Building demand for decarbonised products of heavy industry in the EU: Recommendations for the Industrial Decarbonisation Accelerator Act

Key recommendations

- Establish harmonised methodologies and labelling protocols for embodied carbon in key products of heavy industry, by applying common principles to existing, well-established standards.

- Establish labels with intermediate and progressive decarbonisation categories for industrial products, including clear and ambitious thresholds for categories of ‘lower-emission’ and ‘near-zero emission’ products to aid policy design.

- Expand mandatory requirements for embodied emissions reporting for a wide range of manufactured products using cement, steel, ammonia and other chemicals, including clear indication of the embodied carbon in these basic material inputs, assessed to a common standard and process stage.

- Ensure demand-side drivers are designed to directly incentivise deep decarbonisation projects in energy- intensive industries, for example, by limiting the free attribution of emissions reductions.

- Harmonise and strengthen public procurement targets and mandates for reducing the embodied carbon in purchased materials.

- Design and adopt demand-side mandates for purchase of decarbonised materials in selected end-use sectors with high potential impact on upstream decarbonisation. For example, by setting quotas on the proportion of lower-emission and near-zero emission products (such as cement, steel, and fertiliser inputs) in purchases by actors at an appropriate stage in the value chain. Target sectors could include construction, automotive, food retail, and packaging.

- In parallel, apply overarching limits on the embodied carbon of selected end-use products and buildings, with gradual tightening of limits over time.

Introduction

Heavy industry sectors, such as steel, cement, chemicals, and refining, emit over 500 million tonnes of CO2 annually in the European Union (EU), accounting for 20% of the total CO2 emissions.1 Industrial emissions have declined relatively little in the past decade, as incremental improvements to existing processes approach their limits. At the same time, some heavy industries face growing competitive pressure from imported, often more carbon-intensive goods. As heavy industry becomes increasingly exposed to the EU Emissions Trading System (ETS) through the phase-out of free allowances, it will need to invest significantly in new technologies and transformative production processes that are compatible with near-zero emissions.

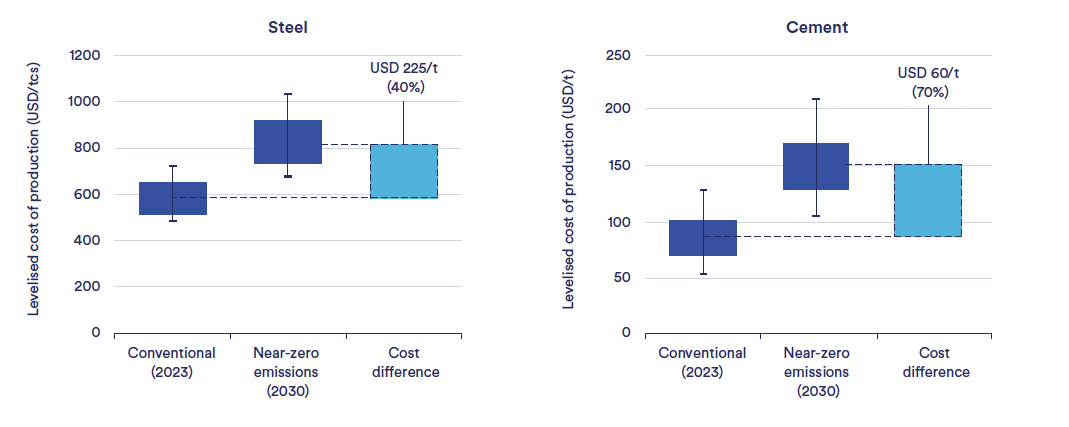

Direct process electrification must play a significant role in decarbonising industrial processes (particularly process heat), but hydrogen and carbon capture and storage (CCS) will also be needed at large scales for some highly emissions-intensive sectors, particularly to address process emissions or where the technology readiness of electrification is low. Depending on multiple site-specific factors, each of these decarbonisation routes can impose a significant cost penalty relative to unabated production processes. The International Energy Agency (IEA) estimates that the production of near-zero emissions steel increases cost by up to 75%, while cement could increase by up to 125% (Figure 1).2 CATF’s analysis of cement decarbonisation costs indicates even higher increases of up to 200% for first-mover projects in locations with higher CO2 transport costs.3 Detailed analysis of the refining sector estimates CO2 costs of over 330 euro per tonne would be required to drive deep decarbonisation projects at European refineries.4 The situation is similar for chemical sector decarbonisation, most notably for the steam crackers which are responsible for producing base chemicals. While these cost gaps are expected to decline over time as technologies and infrastructure develop, there is usually no viable business case to invest in highly decarbonised processes at current carbon prices, with some projects even passing final investment decision (FID) but eventually being cancelled due to lack of offtake.5

Figure 1. The levelised cost of production for near-zero emissions cement and steel, compared with unabated conventional production.2

In addition to the cost gap, decarbonising industries frequently face a number of other barriers to project development:

- Access to enabling resources and infrastructure, including decarbonised electricity, hydrogen supply and CO2 transport and storage.

- Lengthy and complex permitting for connections to the electric grid due to fragmented regulation across the Member States.

- The need for coordination between multiple industrial sites to achieve economies of scale for infrastructure.

- Access to finance for decarbonisation projects – exacerbated by the challenging outlook for EU heavy industry.

- Insufficient willingness to pay a premium for products with reduced carbon intensity.

- Overcapacity in many industries leading to underutilization of existing assets and challenging further investment.

- Ageing facilities which can struggle to compete economically with producers outside the EU.

- Regulatory barriers to the adoption of new materials, such as composition-based standards for cement standards for cement.

The role of supply-side measures

To support the currently inadequate incentive provided by the ETS, policy efforts to accelerate industrial decarbonisation in the EU have largely taken the form of government subsidies for research-scale projects and a few first-of-a-kind commercial plants. Most notably, the Innovation Fund for large-scale projects has awarded over €5 billion to projects aimed at decarbonising cement, lime, steel, chemicals and refining.6 Dedicated funding from Member States has included grant awards and carbon contract for difference (CCfD) schemes such as Germany’s Klimaschutzverträge and France’s funding call for Grands Projets Industriels de Décarbonation.7

Support in the form of capital grants and long-term contracts is critical, particularly for deploying appropriately sized (‘future-proofed’) enabling infrastructure and first-of-a-kind projects for new technologies. Competitively allocated CCfDs – potentially targeted to specific sectors – will also be an effective mechanism for rolling out several large-scale examples of the most cost-competitive technologies and bringing them to commercial maturity. CATF recommends that the EU’s proposed Industrial Decarbonisation Bank provides such a mechanism for the wider roll out of industrial decarbonisation technologies, many of which will be trialled at large-scale first-of-a-kind plants under the Innovation Fund.

However, with climate action competing for increasingly constrained government budgets, subsidies are unlikely to be available at the scale and duration required to decarbonise EU heavy industry. It will be necessary to combine these incentives with measures to grow demand for decarbonised products.

