EU CO2 storage by 2030: Why the NZIA target is more feasible than industry claims

This blog is published under Article 23 Watch, a joint initiative of Carbon Balance Initiative, Clean Air Task Force, and Bellona Europa that tracks transparency and accountability in the implementation of Article 23 of Net Zero Industry Act. Visit the Article 23 Watch site to explore further resources.

Making meaningful cuts to greenhouse gas emissions calls for bold and ambitious targets. The European Union’s aim of building 50 million tonnes of annual CO2 storage capacity by 2030 is no exception.

The Net-Zero Industry Act (NZIA) places the obligation to deliver this target on EU oil and gas producers. But many have pushed back: last year, 12 companies took legal action against the regulation and its implementing acts. Most of these challenges argue that it is simply not feasible to deliver storage projects on this timeline.1 Given the regulation was effectively finalised in February 2024 and assesses compliance at the end of 2030, companies have over six and a half years to deliver. Based on our analysis of existing project timelines, this should be ample time for projects to meet the European Commission’s definition of compliant capacity and contribute to the target.

The storage project timeline and NZIA compliance

Fortunately, the EU is not starting from scratch. Based on the capacities announced by project developers in the region, the current pipeline of proposed projects could yield up to 43 million tonnes per year (Mtpa) of operational capacity by 2030.2 Nearly all of this capacity was already planned at the time the NZIA was implemented – likely informing the size and timing of the target. Given the significance of 2030 in EU climate policy, project developers have typically been keen to target this milestone, but they have often also assumed a favourable policy environment as a prerequisite.

Developing a geological storage site does take several years and can vary significantly between projects. In the EU, acquisition of an exploration licence is usually the first step, although in some Member States this is not required if the storage site is a depleted oil or gas reservoir. The developer then undertakes characterisation work to determine if the site is suitable; the time needed for this step can depend heavily on the availability of existing data for the area. If the results are positive, an application for a storage permit is submitted and processed by a national regulator. Successful receipt of this permit is often aligned with a ‘final investment decision’ (FID) for the full-scale project and the start of construction.

Importantly, the European Commission has formally clarified that storage projects need not be operational by 2030 to be ‘available to the market’ and compliant with the NZIA target, but they must possess a storage permit and have reached an agreement with a prospective user.3 By removing the construction phase, this definition significantly shortens the time required to deliver compliant capacity and increases the proportion of the current project pipeline which could contribute to the target. Six storage projects targeting operation in 2030 have plans to expand capacity in the early 2030s, and four new projects are expected to come online in this period – much of this additional capacity should be permitted by 2030.

Have storage projects been delayed?

Some studies have suggested that carbon capture and storage (CCS) projects are particularly prone to delays. Analysis by Wood McKenzie for some of the obligated producers assessed 11 storage projects in the EU, UK and Norway and identified an average delay of one and a half years against the originally expected development times: this finding is used to support an assertion that CCS projects are subject to ‘persistent multi-factor delays’.4

While delays for large infrastructure projects of this kind are certainly not unusual, such analysis is potentially misleading due to the uneven and evolving policy landscape for CCS over the past decade. Projects showing the largest ‘delays’ are typically those which were announced very early on in the current wave of policy interest in CCS deployment – in around 2018 to 2021 – when there was essentially no business case for investment.

