emerging technologies and catalyzing private investment. This section explores the following five state-level policies that drive technology innovation through financial support.

- 1.1. State Tax Incentives: States offer tax credits, exemptions, or bonus incentives for low-emission technologies to reduce cost gaps and support industrial growth.

- 1.2. State Tax Credits to Augment Federal Support: States provide add-on credits to federal incentives that can close cost gaps for new technologies or enable more comprehensive, technology-neutral support.

- 1.3. Targeted State Support for Lower-TRL Technologies: States fund early-stage research and development for lower-TRL industrial technologies, building local innovation capacity.

- 1.4. State Support for Pilot and Demonstration Projects: States co-fund pilot and demonstration projects with private investment to de-risk early deployment, accelerate cost declines, and retain economic benefits in-state.

- 1.5. State Agency Support: State agencies provide technical assistance, workforce training, and policy coordination to scale low-emission industry and investment.

These financial support policies apply to all four industrial subsectors, which Figure 3 below highlights. This broad applicability results from strategic opportunities to advance supportive infrastructure (e.g., pipelines and grid infrastructure) and early- stage technologies across all subsectors. Importantly, each subsector can benefit from targeted financial interventions that accelerate technological innovation and deployment.

Figure 3: Financial support policies for low-emission industry, with subsector mapping

1.1 State Tax Incentives

Tax incentives can help close the cost gap between low-emission and traditional industrial products and technologies. These incentives could take a variety of forms, including tax credits, property tax exemptions, or credit adders for low-emission technologies in economic development programs. States have a long history of using tax codes to create incentives for businesses operating within their jurisdictions, so this approach is a well-established policy option that many states are already comfortable implementing. States can also tailor tax incentives to achieve additional policy goals by, for example, targeting the incentives to economically distressed zones to distribute economic activity more evenly throughout the state.

How and Where This Policy Has Worked

1.1.1 Property, Payroll, or Income Tax Credits:

States often offer property, payroll, or income tax credits or reductions to industrial facilities as an economic development incentive to make themselvesmore attractive business investment environments and to compete against other states. States could establish this type of tax incentive program specifically for industrial facilities that produce lower-emissions products. For example, states could offer low-emission manufacturing and industrial facilities an exemption from property taxes and arrange for these facilities to instead pay a lower amount through a payment in lieu of taxes (PILOT) program. States also could include credit multipliers for low-emission technologies in their existing economic development programs, encouraging the facilities who participate in these programs to produce lower-emissions products. Twenty-one states currently offer tax incentives specifically for manufacturing, so there is an opportunity to tailor these programs specifically to low-emission manufacturing.63 For example, the Industrial Tax Exemption Program in Louisiana offers an 80 percent property tax abatement for up to ten years on new capital investments made by manufacturers in the state.64

1.1.2 Investment Tax Credits:

Another option available to states is to offer an investment tax credit to industrial facilities when they purchase equipment they will use to manufacture low-emission industrial products. Investment tax credits allow a taxpayer to deduct a certain percentage of eligible investment costs from their tax liability. At the federal level, investment tax credits have been successful in increasing renewable energy deployment. At the state level, some states already have experience offering investment tax credits to manufacturing facilities. For example, Georgia currently offers an investment tax credit to manufacturing and telecommunications support companies that have operated in the state for at least three years. Companies that invest in recycling equipment, in pollution control, or in converting a defense plant to a new product are eligible for a 3 to 8 percent tax credit, and general equipment investments are eligible for a 1 to 5 percent credit.65

Georgia currently offers an investment tax credit to manufacturing and telecommunications support companies that have operated in the state for at least three years.

1.1.3 Accelerated Tax Depreciation Schedules:

States can offer accelerated tax depreciation schedules for low-emission industrial equipment. Accelerated tax depreciation decreases upfront costs by allowing firms to deduct capital expenditures from their taxable income more quickly than under straight line depreciation, thereby reducing corporate income tax payments. State corporate tax rates are typically much lower than the federal rate, which limits the magnitude of this benefit in most states. However, offering accelerated depreciation schedules for low-emission industrial assets could still provide a valuable tax benefit to companies.