The potential for demand-side incentives

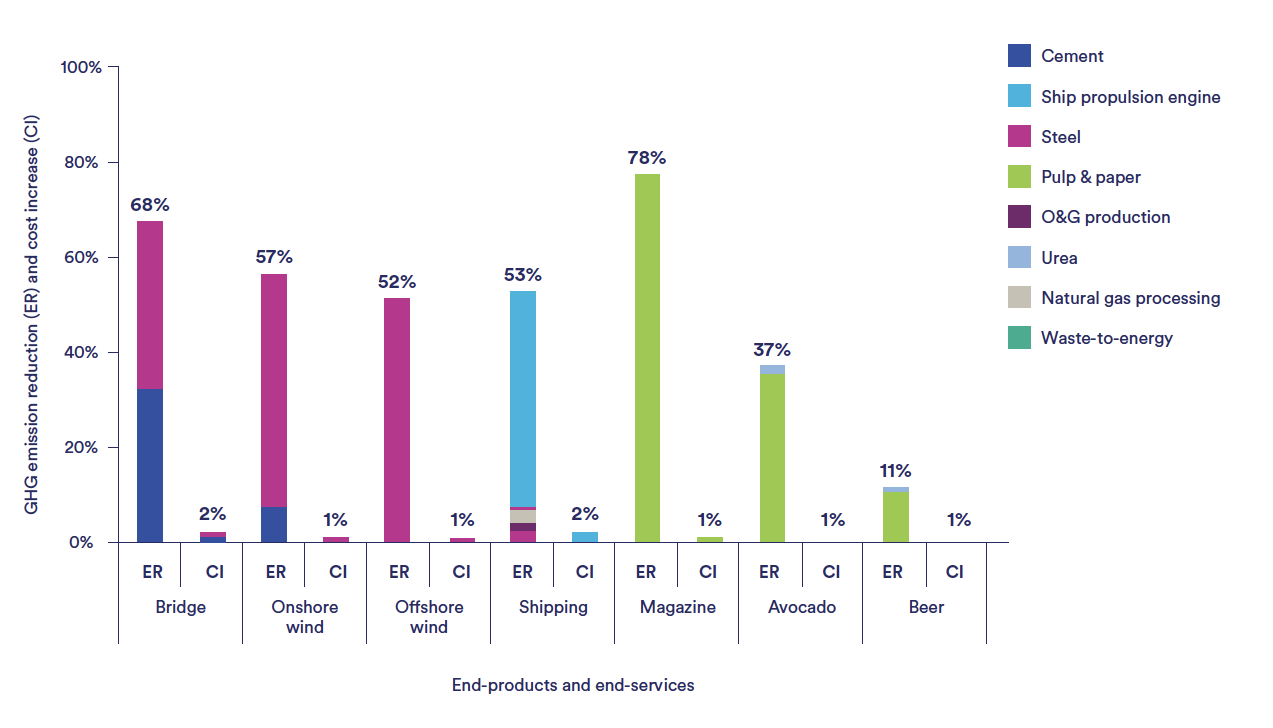

A growing number of studies have highlighted that the use of highly decarbonised material inputs can lead to very small increases in the cost of end-use products, such as buildings, cars, food products, packaging, and transport and energy infrastructure. In most examined cases, material cost increases lead to an end-use product cost increase in the range of 0.5-3% (Figure 2).8 This effect is simply a result of the smaller cost contribution from material inputs for products further down the value chain. Many end-use product markets may be able to absorb these modest cost increases, particularly for higher-value products and those exposed to consumer demand for decarbonised products. In theory, this cost increase could be passed through the value chain and be realised as a significant green premium on decarbonised materials upstream. In combination with carbon pricing (which will also drive an increase in the price of heavy industry outputs), this market demand can enable direct government support for industrial decarbonisation to be phased out more rapidly.9 Long-term offtake agreements for decarbonised products should also provide a more bankable revenue stream than reliance on the relatively volatile carbon price.

Figure 2. Relative cost increases and emissions reductions for a selection of products decarbonised using CCS10

There has been significant recent momentum in voluntary private sector commitments to buy decarbonised products, often through membership of demand aggregation initiatives. For example, members of the First Movers Coalition commit to procurement targets for near-zero emissions steel and low-emissions cement.11

First-of-a-kind plants in both cement and steel sectors have secured advance commitments to buy decarbonised products. For example, Stegra has binding offtake agreements for ‘green steel’ from their plant currently

under construction (producing steel using green hydrogen) with around 20 customers, including automobile manufacturers, and homeware suppliers, at a green premium of 25%.12 Heidelberg Materials’ Brevik cement plant, which commenced CCS operations in July 2025, has stated it has pre-sold all the production of ‘net-zero cement’ branded evoZero for 2025, with buyers including building materials manufacturers.13 The green premium on this cement is unknown.

While these initiatives have made progress for bulk commodities such as steel and cement, they can be more challenging to implement in the chemical sector, where tens of thousands of chemicals are sold onto the market. Nonetheless, the carbon intensity of intermediate bulk chemicals such as film polyethylene or injection-moulded polypropylene are well understood and could be a promising option for demand-side measures.

In practice, leveraging the effect of relatively small cost increases in end products can be challenging, even where there is consumer willingness to buy, for reasons including:

- Voluntary demand is inadequate both in volume and willingness to pay a sufficient ‘green premium’.

- Supply of low-carbon materials may not align with demand in time or location.

- Passing on embodied carbon accounting and willingness to pay can become challenging along complex product value chains, such as those of engineered plastics.

- Diverse carbon accounting methodologies and product labelling lead to a fragmented market and negatively impact buyer confidence.

Voluntary markets are therefore not well-suited to driving industrial decarbonisation at the pace and scale required by the EU’s climate targets. To date, they have tended to respond to the development of deep decarbonisation projects (funded by the EU or national governments), rather than actively driving their deployment by helping close the cost gap and increase project bankability.

EU policy can play a critical role in creating more effective lead markets for energy-intensive industries by harmonising product standards and labelling for embodied carbon, setting ambitious targets for public procurement, and pioneering compliance markets for the private sector. These steps are discussed further in the following sections.

Harmonising standards and product labelling

Transparent accounting methodologies, reporting requirements and labelling for embodied carbon in intermediate and final products are a prerequisite for demand-side drivers to function. There is currently a diverse set of existing labels and certification methodologies for decarbonised industrial products – particularly for cement and steel – variously developed by non-profit organisations, international organisations, governments, and industry.14 For many end-use products, Environmental Product Declarations (EPDs) are the principal mechanism for reporting and are increasingly required in some sectors. All these reporting mechanisms are primarily based on the same underlying methodologies for greenhouse gas accounting, developed under the International Standards Organisation, European Standards, and Greenhouse Gas Protocol. However, these can still differ significantly according to factors including:

- Inclusion of other environmental and social criteria.

- Variation in data quality.

- Different approaches to mass-balance accounting and chain of custody.