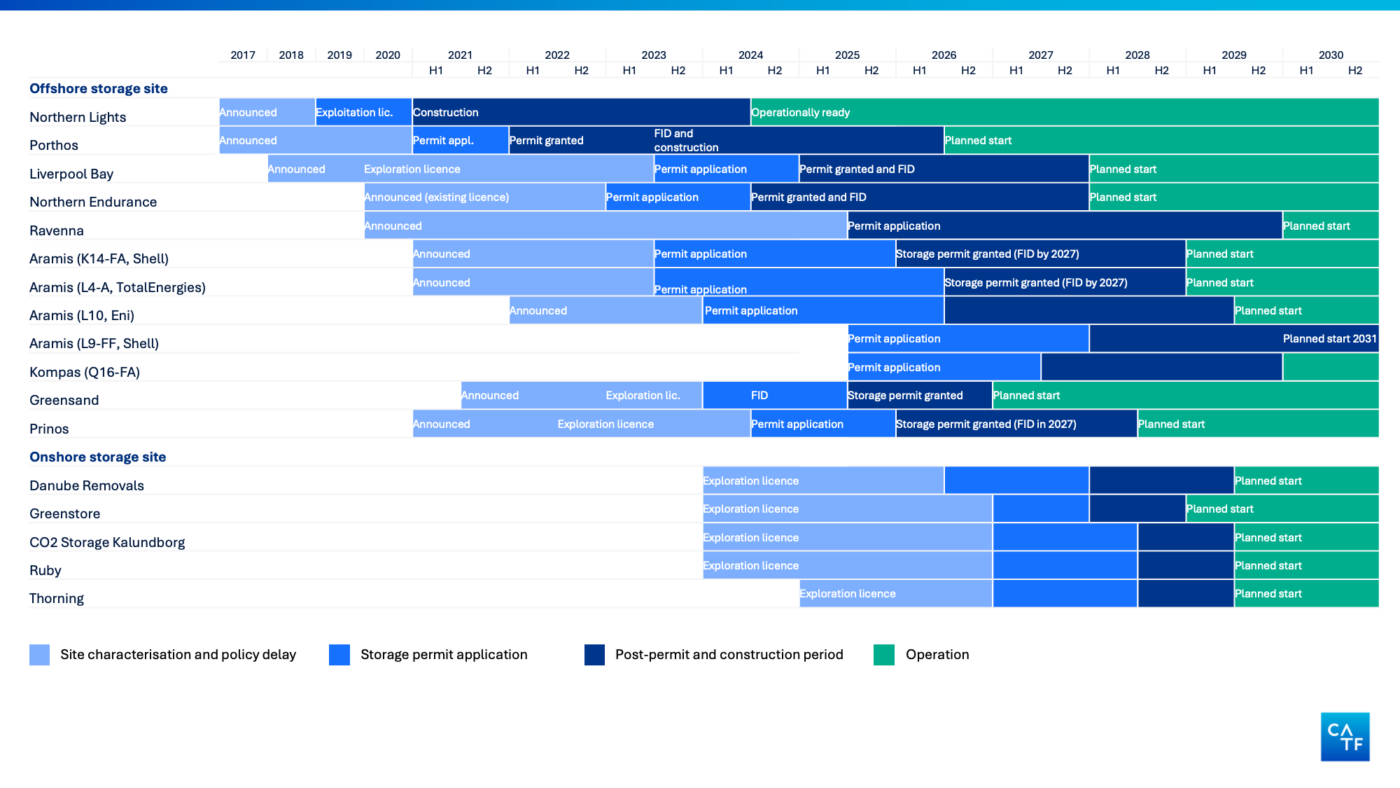

These projects, such as Norway’s Northern Lights and the Netherlands’ Porthos project, are often announced as a starting point for a wider policy conversation around support for CCS. For both these projects, significant government funding ultimately arrived: Norway’s Longship programme brought about an FID for Northern Lights in March 2020, three years after it was first announced. The project began construction in 2021 and was declared operationally ready in September 2024 – four and a half years from the FID, and within the schedule planned at the project’s inception.5

Past and planned timelines for CO2 storage sites in Europe6

Also announced in 2017, the Porthos project was similarly speculative until support arrived in the form of the Dutch SDE++ subsidy scheme in 2021. However, the project suffered further delay from a lengthy legal challenge brought by an environmental group on the impact of nitrogen emissions – a much wider issue than CCS which concerned all construction projects and other nitrogen-emitting activities in the country. Once resolved, Porthos took its FID in 2023 and now plans to operate in 2027. In its favour, the project partly makes use of an existing storage permit developed for an older initiative.7

Several storage projects in the UK have followed a similar path, with some also building on roots developed under a previous wave of impetus for CCS in the early 2010s. The Acorn and HyNet projects were first announced in 2018, while Northern Endurance (a revival of a site assessed for the earlier ‘White Rose’ project) came in 2020. Despite strong government commitments to CCS since around 2018, all of these projects had to wait for the UK’s relatively complex CCS subsidy schemes to be finalised and the conclusion of a lengthy competitive award process. With subsidies confirmed to HyNet and Northern Endurance in 2024, both projects took FID shortly after and are now on track to begin operating in 2028.

