Is there a better approach to electricity reliability in Europe?

Europe is facing several challenges: high gas prices and fuel import security risks, aging firm capacity necessary for electric reliability, and a lack of incentives for clean firm power portfolios. As a result, most of Europe’s security of electricity supply planning relies largely on paying gas power plants to provide dispatchable back-up capacity. Moreover, European mechanisms are fragmented and poorly coordinated across borders, resulting in inefficiency across the continent.

One potential tool available to policymakers is capacity mechanisms. Capacity mechanisms are designed to ensure sufficient generation capacity is available to meet peak electricity demand and have grown increasingly important across Europe. Once viewed primarily as a last-resort measure, capacity mechanisms are increasingly becoming a structural feature of electricity market design in many European countries, a shift reflected in the EU’s 2024 electricity market design reform. Despite this, capacity mechanisms remain fragmented, largely fossil-dependent, and poorly coordinated across borders. Can Europe design capacity markets that deliver both reliability and decarbonisation?

Recent analysis from The Brattle Group and Compass Lexecon, both commissioned by CATF, as well as discussions with leading European energy policy experts, points to a clear answer: enhanced and coordinated approaches to security of supply and carbon-free energy procurement can reduce costs, enable cross-border trade, and accelerate the energy transition.

What are capacity mechanisms and why do they matter?

Energy market prices often fail to generate the revenue and investment certainty needed to build and maintain power plants that ensure grid reliability during peak demand. This “missing money” problem can have several causes: volatile short-term prices, administrative price caps limit revenue, and political interventions during price spikes that erode revenues and investor confidence. This “missing money” problem is especially difficult for the seldom used but necessary plants that maintain reliability during extreme conditions. Capacity mechanisms address this all by providing an additional revenue stream for generators who commit to being available during times of system stress.

Two main types of capacity mechanisms exist in Europe:

- Strategic reserves contract existing plants to be held outside the market and activated only during scarcity – they minimise impacts on electricity markets and customer costs but typically do not incentivise new investment.

- Market capacity mechanisms, in contrast, procure a defined capacity volume through competitive auctions, providing payments to qualifying generators and potentially driving new investment. These can incentivize new generation, but also subject the entire market to costs set by the marginal provider. Other variants exist, such as reliability options, that include a payback to consumers when prices are high, limiting windfall profits.

The EU Electricity Market Design Reform of 2024 revised several foundational principles governing capacity mechanisms — most notably by removing their previously temporary character. The Electricity Regulation and State Aid Guidelines also established design principles, but significant variation persists in auction design, product definitions, contract lengths, and eligibility rules.

Capacity mechanisms are spreading across Europe, but coordination is essential to avoid a costly patchwork

As renewable generation deployment continues to increase, European policymakers are looking for additional market designs, such as capacity mechanisms, to ensure power systems are reliable when the sun isn’t shining or the wind isn’t blowing.

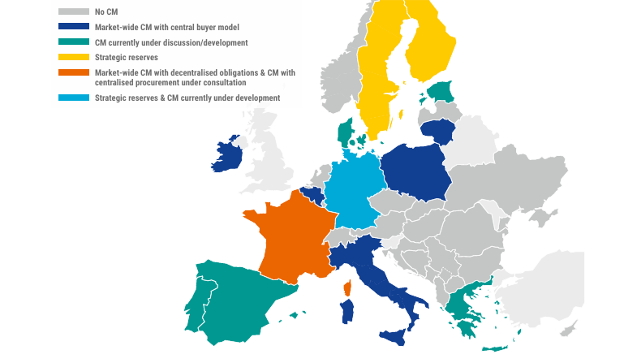

According to ENTSO- E (Figure 1), France, Italy, Ireland, Belgium, and Poland currently operate capacity markets, while Germany, Finland, and Sweden maintain strategic reserves. Meanwhile, Spain, Portugal, Denmark, Estonia, Greece, Germany, and Lithuania are developing or considering new mechanisms. And, according to the European Adequacy Assessment (ERAA) of 2025, Austria, Czechia, Slovakia, Hungary, the Netherlands, and Luxembourg need to develop enhanced security of supply planning to meet projected reliability shortfalls.

Figure 1. Status of CMs across the ENTSO-E membership countries as of 2025

Despite this growth in interest, there is no common EU-wide or regional capacity mechanism supporting reliability across borders.

National capacity planning systematically undervalues electricity imports, leading to over-procurement across Europe. ACER modelling shows coordinated procurement of capacity volumes could reduce additional EU installed capacity needs by up to 70% and 28% of Member State installed capacity on average. Conversely, some countries risk freeriding on neighbours’ investments. Cross-border participation remains minimal, despite the EU Electricity Regulation and the costs of this patchwork are substantial: The 2025 Monitoring Report of ACER shows that capacity auction prices in the EU differ by more than tenfold, and total costs reach EUR 6.5 billion annually – while not even a third goes to low-emission technologies. This patchwork limits cross-border trade and undermines cost efficiency.