- Treatment of recycled scrap content and (for cement) clinker content.

- Greenhouse gas accounting for process by-products such as blast furnace slag.

Many of these existing standards only serve to provide a common methodology for measuring and reporting climate impact. An additional and essential step is to define a common labelling or rating system with specific thresholds for the level of product decarbonisation required to achieve a given label.

The EU has already taken significant steps towards harmonising and mandating environmental performance labelling. The recently revised Construction Products Regulation (CPR) requires all products used in the construction sector to have Declarations of Performance which, in addition to other information, will cover similar environmental reporting requirements to EPDs.15 The Ecodesign for Sustainable Products Regulation (ESPR) requires most products on the EU market to declare a wide variety of environmental performance criteria, including global warming potential indicators, in the form of a digital product passport.16 The ESPR also provides a legislative framework to set thresholds for permissible levels of environmental performance,17 which could be applied to various products of heavy industry, although construction materials will remain under the remit of the CPR.

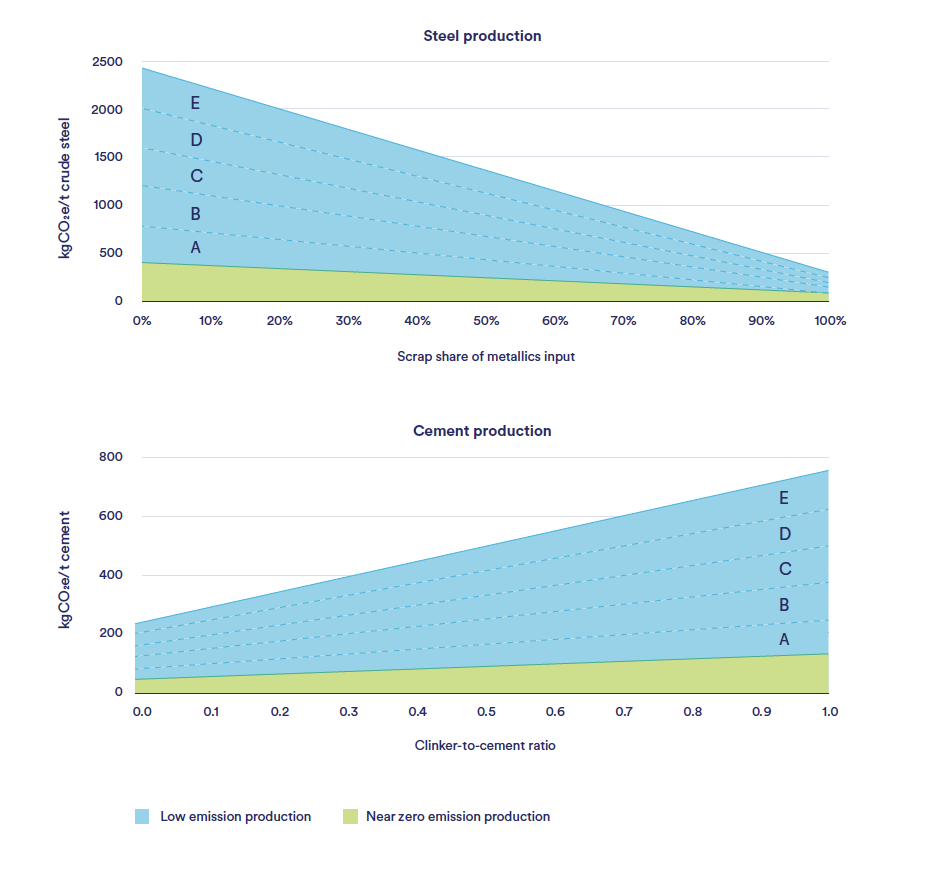

In 2022, the International Energy Agency (IEA) put forward a definition for ‘near-zero emission’ steel and cement, as well as a banded rating system for intermediate levels of decarbonisation, which have been widely adopted and modified by other certification systems (Figure 3).18 For example, non-profit organisation ResponsibleSteel and Germany’s Low-Emission Steel Standard (LESS) apply the same ’sliding scale’ principle of requiring greater levels of decarbonisation for steel with higher scrap content to achieve a given low-emissions label. This approach reflects the greater challenge in decarbonising primary steel production from iron ore. Similarly, the IEA’s classifications for near-zero and low-emission cement require greater levels of decarbonisation with decreasing clinker content (Figure 3). The low-carbon cement label developed by Verein Deutscher Zementwerke e.V. (VDZ) has made use of this methodology, applied to a fixed clinker content of 70%.19 Other groups have developed similar rating systems for concrete, on the basis that cement is usually sold in this form, and enabling decarbonisation thresholds to be set according to material strength class.20

Figure 3. The International Energy Agency’s proposed definitions for low-emission and near-zero emission steel and cement

IEA. All rights reserved

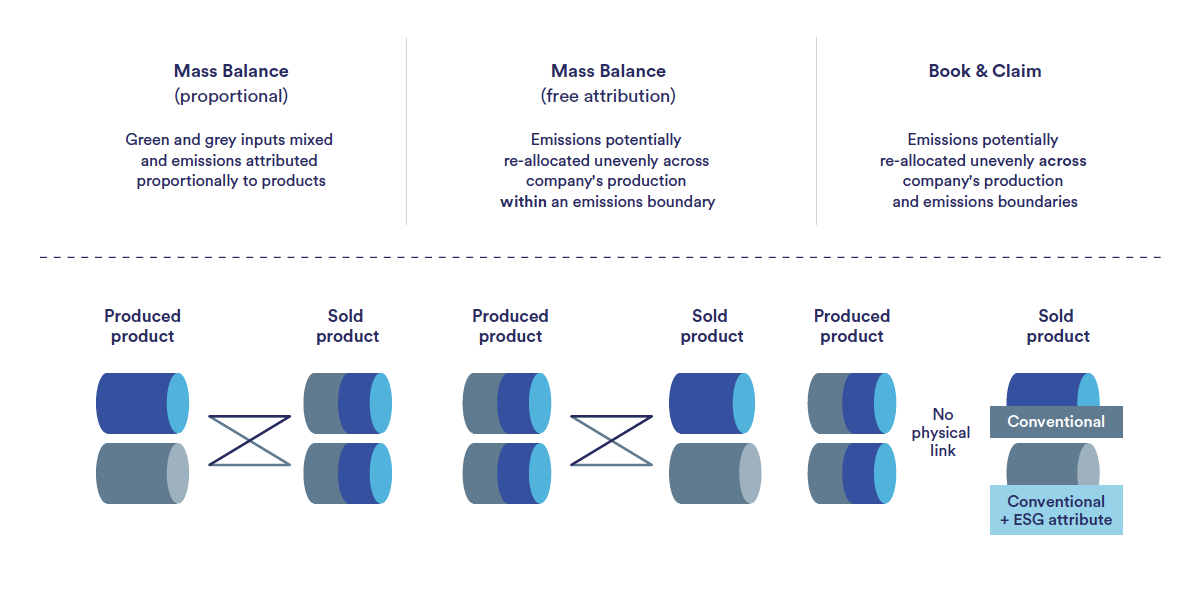

Figure 4. Different chain of custody models used to generate products with reduced emissions intensity21

