Taking Stock of Energy and Climate Policy Since 2020

Key takeaways from CATF’s stock take

- Between 2020 and 2026, Congress enacted major climate and clean energy policy through budget reconciliation and broad bipartisan bills. The Biden administration partially implemented several of these landmark pieces of legislation prior to President Trump’s inauguration.

- In its first year, the second Trump administration aggressively targeted specific clean energy industries and technologies, especially wind, solar, electric vehicles, hydrogen, and building decarbonization, through a broad range of executive actions.

- The Trump administration has demonstrated more support for clean firm electricity generation sources (geothermal, nuclear fission, and fusion energy).

- Other clean energy and climate priorities, such as carbon management and electric grid investment, have seen mixed policy support from the Trump administration.

- Administration-wide personnel actions have reduced the aggregate federal workforce to its approximate size in 2020, with mounting evidence of long-term damage to the climate and clean energy federal workforce, as technical expertise has departed the federal government.

- Congressional Republicans have supported some but not all of the Trump administration’s efforts to roll back clean energy programs. In the One Big Beautiful Bill Act (OBBBA), key energy tax credits and select spending programs survived.

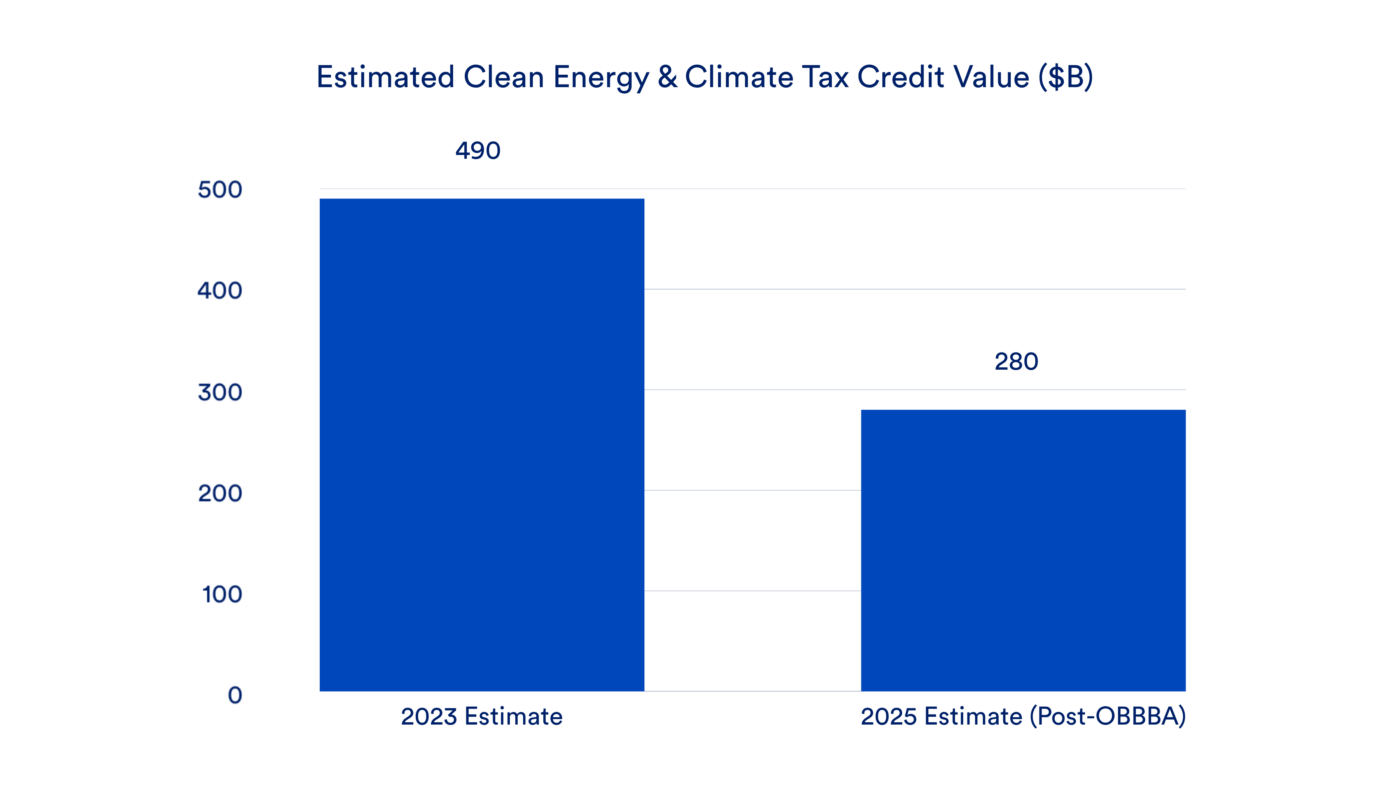

- The Joint Committee on Taxation estimates that the value of key clean energy tax credits (§§ 45/45Y, 48/48E, 45U, 45V, 45Q, 48C, and 45X) will be about 60% of their estimated value in 2023 – on the order of $280 billion dollars through 2034 (compared to JCT’s 2023 score of $490 billion).

- In 2025 and 2026, the bipartisan annual appropriations process has set topline funding levels higher than the those proposed in the President’s Budget Request, and some provisions constraining forward-looking executive discretion.

- The President’s Budget Request for Fiscal Year 2027 proposes significant cuts to key clean energy accounts, while emphasizing new policy areas including artificial intelligence and baseload power; the Congressional response through the annual appropriations process will determine whether the President’s proposal sets policy.

- Absent significant policy shifts in the immediate term, the United States will miss its near-term clean energy targets as the instability, uncertainty, and disinvestment in renewable energy sources and regulatory rollbacks take a toll. Rhodium Group, for instance, estimates that U.S. greenhouse gas emissions rose by 2.4% in 2025.

- In the longer-term, the bipartisan focus and support for emerging clean firm technologies (including, but not limited to, generation technologies such as geothermal, nuclear fission, and fusion energy) provides a source for optimism, with effective implementation.

Introduction

The first Trump administration pursued an all-of-the-above energy policy that skewed toward fossil deployment but encompassed renewables, including offshore wind. The second Trump administration has pivoted to a new energy policy vision. In its first year, the administration canceled billions of dollars in already-obligated funding for clean energy projects (and is reportedly considering canceling billions more); directed agencies to comprehensively slow the deployment of clean, affordable energy sources, particularly offshore wind; and sought to rescind or otherwise impair regulatory efforts to address air and climate pollution across the federal government. Meanwhile, the U.S. Congress passed, and President Trump signed into law, the One Big Beautiful Bill Act (OBBBA), which repealed some clean energy tax credits entirely, restricted some of the remaining tax credits, and rescinded unobligated grant funding for many clean energy provisions of the Inflation Reduction Act (IRA).

These executive and legislative actions undermine progress toward American clean energy leadership, energy affordability, and air pollution reduction. But a focus on the last year alone misses broader shifts in federal clean energy policy since 2020, and assessments that focus narrowly on the current administration’s actions risk obscuring bipartisan cooperation and agreement visible through congressional action, especially apparent in the most recent appropriations bills. An accurate assessment of these activities is required to understand the federal government’s likely policy trajectory in the years to come.

Clean Air Task Force (CATF) has initiated a wide-ranging effort to take stock of the last five years in federal climate and clean energy policy, which we expect to update as the current administration and 119th and 120th Congresses make new policy.

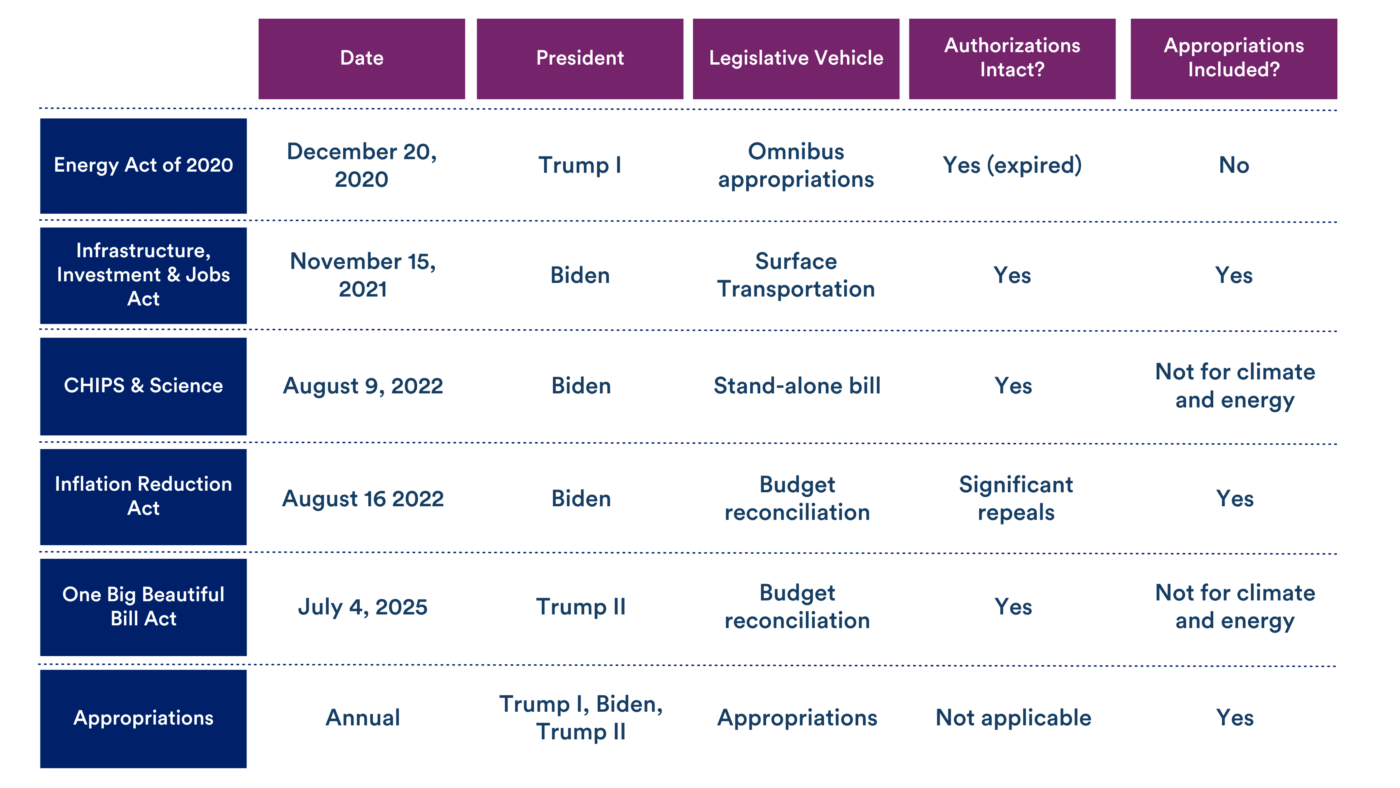

Table 1: Major Climate and Clean Energy Legislation of the Last Five Years

The fiscal year 2026 appropriations process did not fulfill the administration’s request for deep spending cuts