There is growing expert consensus that cross-border coordination is essential. To enable it will require comparability between mechanisms, including aligned needs assessments, common scenarios, and consistent derating methodologies. The EU has made progress on efforts to regulate, standardise, and progressively harmonise capacity mechanisms across Member States, setting out foundations for the design and operation of capacity mechanisms, including reliability standards, carbon emission limits, and rules for cross-border participation.

Regional forums like the Pentalateral Energy Forum, which brings together Austria, Belgium, France, Germany, Luxembourg, the Netherlands, and Switzerland, are working increasingly to coordinate adequacy assessments and crisis preparedness across borders. At the EU level, the European Commission’s Clean Industrial Deal State Aid Framework has introduced a fast-track approval process for capacity mechanisms that follow pre-defined best-practice target models, which gently push Member States toward more harmonised designs.

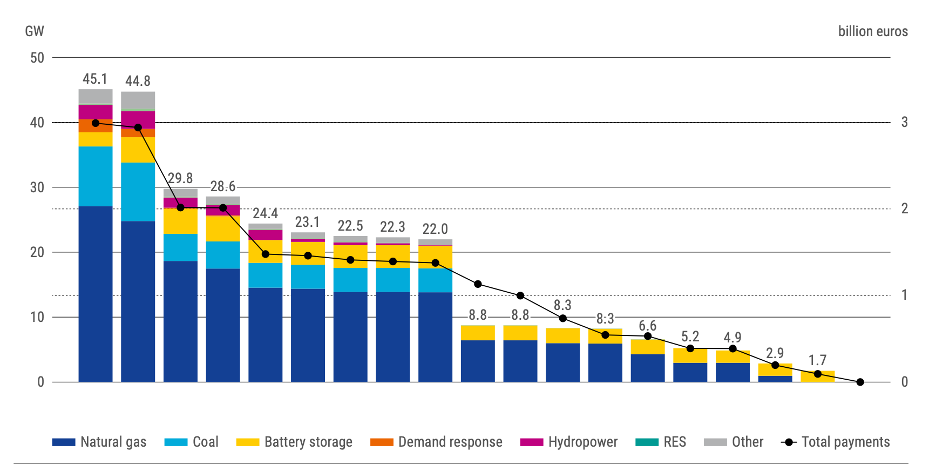

Current capacity mechanisms overwhelmingly support fossil generation. ACER reports that only about one third of capacity support payments go to clean technologies, with gas leading in long-term contracts.

The dominance of fossil generation in capacity mechanisms reflects a chicken-and-egg problem: current capacity mechanism design supports procuring the cheapest firm capacity, which further perpetuates a lack of clean firm incentives that inhibit the development of new clean options that are techno-economically competitive. Clean firm power technologies like nuclear energy and geothermal could not only provide reliability but also strengthen Europe’s energy security via reducing dependence on fossil fuels use in power generation, which would reduce import dependence and cost.

Figure 2: Total payments and capacities awarded long-term contracts under market-wide capacity mechanisms by technology

In fact, the value of gas contracts has doubled from 2024 to 2027 delivery years, while demand response and storage contracts remain negligible. This creates locks in fossil fuel dependence, exposing consumers to volatile LNG prices – which are highly vulnerable to geopolitical tensions – and undermining decarbonisation. If Europe hopes to develop new clean options that can maintain reliability, reduce dependence on imported fuels, and decarbonise, reforms to how reliability is planned and the mechanisms that incentivize firm capacity are necessary.

ACER underlines that, renewable and battery technologies cannot ensure adequacy without complementary resources capable of sustaining output over longer periods. Meanwhile, emerging clean firm technologies such as advanced geothermal, nuclear energy, and gas with carbon capture and storage (CCS) are often uneconomic compared to unabated natural gas or face development and financing hurdles that are not supported by existing capacity mechanism markets.

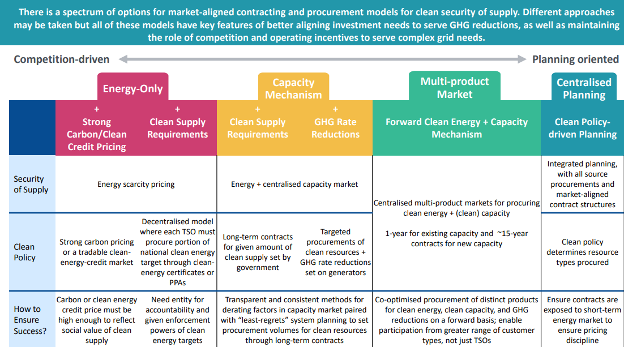

As a recent report from The Brattle Group shows, reforms to capacity mechanism design can improve clean procurement outcomes by drawing on a spectrum of proven approaches (Figure 3). Options range from competition-driven markets to policy-oriented planning, with each model adaptable to national priorities while incorporating best practices for transparency, cross-border coordination, and technology neutrality.

