U.S. clean energy investments: 2025 Quarter 4 analysis

Federal policy and executive actions have a direct impact on private investments in communities across the U.S. – either hindering investments or catalyzing them. CATF tracks private investments in clean energy projects that are eligible for federal incentives as well as the status of federal policies that may impact them. Each quarter, CATF highlights changes to federal policies and new executive actions and analyzes how these changes have affected investments across U.S. states and districts.

What’s impacting investments in Q4?

Uncertainty remained a key driver of investment activity in Q4. The quarter started with what would become the longest federal government shutdown in history, which slowed timelines for projects requiring federal approval. Investors also faced uncertainty while awaiting Treasury guidance that would determine energy tax credit eligibility for current or prospective projects relying on tax credits narrowed by the One Big Beautiful Bill Act (OBBBA). Many federal agency actions also exacerbated this uncertainty, including changes or pauses to permits and announced federal funding cuts for clean energy projects.

Key takeaways from Q4 2025:

- Investment in renewables, including solar and wind, remain steady, signaling federal policy shifts have not been solely determinative for the industry although it is continuing to narrow investments.

- Growing emphasis on battery storage co-located with data centers indicates the storage industry is repositioning to market opportunities, as it shifts to align more closely to current federal policy priorities.

- Recent policies supporting technologies like nuclear fission are likely to translate into increased private investments in future quarters, but will require effective tax credit guidance from Treasury, including workable prohibited foreign entity (PFE)/foreign entity of concern (FEOC) restrictions, to access incentives to fully deploy. Future investments in technologies like hydrogen, SAF, and carbon management will depend on how Treasury administers key tax credits, including how data is reported and verified to qualify for tax credits – which to date has been addressed by the GHGRP. These industries continue to face uncertainty in the current political environment.

Federal Policy

43-day government shutdown. The federal government entered a 43-day shutdown – the longest in history – at the start of Q4 2025. During the shutdown, agencies including DOE, IRS, EPA, and BLM ceased many federal activities, which slowed timelines for projects that require federal action. EPA ceased issuing permits, and Treasury slowed its issuance of guidance including PFE/FEOC guidance, which industry had previously expected in December. Activities related to oil and gas, coal, and mineral leases generally continued. Amid the shutdown, investors faced additional uncertainty when evaluating investments that require federal approvals.

Prohibited Foreign Entities (PFE)/Foreign Entity of Concern (FEOC) guidance. OBBBA narrowed energy tax credit eligibility, which continues to impact projects relying on certain IRA credits for bankability. PFE/FEOC restrictions, which OBBBA applied to six energy tax credits (Section 45U, Section 45Y, Section 48E, Section 45X, Section 45Q, and Section 45Z), increase compliance burdens and impacted projects claiming those credits, including enhanced geothermal and advanced nuclear projects. These restrictions impacted investments as uncertainty about Treasury and IRS guidance weighed on prospective investors and companies. Industry awaits full implementation guidance from Treasury; initial guidance, which was positively received by the industry, was released after the period covered by this Q4 analysis (February 12, 2026).

Executive Actions

August 2025 Department of the Interior (DOI) Memorandum. DOI announced a full review of offshore wind energy regulations to ensure alignment with the Outer Continental Shelf Lands Act and America’s energy priorities under President Trump. DOI’s refusal to approve solar and wind permits on federally managed lands as a result of DOI’s August 2025 memorandum continued to have downstream effects of slowed and/or stalled permitting processes for renewables like solar and wind.

Changes to NEPA implementing regulations and procedures. While difficult to quantify at this time, new changes to agency NEPA processes may impact project investments. The removal of NEPA regulations managed by the Council on Environmental Quality and shift from agency-specific NEPA regulations to agency NEPA procedures could increase compliance costs for projects that must navigate new processes, particularly for those projects that involve multiple agencies, each with its own respective process. In addition, changes to agency NEPA processes that prompt litigation expose projects to additional uncertainty and may deter investment. Because the changes to NEPA processes were made through executive action rather than legislation, they are less durable and may be reversed by future administrations, creating uncertainty for projects already under review.