Annual appropriations are critical to advancing clean energy and climate priorities through federal policy. Every year, Congress seeks to pass 12 regular appropriations bills that fund the entire United States government, providing programmatic funding levels and setting the rules which the executive branch must follow in spending the funding. The appropriations process—which, because of the Senate filibuster, requires bipartisan collaboration—has not always been simple or straightforward.

In the six fiscal years initiated since September 2020, Congress has passed five sets of 12 regular appropriations bills on a bipartisan basis, including funding for energy and climate priorities. Fiscal Year 2025, the outlier, was funded through a year-long continuing resolution. Typically, Congress has been late: forced to rely on one or more continuing resolutions and only resolving disagreements through consolidated or omnibus measures. The most critical of these 12 regular appropriations bills for climate and energy policy is the Energy & Water appropriations bill (E&W), which covers appropriations for the Department of Energy (DOE), as well as the Army Corps of Engineers, parts of the Department of the Interior (DOI), and several other independent agencies.1

The Trump administration, through the Office of Management and Budget’s (OMB) Fiscal Year 2026 (FY26) President’s Budget Request (PBR), called for dramatic funding cuts to the federal agencies managing energy and climate issues. OMB’s submission called for more than $5 billion in cuts from the Fiscal Year 2025 (FY25) enacted budget for the non-defense portion of DOE alone,2 including more than $2.5 billion in cuts from the Office of Energy Efficiency and Renewable Energy (EERE).3 This approach differed significantly from the agreements reached in bipartisan appropriations bills predating the Trump administration. Indeed, some of the PBR’s proposed reductions to the Department of Energy (for instance, the proposed cut of $408 million from the Office of Nuclear Energy) are in some tension with the Trump administration’s focus on certain clean firm energy sources, the energy demands of artificial intelligence, energy exports, and critical minerals.

Congress largely rejected the PBR’s approach. The FY26 E&W bill signed into law by President Trump after bipartisan, bicameral negotiations has a topline cut of about $1 billion for the Department of Energy (DOE) line items associated with clean energy priorities relative to the FY25 package: a clear decrease in funding levels, but not the level sought in the PBR.4

At the account level within the FY26 E&W appropriations text: EERE funding took a $360 million dollar cut (~10%) compared to FY25, substantially above the PBR; the Office of Fossil Energy (FE) has $145 million less (~17%) in funding relative to FY25, half the level of cuts called for in the PBR; the Office of Nuclear Energy has $100 million more in funding than it did in FY25, relative to a PBR request of a $400 million dollar cut. The E&W text also avoids structurally endorsing the Trump administration’s DOE reorganization plan, announced in late November, although it is unclear whether that will remain the case in Fiscal Year 2027 (FY27) appropriations bills.

Despite avoiding the deep account-level cuts proposed by the Trump administration, the FY26 E&W bill is the imperfect product of bipartisan negotiations. Congressional appropriators reached top-level agreement in part by reprogramming $5.164 billion from the previously-passed Infrastructure Investment and Jobs Act (IIJA), which included longer-term appropriations outside of the annual process.5 These multi-year appropriations were intended to speed the deployment of carbon capture and storage (CCS) technology, among other purposes, and their reprogramming slows CCS deployment. The reprogramming compromise retains support for key programs and staff at the Department of Energy, while allowing Republican appropriators to contend that they reduced new spending by reallocating previously appropriated dollars. Additional reprogramming of IIJA funds is likely in future E&W bills under the same logic, absent significant changes in the makeup of Congress.

The Office of Clean Energy Demonstrations (OCED), a flagship clean energy office created by section 41201 of IIJA, did not receive any appropriations in the FY26 text, consistent with the Trump administration’s move to reorganize DOE by reshaping applied offices and de-emphasizing OCED within DOE. The Government Accountability Office found that OCED staffing declined from 285 to 40 in the six months through June 2025, after previously stating that 350 staff were needed to oversee its project portfolio.6 In report text, congressional appropriators directed the Department of Energy “to provide quarterly briefings and reports on the redistribution of project funding from the Office of Clean Energy Demonstrations,” which empowers congressional oversight and may prove important.7

But over the last five years, energy and water appropriations have declined slightly on an inflation-adjusted basis

Zooming out to consider the appropriations process during this decade, annual appropriations for relevant portions of E&W have modestly declined on a real basis since Fiscal Year 2020 (FY20). For accounts aligned with CATF’s focus, appropriations grew by ~15% between FY20 and FY26, while spending on all E&W accounts grew by slightly more (21%). Across the economy, consumer prices increased by about 24% in the same period, which means that real annual investment in energy spending declined modestly.

Assessing specific offices within DOE, EERE, Electricity, Nuclear Energy and Science have all seen nominal growth in annual appropriations since 2020, although none have seen real (inflation-adjusted) growth.

Table 2: Enacted E&W appropriations ($M, nominal) by category in select years and growth rates

| Category | FY26 | FY25 | FY20 | FY25-FY26 % Change | FY20 – FY26 % Change |

|---|---|---|---|---|---|

| ARPA-E | 350 | 460 | 425 | -23.9 | -17.7 |

| EERE | 3,100 | 3,460 | 2,790 | -10.4 | 11.1 |

| Electricity | 235 | 280 | 190 | -16.1 | 23.7 |

| Fossil Energy | 720 | 865 | 750 | -16.8 | -4.0 |

| Nuclear Energy | 1,785 | 1,685 | 1,493 | 5.9 | 19.6 |

| Science | 8,400 | 8,240 | 7,000 | 1.9 | 20.0 |

| Total, CATF Focus Areas | 14,590 | 14,990 | 12,648 | -2.7 | 15.4 |

The President’s Budget Request again proposes significant cuts to clean energy priorities; Congress will respond through the appropriations process8

Despite the significant bipartisan revisions to the climate and clean energy portion of the administration’s FY26 budget request, the recently-published FY27 budget request again proposes significant cuts to bipartisan priorities. The budget request also proposes repurposing previously appropriated IIJA funds for “baseload power”—a category of spending that would provide nearly $2 billion to preserve 9 gigawatts of coal, oil, and gas power and add 5 gigawatts in new generation from the same sources. The FY27 budget request also proposes providing new resources for an Office of Artificial Intelligence and Quantum, an Office of Fusion, and an Office of Critical Minerals and Energy Innovation. The FY 27 budget request proposes eliminating the Office of Energy Efficiency and Renewable Energy, the Grid Deployment Office, or the Office of Clean Energy Demonstrations.

These administration appropriations requests will be evaluated by congressional appropriators in the months ahead. Irrespective of the precise choices made by congressional appropriators in setting funding levels across programs and offices, Congress will retain the authority to exercise oversight over the administration’s implementation of its priorities. Congress may be more willing to exercise its oversight responsibilities this fiscal year following the midterm elections.

Table 3: E&W appropriations ($M, nominal) by category

| Category | FY27 PBR ($M) | Enacted FY26 ($M) | % Cut |

|---|---|---|---|

| ARPA-E | 200 | 350 | 43 |

| EERE | 09 | 3,100 | 100 |

| Electricity | 203 | 23510 | 14 |

| Fossil Energy | 011 | 720 | 100 |

| Nuclear Energy | 1,534 | 1,785 | 14 |

| Science | 7,139 | 8,400 | 15 |

| Total, CATF Focus Areas | 9,076 | 14,590 | 38 |

Congress’s three pieces of bipartisan authorizing energy and climate legislation remain largely intact, but are likely to underdeliver in this administration

Since 2020, Congress has passed three substantive, bipartisan authorizing bills focused on energy and climate policy: the Energy Act of 2020,12 the Infrastructure Investment and Jobs Act (IIJA), and the CHIPS and Science Act (CHIPS). Together, these bipartisan bills outline the possibility (and the limits) of bipartisan collaboration on energy and emissions reductions.

The first of these, the Energy Act of 2020 (Energy Act), passed in an omnibus package within the last month of 2020 and was signed into law by President Donald Trump. The bipartisan legislation contained more than 80 distinct statutory provisions within Clean Air Task Force’s focus, covering topics including fusion energy research, energy storage, nuclear fuel, geothermal research, renewable research and development, and fossil energy and carbon management.