Figure 3: Spectrum of options for market-aligned contracting and procurement models for clean security of supply

How to turn capacity mechanisms into engines of clean firm investment

1. Make capacity mechanisms cleaner

Member States should increase the incentives for and remove barriers to clean energy participation by enabling distributed energy resources, storage, and demand response in capacity mechanisms. Stricter emissions limits or differentiated treatment for clean versus fossil capacity in capacity mechanisms could be used to progressively decarbonise the capacity mix. For demand and storage, aggregation options and flexible service-level agreements can further facilitate participation.

Mechanisms can be designed to embrace technology optionality through multi-year contracts and multi-product procurement that integrates clean energy, clean capacity, and emissions reductions. International models such as Mexico’s Forward Clean Energy Market concept provide useful blueprints.

Additionally, Member States should consider adopting reliability-focused clean capacity procurement targets in addition to existing energy-focused targets, which would incentivise procurement of clean firm generation technologies.

2. Commercialise new clean firm options

If Europe’s capacity mechanisms are to become genuinely cleaner, more commercially available clean alternatives to coal and gas must exist. Clean firm generation technologies, including advanced geothermal and nuclear energy, can deliver dispatchable, low-emission electricity regardless of weather conditions. Not only can these technologies provide reliable power generation, modeling shows they are essential to lowering the costs and total buildout scale of the energy transition.

Without clean firm technology options, capacity mechanisms will continue to largely default to gas. To commercialize these technologies, policymakers will need more than capacity mechanisms to overcome financing barriers. Innovative contracting structures, such as tripartite agreements involving governments, suppliers, and off takers, can bridge the gap by providing revenue certainty for developers beyond what capacity markets provide while allowing buyers to hedge long-term costs and governments to manage ratepayer risk.

3. Improve the transparency and consistency of capacity derating

Capacity derating factors – translating installed capacity into reliable deliverable capacity – should be consistent and transparent across Member States. The methods used to derate technologies must better capture what resources can do for the system across all hours and weather scenarios, including extreme events, and incorporate new performance data quickly. For storage, duration matters: 8-hour batteries contribute significantly more to reliability than 2-hour ones. Regionalised, consistent derating approaches will be necessary to enable cross-border trade.

4. Co-optimise adequacy and flexibility procurement

Adequacy and flexibility are increasingly interdependent but typically procured separately. Member States should move toward co-optimised procurement using a single clearing mechanism that jointly minimises costs while meeting both needs. Where this is not feasible, separate products can be defined within one contracting framework with technology-specific derating for each dimension. Great Britain’s standalone flexibility procurement for long-duration storage offers a useful precedent.

5. Harmonise capacity mechanism design across the EU

Cleaner national mechanisms are necessary but not sufficient – they must also converge and prevent potential market distortions. The current patchwork of diverging designs prevents cross-border competition and drives up costs for consumers across Europe. The fast-track approval process for capacity mechanisms, introduced by the Clean Industrial Deal State Aid Framework (CISAF), adopted by the European Commission in June 2025, is an important first step towards harmonisation. Going further, the EU should work toward a common capacity product definition, consistent derating methodologies, and aligned auction processes. This does not require a one-size-fits-all mechanism, but it does require enough common ground for capacity resources to compete across borders on a level playing field.

6. Move toward regional capacity procurement

Harmonisation opens the door to the biggest prize: regional procurement. In highly interconnected regions, regional stress events are more relevant for security of supply than national ones – procurement should reflect this reality. When each country dimensions capacity needs in isolation, they risk systematically over-procuring – ACER’s modelling shows coordinated approaches could cut additional installed capacity needs by up to 70%. The Florence School of Regulation suggests a phased path forward : first, make cross-border participation in national mechanisms meaningful through better transmission system operator collaboration and more consistent methodologies; then, enable generators to compete across borders in common auctions; and ultimately, define procurement volumes cooperatively at the regional level to capture the full benefits of Europe’s interconnected system.

Looking forward

Capacity mechanisms are here to stay in Europe’s electricity market, but it remains to be seen whether they will remain a fragmented, fossil-heavy patchwork or evolve into coordinated, clean instruments serving both reliability and decarbonisation. Harmonisation saves money, coordination reduces over-procurement, and deliberate design can steer investment toward the clean firm resources Europe needs. Regardless of progress on capacity mechanisms, Europe will also need to develop complementary policy to quickly advance clean firm technologies to be ready to lower the costs of decarbonizing reliably. As new mechanisms are being designed across the world, European policymakers should seize this moment to build a capacity framework fit for a decarbonised, reliable, and affordable electricity future.