Proposed EPA Rule: Reconsideration of the Greenhouse Gas Reporting Program (GHGRP). Uncertainty over EPA’s proposed rollback of GHGRP continued to impact Q4 2025 investments. Treasury and IRS rely on the GHGRP to administer Section 45Q Carbon Sequestration Tax Credit, Section 45V Clean Hydrogen Tax Credit, and Section 45Y Clean Electricity Tax Credit. EPA’s proposal could hinder compliance with tax credit reporting requirements reliant on GHGRP data, and therefore the ability to claim the credits, unless IRS regulations are revised, and/or sufficient alternatives for measurement, reporting, and verification and lifecycle analysis are implemented. The proposed rollback may also hinder investments intended for exports, putting U.S. companies at a competitive disadvantage in rapidly evolving global markets and frameworks that require verified emissions data. Treasury did provide a safe harbor for taxpayers claiming 45Q on December 19, 2025, for calendar year 2025 (discussed below).

DOE announced project funding cuts and an unconfirmed list of additional cuts considered for existing awards. In early October, DOE announced the termination of 321 awards for energy projects worth approximately $7.56 billion in obligations. A leaked list including an additional ~300 projects was reported later in October but remains unconfirmed by DOE, suggesting there are hundreds of projects in limbo. The announced and reported cuts include projects spanning energy, industry, and manufacturing sectors, such as hydrogen, carbon capture, near-term infrastructure, and vehicles and transportation. Each project represents local jobs and economic development, partnerships, supply chain investments, and up to 50% non-federal cost share from project partners.

DOE Organizational Realignment. The reorganization announced in November suggests a shift in DOE focus areas for research, development, and demonstration (RD&D). Nuclear fission, fusion, next-generation geothermal, artificial intelligence (AI), fossil fuels, and critical minerals are clear priorities for DOE while renewables (specifically solar and wind) have been deprioritized. The DOE reorganization introduces additional uncertainty for how federal programs will be resourced, as the congressional appropriations process has not yet adopted the DOE reorganization in its budgeting and therefore the funding for some of these organizational shifts remains unclear. The realignment is significant for private sector investments, as DOE’s priorities influence and signal which technologies are financeable, and changes which technologies receive RD&D grant, demonstration, and loan support.

Preview for 2026

The following executive actions taken at the end of Q4 in December may provide investment insights into Q1 2026.

- 45Q Safe Harbor Guidance. On December 19, 2025, the Treasury Department released safe harbor guidance for 45Q (Notice 2026-1) in light of EPA’s proposed GHGRP rollback. The notice provides guidance and a safe harbor for determining the section 45Q tax credit eligibility and credit amount for carbon dioxide capture and geological storage that occurred during calendar year 2025. Although this represents a step forward for taxpayers who claim the credit, it does not address the longer-term uncertainty for the industry driven by the GHGRP rollback, which would upset an effective and longstanding program without an adequate replacement in place. The notice also indicates that Treasury intends to issue forthcoming revisions to existing 45Q regulations, which may or may not impose additional administrative burdens relative to the firmly-established GHGRP methodology.

- Offshore wind lease order. On December 22, 2025, DOI issued a stop work order for five offshore wind projects that had received all approvals and begun construction. One project, Vineyard Wind 1, was already sending power to the grid. The stop work orders were overturned in litigation, although Sec. Burgum has publicly stated that the administration intends to appeal.