1.1.4 Tax Equity Partnerships:

Tax equity partnerships allow companies to gain access to cash financing for projects that will be eligible for tax credits. The partnerships generally involve one party agreeing to assign the rights to claim tax credits to another party in exchange for an equity investment.66 According to the Congressional Research Service, this arrangement can be beneficial in cases when “tax credits are nonrefundable and the intended beneficiary of the tax credit has little or no tax liability (e.g., a nonprofit), or because the credits are delivered over multiple years whereas upfront funding is needed to break ground.67 State-sponsored tax equity partnerships can help to increase access to these benefits by combining state tax credits and risk guarantees with federal incentives, making projects more financially attractive to investors. This public-private partnership model could accelerate industrial modernization by mobilizing private capital at lower costs while sharing project risks with the state. While not previously implemented for low-emission industry, over 20 states provide state-sponsored tax equity through state low-income housing tax credit programs, partnering with investors to reduce upfront capital costs and make affordable housing projects financially viable.68

While not previously implemented for clean industry, over 20 states provide state-sponsored tax equity through state low-income housing tax credit programs, partnering with investors to reduce upfront capital costs and make affordable housing projects financially viable.

Implementation Strategies

| Policy Type | Legislative to authorize funding and establish program authority. Once authorized, state departments of revenue and economic development agencies would administer the tax incentive programs. |

| Duration | Near-term adoption, medium- to long-term impact. |

| Funding Required | High, depending on technology uptake, because many tax incentives provide ongoing payments to industrial producers and reduce net tax revenue. |

Policy Design Considerations

- Reduces government revenue: Tax incentives reduce government revenue because the businesses that receive them pay less in taxes. This effect may be partially offset by increases in other forms of tax revenue from economic activity driven by the industrial facility, such as increased state personal income and sales tax.

- Limited influence on corporate site selection: Tax incentives may not be the most important factor influencing where industrial facilities choose to locate. For example, availability of skilled labor and adequate land and infrastructure are two important drivers of corporate site selection that are not typically affected by tax incentives.

- Risk of picking winners and losers: Typically, a state tax incentive benefit would detail the specific equipment or investment type that qualifies. This may lead to perception of picking technology winners and losers. This could undermine public support for these tax credits. However, states can avoid this concern by making the tax credits broad and applicable to a range of low-emission industries and technologies.

1.2. State Tax Credits to Augment Federal Support

In addition to offering their own tax incentives as discussed above, states can offer credit adders to augment existing federal tax credits. Given that there will likely continue to be a cost premium for low- emission industrial products, establishing incentives that make these technologies cost-effective for industrial facilities will be key to their wider deployment. However, federal tax credits may not be sufficient on their own to incentivize meaningful levels of investment in low-emission technology in many industrial sectors, especially as U.S. inflation has increased. State-level credit adders could help close the cost gap for low- emission technologies in sectors where adopting these technologies is more expensive than current federal incentive levels. Further, while most federal credits are technology specific, states can create technology- neutral tax credits tailored to complement federal support; this strategy could incentivize a chemical plant, for example, to pair state-supported electrification of low-temperature heating with federally supported CCUS for process emissions. Augmenting federal support helps states use their own funds more efficiently.