The Energy Act appropriated little money for these priorities itself—less than $500M for two provisions—on the theory that future legislation, including annual appropriations bills, would fill in the appropriations behind the Energy Act’s five-year authorizations. CATF’s analysis finds that the next five years of legislation successfully provided some $22 billion in appropriations directly targeted at about 20 different Energy Act provisions, including many that CATF believes critical to developing new, innovative energy technologies to reduce air pollution.13 Furthermore, although the default for appropriations is to expire after a single fiscal year, about $20 billion out of $22 billion are no-year funds made available “until expended,” an important flexibility that enables execution of longer-term priorities.

Energy Act provisions provide tangible evidence of the durability of bipartisan legislation. As discussed in detail later in this report, the OBBBA repealed some clean energy provisions and cut funding for other clean energy and climate priorities. But the Energy Act survived intact—all of the act’s authorizing text remains after OBBBA’s passage, without a single provision experiencing a repeal. Although many Energy Act authorizations technically expired in 2025, five years after the law’s passage, a future Congress could still direct appropriations to achieve the objectives of the expired authorizations.14

Most Energy Act programs did not receive program-level appropriations by the end of 2025. For programs that do not receive these appropriations, the executive branch may still choose to allocate account-level appropriations to a specific program—for instance, account level funding directed to an office within DOE may be allocated to achieving a program—but without congressional direction, fund availability is subject to the discretion of the administration personnel at the time. DOE must follow reprogramming procedures and is bound by the purpose statute, which requires that agencies not use funds for purposes other than those for which Congress appropriated them.15

IIJA, Congress’s second major bipartisan effort, secured the support of 13 Republican representatives and 19 Republican senators before then-President Joe Biden signed it into law. Through about 100 provisions related to CATF focus areas, IIJA directed federal dollars toward technologies including hydrogen, carbon capture and storage, geothermal, nuclear fission, and the electric grid. In contrast to EA20, IIJA directly appropriated funds for more than half of these provisions (53). In IIJA, Congress appropriated more than $72.26 billion for these provisions, with $66.79 billion of no-year funds made available “until expended,” providing the executive with significant flexibility and the option to deploy these funds on a longer time horizon than through annual appropriations.

IIJA funding was largely self-contained. Its programs have mostly not benefited from subsequent appropriations. After the initial IIJA funding injection, only a few programs have received top-ups—a program for orphaned wells, the Loan Programs Office (since renamed the Office of Energy Dominance Financing by the Trump administration), the Office of Clean Energy Demonstrations, and the Advanced Reactor Demonstration Program together received about $497 million dollars in subsequent appropriations.

IIJA proved largely, but not wholly, legislatively resilient during the Trump administration’s first year. Although the President’s Budget Request proposed cancelling more than 30 of the IIJA programs assessed, they all emerged from One Big Beautiful Bill Act without statutory repeals or rescinded appropriations, demonstrating the durable bipartisan framework underpinning IIJA. Nonetheless, more than $5 billion in IIJA funding was reprogrammed to pay for the Energy and Water bill FY26 topline, as described above. The Trump administration has also sought to reprogram IIJA funding on its own, without legislative directive, in at least one instance—repurposing carbon capture funds to support coal plants, which Democrats argue violates the Purpose Statute. As discussed below, the administration has also sought to cancel obligated funding for IIJA projects, and their FY27 budget proposes reprogramming IIJA funds.

The prospects for IIJA programs moving forward are uncertain. Congress directs continued spending tow support these programs.16 The next Surface Transportation Reauthorization bill—a previous iteration of which provided the legislative vehicle for 2021’s IIJA—is currently under negotiation in Congress, although its prospects for passage remain uncertain in the 119th Congress.17

Finally, CHIPS, a bipartisan piece of legislation passed in 2022, remains largely an unfulfilled authorization framework as much of CHIPS remains unfunded. CATF’s analysis of the bill text found 23 different provisions of relevance for this stock take.18 OBBBA did not repeal any of these provisions, and the President’s FY26 Budget Request proposed to cancel funding for only two provisions, one modifying the Office of Clean Energy Demonstrations (OCED) and another modifying the Office of Technology Transitions (OTT, which the Trump administration has renamed the Office of Technology Commercialization). At the same time, nearly the only provisions that saw appropriations during the covered period were those two programs, OCED and OTT.19

Dueling budget reconciliation bills underscore consensus on clean firm energy generation

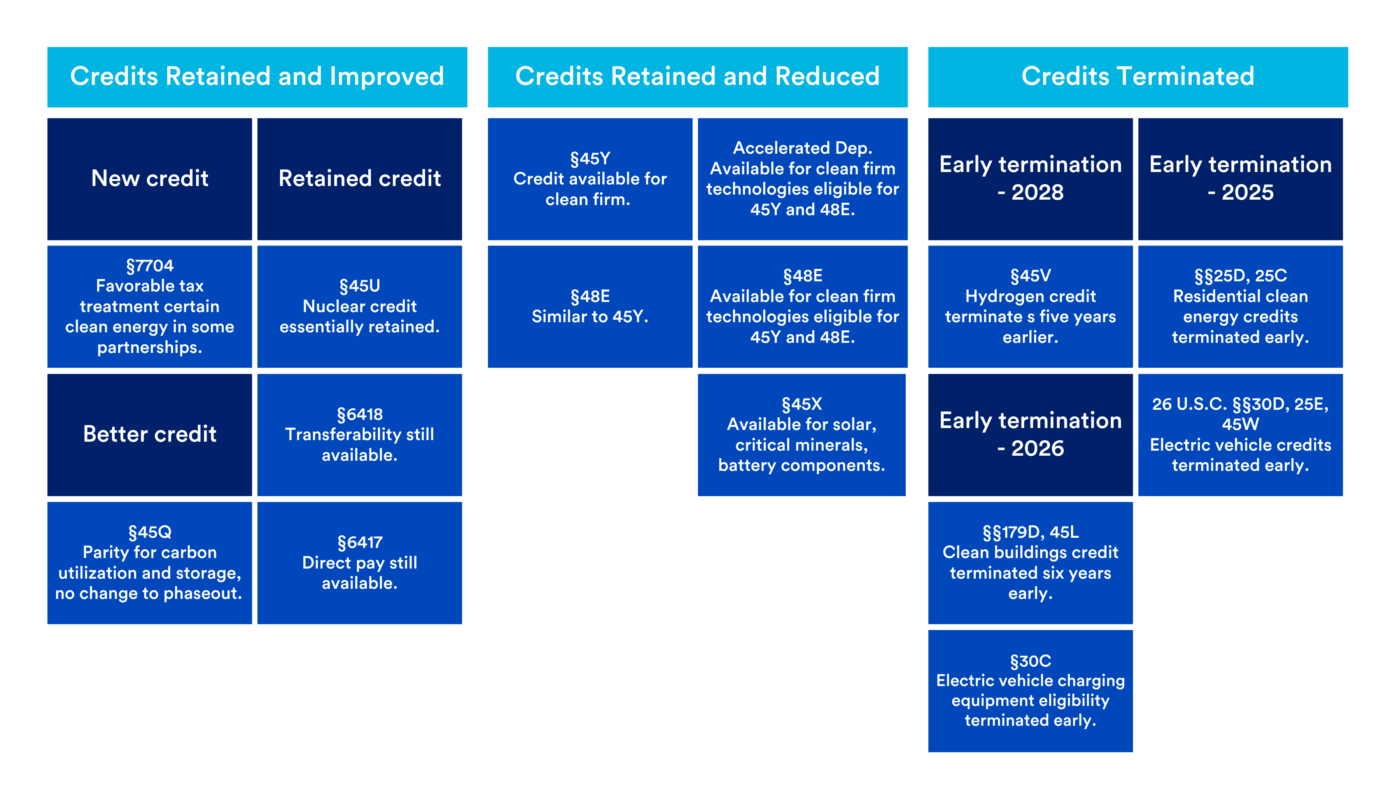

Congress also legislates through budget reconciliation, a procedure that allows the Senate majority party to avoid a filibuster—which requires 60 votes to overcome—and pass tax- and spending-related legislation with a simple majority vote. Extraneous provisions unrelated to the budget process are procedurally excluded. The two budget reconciliation bills passed in recent years, IRA and OBBBA, underscore areas of agreement and disagreement between the two parties’ congressional caucuses: agreement on clean firm generation and disagreement on fossil fuels and renewables. As dust has settled since OBBBA’s passage, policy support for clean firm energy generation—geothermal, nuclear fission, carbon capture, fusion energy, and battery storage (even when tied to wind and solar generation)—has remained intact. OBBBA dramatically cut tax credit eligibility for renewables, a change which accelerated project timelines to fit narrowed eligibility dates but which will not drive net new projects.