Findings

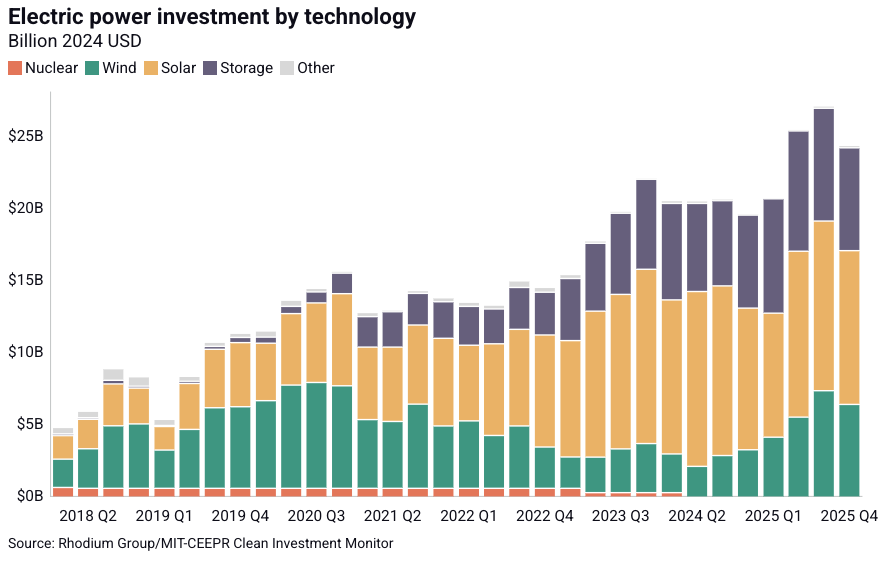

Electric Power

In Q4 2025, Rhodium Group’s data analysis shows $24 billion in actual investments (vs. announced) in clean electricity, with $18 billion in utility-scale solar and storage making up the majority of energy investments. Q4 announced energy investments totaled ~$22 billion across solar ($11.5B), storage ($8.4B), and wind ($2.1B).

Figure 1. Actual electric power investment by technology

Solar

Actual Q4 investments totaled ~$10.6 billion and announced investments totaled ~$11.5 billion.

Despite a $1 billion decrease in solar investment in Q4 compared to Q3, the overall trend remains elevated compared to year-earlier levels, showing near-term deployment remains strong. Developers continued solar investments this quarter ahead of OBBBA’s requirements for projects to begin construction by July 4, 2026, or be placed into service by December 31, 2027, to be eligible for full credit values, underscoring how federal incentives shape the timing of private sector investments. The American Clean Power Association estimates 10,116 MW of solar power capacity was added to the grid in Q4 2025, and utility-scale solar accounted for 50% of all new generation capacity added to the grid in 2025 overall – demonstrating solar’s continuing role in the U.S. energy mix.

The majority of Q4 electricity investments were comprised of utility-scale solar and storage, with a shift toward solar co-located with battery storage, as storage tax incentives do not phaseout until the beginning of 2034. For example, Xcel Energy submitted a petition to the Minnesota Public Utilities Commission requesting approval for a portfolio of 768 MW of solar generation capacity and 855.5 MW / 3,422 MWh battery energy storage system (BESS) capacity at the Sherco Energy Hub, the Upper Midwest’s largest solar generating facility. If approved, Xcel plans to start construction on the battery storage projects in 2026 and serve customers by late 2027. The company expects federal tax credits to offset 30% of the cost for the Blue Lake battery and 40% for the Sherco battery projects and Sherco Solar. The project site is near the ~2,300-MW Sherco coal plant set to fully retire in 2030, with the Sherco Energy Hub expected to compensate for a portion of that power generation loss.

Q4 investment cancellations totaled $2.1 billion.

While actual investments in solar remained strong, investment cancellations nearly quadrupled in Q4 compared to Q3. Lack of federal support and incentives likely contributed to the canceled investment, including permitting bottlenecks at DOI.

For example,the federal government revoked previously secured federal permitting approvals and canceled NEPA analyses for some solar projects. The BLM canceled the NEPA process for the Esmeralda Seven Solar Project, a 6.2 GW solar and battery storage project with multiple subprojects planned on public lands in Nevada. Instead of continuing the programmatic environmental analysis (a method of streamlining the NEPA process) BLM started in November 2023 to expedite future reviews of the subprojects at the site, reporting suggests each of the subproject developers will have to submit individual NEPA analyses.