How and Where This Policy Has Worked

States can tailor additional incentives to meet their specific needs. For example, states could structure these adders either as production tax credits (per ton of low- emission product produced), as investment tax credits (cover a portion of the project capital costs), or as a tax credit designed to reward the producer for lowering facility or product emissions intensity. States could also target these incentives to specific industries—such as cement, petrochemicals, and refining—based on the subsector cost gap or economic relevance. In 2024, New Mexico enacted a 20 percent investment tax credit for manufacturing facilities that qualify for the federal 45X advanced manufacturing production tax credit.69

States can ensure that an industrial facility is able to stack the state and federal credits to make projects more financially viable. For example, the 45Q CCUS federal tax credit provides a financial incentive up to $85 per ton of captured CO2 from industrial facilities that permanently sequester the CO2. The cost of storing captured carbon in some industrial sectors, such as refineries and steel mills, can be similar to or even higher than $85.70 These sectors would benefit from higher state credit adders, or other financial incentives, such as voluntary carbon markets, to be fully cost-effective.

Notably, in 2025, New Mexico proposed legislation71 featuring a state production tax credit for $85/ton of CO2 reduced below a benchmark, along with a 10 percent investment tax credit for low-carbon industrial equipment. While the state-level $85/ton credit could not be stacked with the federal 45Q tax credit, the investment tax credit can be compatible with other federal tax credits. Although this bill did not pass, this bill could be considered in a future legislative session.

Implementation Strategies

| Policy Type | Legislative to establish new tax credits or authorize supplementary funding. |

| Duration | Near-term adoption; medium- to long-term impact. States could design credit adders that gradually phase out to avoid subsidizing technologies indefinitely. |

| Funding Required | Moderate to high, depending on level of technology uptake and state tax credit levels. |

Policy Design Considerations

- Setting credit at competitively attractive levels: A state supplementary tax incentive would have to be set at a level high enough to incentivize increased investment while avoiding being overly generous. Tailoring tax incentive levels and design to specific industries can help make efficient use of state funds. However, fully closing the cost gap for technologies, such as CCUS adoption in certain industries, may be prohibitively expensive for state governments. This approach may not be realistic unless the federal government further increases the value of credits.

- State monitoring and verification: With state funds at stake, state officials would want to ensure that recipients are abiding by compliance mechanisms, which could require additional staff and auditing expertise to ensure that recipients are accurately reporting emissions and investment. The state tax authorities could piggyback on federal reporting requirements and standards.

- Need for supporting infrastructure: Deployment of low-emission technologies depends on the availability of adequate transportation and storage infrastructure and offtakers, which may require additional state and federal support or reform.

1.3. Targeted State Support for Lower-TRL Technologies

While many low-emission industrial technologies are ready for deployment today, others are currently at lower TRLs and will require targeted research and development (R&D) to advance them to the point where they are ready for demonstration, eventual commercialization, and market take-off. States can play a valuable role in R&D of low-emission industrial technologies, both by conducting R&D directly and by providing funding to universities, private companies, and nonprofits for R&D activities.

State support for R&D builds a local knowledge base and may subsequently encourage industrial facilities to locate within the state once the technologies under development reach commercialization, creating economic growth and innovation hubs. By supporting a range of lower-TRL technologies, state can help ensure that key industries have multiple low-emission pathways available as technologies mature, preserving operational flexibility and strengthening economic resilience.

How and Where This Policy Has Worked

All 50 states already have budgets for R&D activities, and in 2023, total state agency spending on R&D was $3 billion.72 Most of this amount (76 percent) went to external organizations such as higher education institutions, private companies, and nonprofits.73 The remaining 24 percent was funding for R&D performed directly by state agencies.74 Currently, healthcare dominates state R&D expenditures, followed by environment and natural resource research and then research in the energy sector.75 In 2023, the five states with the highest total R&D budgets were California, New York, Texas, Florida, and Ohio.76 These and other states can build on the success of their existing R&D programs to dedicate additional funding to low-emission industrial technologies.

States can also provide R&D funding to supplement federal funding. For example, Arizona State University leads a clean energy manufacturing innovation institute, partially funded by the Department of Energy, dedicated to decarbonizing process heat, including in the iron and steel, cement, chemicals, and petroleum refining industries.77 Other higher education institutions that are partners of this institute include the University of Texas at Austin, Carnegie Mellon University, Missouri S&T, Texas A&M, Tuskegee University, NC State University, Navajo Tech University, and Stanford University. State governments can play a valuable role in providing supplemental funding to ensure that research efforts can continue, even with federal uncertainty.