Chart 1: Status of Clean Energy Tax Credits Post-OBBBA

The IRA energy tax credits were curtailed but not eliminated

The IRA’s energy tax credits were the flagship energy policy of the Biden administration. Unprecedented in scope, at the IRA’s passage the non-partisan Congressional Budget Office (CBO) estimated that the 24 clean energy tax provisions would drive some $271 billion in financial support over the decade starting in 2022.20 Two years later, the CBO assessed that their analysis had underestimated the financial scope by some $277 billion.21 Other independent analyses at IRA passage put the financial scale of the IRA’s credits in excess of $1 trillion over a decade.22

Post-OBBBA, the scope of the clean energy tax credits will shrink significantly. The Trump administration’s flagship law curtailed the IRA’s impact by early terminating nine credits for clean hydrogen, the building sector, and electric vehicles. Targeted changes to the formerly technology-neutral zero-emission production tax credit and investment tax credit for electricity generation eliminates wind and solar eligibility after mid-2027; wind energy components cannot avail themselves of the advanced manufacturing credit after 2027. Further, where previously these tax credits had two separate expiration triggers—a specific date and a minimum emissions reduction target, where industry was largely planning on the latter—the revisions in OBBBA eliminated the emissions reduction expiration language, providing a much shorter runway for promising but nascent technologies including geothermal and nuclear fusion. New, complicated language on prohibited foreign entities/foreign entities of concern (PFE/FEOC) that applies to most of the credits adds implementation uncertainty for taxpayers that may further reduce investment.23 The scope of the clean fuels production credit was expanded, but the associated policy changes have transformed it to a subsidy to mature industries that may increase emissions. The cumulative impact of these changes is substantial: the CBO estimates that OBBBA’s clean energy changes will save the U.S. government about $500 billion over the 10 years from FY 2025 to FY 2034—a half trillion-dollar reduction in financial support for clean energy.24

But the death of the IRA’s clean energy credits has been overstated. Much of OBBBA’s credit curtailment is limited to industries disfavored by the Trump administration and congressional Republicans: wind, solar, electric appliances for homes and buildings, and electric vehicles. Economy-wide emissions reduction will require support for these critical industries, and CATF advocated for their inclusion in the IRA and retention in OBBBA, but the fate of these industries within OBBBA should not be conflated with the overall scope of the revised tax credits. Indeed, the Joint Committee on Taxation estimates that the value of key clean energy tax credits (§§ 45/45Y, 48/48E, 45U, 45V, 45Q, 48C, and 45X) will be about 60% of their estimated value in 2023—on the order of $280 billion dollars through 2034 (compared to JCT’s 2023 score of about $490 billion).25 Further, beyond OBBBA’s changes to energy incentives, the broader-based corporate tax relief contained in the bill—such as making bonus depreciation and R&E expensing permanent—will provide benefits to some parts of the industry.

Chart 2: Post-OBBBA, clean energy and climate tax credits retain ~60% of estimated 2023 value

Examining the tax credit landscape post OBBBA unearths still-present support for clean energy, especially clean firm generation:

- Clean firm technologies will still benefit from the clean electricity production and investment credits (45Y and 48E, respectively) through at least 2033, when they are currently set to expire. Although many clean firm technologies are still at an earlier stage of deployment than wind and solar, bipartisan endorsement in 2025 suggests the potential for future extension past 2033.

- New wind and solar facilities are still potentially eligible for the clean electricity production (45Y) and investment (48E) credits if they meet “commence construction” and “placed in service” deadlines in 2026 and 2027. These timelines are aggressive, but not impossible. Further, existing wind and solar facilities will continue to receive financial support from the production credit for 10 years after the facility’s placed-in-service date.

- The 45U zero-emission nuclear production credit, which the initial CBO score estimated at $30 billion, is still available with marginal changes.

- The 45Q carbon oxides credit now provides parity for utilization, a change that the CBO estimates will drive more than $14 billion in financial value for the carbon capture utilization and storage ecosystem. The credit value for storage of carbon oxides was retained.

- The 45X advanced manufacturing credit is still available for wind energy for the next two years; solar energy components for the next four years; and battery components that complement solar and wind energy installations by providing energy storage for the next four years.26

- Accelerated depreciation for energy property is still available for all clean firm technologies otherwise eligible for the production and investment credits, and new solar and wind energy facilities retain eligibility consistent with these credits (that is, new renewable facilities could potentially claim the accelerated depreciation through mid-2027).

- Direct pay and transferability, which enable additional taxpayers to claim and value the credits, were retained without modification.

The federal government also disbursed billions in clean energy tax credits between the 2022 passage of the IRA and the 2025 passage of OBBBA. Although precise figures are generally not publicly available due to Treasury and Internal Revenue Service reticence to publish potentially identifiable taxpayer information, public information suggests that the credits spurred significant clean energy progress. For instance, in August 2024, the Treasury shared that for tax year 2023, “more than 1.2 million American families […] claimed over $6 billion in credits for residential clean energy investments” and “2.3 million families […] claimed more than $2 billion in credits for energy efficient home improvements.”27 In 2023, 487,000 tax returns claimed the Clean Vehicle Credit for a total of $3.3 billion; in that same year, 28,000 tax returns claimed the used Clean Vehicle Credit for $95 million.28 In 2024, the Treasury and the IRS announced that consumers had saved more than $2 billion in upfront costs on purchases of more than 300,000 clean vehicles between January 1, 2024 and October 1, 2024.29

IRA energy provisions that provided grants, invested in federal capacity, or created loan programs fared poorly in OBBBA, but some programs remain

Beyond tax credits, the IRA also included significant direct appropriations for grant programs, investments in federal capacity, and loan guarantee and direct loan programs relevant to climate and energy. The IRA appropriated ~$82 billion across 31 grant programs, with some $29 billion of that funding available through fiscal year 2031. IRA also included approximately $33 billion in investments in federal capacity, such as national laboratory infrastructure and conservation on national parks and public lands,30 with $5 billion available through the end of FY26, $2 billion available through the end of FY27, $4.5 billion available through FY28, $2.5 billion available through the end of FY30, and $24 billion available through the end of fiscal year 2031. IRA also provided loan guarantee authority for innovative clean energy technologies ($40 billion), energy infrastructure ($250 billion), and tribal energy projects ($18 billion), as well as a $3 billion credit subsidy for the Advanced Technology Vehicles Manufacturing Program and a $2 billion appropriation for the new transmission facility direct loan program.

OBBBA repealed statutory authorizations and rescinded unobligated funding for many grant programs, but its enactment did not return federal funding to the pre-IRA status quo. The Greenhouse Gas Reduction Fund, originally allocated $27 billion by the IRA, saw its statutory authorization repealed and unobligated funds rescinded. But the exact amount that will be rescinded is currently disputed and under review by an en banc panel of the D.C. Circuit, after a coalition of nonprofits sued EPA.31 Another 18 grant programs that were originally provided with nearly $26 billion dollars in appropriations had unobligated funds rescinded while their statutory authorizations remained intact;32 12 more grant programs with nearly $29 billion in appropriations through FY2031, however, experienced neither repeal nor rescission. These 12 programs include grants for: renewable energy in rural America, deployment of zero-emission technologies through rural electric cooperatives, home rebates for energy efficiency, assistance for energy code adoption, climate resilience for native communities, and grants to reduce air pollution at ports.33 Notably, several of the preserved programs benefit rural and agricultural communities, likely due to their close ties to the Republican majorities that enacted OBBBA. A high-level assessment of obligations and outlays for IRA grant programs and other federal spending can be found in a later section.

OBBBA also cut investment in federal capacity for climate and energy programs. Of the 26 provisions that provided more than $33 billion, OBBBA rescinded $24.75 billion funding for 17 provisions. But nine provisions with $8.786 billion in federal investments were not repealed or rescinded, covering electric fleets for the U.S. Postal Service, the Federal Permitting Improvement Steering Council, computer modeling, agricultural conservation, and national laboratory infrastructure.34

Finally, OBBBA dramatically rewrote the IRA’s loan programs. The Advanced Technology Vehicle Manufacturing program, which received new loan subsidy funding in IRA, was repealed and its unobligated funding rescinded.35 Unobligated funding for the transmission facility financing program and the tribal energy loan guarantee program was rescinded. Funding for the Section 1703 innovative clean energy program under the Loan Programs Office was fully rescinded; the Section 1706 Energy Infrastructure Reinvestment Financing Authority was transformed into the Energy Dominance Financing Authority, which now includes eligibility for fossil programs (and whose commitment authority was extended to 2028).

The federal government workforce grew—and despite 2025 attrition, the workforce remains above 2020 level

The federal government staffed up to address the priorities of the Biden administration, including on energy and climate.36 Between September 2020 and September 2024, the federal workforce grew from 2.18 million to 2.31 million, an increase of 6%. Key energy and climate agencies grew even more rapidly. The Department of Energy (DOE), which took on significant new responsibilities under the energy titles of IIJA and IRA, grew by more than 20% cumulatively over that period, including an annualized maximum rate over 8% between September 2022 and September 2023. The Federal Energy Regulatory Commission (FERC) also grew more quickly than the broader federal government, with headcount also increasing nearly 8% between September 2020 and September 2024. The EPA, tasked with overseeing substantial portions of the IRA and President Biden’s climate-related regulatory agenda, grew by nearly 13% over the same period. Within the Department of the Interior, the Bureau of Land Management (BLM) grew by more than 3%, while the Bureau of Ocean Energy Management (tasked with overseeing offshore wind, among other Biden administration priorities) grew more than 11%. The Council on Environmental Quality, starting from a very low base, quadrupled in size.37

Federal employment grew most rapidly in the second half of the Biden administration. According to data from the Bureau of Labor Statistics, the overall federal workforce was less than half a percent larger in February 2023 than it was in January 2021. By January 2025, the federal workforce had grown by nearly 6% from when President Biden assumed office in January 2021. Hiring peaked in early 2024, with year-over-year growth of about 4% in the first quarter of the year before dropping to closer to 2% by the end of the year.38

The Department of Government Efficiency (DOGE) and the Office of Management and Budget (OMB), working across federal agencies, shrank the federal workforce in 2025. Cumulatively, federal employment in October 2025 was still up by about 2% over September 2020 levels, although it declined by more than 3% from its 2024 peak.39 According to the May 2025 President’s Budget Request (PBR),40 combined employment in DOE, EPA, segments of Interior, FERC, CEQ, and the Nuclear Regulatory Commission (NRC) declined by a little more than 1% from 2024 levels. At a more granular level, employment in the DOE workforce grew by about 1% (likely a reflection of hiring in the final months of 2024); FERC declined by about half a percent; BLM declined by about 8%; the Bureau of Ocean Energy Management (BOEM) grew by about 10%; and CEQ added three staff for a growth rate of 4%.