DOE’s announced cuts include many instances of RD&D that would have continued to drive down the cost of solar energy and support domestic manufacturing – totaling ~$330 million across ~85 projects. Historically, DOE’s solar RD&D efforts accelerated the industry’s progress by an estimated 12 years and helped drive down the average cost per watt. Continued lack of sustained federal support for solar RD&D is likely to have negative long-term impacts on further technology cost reductions.

Storage

Actual Q4 investments totaled ~$7.1 billion and announced investments totaled ~$8.4 billion.

Actual storage investment was ~$7.1 billion in Q4, a slight decrease compared to Q3, which saw $7.8 billion in actual investments. The American Clean Power Association estimates storage developers added 4,970 MW of power capacity to the grid in Q4 2025. Data center developers continue searching for energy solutions, and Q4 investments indicate battery storage is being explored as one of those options. In October, Aligned Data Centers and Calibrant Energy announced an agreement in which Calibrant will deliver 31 MW / 62 MWh battery energy storage system (BESS) at Aligned’s data center campus in the Pacific Northwest. Star Charge Americas and Beneficial Holdings also announced $3.2 billion plans in October to deploy a series of projects across the U.S. and Puerto Rico to accelerate grid connections and allow data centers to begin operating sooner. Announced agreements and project plans like these may offer a roadmap for others to follow if proven successful, but the impacts of these energy decisions by data centers are not yet known – the administration issued new policy in Q1 2026 that may influence these decisions in future quarters, such as the Ratepayer Protection Pledge.

Q4 investment cancellations totaled $1.6 billion.

While actual storage investments remained steady, investment cancellations jumped from ~$723 million in Q3 to $1.6 billion in Q4. Rhodium Group identified six storage project cancellations across Texas, California, and Virginia, with Texas representing the largest share of Q4 cancellations. These cancellations may be attributable to market saturation and high grid costs in those states, and if so, it may suggest a regional shift in where battery projects are deployed.

Wind

Actual Q4 investments totaled ~$6.3 billion and announced investments totaled ~$2.1 billion.

Actual Q4 wind investments (~$6.3 billion) were down by ~$1 billion compared to Q3 (~$7.2 billion), but overall investment levels remained strong over the year. OBBBA’s tax credit phaseouts requiring projects to begin construction by July 4, 2026, or be placed into service by December 31, 2027, to be eligible for full credit values continued accelerating construction and commissioning in Q4, again underscoring how federal incentives shape the timing of private sector investments. Despite federal stop work orders, permitting uncertainty, regulatory uncertainty, and other executive actions impacting the wind sector, the American Clean Power Association estimates wind project developers added 3,562 MW of power capacity to the grid in Q4 2025.

Q4 investment cancellations totaled $1 billion.

Q4 wind investment cancellations totaled ~$1 billion, following Q3 that showed no investment cancellations. Invenergy Services LLC, self-referred as North America’s largest privately held independent power producer, canceled projects in New York and Wyoming, and the Leading Light Wind project off the coast of New Jersey, citing the offshore wind industry’s difficult economic and regulatory conditions. These types of cancellations are likely to continue for both offshore and onshore wind in the near-term, given the lack of federal support for the industry.

For example, DOE funding for wind technology innovation was hard-hit by the October cancellations. In late December, 2025, DOI ordered an immediate halt to the construction of five major offshore wind projects spanning New England, the Mid-Atlantic, and New York—Vineyard Wind 1, Revolution Wind, Coastal Virginia Offshore Wind, Sunrise Wind, and Empire Wind – risking $28 billion of private investment. In addition, tariff uncertainty is slowing turbine procurement, and Wood Mackenzie projects tariffs will increase the costs of turbines in 2026.

Nuclear Energy

In October, the federal government announced an $80 billion partnership between the U.S. Department of Commerce, Westinghouse Electric Company, and its owners Brookfield Asset Management and Cameco Corporation to deploy a fleet of eight Westinghouse AP1000 light-water reactors across the U.S., or a mix of large and small modular units. Activity in Q4 suggests nuclear investments will begin to have a stronger showing in future quarters announced and actual investment numbers, assuming a supportive political environment, effective implementation of investment and production tax credits and workable guidance on PFE/FEOC restrictions, and adequate regulatory and licensing frameworks are in place that allow for actual deployment.