Different approaches to mass-balance accounting and chain of custody require particular attention when harmonising product labelling. Currently, some reporting methods employ free attribution of greenhouse gas savings, where incremental reductions across several process steps or sites can be aggregated as larger reductions in a single product unit (Figure 4). This approach can hinder investment in deep decarbonisation projects by reducing the incentive to achieve significant reductions through transformational technologies for a single production process. In contrast, proportional allocation distributes greenhouse gas savings in process inputs evenly across all product outputs. Some flexibility in the allocation of CO2 abatement may be pragmatic for incentivising deep decarbonisation projects. For example, if a process can achieve over a threshold reduction in emissions, it could be possible to concentrate the achieved reduction on a portion of the output (i.e. to gain ‘near-zero emission’ status for that portion). Any threshold should be ambitious, determined by technology availability and progressively reassessed.

‘Book and claim’ is a means of allowing producers of decarbonised products to decouple the delivery of physical product from the actual decarbonised process, through the transfer of a certificate. This greatly expands the market accessible to the product, which may be particularly limited for cement, given that it is mostly used in local markets. For the early stages of growing product demand, book and claim could be a valuable tool for aggregating and enhancing the demand signal for some decarbonised products. However, it requires appropriate safeguards to ensure transparency and a clear chain of custody, and should be reassessed once the market has become more established. It should not be used to aggregate reductions over multiple processes or sites, but as a means of expanding the market for near-zero emission products from a single site. Book and claim also risks diminishing early demand for low-carbon output from facilities in regions facing higher decarbonisation costs. This could be mitigated by supply side policies which support decarbonisation projects in diverse Member States.

CATF recommendations to ensure accounting methodologies and labels can drive deep decarbonisation projects at industrial facilities:

- Include a clear and ambitious ‘near-zero emission’ or deep decarbonisation label in addition to intermediate and progressive decarbonisation categories for lower-emission products.

- Ensure materials and end products display total embodied emissions in addition to category-based labels for their basic input materials.

- Strictly limit the free attribution of emissions in labelling to ensure a strong incentive for investments enabling the deep decarbonisation of individual emissions-intensive production processes.

- Allow rigorous ‘book and claim’ accounting to the extent that one unit of physical near-zero emissions product can generate a certificate which can be allocated to a unit of unabated product.

- Provide guidance on acceptable data sources used in embodied carbon accounting and require transparent reporting and verification of sources used.

- Standardise accounting for alternative fuels, process byproducts and recycled scrap, e.g., through a ‘no allocation’ and ‘cut-off’ approach.

- Set near-zero emissions labels for steel and cement according to scrap and clinker content, to ensure a distinct focus on decarbonising the hardest-to-abate materials.

Leveraging green public procurement to decarbonise industry

Public procurement accounted for 14% of EU GDP in 2019 and represents a significant proportion of demand for some basic materials.22 Analysis by the Industrial Deep Decarbonisation Initiative finds that public procurement in Germany accounts for 23% of total cement demand and 5% of total steel demand.23 Maximising the levels of green public procurement (GPP) – accounting for environmental criteria as well as cost in bid assessments – is often highlighted as the most straight-forward means for policy to build demand for decarbonised products, given that governments can exert direct control over their purchasing choices and can operate within existing legislative frameworks for GPP. While a guiding framework for GPP exists at the EU level, implementation in Member States is highly varied, relatively limited in scope, and lacking sufficient focus on the carbon intensity of material inputs.24 The proportion of public procurement which can be classified as ‘green’ accounts for less than 5% of contracts in most countries.25

The Netherlands is a frontrunner in applying GPP principles, which have been mandatory for public authorities since 2015, and has developed a CO2 Performance Ladder as a tool for assessing the climate performance of bidding contractors.26 Ireland has mandated the use of cement with a minimum of 30% clinker replacement for public buildings.27

There are several examples of municipalities, often driven by their own decarbonisation targets, implementing particularly ambitious environmental requirements for procurement. Notably, since 2013, the City of Zurich has specified CEM III/B standard cement (with a clinker content of 20-34%) for all buildings it procures.28 The city of Hamburg has pledged to use cement and steel with growing levels of decarbonisation in the construction of the U5 metro line, including cement with partial CCUS from 2028 and 100% CO2 capture from 2035, as well as green steel from 2035.29

New requirements for GPP under the Construction Products Regulation can help strengthen the role of the public sector as a lead market for decarbonised construction materials.30 Article 83 of the regulation requires the Commission to adopt delegated acts which set minimum environmental sustainability requirements for construction products. The ESPR also requires Green Public Procurement to include minimum environmental requirements. However, for public procurement to fulfil its potential as a driver for deep decarbonisation projects, it should incorporate targets or quotas for procurement of lower-emission and near-zero emission material inputs. The revision of the Public Procurement Directive in 2026 provides an opportunity to bring greater climate ambition and consistency across the EU.

Compliance markets to drive private sector demand

There are several possible regulatory approaches to bringing about a rapid and more predictable shift in private sector procurement towards decarbonised materials, including:

- Limits on the embodied carbon or life-cycle emissions for end-use products: These provide an entirely technology-neutral demand signal to the market. Examples include building standards set by voluntary building codes or building regulations.

- Limits on the carbon or greenhouse gas intensity of input materials for specific end-use sectors.

- Quotas on the proportion of lower-emission and/or near-zero emission materials in private purchases, potentially applied for specific sectors or purchase volumes.

Limits on the embodied carbon and/or lifecycle carbon emissions of end-use products such as buildings, automobiles, machinery, household goods and food products provide an important overarching, technology neutral driver for more climate-compatible design and procurement choices in the private and public sectors. In addition to the use of decarbonised conventional products, such limits can be met by reducing the excessive use of emissions-intensive inputs and utilising alternative materials. Standards for embodied and lifecycle emissions in buildings are established in the form of voluntary certification schemes such as Leadership in Energy and Environmental Design (LEED) and Building Research Establishment Environmental Assessment Method (BREEAM),31 and mandatory reporting of embodied carbon will be required under the EU’s Energy Performance of Buildings Directive (EPBD), when implemented into national law.32 The EPBD requires all new buildings to report embodied carbon from 2028 and for Member States to set roadmaps for decarbonising the building stock. Similar approaches can be applied to other product sectors with significant upstream emissions, either through supporting legislation under the ESPR, or through the forthcoming IDAA.

However, more direct, stable demand signals are needed to help close the cost gap and unlock finance for deep decarbonisation projects in industry – analogous to the long-term offtake agreements which are currently driving investment in many engineered carbon dioxide removal projects.33 This could be provided by more targeted demand-side mandates on the purchase of emissions-intensive products such as cement, steel, and fertiliser. For example, a mandate to reduce the overall carbon intensity of these inputs, in parallel with quotas to procure a small but rising proportion of near-zero emission materials. Such an approach would establish confidence in future product demand and can draw on experience from similar mandates in other hard-to-abate sectors.