Arizona State University leads a clean energy manufacturing innovation institute, partially funded by the Department of Energy, dedicated to decarbonizing process heat, including in the iron and steel, cement, chemicals, and petroleum refining industries.

Implementation Strategies

| Policy Type | Legislative to authorize funding. A combination of state agencies and partner organizations, such as higher education institutions, private companies, and nonprofits, would carry out the R&D. |

| Duration | Near-term adoption; medium- to long-term impact. |

| Funding Required | Medium; impact will scale with amount of funding provided. |

Policy Design Considerations

- Need to secure funding: Whether performed directly by state agencies or by partner organizations such as universities and private companies, R&D requires consistent funding. This funding involves an opportunity cost because government funds dedicated to R&D cannot be used for other purposes. Additionally, these funds should be committed for a long enough time horizon to incentivize R&D investments. State annual budgeting processes could complicate efforts to develop long-term funding streams.

- Emissions impact ramps up over time: Not all technologies will ultimately succeed, and the emissions reduction from R&D programs will be low at first until technologies progress to the point where they can be deployed at scale.

CASE STUDY 1: MISSOURI

Missouri Cement Decarbonization: Using Federal Grants to Accelerate Low-Carbon Innovation

Overview

In 2024, the Missouri Department of Natural Resources (DNR) released its Plan for Environmental Improvement Grants to guide the distribution of federal implementation funds through the U.S. EPA’s Climate Pollution Reduction Grant (CPRG) program.

The plan clearly establishes the framework for industrial decarbonization funding and highlights industrial sources—including cement—as major contributors to Missouri’s statewide emissions. The plan positions Missouri to leverage federal support for clean heat, fuel-switching, and emissions control technologies across hard-to-abate sectors like cement.

Policy Design

Through this plan, DNR invited local governments and planning commissions to submit project ideas in partnership with private industry, utilities, and community stakeholders. DNR also awarded subgrants of up to $10,000 to 14 regional partners to host workshops and gather input on community- prioritized emissions reduction strategies. Industrial decarbonization, including process upgrades and pollution control retrofits, was explicitly included as a priority project category. The plan’s inclusive structure creates a pathway for facilities such as Missouri’s four Portland cement plants to participate in CPRG-funded decarbonization through eligible public-sector sponsors.

Industry Stakeholders

Missouri is home to major cement producers including Continental Cement, Holcim, Buzzi Unicem, and Ash Grove. These companies operate facilities that contribute materially to Missouri’s industrial emissions and are well- positioned to pursue funding for retrofits, clean fuels, and supplementary cementitious materials (SCMs). While the plan does not name specific projects, the structure strongly encourages public-private collaboration that could support these low-emission pathways.

Expected Impacts

- Strong foundation for cross-sector collaboration that could support future cement decarbonization projects, including public-private grant applications.

- Increased institutional capacity at the regional level to manage large federal energy investments, especially through regional planning commissions and municipal utilities.

- Stronger alignment of industrial emissions priorities with federal funding streams, improving Missouri’s competitiveness for future DOE or EPA awards.

- Community co-benefits, such as local air quality improvements and retained industrial jobs in traditionally underserved or economically distressed regions.

Policy Rationale

- Targets near-term emissions reductions from major point sources, including cement kilns.

- Advances deployment of clean heat, alternative fuels, and materials efficiency in hard-to-abate sectors.

- Aligns with Missouri’s Priority Climate Action Plan, which identifies industrial processes as a top low-emission target.

- Leverages federal investment to build durable public- private infrastructure for long-term emissions planning.