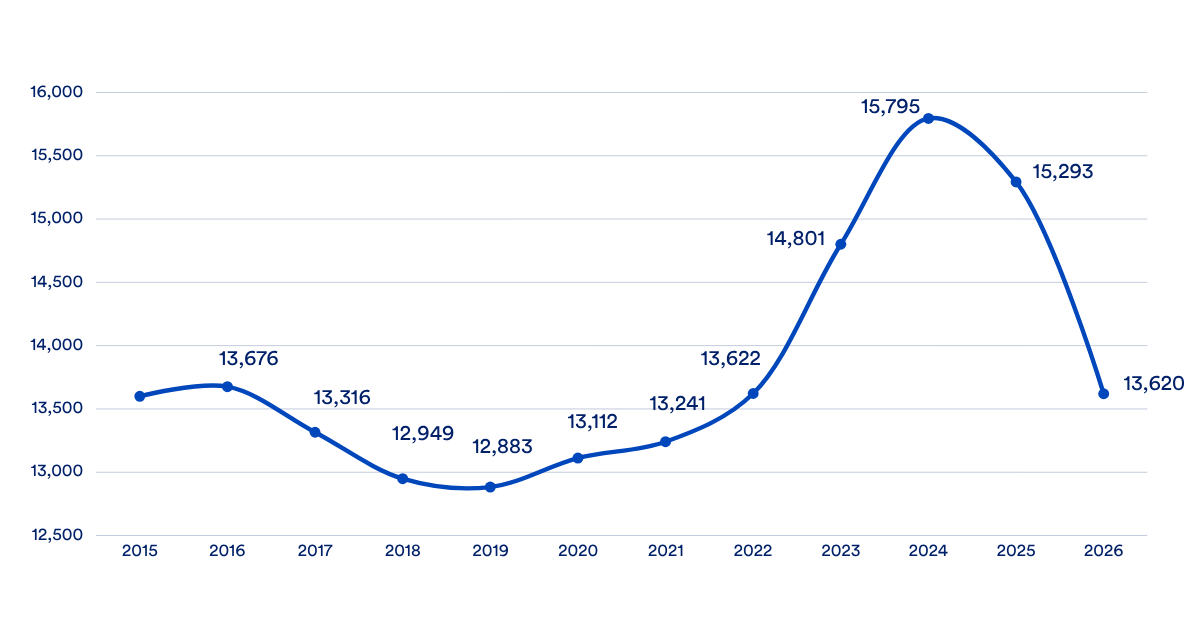

The latest data for the Department of Energy illustrate the general pattern acutely: a slight decline in employment from the end of the Obama administration through the first Trump administration; rapid acceleration through the second half of the Biden administration, and then an equally rapid decline in the first year of the Trump administration, returning the 2026 DOE headcount to 2022 levels.

Chart 3: Department of Energy Headcount, 2015-2026

Last May’s PBR projects further federal workforce declines in 2026. The PBR projects a cumulative incremental decline of 10% within the DOE, EPA, segments of Interior, FERC, CEQ, and the NRC. Within that total, certain groups stand out: the PBR projects BOEM to decline by 19%, followed by EPA at more than 11%. More granular actuals for specific agencies through the end of 2025 are unavailable at time of publication, but anecdotal evidence suggests further decline in federal staffing at agencies with critical climate and energy responsibilities, although the PBR’s projections are unlikely to bear out given congressional pushback. A subsequent post will dig into this year’s PBR’s actuals.

The Trump administration’s actions to shrink the federal workforce have resulted in the reduction of significant amounts of scientific expertise. Science found that more than 10,000 PhDs in science, technology, engineering and math (STEM) have left the federal government since President Trump took office for the second time.41 These departures occurred across the federal government, but agencies with important energy and climate responsibilities, including the National Oceanic and Atmospheric Administration, the Environmental Protection Agency, and the Department of Energy all suffered disproportionately high loss rates.42

The administration’s personnel policies in the civil service have extended beyond reducing the size of the workforce. Early in 2026, the Office of Personnel Management finalized a rule that established an excepted service category for Schedule Policy/Career (note that the Trump administration pursued the same program near the end of its first term under the name “Schedule F”). This new category could result in the elimination of civil service protections for tens of thousands of civil servants engaged in “confidential, policy-determining, policy-making, or policy-advocating work.” Implementation of this new rule will take time—agencies submit lists of positions for conversion to the new category to the President—but it poses a clear risk of politicizing work on energy and climate-related policy matters that may change the type and quality of policy decisions. The administration has also canceled collective bargaining agreements at many federal agencies including the Department of Energy, eliminated the Presidential Management Fellow program, altered the policy in determining retention during reductions in force, and proposed changes to performance ratings procedures.

Early conclusions from our analysis of the workforce:

- The Trump administration has significantly reduced the federal workforce, but not completely rolled back the hiring under the previous administration to date.

- Congressional pushback, specifically through the annual appropriations process, has prevented some proposed Trump administration cuts over the last year.

- Significant technical expertise in climate and energy departed the federal government during the first year of the Trump administration.

The Trump administration has moved to cancel federal investments in clean energy projects and has begun redirecting existing federal funds toward projects with limited emissions reduction impacts

Beyond pursuing the elimination of the previous administration’s energy and climate programs through the legislative process, the current administration has undertaken a two-pronged effort: first, to cancel financial awards made under the Biden administration, and second, to repurpose some of those funds for projects more aligned with Trump administration policy, sometimes in ways that may contravene the underlying statutory requirements.

As CATF has previously highlighted, the administration has undertaken an unprecedented effort to cut federal investment in clean energy projects that have contracted with the federal government for financial assistance.43 The effort has primarily targeted projects where money has been “obligated” (that is, a contractual agreement has been made between the federal government and another entity) but where the money has not been “outlaid” (actually spent). The announced cuts and additional cuts being considered potentially impact approximately 650 projects, encompassing $23 billion in federal funding. In the largest round of confirmed cuts, the Department of Energy announced the termination of 321 financial awards contracted to provide approximately $8 billion in support for clean energy projects around the country.

The nearly $8 billion in financial awards that have been officially terminated were primarily managed by four offices within the DOE: the Office of Clean Energy Demonstration (OCED) (42%); the Grid Deployment Office (27%); the Office of Fossil Energy and Carbon Management (16%); and the Office of Energy Efficiency and Renewable Energy (13%). The projects that were recipients of these awards had already received approximately $413.5 million in outlays (5% of total award) when they were canceled. The additional cuts being considered have a different distribution: 57% originate in OCED and 26% originate in the Office of Manufacturing and Energy Supply Chains (MESC). These projects had received about 4% of their awards in outlays ($643 million).44 The Trump administration has sought to eliminate and / or restructure these offices in a reorganization, a move that has drawn congressional scrutiny.45 In the Joint Explanatory Report accompanying the FY 26 E&W appropriations bill, Congress directed the Department of Energy to “carry out federal award terminations in accordance with its published procedures in the Department of Energy Guide to Financial Assistance.”46

The Trump administration has also “restructured, revised, or eliminated” more than $83 billion in Biden-era Loan Programs Office programs. Beyond their direct effects, these project cancellations and changes to loan portfolios will have significant implications for the clean energy sector’s confidence in the federal government as a reliable partner. CATF’s Clean Energy Investments Tracker monitors clean energy investment trends; the tracker cannot disaggregate between different causes of federal policy uncertainty, but it provides useful context on the sector’s investment trajectory.

The Trump administration has also repurposed funds appropriated for emissions reduction and industrial innovation to achieve other unrelated ends. As CATF has previously covered, the administration has sought to repurpose money intended for carbon capture demonstration facilities to support coal-powered electric generation. Senate Democrats are currently seeking to scrutinize that effort through Congress’ oversight powers.47

Billions of dollars for clean energy are already spent

The Biden administration’s Department of Energy made substantial progress in obligating and outlaying congressionally appropriated climate and clean energy funds. CATF analysis of the financial assistance data available from USASpending.gov finds that, across all funding sources, from fiscal year 2021 through fiscal year 2025, the U.S. Department of Energy obligated approximately $35 billion in federal spending and outlaid roughly one third of that amount—$11.9 billion.48 CATF estimates that, excluding certain defense-related and other spending, to focus on clean energy spending, approximately $32.56 billion was obligated throughout those fiscal years, with $9.77 billion actually outlaid to the intended recipients.49 Of total outlays, the Advanced Reactor Demonstration Program received 13.02%; ARPA-E projects received 12.4%; fusion energy sciences projects received 10.27%; nuclear physics received 10.00%; carbon capture received 4.97%; vehicle technologies received 4.65%; and solar energy received 3.4%. Many other program activities received smaller proportions of total clean energy spending over the period.

These billions in outlays—funds that that have already left the federal government—will be difficult, if not impossible, for the federal government to claw back and may support emissions reduction in years ahead.

These outlays also show a federal government that was becoming more effective at spending money over time. Outlays increased over the covered period, with just $668 million outlaid in FY21, rising to $2.98 billion in FY24 and $3.63 billion in FY25. Obligations also rose over the five fiscal years, rising from $2.47 billion in FY21 to $8.89 billion in FY24 and $15.85 billion in FY25. Taken together, these trends may suggest an improving federal government implementation capacity over the course of the previous administration. Still, the relatively slow pace of disbursements also suggests a clear area for improvement in subsequent efforts to catalyze clean energy and emissions reductions.