Learning from decarbonisation mandates in other sectors

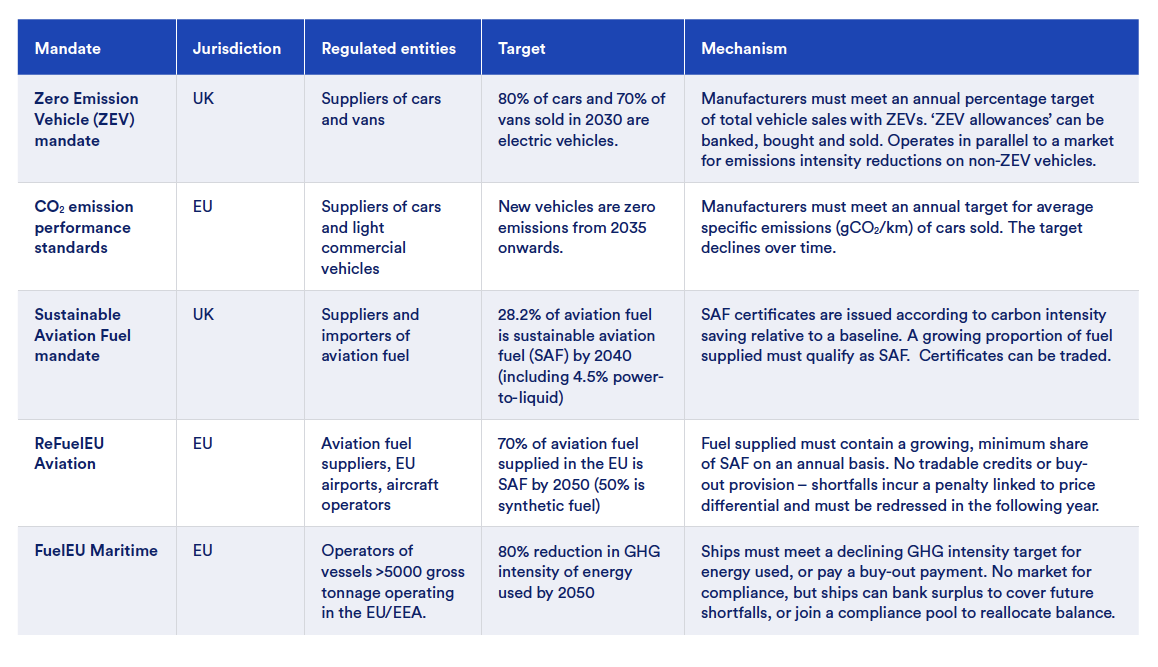

In recognition of the need for additional regulatory drivers to support carbon pricing, the EU and other jurisdictions have implemented mandates for the decarbonisation of hard-to-abate transport sectors such as shipping and aviation (Table 1). These mandates complement carbon pricing and incentivise more targeted sectoral transformation with a clear decarbonisation trajectory, and even the scale up of specific technologies.

Table 1. Existing decarbonisation mandates for hard-to-abate transport sectors34

A key advantage of the greater certainty provided by a mandate – relative to cap-and-trade carbon pricing alone – is that they can resolve coordination failures for deployment of supporting infrastructure, such as charging infrastructure for electric vehicles. This infrastructure becomes more investable when there is a mandated trajectory for scale up of the target sector, which in turn unlocks consumer confidence.

Applying similar demand-side mandates to sectors currently using emissions-intensive products would involve several key design choices and face new challenges and considerations. Some products and end-use sectors offer greater suitability for application than others. In particular, mandates on consumer products which are relatively exposed to international trade will need to ensure competing imported products can be assessed to the same standard. Upstream sectors with export markets may need to sell some decarbonised output into regions without a mandate and corresponding green premium. Mandates on downstream sectors will tend to be more effective at driving upstream decarbonisation when:

- The end-use product incorporates a high proportion of the basic material outputs of heavy industry (i.e., steel, cement, fertiliser, high-value chemicals).

- The input materials contribute a significant proportion of the total embodied emissions in the end-use product.

- The input materials represent a relatively low share of the final product cost.

- The number of entities to regulate in the end-use sector is relatively low (administratively less complex).

- The end-use sector is less exposed to competition from imported end-use products produced in regions without the obligation.

Once a suitable product or sector has been selected, a critical design choice will be where the obligation is placed in the material value chain. This should take into account the administrative complexity associated with regulating a larger number of entities, as well as the ability to pass on costs to the next stage in the value chain. Targets can be met directly by obligated entities, or a system of trading compliance certificates can be established. As for some examples in Table 1, sub-mandates for near-zero emission products could be included in addition to an overarching mandate on declining carbon intensity of material inputs. Another key design choice is the level at which carbon intensity and procurement targets be set. Overall, carbon intensity targets should decrease to zero by 2050, as outlined in Table 1. Quotas for low-emission and near-zero emission products could reflect an ambitious yet feasible deployment of decarbonised production capacity.

Demand-side mandates for industrial decarbonisation: sectoral analysis

Based on the above criteria, several consumer-facing sectors emerge as potentially promising candidates for the implementation of demand-side mandates, which could have a significant impact on the decarbonisation of upstream processes. These include buildings and construction (targeting cement, steel and potentially plastic), automotive and household good sectors (targeting steel), food retail (targeting fertiliser production), and packaging (targeting plastic and paper production). For each of the sectors examined below, it is clear that the initial stages of deployment for deep decarbonisation technologies, including cement with CCS, hydrogen based steel, green/blue ammonia, or electrified steam cracking, will be a small fraction of total sectoral demand. However, using a robust system of book-and-claim to decouple physical production from ‘decarbonised production’, it should be possible to aggregate initially incremental demand into a meaningful investment signal for the first production facilities.