- In Q4, DOE made several awards for projects to be matched with private funds in future quarters. DOE announced the second round of conditional commitment selections under the Fuel Line Pilot Program, with projects intended to ensure a robust supply of fuel is available for RD&D purposes, including the 11 reactors initially selected for DOE’s Reactor Pilot Program. Private investment totals depend on each project, with pilot program applicants responsible for all costs associated with designing, manufacturing, constructing, operating, and decommissioning the test reactors and fuel lines on DOE sites. DOE’s Office of Energy Dominance Financing (EDF) also closed a $1 billion loan to Constellation Energy Generation, LLC to help leverage additional private investments to finance the Crane Clean Energy Center, an 835 MW nuclear plant in Londonderry Township, Pennsylvania.

In December, DOE selected the Tennessee Valley Authority (TVA) and Holtec Government Services under the Generation III+ Small Modular Reactor Program to develop and construct the first Gen III+ small modular reactor plants in Tennessee and Michigan. Site construction for the TerraPower Natrium Reactor project in Wyoming continued in Q4. In October, the Nuclear Regulatory Commission (NRC) completed the EIS for TerraPower’s construction permit and in December, the NRC completed its final safety evaluation for the Natrium reactor. This project is receiving 50% federal cost share from the DOE under the Advanced Reactor Demonstrations Program, matched with 50% private funding.

U.S. nuclear investment still requires federal support and de-risking, and the combination of multi-reactor commitments, like the Westinghouse partnership, with programmatic and first-of-a-kind (FOAK) project level funding announcements from DOE in Q4 continued to signal both political and financial backing for large-scale nuclear buildouts. In addition, DOE’s EDF restructuring and available loan authority makes it well positioned to help finance nuclear builds.

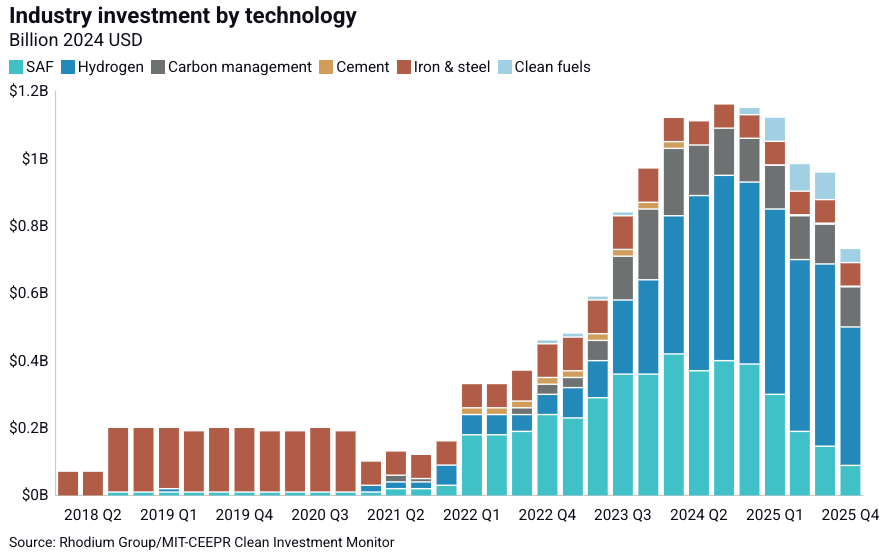

Industry

In Q4 2025, Rhodium Group data analysis shows ~$730 million in actual (vs. announced) investments went toward industrial sector projects in Q4. Hydrogen saw the most actual investment (~$410.9M), followed by carbon management ($119 million), sustainable aviation fuel (SAF) (89.1 million), iron & steel ($71.1 million), and clean fuels ($39 million). Q4 announced industry investments totaled ~$445.9 million, all in hydrogen.