OBBBA reshaped the Loan Programs Office into the Energy Dominance Financing Office, altering the core policy focus of the office, but the Office is still advancing some clean energy

The Loan Programs Office (LPO) was created by the 2005 Energy Policy Act. Congress temporarily expanded its scope and size during the American Reinvestment and Recovery Act,50 and then supercharged it during the Biden administration, increasing the funds available for LPO and expanding eligible projects.51 The LPO during the Biden administration committed $108 billion in loans across 53 clean energy projects, including nuclear, transmission, electric vehicles, and batteries.52 Former staffers assess that the program moved too slowly as a result of “executive branch machinery that defaulted to caution, process, and reactive strategies rather than speed, outcomes, and clear direction.”53 Many loan commitments were not fully finalized at the end of the Biden administration.

The One Big Beautiful Bill Act made two major changes: first, it rescinded unobligated balances from the Inflation Reduction Act provisions; second, it refocused one of the key loan programs on critical minerals, electricity supply, and grid reliability, which enables the program to support fossil-powered electricity generation—but which still allows clean electricity to qualify.54 In early January 2026, the Trump administration’s DOE claimed that it was “restructuring more than $83 billion in Green New Scam loans and conditional commitments from the Biden-era loan portfolio.”55 But this claim does not tell the full story: many of the cancellations were due to market conditions unrelated to Trump’s election, although the administration has canceled high-profile loans including the Grain Belt Express transmission line.56 Other loans continue with modifications but still retain support for clean energy sources.57

Deregulatory and administrative actions pose an ongoing and developing threat to the climate and energy policy in the remaining years of the Trump administration

Addressing climate pollution and supporting clean energy sources is not merely supported by major fiscal initiatives supported by major legislation over the past five years. The executive branch can—and during the previous administration did—also use the regulatory state to complement tax credit and financial assistance programs. A stock take of the last five years would be incomplete without summarizing the key deregulatory actions of the Trump administration during its first year—and future threats on the horizon. This effort is ongoing and will be regularly updated as the administration initiates new actions, existing actions make their way through the administrative process, and legal challenges are resolved.

The Trump administration’s assault on the regulatory effort to address climate pollution and support clean energy sources has been near-comprehensive in scope. Key deregulatory actions include:

- A proposed rule that amends the Greenhouse Gas Reporting Program (GHGRP) to remove program obligations for most source categories. If the rule is finalized and survives legal challenge, this deregulatory effort would largely eliminate the best source of GHG emissions information available, posing challenges for implementation of tax credits and threatening our ability to quantify the scope of the emissions challenge across the U.S. economy.

- A final rule that seeks to repeal all greenhouse gas emissions standards for light-duty, medium-duty, and heavy-duty vehicles and engines. This action introduces new uncertainty into the motor vehicle sector and could hamstring a key regulatory tool for addressing transportation emissions. The same final rule also repeals the endangerment finding, a key scientific determination that motor vehicle greenhouse gas emissions contribute to climate change endangering the public health and welfare, which forms the basis for EPA’s regulation of those emissions under the Clean Air Act. This rescission, if it stands, would create new barriers to reducing emissions.

- A proposed rule that would repeal all greenhouse gas emissions standards for fossil fuel-fired power plants and declare that greenhouse gas emissions from fossil fuel-fired power plants do not contribute significantly to dangerous air pollution. If successful, this effort would eliminate a key tool for reducing emissions from the power sector.

- An Office of Management and Budget directive that instructs agencies to review internal documents and consider greenhouse gas emissions only in those cases plainly required in their governing statutes. If implemented, this guidance would limit federal agencies from considering the social cost of greenhouse gas emissions in their decisions, including in their procurement decisions, a significant step back from action under the previous administration.

- An interim final rule, followed by a “final” final rule, from the Environmental Protection Agency that delays many compliance deadlines for the Crude Oil and Natural Gas source category methane and VOC standards under Clean Air Act section 111(b) and (d) until January 2027. Most of the standards for which compliance has been delayed have been effective since May 2025.

The Trump administration has also sought to hamper renewable deployment through administrative action. Key actions include:

- The Department of the Interior stop-work orders —purportedly for national security concerns—for offshore wind projects currently under construction in the United States;

- An order by the Secretary of the Interior instructing agencies to prioritize “energy density,” based on supposed land use of gas, coal, and nuclear relative to wind and solar;

- An “overhaul” of offshore wind rules launched by the Department of the Interior;

- An order by the Secretary of the Interior requiring all decisions, actions, consultations and other undertakings related to wind and solar energy facilities to receive elevated review by the Office of the Secretary;

- A recommendation by the U.S. Department of Transportation that wind turbines be set back 1.2 miles from highways and railroads;

- A Treasury Department Notice that removes a key safe harbor for wind and solar facilities seeking to qualify for the Clean Electricity Investment Tax Credit and the Clean Electricity Production Tax Credit.

Prospectively, the Trump administration must issue further guidance to implement the energy and climate policies of the Inflation Reduction Act that remain following OBBBA. The initial round of Treasury Department guidance on the PFE/FEOC provisions from OBBBA did not hamper energy tax credit availability for clean energy resources, but Treasury must issue more complete guidance in order to make tax credits accessible for all technologies, including clean firm energy sources like nuclear and geothermal.

Conclusion

The narrative around federal clean energy and climate policy in the first year of the Trump administration has emphasized the many disruptive actions taken. CATF’s stock take analysis suggests that narrative is overly reductive—though not incorrect—for three reasons.

First, legislative actions over the last five years reflect a growing bipartisan consensus in support of clean firm energy generation, including nuclear fission, fusion, advanced geothermal, and carbon capture, as demonstrated most notably by OBBBA’s retention and, in one case, expansion of relevant tax credits.

Second, while the Trump administration has taken significant executive actions in 2025, Congress has used the appropriations process to protect some clean energy programs, spending, and federal staff, as reflected by the topline numbers in the FY26 E&W bill.

Third, some of the resources intended for emissions reduction and energy innovation were obligated and outlaid in the last administration, and additional funding will be spent during this administration, particularly on technologies—like nuclear and geothermal—that the administration sees as consistent with its energy dominance agenda.

Support for emissions reduction and energy innovation is far from what it should be. But significant investments are still being made, and major parts of the statutory foundation built over the last five years remain intact.

Appendix: OBBBA Tax Credit Changes

| Categories | Credits | Description of Credit and OBBBA Change | Climate Upside Post-OBBBA |

|---|---|---|---|

| New credit | 26 U.S.C. §7704 | OBBBA created a new credit that provides favorable tax treatment for income from hydrogen storage, carbon capture, advanced nuclear, hydropower, and geothermal energy for certain publicly traded partnerships. | New credit available for clean firm power and hydrogen storage. CBO estimates $3.23 billion over ten years, an increase in impact.58 |

| Improved | 26 U.S.C. §45Q (Carbon oxides) | Pre-OBBBA, credit provided $60 for utilization and $85 per ton for storage for facilities that begin construction before 2033. OBBBA created parity for carbon utilization and storage at $85 per ton, and applied PFE/FEOC provision. Did not change the phaseout. | Increases value for carbon utilization, including enhanced oil recovery (EOR). CBO estimates $14.23 billion over ten years, an increase in impact.59 |

| Extended | 26 U.S.C. §6427 Agro-diesel | Extends the §40A credit for agro-biodiesel producers by two years to 12/31/26, doubles the credit value, making it stackable. | N/A. No separate CBO estimate for this provision. |

| Maintained | 26 U.S.C. §45U Zero-emission nuclear power production credit | Pre-OBBBA, a production tax credit of 1.5 cents per kilowatt hour of electricity sold if prevailing wage requirements were met. OBBBA retained for existing facilities through 2032. Adds new PFE/FEOC restrictions | Provides financial support to key clean firm technology. No new CBO estimate, but post-IRA estimate of $30.1 billion over ten years.60 |

| 26 U.S.C. §6417 (Direct Pay) | Pre-OBBBA, tax-exempt entities could receive many of the IRA tax credits. No direct change to this provision, but OBBBA adds domestic content requirements to many IRA credits that may impact tax exempt entities’ ability to access the credits through direct pay. | Tax-exempt entities can still receive payments for 45U, 45V, 45X, 48E, 45Q, 45Z, 45Y. No separate CBO estimate for this provision. | |

| 26 U.S.C. §6418 (Transferability) | Pre-OBBBA, taxpayers could transfer eligible credits to an unrelated party. No direct change to this provision, but OBBBA adds domestic content requirements to many IRA credits that may impact taxpayers’ ability to access the underlying credit. | Taxpayers can still transfer credits from 45U, 45V, 45X, 48E, 45Q, 45Z, 45Y to unrelated third parties. No separate CBO estimate for this provision. | |

| 26 U.S.C. §48C | Pre-OBBBA, IRA expanded this credit by $10 billion; available to taxpayers investing in clean energy manufacturing, industrial decarbonization, or critical minerals processing. OBBBA eliminates administrative ability to reallocate forfeited credits and adds new PFE/FEOC restrictions. | Unallocated portions of tax credit are still available for taxpayers. No separate CBO estimate for this provision. | |

| Degraded | 26 U.S.C. §45Y Clean Electricity Production Credit | Pre-OBBBA, electric generation facilities placed in service after 12/31/24 received ten years of inflation-adjusted credit of 0.3 cents per kilowatt hour, up to 1.5 cents if certain conditions were met. Phaseout in either 2032 or when power sector emissions drop to 25%. Post-OBBBA, credit is terminated for wind and solar facilities that begin construction after 6/30/26 or that are placed in service after 12/31/27; phasedown for other technologies after 2033; relaxes eligibility for natural gas-fueled fuel cells. Adds new PFE/FEOC restriction. Eliminated emissions-based phasedown which would have benefited early-stage clean firm technologies. | Taxpayers can still receive the credit for nuclear fission, geothermal, energy storage, and fusion. Wind and solar facilities can also receive the credit if they comply with the placed in service or commence construction language. CBO scores this provision as providing $24.9 billion in savings relative to the pre-OBBBA baseline (a reduction in impact).61 |