Buildings

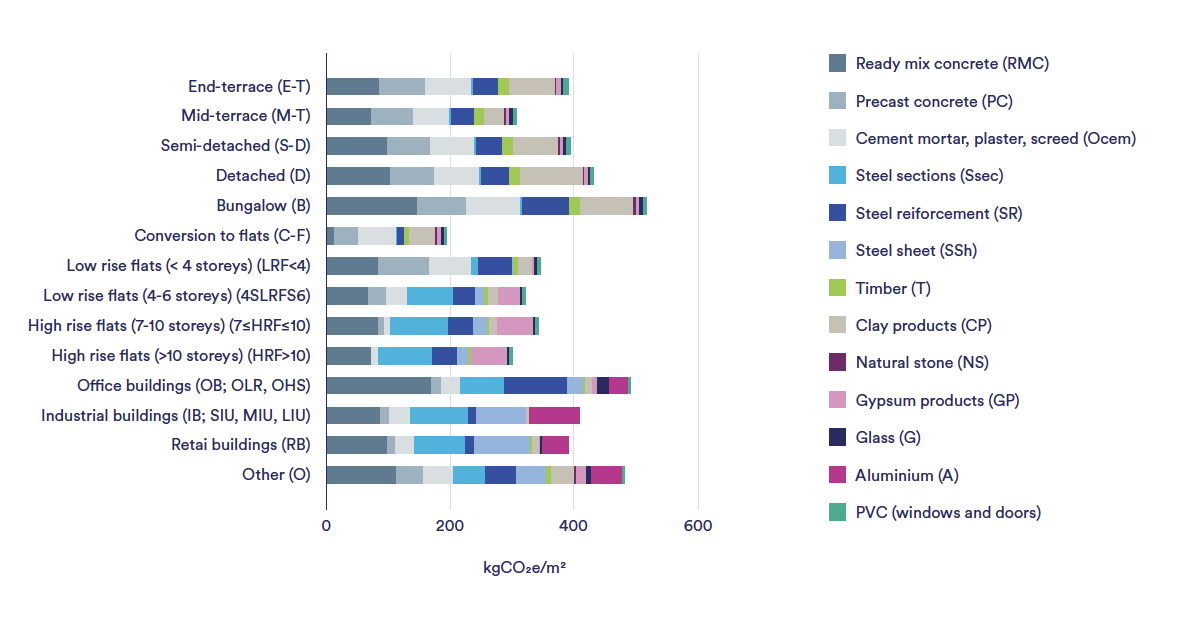

The construction sector presents a promising option for a demand-side mandate for decarbonised products, given it is a major consumer of both cement and steel, and is inherently insulated from competition outside the internal market. Cement and concrete account for around 30 to 70% of the embodied carbon in buildings, while steel contributes around 10 to 15% (Figure 5).35 Chemicals also feature prominently in the construction sector, as they are used in insulation (polyurethane and expanded polystyrene), paints and coatings, plastics (pipes & roofing membranes (PP), window frames and flooring (PVC)), and in adhesives and sealants. However, their contribution to embodied carbon is relatively small.

The embodied carbon in buildings represents up to 50% of the whole lifecycle emissions of buildings with energy efficient design.36 Consequently, ambitious limits on lifecycle emissions (e.g., via the EPBD) are likely to drive some increased procurement of decarbonised cement and steel. However, an additional mandate specifying a growing proportion of near-zero or low-emission cement and steel in the procurement of these products would provide an even stronger signal to developers of deep decarbonisation production processes. Following existing standards on lifecycle building emissions at the EU level and in some Member States, this could initially apply for projects over a minimum floor size or number of individual dwellings.

Figure 5. The contribution of different material inputs to the embodied carbon intensity of buildings35

Automobiles

In the automotive sector, steel production can contribute around 30% of the embodied emissions in a finished car, but less than 3% of its market value.37 Estimates of the cost impact of using decarbonised steel on the price of a car have ranged from 0.4 to 1%.38 The sector is also the second largest market for steel in the EU after construction (accounting for 19% of total production), and the largest user of flat steel products, which are mainly derived from carbon-intensive production routes using blast furnaces.39 Given the high impact nature of this sector and the relatively small number of automobile manufacturers selling in the EU, several of which have already taken voluntary steps to source decarbonised steel, it could also be an effective place for a mandate. Automobile manufacturers selling in the EU market are already regulated by CO2 emission performance standards, which require a progressive reduction in the average specific emissions of the cars they sell on an annual basis.40 A mandate to reduce embodied emissions could therefore be applied to the same group of manufacturers defined by this regulation, consisting of both overarching embodied emissions targets and a mandate to source a proportion of low-emission and/or near-zero emission steel in any steel used. The automotive industry also procures bulk polypropylene pellets, which are modified with colourants and additives and moulded into components such as bumpers. Bulk purchases of polypropylene are therefore an important node in the procurement process where specific criteria for embodied carbon emissions could be initially introduced.

Consumer Packaging

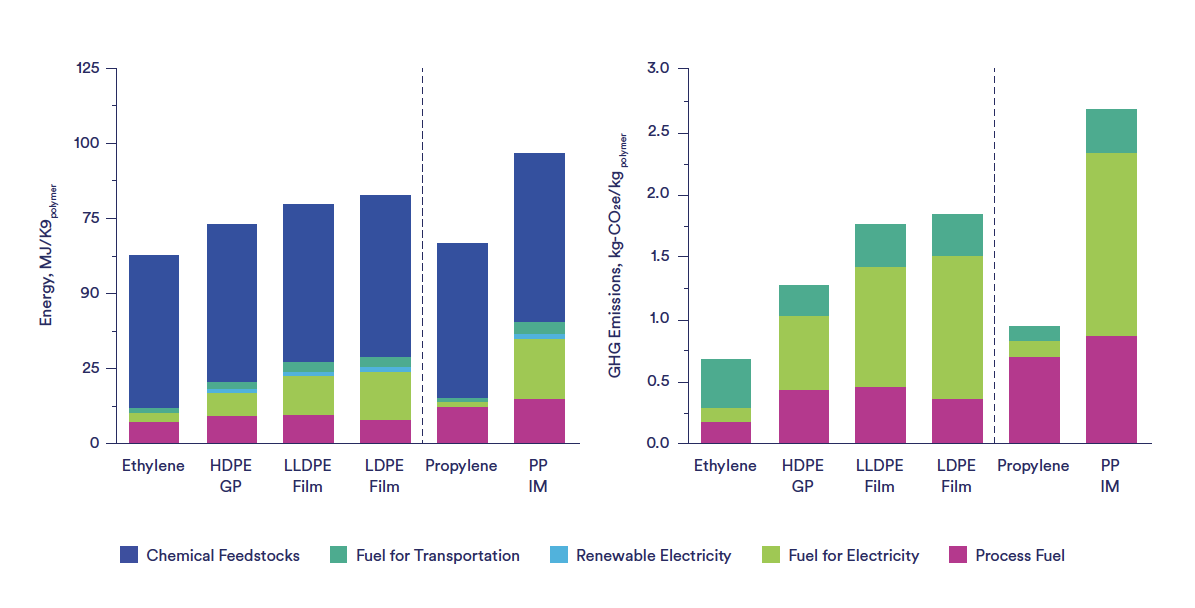

The production of high-value chemicals, such as ethylene, propylene, and aromatics (benzene, xylene, and toluene) is a highly emissions intensive-process which, in the EU, is closely associated with oil refineries that provide naphtha feedstock to steam crackers.41 These chemicals are the essential building blocks of solvents, fertilizers, synthetic rubbers, fibres, specialty chemicals and plastics such as polyethylene (PE), polypropylene (PP), and polyvinylchloride (PVC). While plastics are used for a vast range of applications, packaging is the dominant end-use market, accounting for around 40% of EU plastics production.42 Energy-intensive steam cracking of fossil feedstock to high-value chemicals and polymerisation are the dominant source of emissions in plastics production (see Figure 6), and a priority target for industrial decarbonisation policy and potential demand-side mandates in the plastics value chain. In the EU, approximately 40% of ethylene production is used to produce low-density polyethylene (LDPE) and linear low-density polyethylene (LLDPE), primarily used in plastic bags, bottles, film and containers. While substantial downstream processing is involved in the production of food-grade packaging, for instance, addressing the carbon intensity of packaging at the stage of unfinished LDPE and LLDPE can be instrumental, given the easier traceability.