Figure 2. Industrial decarbonization investment

Hydrogen

Actual Q4 investments totaled ~$410.9 million and announced investments totaled ~445.9 million.

Hydrogen investments in Q4 decreased by ~$130 million compared to Q3. These investments include hydrogen produced via water electrolysis and via fossil-based pathways with CCUS and range across a variety of end uses including chemicals production, fuels production, and petroleum refining. Amid ongoing industry uncertainty around OBBBA’s legislative changes to the 45V tax credit, DOE hydrogen hub funding, and long-term demand, Q4 saw continued actual and announced investments for hydrogen projects. In October 2025, the DOE’s EDF closed a $1.5 billion loan to Wabash Valley Resources, LLC, to help finance a coal and ammonia fertilizer facility in Indiana that is planning to integrate CCS into the project. Since then, Baker Hughes announced multiple orders to advance the project and Honeywell was selected as a carbon capture technology provider.

Under the IRA, the 45V tax credit was available for projects that “begin construction” by the end of 2032, which provided a long-term market signal for investments. Under OBBBA’s revisions to 45V, however, facilities need to begin construction before the end of 2027 to be eligible to receive the credit. It is unclear whether there is enough policy, regulatory, or financial certainty to sustain or spur increased investments in future quarters before the 2027 phaseout of the tax credit. Alternatively, projects employing CCUS may choose to claim 45Q rather than 45V, which may be more lucrative for high volumes of captured CO2.

Q4 investment cancellations totaled $1.4 billion.

Hydrogen investment cancellations jumped from ~$564 million in Q3 to ~$1.4 billion in Q4 amid ongoing industry uncertainty, reduced federal incentives and support, and poor demand signals.

Cancellations included two Plug Power projects in Texas and New York, following the company’s announcement that they were suspending work related to the $1.7 billion DOE loan guarantee they received in 2024 to construct six hydrogen production facilities across several states. Future quarters may show private investment cancellations in response to DOE’s October funding cuts, which included $1.2 billion in federal cost-share for California’s ARCHES hydrogen hub and $1 billion for the Pacific Northwest Hydrogen Hub. ARCHES since announced it would pause activities in response to the funding cut, and both hubs formally appealed the decision by DOE, with timelines and details unclear at this time. It is also unclear which projects will be financially viable to move forward without federal support, with more clarity expected to come in future quarters.

Carbon Management

Actual Q4 investments totaled ~$119 million, zero announced investments.

Q4 actual investments increased by ~$1 million compared to Q3. Supportive state policies coupled with the federal 45Q tax credit incentives and efficient Class VI permitting may attract and unlock more carbon management investments across the country. For example, California enacted legislation (SB 614) that authorized the development of dedicated CO2 pipelines and geologic storage, aiming to boost the state’s carbon capture, removal, and storage market. Within a week, the California Resources Corporation broke ground on the state’s first CCS project with a Class VI permit at the Carbon TerraVault I site in Kern County capable of storing up to 1.6 million metric tons of CO₂ annually, with a total storage potential of 38 million metric tons.

There were zero Q4 investment cancellations.

While there were no investment cancellations recorded by Rhodium Group in Q4, executive actions signaled a lack of federal support for carbon management technologies. Ongoing industry uncertainty continued in Q4 around claiming the 45Q tax credit in light of EPA’s proposed rollback of the GHGRP, which is used to claim the credit. DOE’s October funding cancellations included many carbon management projects and large-scale pilots and demonstrations; these large-scale federal awards were matched with private sector investment commitments, and we may see investment cancellations increase in future quarters if project developers can’t move forward without the federal cost-share.

Sustainable Aviation Fuel (SAF)

Actual Q4 investments totaled $89.1 million, zero announced investments.