- Missouri’s cement-related emissions rose from 2.5 MMT CO₂e in 2005 to 4.4 MMT CO₂e in 2021, making it a priority area for industrial emissions reductions.

- The plan aligns with CPRG goals to reduce both greenhouse gases and criteria air pollutants in sectors with large stationary sources.

- Collaborative project scoping through regional councils encourages local economic development while reducing emissions.

Case study citations provided in Appendix D.

1.4. State Support for Pilot and Demonstration Projects

While the policy described above targeted early- stage technologies that require further research and development, this policy addresses more mature technologies that need support in early-stage deployment. Specifically, it addresses government funding for pilot and demonstration projects to support technologies that are at a higher TRL and are ready for larger-scale demonstrations. While pilot and demonstration funding for emerging technologies has historically been provided primarily by the federal government, states can create similar incentives. State funding can provide a cost-share with industry to construct pilots that bring down costs for future projects by advancing technologies from “first-of-a-kind” to “nth- of-a-kind,” thereby unlocking learning-curve benefits. Funding for pilot and demonstration projects can help ensure that technologies, including those for which R&D takes place within the state, remain within the state into the commercialization stage and continue to bring jobs and economic benefits.

How and Where This Policy Has Worked

Government funding for pilot and demonstration projects generally supplements private funding and can play an important role in derisking technologies through building a road to financial bankability. Without state or federal support, emerging technologies can find it difficult to attract private capital for pilot and demonstration projects, due to their risk profiles. States could offer support similar to the Industrial Demonstrations Program (IDP), an IIJA- and IRA-funded program that provided $6 billion in federal funding to support 29 first-of-a- kind industrial projects across the country, leveraging an additional $14 billion of private investment for a federal cost-share of about 30 percent. The IDP was 10x oversubscribed, with over $60 billion requested in funding requested and $100 billion in industry cost share, indicating significant cross-sector interest.78

Though this program has been partially canceled, state governments could replicate this model to fund additional demonstration and pilot projects in industries most relevant to their local economies. One such approach is the use of state sovereign wealth funds to capitalize a low-emission industrial technology fund. The North Dakota Legacy Fund, established in 2010 and capitalized by 30 percent of state oil and gas tax revenues, is designed to ensure long-term financial stability beyond the state’s fossil fuel economy. North Dakota allocates a portion of its earnings to initiatives such as the Clean Sustainable Energy Fund, which supports carbon capture and low-emission technology projects.79

North Dakota allocates a portion of its [state oil and gas tax revenues, through the North Dakota Legacy Fund] to initiatives such as the Clean Sustainable Energy Fund, which supports carbon capture and low-emission technology projects.

Another financial support approach to lowering investment risk for low-emission industry is state-backed insurance guarantees that provide a backstop covering losses beyond a certain threshold. These guarantees reduce private insurers’ exposure and encourage them to insure innovative or higher-risk technologies that might otherwise lack coverage or face prohibitively high premiums.

Implementation Strategies

| Policy Type | Legislative to authorize funding. State agencies would administer the program in partnership with private companies. |

| Duration | Near-term adoption; medium- to long-term impact. |

| Funding Required | Moderate; impact will scale with amount of funding provided, and per-project costs are generally higher than for R&D. |

Policy Design Considerations

- Need to secure funding: A primary barrier to wider state support for pilot and demonstration projects is the need to secure dedicated, long-term funding.

- Available cost savings vary by technology: The goal of government-supported pilot and demonstration projects is generally to reduce costs for future projects by gaining experience constructing the technology at larger than bench-scale. Depending on the technology, a risk of funding pilot projects is that the projects may not yield hoped-for cost reductions. Technologies with low degrees of complexity and need for customization tend to have the highest learning rates, which is the percent reduction in project costs associated with each doubling of installed capacity.80 Some technologies that will be key to low-emission industry have high complexity and/or high requirements for customization. Consequently, these have lower potential for learning-curve savings.