Figure 6. Energy consumption and greenhouse gas emissions for polyethylene and polypropylene and their constituent monomers (ethylene and propylene respectively). (IM: injection moulded, GP: general purpose).43

However, production emissions may represent only a third of the end-of-life emissions due to plastic incineration.44 Although waste incineration emissions are covered by carbon pricing in some Member States, and should be fully incorporated into the ETS in the 2026 revision of the ETS Directive, this carbon price signal is not effectively transferred to producers of incinerated products. Policy levers aimed at decarbonising plastic production, therefore, face a complex challenge of appropriately distributing incentives along the value chain to those actors which are best placed to take emissions mitigation steps.

The EU’s Packaging and Packaging Waste Regulation already establishes a mandate on producers to increase recycled content in plastic packaging (to 65% by 2040 for most applications).45 This market could potentially also be leveraged as a driver of decarbonisation of remaining fossil fuel-based production pathways via steam cracking. For example, a declining cap on the carbon intensity of virgin plastic feedstock could be implemented. Raw materials costs represent a relatively large proportion of the final cost of many packaging products, and a smaller proportion of the total product cost, depending to a great extent on product type. Intermediaries in the material supply chain may experience significant price increases which could create a bottleneck for downstream chemicals to access the decarbonized feedstock. Given also the complexity in establishing harmonised labelling for lower-emission and near-zero emission plastic feedstocks, the potential for demand-side mandates in the consumer packaging sector requires further analysis. Building and construction is the second largest end-use market for plastics in the EU, and may be another promising sector for driving upstream decarbonisation.

Food retail

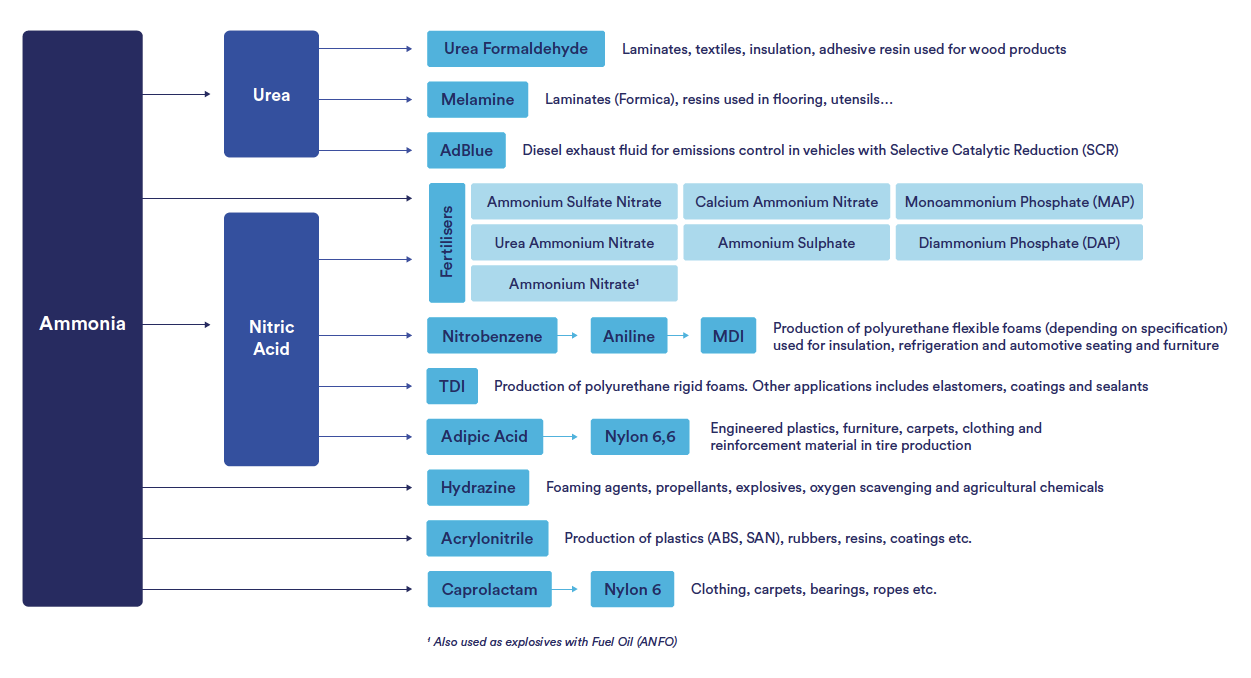

Production of ammonia and other nitrogenous fertilisers contribute over 17 Mt of annual CO2 emissions in the EU.46 The most emissions intensive step for producing nitrogenous fertilizers involves the production of hydrogen in the ammonia plant. As such, the sector aims to develop lower-carbon production processes based on electrolytic or CCS-enabled hydrogen.47

Figure 7. A summary of downstream applications for ammonia.48

Food products are the consumer-facing, end-use product to which much of these emissions can be attributed, and should be explored as a driver of upstream process decarbonisation. While the agricultural sector is unlikely to support mandates on fertiliser procurement, food retailers such as supermarkets may be a more suitable stage in the value chain to place mandates on embodied carbon for some high-impact products. A general requirement to reduce the carbon intensity of supply chains would allow retailers to choose from a range of decarbonisation routes — such as sourcing produce grown with low-carbon fertilisers, improving fertiliser use efficiency, or favouring suppliers who use renewable energy — depending on cost-effectiveness and practicality. The impact of fertiliser emissions on embodied emissions of food products is highly variable and context specific, given the potentially significant contributions from factors such as land use change, agricultural methane, transport and refrigeration.49 Depending on the product, food production emissions can also be smaller than the embodied emissions in food packaging (as for the example of an avocado shown in Figure 2). Conversely, a case study of bread produced in Italy shows fertiliser production contributing 28% of the total carbon footprint from farm to shop (including packaging and transport).50 Establishing a more direct link between food retail mandates and fertiliser decarbonisation could therefore require targeting specific products, or even a form of sub-mandate on procurement of produce with low-carbon fertiliser certification.

Conclusions

The IDAA has the potential to bring about a step change in efforts to decarbonise the EU’s hard-to-abate sectors. Strong carbon pricing through the ETS will remain a fundamental driver of this transition for emissions- and energy intensive industrial processes, including cement, steel, and chemicals, if adequately supported by investment in decarbonising infrastructure and funding for pioneering deep decarbonisation projects. However, creating stronger demand signals for decarbonised products will be essential for building and sustaining investment into new production processes. The IDAA can accelerate and increase the ambition of nascent, voluntary demand signals by establishing harmonised and rigorous product certification protocols and implementing new mandates for public and private procurement

Footnotes

- Sectoral emissions from CaptureMap by Endrava (accessed July 2025). Total emissions from EEA greenhouse gases – data viewer.