| 6126 U.S.C. §48E Clean Electricity Investment Credit | Similar to 45Y. | Similar to 45Y. CBO scores this provision as providing $165.7 billion in savings for the Treasury relative to the pre-OBBBA baseline (a reduction in impact).62 | |

| 26 U.S.C. §168 Modified accelerated cost recovery system | Eliminates accelerated depreciation eligibility for disfavored technologies (wind, solar) after 2027, but retains eligibility for all other clean energy technologies | Clean firm technologies eligible for 45Y and 48E can still use MACRS. CBO scores this provision as providing $328 million in savings relative to the pre-OBBBA baseline (a reduction in impact).63 | |

| 26 U.S.C. §45X Advanced Manufacturing | Pre-OBBBA, credit provided value for producers of domestic solar, wind, battery components, and critical minerals, phasing down from 2030-2032. Post-OBBBA, wind energy components are ineligible after 2027 and applies new PFE/FEOC restrictions. | Taxpayers can still access the credit for solar, critical minerals, and battery components. CBO scores this provision as providing $49.96 billion in savings for the Treasury relative to the pre-OBBBA baseline (a reduction in impact).64 | |

| Early termination (2028) | 26 U.S.C. §45V Clean Hydrogen | Pre-OBBBA, production of clean hydrogen received up to $3 per kilogram for facilities that began construction before 1/1/33. OBBBA terminated credit for facilities that begin construction after 12/31/27. | Facilities that begin construction before 1/1/28 may still receive the credit; leaves open potential for extension past this date. Nonetheless, CBO scores this as a $5.88 billion savings for the Treasury relative to pre-OBBBA baseline (a reduction in impact).65 |

| Early termination (2026) | 26 U.S.C. §179D Energy Efficient Commercial Buildings Deduction | Pre-OBBBA, commercial properties that commenced construction prior to 2032 could receive $5 per square foot (increased by meeting prevailing wage requirements) if the property reduced energy costs by 25%+. OBBBA terminated credit for property beginning construction after 6/30/26. | Taxpayers can still access the credit for property that begins construction prior to 6/30/26. CBO scores this provision as providing $136 million in savings for Treasury relative to the pre-OBBBA baseline (a reduction in impact).66 |

| 26 U.S.C. §30C | Pre-OBBBA, investment tax credit covered electric vehicle chargers through the end of 2032. OBBBA terminated the credit for any property placed in service after 6/30/26. | Facilities that are placed in service prior to 6/30/26 can still receive the tax credit. CBO scores this provision as providing $2 billion in savings for the Treasury relative to the pre-OBBBA baseline (a reduction in impact).67 | |

| 26 U.S.C. §45L New Energy Efficient Home Credit | Pre-OBBBA, the credit provided up to $5,000 per unit for homes that meet certain federal standards. Post-OBBBA, the credit is not available for property beginning construction after 6/30/26. | Available for taxpayers that begin construction prior to 6/30/26. CBO scores this provision as providing $5.45 billion in savings for the Treasury relative to the pre-OBBBA baseline (a reduction in impact).68 | |

| Early termination (2025) | 26 U.S.C. §25C Nonbusiness energy property credit | Credit for nonbusiness energy property that IRA extended through 2032. OBBBA terminated the credit effective 12/31/25. | Available for taxpayers prior to 12/31/25. CBO scores this provision as providing $21.22 billion in savings for the Treasury relative to the pre-OBBBA baseline (a reduction in impact).69 |

| 26 U.S.C. §25D Residential clean energy credit | Pre-OBBBA, residential taxpayers could obtain a credit equal to a percentage of qualified expenditures for eligible clean energy property installed at their home, through 2034. Post-OBBBA, the credit was only available 9/30/25. | Some taxpayers could still use credit prior to end of 2025. CBO scores this provision as providing $77.36 billion in savings for the Treasury relative to the pre-OBBBA baseline (a reduction in impact).70 | |

| 26 U.S.C. §30D Clean Vehicle Credit | Pre-OBBBA, consumers could acquire a $7,500 per vehicle credit through 2032. OBBBA terminated the credit effective 9/30/25. | Some taxpayers could still use the credit through September 2025. CBO scores this provision as providing $7.78 billion in savings for the Treasury relative to the pre-OBBBA baseline (a reduction in impact).71 | |

| 26 U.S.C. §25E Previously Owned Vehicle Credit | Pre-OBBBA, taxpayers could receive a credit toward a clean new vehicles up to $4000 through 2032. OBBBA terminated the credit effective 9/30/25. | N/A. CBO scores this provision as providing $7.43 billion in savings for the Treasury relative to the pre-OBBBA baseline (a reduction in impact).72 | |

| 26 U.S.C. §45W | Pre-OBBBA, taxpayers could receive a credit of up to $7,500 for light-duty vehicles or up to $40,000 for medium/heavy-duty vehicles, sunsetting at the end of 2032. OBBBA terminated the credit effective 9/30/25. | N/A. CBO scores this provision as providing $104.52 billion in savings for the Treasury relative to the pre-OBBBA baseline (a reduction in impact).73 |

Footnotes

- Other appropriations bills such as the Interior, Environment, and Related Agencies Appropriations bills also fund climate and energy priorities, but have not been incorporated into this assessment.

- The E&W bill includes funding for the DOE’s National Nuclear Security Administration, which has received more than $20 billion in appropriations in recent years. These topline numbers and other calculations exclude these appropriations.

- 2026 President’s Budget Request at 21. $5 billion number includes more than $2.5 billion from EERE, more than $1.1 billion from the Office of Science, $389 million from environmental management, $260 million for Advanced Research Project Agency—Energy, $408 million from the Office of Nuclear Energy, and $270 million from the Office of Fossil Energy. It excludes the $15 billion plus in cuts that the OMB sought from the Infrastructure Investment and Jobs Act sources.

- This includes: Advanced Research Projects Agency-Energy, Clean Energy Demonstrations, Electricity, Energy Efficiency and Renewable Energy, Fossil Energy, Grid Deployment, Nuclear Energy, Office of Science, Office of Technology Transitions, and the Title 17 Innovative Technology Loan Guarantee Program.

- Specifically, Section 311 of the FY26 E&W bill reprograms $1.28 billion from the Civil Nuclear Credit Program, $1.5 billion from the Carbon Dioxide Transportation Infrastructure Finance and Innovation Program, $1.04 billion from regional direct air capture hubs, $950 million from carbon capture large-scale pilot projects and carbon capture demonstration projects program, and $393 million from energy programs under EERE.

- Government Accountability Office, Department of Energy: Plan Needed to Meet Statutory Requirements for Clean Energy Demonstration Projects, February 11, 2026. Available at: https://www.gao.gov/products/gao-26-107997.

- Explanatory Statement Submitted by Mr. Cole, Chair of the House Committee on Appropriations, Regarding H.R. 6938, Commerce, Justice, Science; Energy and Water Development; and Interior and Environment Appropriations Act, 2026; Volume 172 at H390 of the Congressional Record (January 8, 2026).

- Appendix to the Budget of the United States Government, Fiscal Year 2027, at 382-411.

- Some elements of EERE (the Advanced Materials & Manufacturing Technologies Office, the Industrial Technologies Office, and Building Technologies Office) have been moved to Critical Minerals and Energy Innovation, with budget requests significantly reduced from FY26. Geothermal Energy has been moved to the Hydrocarbons and Geothermal Energy Office from EERE. Department of Energy FY27 Congressional Justification Budget in Brief at 43,66. Available at: DOE FY 2027 Budget in Brief.

- The Trump administration total includes funding previously allocated to the Grid Deployment Office to arrive at an FY26 appropriation level of $259 million. Id. at 50.

- “As a result of the Department’s reorganization, amounts in the current year as well as prior year balances for research, development, demonstration and deployment to unleash the full potential of America’s hydrocarbon resources in the Fossil Energy (FE) account will be administered by the Hydrocarbons and Geothermal Energy Office (HGEO). Funding that was appropriated through the Mineral Sustainability Control Point, with the exception of Carbon Ore Processing work, will now be managed by the Office of Critical Minerals and Energy Innovation (CMEI), formerly the Office of Energy Efficiency and Renewable Energy. In addition, the Geothermal Energy funding appropriated through CMEI will be managed by HGEO. HGEO and CMEI are finalizing an MOU delineating a framework for cooperation and collaboration regarding the efficient and effective transfer of resources, and operational oversight of the functions. All other funding will continue to be overseen by HGEO.” Appendix to the Budget of the United States Government, Fiscal Year 2027, at 397.

- The Energy Act of 2020 was technically passed as part of the Consolidated Appropriations Act of 2021, Pub. L. 116-260.

- Between 2020 and 2025, Energy Act of 2020 provisions that have seen appropriations in succeeding years include sections 1005, 1006, 1011, 2001, 2005, 3003, 3004, 3005, 3201, 4002, 4003, 4004, 5001, 6003, 7001, 8013, 9001, 9010, and 10001.

- “…Congress has on occasion appropriated money to fund programs with expired authorizations of appropriations. Because the distinction between authorizations and appropriations is a construct of congressional rules, it applies only to the consideration of legislation. If Congress appropriates funds for a program whose funding authorization has expired, that appropriation provides sufficient legal basis to continue the program during that period of availability absent indication of congressional intent to terminate the program.” Authorizations and the Appropriations Process, Congressional Research Service, May 16, 2023. Available at: Authorizations and the Appropriations Process | Congress.gov | Library of Congress.