- Emissions impact ramps up over time: The direct economic and emissions abatement impact of pilot projects will be small at first but will enable future reductions.

1.5. Increased State Agency Support

State agencies play a facilitating role connecting industrial facilities with technical assistance and workforce training, as well as building awareness for available government programs, including state tax credits and energy efficiency programs. The presence of a trained workforce in a state can help attract additional industrial facilities to the state, contributing to a positive feedback loop. State agencies also have a high-level planning role that includes communicating a state’s priorities and long-term commitment to fostering low- emission industry.

How and Where This Policy Has Worked

State agency support for industrial emissions reduction can take a variety of forms.

1.5.1. Technical Assistance:

One important role for states is to provide technical assistance to industrial companies. Some states provide technical assistance directly through their state agencies, which requires the agencies to have staff with specific technical expertise. Often a more efficient use of state resources is for states to play facilitative roles, connecting industrial companies with external partners that specialize in low-emission technologies. For example, Illinois proposed to establish a Clean Industry Concierge Program as part of its Climate Pollution Reduction Grant. The state would hire a third party to “help Illinois industrial facilities navigate, coordinate and access funding opportunities, get support in designing and implementing decarbonization measures, and provide strong guidance on industry best practices in efficient and cost-effective low- carbon technologies and processes.”81 The program would provide contractor and supply chain connections and education, strategic planning support, workforce training liaisons, and low-emission industry planning and stakeholder engagement.82

Illinois proposed to establish a Clean Industry Concierge Program as part of its Climate Pollution Reduction Grant. The state would hire a third party to “help Illinois industrial facilities navigate, coordinate and access funding opportunities, get support in designing and implementing decarbonization measures, and provide strong guidance on industry best practices in efficient and cost-effective low- carbon technologies and processes.”

States can also provide funding to technical assistance and workforce training programs at universities, including at existing Industrial Assessment Centers or Manufacturing USA centers. There are over 50 Industrial Assessment Centers across the country, which provide energy efficiency assessments to small- and medium- sized manufacturers, as well as grants to implement the suggested improvements. States could investigate expanding the mission of these centers to include low- emission technologies alongside energy efficiency.

In addition to the Industrial Assessment Centers, other universities have existing technical assistance programs that allow faculty and students to partner with the private sector and share their technical expertise. States could provide additional funding to deepen these programs’ focus on low-emission industrial technologies. Additionally, there are 18 Manufacturing USA centers across the United States. These serve as research centers for advanced manufacturing technologies and products and aim to develop public-private partnerships with universities, industry, and the federal government. More broadly, states can work to establish cross-state, regional, or national technical assistance partnerships to ensure that industrial players are able to take full advantage of knowledge sharing from innovations occurring in other parts of the country.

1.5.2. Financial Matchmaking

Access to capital can be a barrier to projects. States can help companies access capital by connecting them to private and public institutions that provide financing. Options include venture capital, philanthropic funding, state green banks, and community bonds. Sixteen states and the District of Columbia currently operate green banks, which are public, quasi-public, or nonprofit entities that leverage public and private capital to offer financing to projects that reduce GHG emissions.83 Several states also recently established State Energy Financing Institutions (SEFI) to leverage state dollars to bring federal Loan Programs Office financing to their states.84 Projects financed by SEFIs generally rely on a combination of state, federal, and private investments to achieve the full capital investment needed. The most appropriate financing source will depend on the length of time a project needs to achieve a return on the investment, as well as its risk level; public institutions are often able to offer more patient capital than private lenders. Green banks, for example, often offer loans at lower than typical market rate or take on risks that the private market would not accept, allowing them to target market gaps not served by private financial institutions.85

1.5.3. Tax Credit Accessibility Assistance:

Within their own agencies, states can work to improve the accessibility of programs targeted at industrial facilities, such as offering tax credit accessibility assistance and expanding energy efficiency and energy management programs offered through state energy offices.