Of course, these projects were not idle during these political lag periods, but used the time to develop engineering design, engage with potential users and – in some cases – carry out site characterisation and permitting. But these necessary project development steps do not appear to have been rate limiting. Northern Lights applied for a storage permit in 2020 and obtained it in 2022; Porthos applied in 2021 and had the permit granted in 2022; HyNet and Northern Endurance also appear to have spent around one to two years on this crucial step. All four projects have progressed from first characterisation work to permit in five years or less.

The Ravenna project in Italy has been injecting a small quantity of CO2 since 2024, at levels below those needed for a full storage permit, but has long planned to scale up to 4 Mtpa. Originally announced in 2020, it is another project that was conceived well before supportive national and EU policy caught up. The project only appears to have begun progressing in earnest once political momentum gathered for CCS deployment in Italy. An application for a full storage permit was only made in 2025, presumably helped by positive results from the small-scale injection trial. Ravenna now intends to take FID in 2026, with a target start date of 2029.

Recent projects highlight faster timelines are possible

Many recent projects in the EU tell a similar story: a principal cause of project delay is developers waiting on funding policy and an adequately funded user base to materialise, rather than technical or permitting delays.

The first EU projects to receive storage permits – Prinos in Greece and Greensand in Denmark – show what is achievable when policy is better aligned with project timelines. Prinos was first announced in late 2021, received an exploration licence in the following year, applied for a storage permit in 2024 and received it in February 2026. The project is targeting an FID this year for a 2028 start date, representing a definite slip on the originally announced – and perhaps overly ambitious – target of 2025. This pace has been helped by EU funding to the project, as well as to the Greek industrial sites which represent its user base; however, even here, the FID is likely dependent on enough users securing a business case, which may require a new funding mechanism from the Greek state.8

Greensand has followed a very similar path, receiving its exploration licence in February 2023 and a storage permit in December 2025. The project took FID shortly before the permit was granted, in 2024, and it expects to start injecting CO2 in 2027 – albeit at a relatively small scale (0.4 Mtpa). This is only one year after the originally targeted start of operations. Greensand has been able to forge ahead thanks to the captured CO2 it has secured from biogas plants supported by the Danish government.

Delays at the Netherlands’ flagship CCS project ‘Aramis’ may in part be attributable to long permitting timelines, but the wait for an adequate business case is again a dominant factor. This large offshore transport system linking several storage sites was first announced in September 2021, targeting a 2026 start date. The storage developers have experienced relatively long waits to receive their permits, with Shell applying in June 2023 and receiving the permit nearly three years later in May 2026.9 However, regardless of the permit status, the project has long struggled to meet its goal of securing at least 7.5 Mtpa of CO2 from committed users, which is largely dependent on CO2-emitting facilities receiving government subsidies under the SDE++ programme. The large scale of the proposed infrastructure (22 Mtpa of CO2) means first users are burdened with high costs, and earlier subsidy recipients now face inflated tariffs which they can no longer cover. In 2024, the government stepped in with additional funding in an effort to resolve this vicious circle, aiming to bring Aramis to FID in 2027.10

Much of the remainder of the EU’s storage project pipeline consists of onshore initiatives – primarily in Denmark, but also across Central and Eastern Europe. Onshore projects could present both challenges and advantages for development timelines: on the one hand, carrying out site characterisation and engineering work onshore is technically easier; on the other hand, environmental permitting can be more complex and there is a greater chance of public opposition. In Hungary, the Danube Removals project was announced in 2024 and expects to apply for a storage permit in 2026, with a projected start date in 2029. Three Danish exploration licences were awarded in June 2024, and each of these projects plans similar timelines, with a period of site characterisation followed by permit applications in 2027 (should the site prove favourable) and construction from 2028.

What is a typical project timeline?