- IEA (2025) Demand and supply measures for the cement and steel transition

- CATF (2025) The role of CCS in decarbonising Europe’s cement sector

- CATF (2024) Refinery of the Future

- Industry decarbonization newsletter (2024) Why no one wanted to buy the green shipping fuel. Available at: https://industrydecarbonization.com/news/why-no-one-wanted-to-buy-the-green-shipping-fuel.html

- Innovation Fund – Performance.

- Lockwood T (2025) Designing carbon contract for difference incentives to drive the deployment of carbon capture and storage in Europe; Proceedings of the 17th Greenhouse Gas Control Technologies Conference.

- Rootzen et al. (2016) Paying the full price of steel; Energy Policy; Rootzen et al. (2017) Managing the costs of CO2 abatement in the cement industry; Climate Policy; Subraveti et al. (2023) Is CCS really so expensive?; Sustainable Systems; Roussanaly et al. (2025) Putting the costs and benefits of carbon capture and storage into perspective; Progress in Energy; IEA (2025) Demand for cement and steel; Mission Possible Partnership (2022) Making net-zero steel possible; Mission Possible Partnership (2023) Making net-zero concrete and cement possible; Invest.nl (2025) Mobilizing consumer demand for green hydrogen-based products; IEAGHG (2024) Clean steel: an environmental and technoeconomic outlook of a disruptive technology; Mission Possible Partnership (2021) Steeling demand: Mobilising buyers to bring net-zero steel to market before 2030

- CATF (2025) Building demand for low-carbon materials: how market demand can accelerate cement and steel decarbonisation in Europe

- Adapted from Roussanaly et al. (2025) Putting the costs and benefits of carbon capture and storage into perspective; Progress in Energy.

- First Movers Coalition

- Stegra: welcoming a new era of green steel production

- Heidelberg Materials. Customer references. Available at : https://www.cement.heidelbergmaterials.se/sv/evozero-cement-for-betong- utan-klimatavtryck (accessed Jul 2025)

- IDDI (2024) Driving consistency in the greenhouse gas accounting system.

- Regulation (EU) No 305/2011 of the European Parliament and of the Council of 9 March 2011 laying down harmonised conditions for the marketing of construction products

- Regulation (EU) 2024/1781 of the European Parliament and of the Council of 13 June 2024 establishing a framework for the setting of ecodesign requirements for sustainable products

- This could be analogous to the existing rating system for energy efficiency, implemented under the Ecodesign Directive

- IEA (2023) Achieving net zero heavy industry sectors in G7 members.

- VDZ (2025) CO2-Label für Zement

- GCCA (2024) Numerical definitions for low carbon and near zero emissions concrete.

- Adapted from: IDDI (2023) Driving consistency in the greenhouse gas accounting system

- Sapir et al. (2022) Green public procurement: a neglected tool in the European Green Deal toolbox?

- IDDI (2024) The scale and impact of green public procurement of steel and cement in Canada, Germany, the UK and the US

- European Commission 92008) Communication on Public procurement for a better environment.

- Sapir et al. (2022) Green public procurement: a neglected tool in the European Green Deal toolbox?

- OECD (2022) The Netherlands’ CO2 performance ladder

- Department of Enterprise, Tourism and Employment (2024) Government approves public procurement guidance to promote the reduction of

embodied carbon in construction - European Commission (2019) GPP in practice. A low carbon, circular economy approach to concrete procurement.

- Hochbahn U5 projekt GmbH (ND) U5: Klimaschonender U-Bahn-Bau

- Regulation (EU) No 305/2011. Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32011R0305

- Casey C (2025) BREEAM vs. LEED: Understanding key differences in green building certifications. CIM

- Directive EU/2024/1275. Available at: https://eurlex.europa.eu/eli/dir/2024/1275/oj?locale=fr

- https://orsted.com/en/media/news/2023/12/oersted-begins-construction-of-denmarks-first-carb-13757543 ; https://www.offshoretechnology.com/news/stockholm-exergi-carbon-capture-facility-sweden/ ; https://www.reuters.com/sustainability/norway-resumes

work-oslo-waste-carbon-capture-project-2025-01-27/ - Department for Transport (2024) The vehicle emissions trading schemes: how to comply; Department for transport (2025) Sustainable aviation fuel mandate: compliance guidance; DNV (2025) FuelEU Maritime Requirements, compliance strategies, and commercial impacts; IATA (2024) ReFuelEU Aviation Handbook; Regulation (EU) 2019/631 of the European Parliament and of the Council of 17 April 2019 setting CO2 emission performance standards for new passenger cars and for new light commercial vehicles.

- Drewniok et al. (2023) Mapping material use and embodied carbon in UK construction, Resources, conservation and recycling; 197; 107056.

- Lutzendorf T and Balouktsi M (2022) Embodied carbon emissions in buildings: explanations, interpretations, recommendations, Buildings and cities; 3(1); pp. 964-973

- Mission Possible Partnership (2021) Steeling demand: Mobilising buyers to bring net-zero steel to market before 2030; IEAGHG (2024) Clean steel: an environmental and technoeconomic outlook of a disruptive technology

- Ibid.

- Eurofer (2025) European steel in figures.

- Regulation (EU) 2019/631 of the European Parliament and of the Council of 17 April 2019 setting CO2 emission performance standards for new passenger cars and for new light commercial vehicles

- The EU has 40 operating mainstream steam crackers. Approximately two-thirds of the EU’s ethylene production uses naphtha, a light distillate and refining product normally used to produce gasoline, as feedstock and around a quarter use Liquified Petroleum Gas (LPG). Refineries not only provide the feedstock but also produce propylene and benzene, toluene and mixed xylene (BTX).

- Plastics Europe (2022) Plastics – the facts 2022

- Nicholson et al. (2021) Manufacturing energy and greenhouse gas emissions associated with plastics consumption, Joule; 3; pp 673-686. Supplementary Information.

- Material Economics (2019) Industrial transformation 2050.

- Regulation (EU) 2025/40 of the European Parliament and of the Council of 19 December 2024 on packaging and packaging waste

- CaptureMap by Endrava. Accessed July 2025.

- This section only addresses emissions from nitrogenous fertilizers. A more comprehensive analysis would require an assessment of the lifecycle emissions of phosphorus, potassium and sulfur-based fertilizers.

- CATF analysis

- Poore J and Nemecek T (2018) Reducing food’s environmental impacts through producers and consumers, Science; 360; pp. 987-992v

- Chiriaco et al (2017) The contribution to climate change of the organic versus conventional wheat farming: A case study on the carbon footprint of wholemeal bread production in Italy, Journal of Cleaner Production, 153, pp. 309-319