- 31 U.S.C. §1301.

- See, e.g., Explanatory Statement Submitted by Mr. Cole, Chair of the House Committee on Appropriations, Regarding H.R. 6938, Commerce, Justice, Science; Energy and Water Development; and Interior and Environment Appropriations Act, 2026; Volume 172 at H390 of the Congressional Record (January 8, 2026) (directing Department of Energy to spend $45 million to carry out the CDR Purchase Pilot Prize as directed in the Fiscal Year 2023 Act).

- Politico, Hopes fade for highway bill ahead of Sept. 30 deadline, March 13, 2026. Available at: https://subscriber.politicopro.com/article/2026/03/highway-bill-expected-to-miss-sept-30-deadline-00825717.

- Sections 10102, 10103, 10105, 10222, 10233, 10303, 10359, 10381-10399A, 10622, 10641, 10691, 10713, 10714, 10715, 10716, 10722, 10731, 10741-10745, 10751, 10771, 10781, 10833, and 10723. Note that some provisions are grouped together because they are part of the same program.

- The Joint Explanatory Statement accompanying the FY26 E&W appropriations bill also directed $25 million for the Carbon Sequestration Research and Geological Computational Science Initiative, as authorized in Section 10102(f) of the CHIPS and Science Act of 2022. Joint Explanatory Statement, supra note 14, at H394.

- Congressional Budget Office, Estimated Budgetary Effects of Public Law 117-169, to Provide for Reconciliation Pursuant to Title II of S. Con. Res. 14, Sept. 7, 2022. Available at: https://www.cbo.gov/system/files/2022-09/PL117-169_9-7-22.pdf.

- Congressional Budget Office, The Budget and Economic Outlook 2024 to 2034 at 87 Box 3-1 (noting that $151 billion is from reductions in projected revenues due to reductions in the gasoline excise tax, $73 billion in increased outlays for the clean vehicle tax credits, $153 billion in other reductions in projected revenues driven by other clean energy tax provisions, and $51 billion in outlays for clean energy provisions).

- Goldman Sachs, The U.S. is poised for an energy revolution, April 17, 2023 (estimating scale of credits at $1.2 trillion). Available at: https://www.goldmansachs.com/insights/articles/the-us-is-poised-for-an-energy-revolution.

- Despite recent guidance on material assistance calculation and related safe harbors released by Treasury and the Internal Revenue Service on February 12 as Notice 2026-15, other key guidance areas remain open.

- Congressional Budget Office, Publication 61570. Includes a reduction of ~$72 billion in direct spending and increased tax revenues of ~$430 billion. Available at: Estimated Budgetary Effects of Public Law 119-21, to Provide for Reconciliation Pursuant to Title II of H. Con. Res. 14, Relative to CBO’s January 2025 Baseline | Congressional Budget Office.

- CATF analysis of Joint Committee on Taxation publications JCX-18.22, JCX-7-23, and JCX-35.25. Available at https://www.jct.gov/publications/2022/jcx-18-22/, 7 https://www.jct.gov/publications/2023/jcx-7-23/, and https://www.jct.gov/publications/2025/jcx-35-25/.

- Bipartisan support to expand the 45X credit after OBBBA can also be seen in H.R. 5441, the Fusion Advanced Manufacturing Parity Act, which has four Democratic co-sponsors and six Republican co-sponsors. Available at: https://www.congress.gov/bill/119th-congress/house-bill/5441.

- Department of the Treasury, The Inflation Reduction Act: Saving American Households Money While Reducing Climate Change and Air Pollution, Aug. 7, 2024. Available at The Inflation Reduction Act: Saving American Households Money While Reducing Climate Change and Air Pollution | U.S. Department of the Treasury.

- Internal Revenue Service, SOI tax stats – Clean energy tax credit statistics, January 16, 2025. Available at SOI tax stats – Clean energy tax credit statistics | Internal Revenue Service.

- U.S. Department of the Treasury, U.S. Department of the Treasury Announces More Than $2 Billion in Upfront Savings for Consumers on Electric and Plug-In Hybrid Vehicles Sales under Biden-Harris Administration’s Inflation Reduction Act, October 1, 2024. Available at: https://home.treasury.gov/news/press-releases/jy2626.

- IRA Sections 50172, 50221, 50222, 50223.

- Utility Dive, Court agrees to rehear $14B climate funding freeze case, Dec. 18, 2025. Available at: https://www.utilitydive.com/news/appeals-court-rehear-climate-funding-freeze/808298/.

- IRA Sections 23002, 30002, 40004, 40007, 50123, 50152, 50161, 60101, 60104, 60105(a), 60106, 60108(a), 60113, 60114, 60201, 60503, 60506. 23003 was partially repealed ($1.5 billion).

- IRA Sections 22002, 22003, 22004, 510121, 50122, 50131, 50143, 80001, 80002, 60102, 60402, 21002.

- IRA Sections 21002, 22001, 40005, 50172, 50173, 70002(1) and 70002(2), 70007, 80003.

- The FY26 E&W bill provided $9.5 million for the Advanced Technology Vehicles Manufacturing Loan Program. Joint Explanatory Statement, supra note 14, at H397. The money is likely to conduct management of grandfathered obligations and wind-down activities for the repealed ATVM authority.

- This analysis relies on three data sources: FedScope, the 2025 President’s Budget Request, and the Bureau of Labor Statistics estimate for government employment. Each source has its limitations, and so we use them in combination. The President’s Budget Request Data has estimates for 2025 and 2026. The Bureau of Labor Statistics data is taken from each September for comparability with FedScope, with the exception of the 2025 number, which references October to capture the effects of the deferred resignation program implemented early in the Trump administration.

- The Council of Environmental Quality during the Biden administration included political appointees, detailees, and other personnel beyond typical civil servants.

- Bureau of Labor Statistics, CES Data, All Federal, Seasonally adjusted except postal service.

- Id.

- Note that these data do not precisely match the data in the FedScope data source.

- Partnership for Public Service, The Unraveling of Public Service: How one year dramatically changed the federal service landscape. Available at: The Unraveling of Public Science • Partnership for Public Service.

- U.S. government has lost more than 10,000 STEM PhDs since Trump took office, Science, 26 January 2026. Available at: U.S. government has lost more than 10,000 STEM Ph.D.s since Trump took office | Science | AAAS.

- CATF has already covered this topic. See The High Cost of Retreat: Impacts of Department of Energy Project Cuts, November 21, 2025. Available at The High Cost of Retreat: Impacts of Department of Energy Project Cuts – Clean Air Task Force.

- All data here is based on excerpts from USASpending.gov.

- Letter from the Ranking Member of the Committee on Science, Space, and Technology, Representative Zoe Lofgren, December 18th, 2025. Available at SST Minority – Letter to Secretary Wright – OCED Elimination – 12.18.25.pdf.

- Joint Explanatory Statement, supra note 14, at H390.

- Letter from Senators Murray and Heinrich to Secretary of Energy Chris Wright, February 11, 2026. Available at: subscriber.politicopro.com/eenews/f/eenews/?id=0000019c-4ef5-d0f8-adde-feff5f360002.

- All data pulled from the federal assistance portion of the USASpending.gov. Analysis performed by the Clean Air Task Force, using the program activity name field to focus on relevant spending.

- CATF analysis, based on data from USASpending.gov. Excludes program activities for defense-related Department of Energy spending, basic energy sciences, energy justice and equity, unspecified program direction, unspecified strategic programs, supercritical CO2, critical minerals, cross-cutting research, and carbon ore processing.

- Section 406 of the American Recovery and Reinvestment Act of 2009 (Pub. L. 111-5) provided a temporary expansion of Section 1703 of the Energy Policy Act of 2005 to cover loan guarantees renewable energy systems, electric power transmission systems, and certain biofuels projects. The law also appropriated $6 billion for that purpose.

- Section 50141 of the Inflation Reduction Act (Pub. L. 117-169) expanded existing loan guarantee authority by $40 billion and also included $3.6 billion to cover the cost of the loan guarantees. Section 50144 made eligible projects that would “retool, repower, repurpose or replace energy infrastructure that [had] ceased operations” or “enable operating infrastructure to avoid, reduce, utilize, or sequester air pollutants or anthropogenic emissions of greenhouse gases.” Section 40401 of IIJA (Pub. L. 117-158) expanded eligible projects under Section 1703 of the Energy Policy Act of 2005 to include certain critical minerals projects.

- Ramsey Fahs, Alan Propp, and Louise White, Implementing Federal Clean Energy Programs: Lessons Learned from DOE and Partner Agencies, Summary Report, October 2025, at 4. Available at: implementation-report.pdf.

- Id.

- Section 50402 and 50403 of the One Big Beautiful Bill Act (Pub. L. 119-1).

- U.S. Department of Energy, Energy Department Reins in Over $83 Billion in Biden-Era Loans and Conditional Commitments, January 22, 2026. Available at: Energy Department Reins in Over $83 Billion in Biden-Era Loans and Conditional Commitments | Department of Energy.

- Jake Bittle, This $400B Biden climate programs is surviving the Trump administration, March 23, 2026.Available at: This $400B Biden climate program is surviving Donald Trump | Grist.

- Id. (noting that the $26.5 billion loan to Southern Company substitutes 5 gigawatts of gas power for a solar project but noting that the solar project will still be built).

- Congressional Budget Office, supra note 22.

- Id.

- Congressional Budget Office, supra note 18.

- Congressional Budget Office, supra note 22.

- Id.

- Id.

- Id.

- Id.

- Id.

- Id.

- Id.

- Id.

- Id.

- Id.

- Id.

- Id.