Storage projects in Europe have tended to announce target timelines of around 4 to 5 years from inception to permitting, typically covering around 3 years for characterisation work, and around 1.5 to 2 years for permitting. All storage permits awarded in Europe to date have taken place within this five-year period from first appraisal work, with Greensand and Prinos achieving much shorter lead times.11 While some Dutch projects have experienced long waits on permits, it is worth noting that the NZIA requires storage permits for ‘Net-Zero Strategic Projects’ to be processed within 18 months, suggesting that steps will be taken to ensure this part of the timeline is minimised.12

Evidence for real construction phase timelines is more limited, and clearly highly project dependent, with offshore projects requiring up to three years. Northern Lights is a complex, offshore project encompassing new offshore infrastructure and a shipping terminal and took around three years to build. Porthos re-uses some offshore infrastructure, but also includes a challenging 30-km onshore pipeline through a built-up area. The project is currently aiming to complete construction by the second half of 2027 – three and a half years after construction began. Greensand’s construction phase targets an ambitious timeline of less than two years (December 2024 to mid-2026). Wholly onshore projects have good reason to project slightly shorter construction timelines, although there is a risk that rapid expansion in the sector could lead to scarcity in the specialised expertise and equipment needed to carry out this work.

The NZIA should accelerate current timelines – not reflect them

It is clear that political uncertainty, funding policy design, and funding award timelines are the major causes of delay for European storage projects – particularly for projects conceived prior to a strong EU or national-level commitment to CCS in climate plans. This uncertainty has led to years of stalling for first-mover projects, and revenue uncertainty appears to still be a key factor for slow progress for projects like Aramis, Prinos and Ravenna. The NZIA storage obligation was conceived to help unlock this impasse, requiring storage developers to progress projects in advance of secure demand from heavily subsidised capture projects.

The obligation has already spurred some obligated entities to commit to new projects with rapid timelines. Launched in 2026, the Kompas project developed by ONE Dyas and the Abeona project from Petrogas13 are using depleted oil and gas reservoirs in the Dutch North Sea and target operation in 2030. While these projects may be able to move faster than others, our analysis of real and planned project timelines indicates that reaching the key milestone of a storage permit and NZIA compliance is eminently achievable by 2030 – even for projects that begin work this year.

It would be a mistake to assess the practical feasibility of the NZIA target based on a superficial assessment of existing project timelines, which are so heavily influenced by the very market failures which the obligation sets out to address. The NZIA obligation is a new kind of policy driver for CCS projects in the EU, but it should be seen as no less an incentive to act than the subsidies on which projects have previously relied.

1 Of the litigating entities, only OMV Petrom does not make this argument. See: https://article23watch.eu/2026/05/26/article-23-on-trial-how-oil-and-gas-producers-are-challenging-the-eus-flagship-ccs-market-building-measure/ for more details.

2 https://www.catf.us/article-23-watch-initiative/article-23-watch-tracker/

3 This was formally indicated in EC (2026) NZIA Monitoring report, but was also communicated to obligated entities at a closed-door workshop in October 2025.

4 Available at: https://www.woodmac.com/news/opinion/policy-vs-practicality-assessing-the-feasibility-of-meeting-nzia-article-23/ and https://www.woodmac.com/news/opinion/nzia-feasibility-report-is-the-nzia-achievable-from-a-full-value-chain-perspective/.

5 Unusually, Northern Lights applied for a full storage permit in late 2022, after beginning construction, and received the permit in 2025. However, the project had already received an exploitation licence which, in the Norwegian regulatory framework, grants the developer the rights to develop the reservoir. The site became operational in August 2025, when captured CO2 was first delivered.

6 Analysis by CATF for Article 23 Watch.

7 The ROAD project, which aimed to implement CCS on a coal-fired power plant in Rotterdam.

8 Several CO2 capture projects in Greece have secured Innovation Fund grants, however, such projects typically need to secure further revenue or support to take FID.

9 In the Netherlands, an exploration licence is not required for storage in depleted hydrocarbon reservoirs. The Netherlands has granted two exploration licences for CO2 storage in saline reservoirs.

10 For UK projects, the challenge of funding infrastructure sized beyond the initially funded users was addressed via a separate subsidy mechanism to transport and storage developers.

11 There is some ambiguity over the timing of first characterisation work on most storage sites – this analysis assumes work started with the granting of an exploration licence, where applicable.

12 Most storage projects are expected to be granted this status, given their significance in achieving the EU storage target.

13 Kompas had already applied for a storage permit in 2025.