Q4 actual investments decreased by ~$56 million compared to Q3. OBBBA’s amendments to the 45Z tax credit, which reduced the maximum per-gallon credit value from $1.75/gallon to $1.00/gallon continued to impact SAF investment numbers in Q4. However, just before the start of Q4, the oneworld BEV Fund was announced by a group of the world’s leading airlines in partnership with Breakthrough Energy Ventures. The new investment fund is designed to address the limited availability and high cost of SAF and advance and commercialize SAF technologies. The fund is led by Alaska Airlines and American Airlines, and provides a positive market signal about the industry’s commitment to advancing SAF despite restricted federal policy.

Q4 investment cancellations totaled $1.8 billion.

Rhodium Group identified two projects totaling ~$1.8 billion in SAF project cancellations in Q4, with 45Z tax credit restrictions being a likely factor. Velocys canceled its $308 million plans for the Bayou Fuels Sustainable Aviation Fuel (SAF) refinery in Natchez, Mississippi. Shell also canceled a $1.47 billion SAF and renewable diesel project in Louisiana. Without sufficient federal policies and incentives, SAF project cancellations may continue or even increase in future quarters.

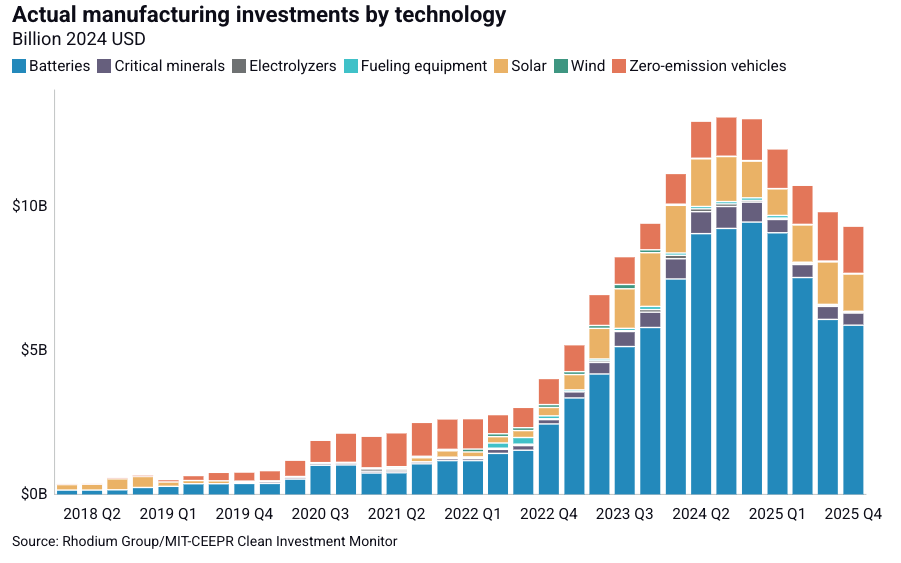

Manufacturing

In Q4 2025, Rhodium Group data analysis shows actual manufacturing investment (vs. announced) totaled $9 billion. Battery manufacturing investment, a key part of the EV supply chain, made up the majority of actual investments, totaling $5.9 billion, followed by zero emission vehicles and solar.

Figure 3. Clean manufacturing investment

In Q4 2025, Rhodium Group analysis identified five projects totaling ~$8.4 billion of manufacturing sector investments that were canceled, all in the EV supply chain and prior to project operation. Legal and logistical challenges, local opposition, and lack of demand contributed to these cancellations, in addition to shifting federal incentives.

For example, Ford Motor Company announced a major EV pivot in Ohio and Tennessee in Q4. Ford is foregoing its plans to manufacture electric pickup trucks at the Tennessee Electric Vehicle Center and instead will produce gas-powered truck models at the renamed Tennessee Truck Plant. Instead of manufacturing electric vans at Ford’s Ohio Assembly Plant, they plan to manufacture gas and hybrid models. Q4 project cancellations also included ICL Group’s $500 million battery plant in Missouri, after DOE announced they were revoking federal cost share for the project – just one example of how loss of federal support translates to loss in private investment.

Check back next quarter to see how federal and executive actions have impacted projects across the U.S. and visit CATF’s clean energy investment tracker. Read the 2025 Q3 analysis here.